All Forum Categories

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

All Forum Posts by: Andreas Mueller

Andreas Mueller has started 49 posts and replied 177 times.

Post: Should you Rent or Buy?....How about Both! (Yes it's possible)

Post: Should you Rent or Buy?....How about Both! (Yes it's possible)

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

@Steve Vaughan, Love it. Im sure there were some amazing stories in the TP :)

Totally, house hack anything, especially something nice is the path. Good Luck up there in WA! If you ever visit Nashville let me know.

Post: Finding deals and my real estate journey

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Helen, just wrote a post on this very topic. May be helpful!

https://www.biggerpockets.com/forums/921/topics/1170425-shou...

-Andreas

Post: Should you Rent or Buy?....How about Both! (Yes it's possible)

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

And share your barbarian rehab stories!

Post: Should you Rent or Buy?....How about Both! (Yes it's possible)

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Hello all my BP Compatriots!

Welcome to my weekly a real estate investment article, coming at you live from Nashville, TN, where I do a brief, hopefully insightful, dive into real estate and financial markets, for all you tubular dudes and dudettes out there.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Main Story: Is it Better to Rent or Buy? We Calculate the Answer!

- - The Bottom Line

- - More Positive Economic News. The US added 353k jobs (seasonally adjusted). Unemployment unchanged at 3.7%. Wage growth continued higher, hourly earnings were up 0.6% in January, which is a 6.8% annual rate. That is a big number, and is higher than pre-COVID numbers. This, after last weeks’ 2023 GDP print. (BLS).

- - Office Building Conversion. A record number of office buildings will be converted into apartments in 2024 (NYPost).

- - US Consumer Credit Card Debt Hits Record. (YahooFinance)

Today’s Interest Rate: 6.96%

(☝️ .21% from this time last week, 30-yr mortgage)Not much happening with interest rates this week, they remain range-bound near 7%. High. This begs the question, with rates so high….

…Is it “Better” to Buy or Rent your Home?

Let’s get into it…

This is obviously an aged-old question. Whether it’s 1954 or 2024, it’s never been particularly easy to save-up a pile of money to buy a home. We all have to rent at some point, or stay longer in mom and dad’s home, as is common in many Asian and… Long Island cultures. Or, option 4, go full barbarian. (Keep reading).

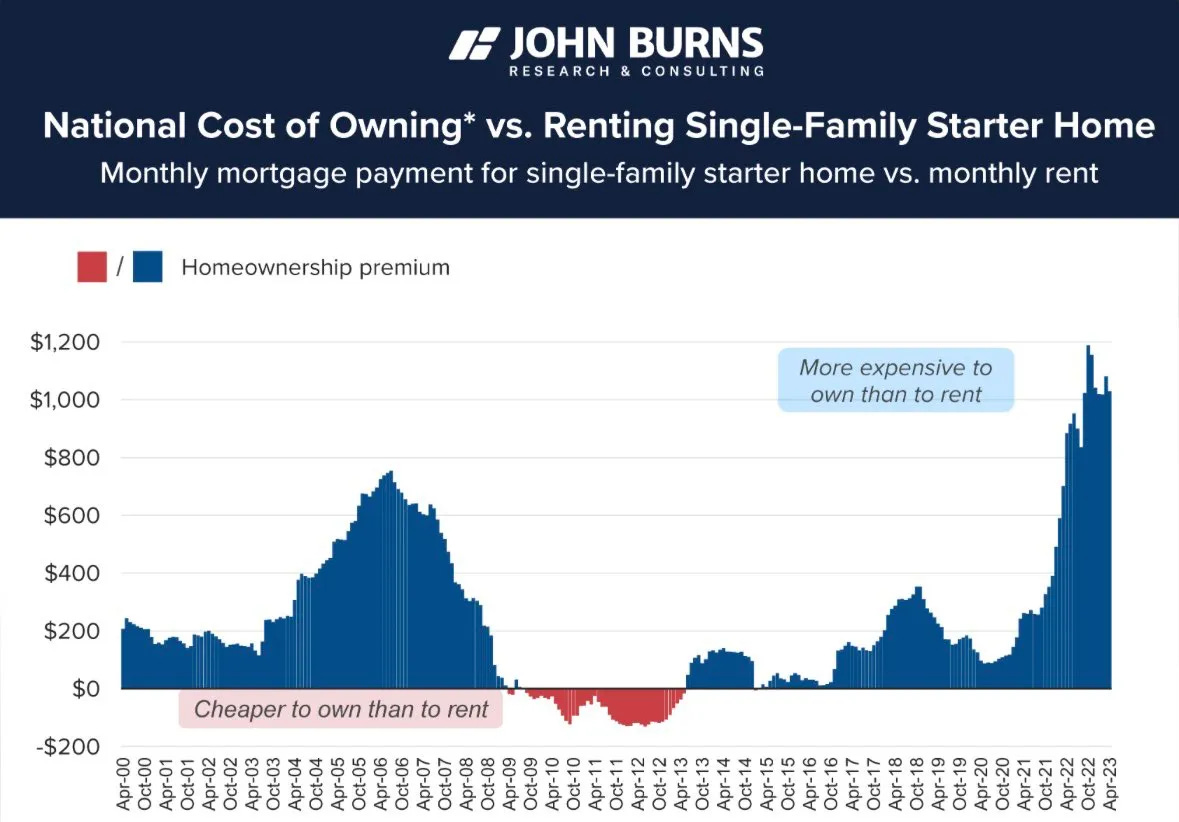

How “expensive” is it to rent vs buy? According to John Burns research, interest rates have made it just too “expensive,” in general, to own vs rent.

According to Redfin, demand for large rental apartments and houses is climbing, one in five millennials who responded to a 2023 housing survey believe they’ll never own a home. Nearly half said it’s because homes are too expensive or they can’t afford to the down payment. But others just prefer renting: 12% said they aren’t interested in homeownership and 7% said they don’t want to put in the effort to maintain their own home. As a result, Redfin expects prices of large rental units to climb next year as supply fails to meet demand, but smaller rentals may drift slightly lower because there are more of them and a backlog waiting to hit the market.

So what should we do? Rent or buy? Well the answer is….it depends. It depends on your goals, are we speaking strictly financially? Do you like owning something? Or just running around the (secluded) yard naked?

Let’s dive in.

In my humble opinion, I say it’s virtually always a better financial decision to own instead of rent. This is because of all the additional ways we are growing our wealth when we own real estate assets, much like owning other assets like a small business. In fact that’s how I look at home ownership/owning real estate in general.

Let’s do some quick math. Don’t worry, I’ll keep it light. This is rough math so don’t get cute and tweet at me all the little things we don’t account for. This will be very close approximation, with some assumptions, like insurance and property tax costs. For those I’ll be using average costs to fill in the blanks and borrowing from costs in my home city of Nashville, TN. We also assume this is your primary residence, not an investment property (much more on that below).

Renting Your HomeAccording to the above research, the average premium for home ownership, given the high interest rates, is about $1000, meaning, ostensibly, that the cost to own the home is $1000 more / mo than it would be to rent it. This number seems extremely high to me, but we will use it as an average to remain conservative. This means the rent for the same average home of $417,700 would be $1636.

Saving the 20% $83,400 downpayment, let’s say you invest that instead in the stock market and make 7% avg. returns. At the end of the year you have made $5838 on that money. Your total housing costs were $19,632. Net, this is $13,794.

After 10 years - The Net Wealth Effect of RentingBut, what about after 10 years? The 10yr net wealth effect of renting a home and saving your money is: $-73,841.15. In other words, you will have made $80,660.42 in gains from your investment of the original down payment + the original capital from your down payment, and paid $237,910.57 in rents, for a net total wealth effect of $-73,841.15, from renting. All other things equal.

- Savings invested Total Value - $164,060.42

- Rent Paid - $237,901.57 (yuck!)

**Assumes rents increase 4.2% on average each year (Rents inflated 6.2% last year but we will use the historical average).

Owning Your HomeThe average home value in the US is $417,700 (Fed). A mortgage on that home would be roughly $2636 (including taxes and insurance). This means your annual housing costs would be $31,632 /yr.

Now, owning a home means you own an asset, so this asset will naturally appreciate. The historical average natural home price appreciation is 5.4%. (CoreLogic, since 1992).And each month you actually pay yourself; a portion of the mortgage payment goes toward paying down the loan you took out to buy the property. And this amount increases over time as a % of the mortgage.

After 10 years - The Net Wealth Effect of Owning

After 10 years - The Net Wealth Effect of Owning

But, what about after 10 years? The 10yr net wealth effect of owning your home is: +$103,687.09. In other words, after 10 years I have $103,687.09 in positive wealth, all other things in my life being equal.

- Equity (wealth) I own in home - $420,007.09

- Home’s value after 10 years from Natural Appreciation ($706,757.76) - original loan amount ($334,160) + Principle Pay-Down ($47,409.33)

- Mortgage costs paid - $316,320.

So without doing really anything in either scenario - no crazy financial engineering or value boosting home remodeling etc… - what is the best financial decision? In 2 words:

Owning > RentingLooks like home ownership wins, and it ain’t close. The real force at play here is that while you start with a lower rent amount vs mortgage, both rent costs and home values are inflating, yet the basis for the home inflating is much much greater, so it compounds at a much faster / larger clip. Add to that the principle you are banking away each month and the tortoise becomes the rabbit pretty rapidly. (er or vice versa? anyway….)

What’s more, we didn’t even talk mortgage interest rates coming down! These calculations assume interest rates remain at 7%. What if you refinance in year 2 to 6% or 5% in year 3? etc… For brevity, I’m not going to calculate all scenarios but it would obviously much improve the home owning scenario. Mortgage interest rates coming down would be a big deal.

But Wait, There’s More….We have forced appreciation, that is forcibly appreciating the value of the home through a renovation / property improvements. What if, in addition to the above, you decided to spend $30k on a modest renovation of 2 bathrooms in your home? And let’s assume, IMO conservatively, that you will realize a 50% return on that investment in the value of the home. So the home is now worth $45k more in value? Well, congratulations you gained an additional $15k in equity / wealth. Forcing appreciation to a home you own is unique to home ownership, can’t do that as a renter. Pretty cool!

The X-Factor to Owning a HomeLastly, the intangible, which is up to your personal preference and lifestyle. Many of us, just love owning the home. We can do (pretty much) what we want and don’t have anyone telling us what to do. Want to get a dog? You get that pound pup. Want to compost in the backyard and add some raised garden beds? Time to get dirty. There is an emotional aspect to consider.

Do you like working on your home? We have seen that you can add tremendous value through a renovation. And if you do it yourself, at a discount to having to hire a contractor, well that’s even more $ added to your overall wealth. That’s equity in your pocket.

On the other hand, renting can be a much less stressful option and many folks just like that lifestyle. Have the landlord handle those pesky maintenance issues, roofing repairs, deluge of water coming from the washing machine on the 3rd floor that just exploded through to the kitchen below (yes, this just happened to me in my home. Ah the humanity!) If this lifestyle appeals to you, by all means rent (or find a spouse that is handy :)

Option 4…Do Both! Yes, you can!

Yes it is very possible to do both, and financially, it’s the best option by far.

Here it is…

Rent where you live, and rent-out what you buy. Why? Well, tax incentives for one, which you don’t get when living in your primary residence. Real estate mogul Grant Cardone agrees. If you can stomach his brash and boisterous attitude, he preaches in his books that owning your primary residence is a “trap” and that money is better put to use in buying investment properties and renting where you physically live. And if renting in your area is “cheaper” than owning, more reason to pay rent and have your tenants pay your mortgage. Plus, there are 5 total ways you make money real estate investing that likely make it financially a better choice of where to put your money and are all only available to you if you are renting-out the home. We have already reviewed most of these but there is a new kid on the block, tax depreciation:

- Cash flow + rent increases over time

- Natural appreciation

- Principle pay down of mortgage + increases over time

- Forced appreciation through a renovation

- Tax benefits to renting-out a home:

- tax depreciation (you get to deduct 3.6% every year of the value of the home structure, for 27.5 years!)

- Bonus depreciation

- Cost segregation

- And a few more too….

Bottom Line

People need homes. This issue is not going away. It’s no longer acute, housing supply has now become a chronic issue. Regardless of your perspective on renting vs buying your primary residence, IMO more individuals should become real estate investors. It is a great personal finance decision, and an even better investment decision. Getting involved in real estate investing is also good for humanity. We have a severely limited housing supply and we need every investor we can get to pitch in. After all, the government doesn’t build homes, investors do. IMO we should think about real estate investing as a service to your fellow human, frankly (not to get too sappy / patriotic on you).

But don’t take my word for it. Think about what makes sense for you and yours. Let me tell you a story about the wild decision my dad made.

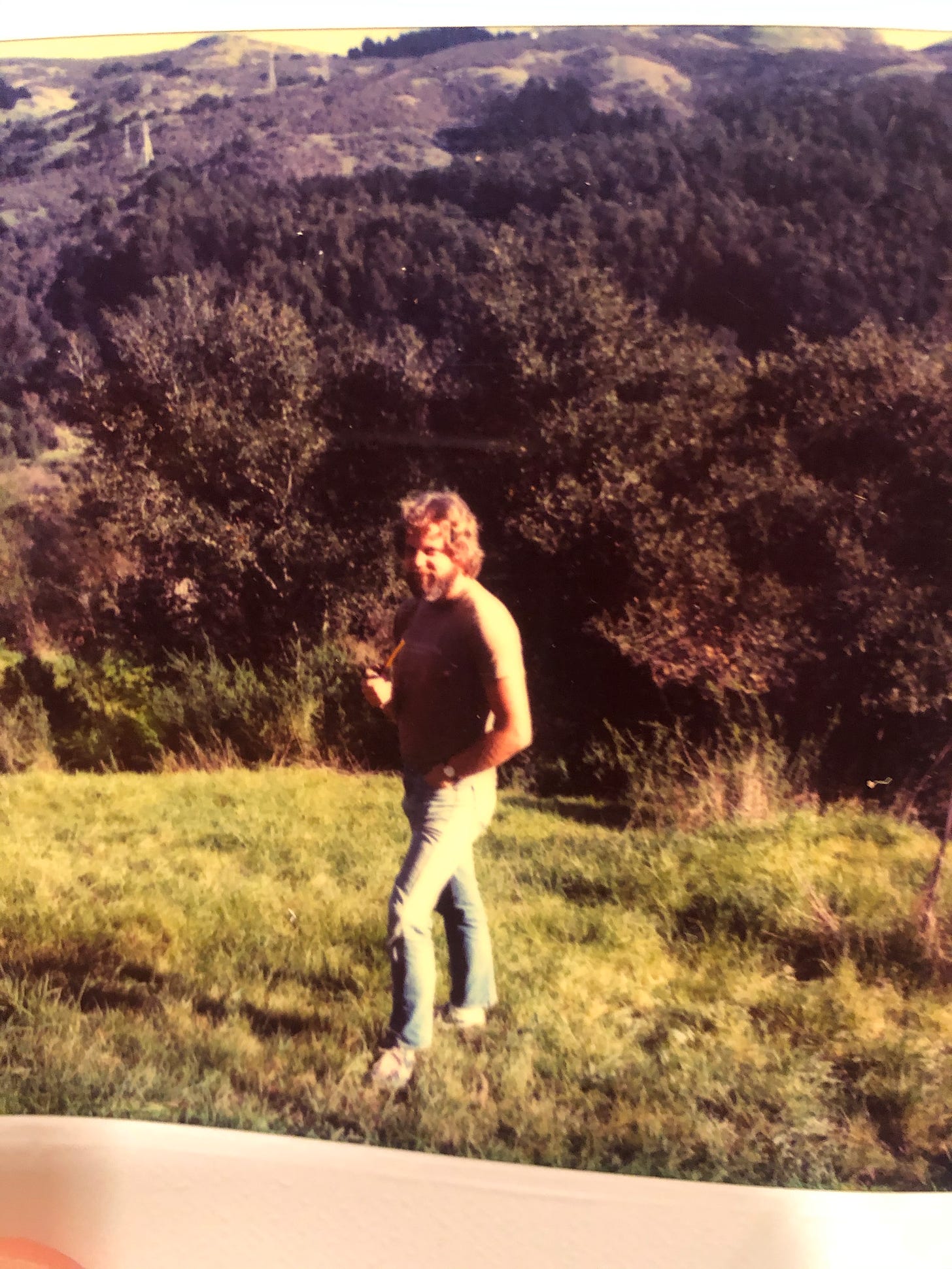

My dad was the ultimate homeowner. In 1976 he bought a piece of land in Kensington, CA for $70k. He built the home himself over the course of 4 years, relying only on a few subcontractors to lay the large pillar foundation into the property’s steep grade. But he didn’t rent an apartment while he built it. No, No… He was a little bit of a barbarian. He slept in a tent in the backyard for 2 years until the home was livable. And when he was done - around the time I was born, after he had built this beautiful redwood and cedar home - we lived in the lower level and he rented-out the main home upstairs! No mortgage, and the rents paid far more than the mortgage and insurance cost.

Do I recommend you do this? Probably not. But maybe you can live through a little renovation on your home, even use some elbow grease to lay down some tile yourself?

I think there is a little barbarian in all of us. Tap it.

And as always…Stay skeptical.

** A Few Assumptions to Note:

- Calculations assumes home values increase on average 5.4%, since 1992. Natural appreciation obviously varies by location, my home city of Nashville rose at 9%. But we used the average to remain conservative.

- Yes, true, I did not take into consideration property taxes and insurance costs inflation. These are hyper local so it’s tough to do in this space, and, importantly, it is likely a small portion of your overall housing payment, relative to the cost of rent or mortgage so even if they appreciate faster than rents appreciate the basis is lower and they won’t catch up to make a meaningful difference in our decision. Anecdotally my property tax and insurance would not have. If you feel strongly, tack on a an extra % to mortgage costs.

- Importantly, there are tax advantages to owning a home. You are able to deduct your property tax and the interest you pay on your mortgage from taxes you owe, this should be counted as income from the asset. This can get complicated and there are limits so consult a CPA. This is not financial advice. I won’t count them for our example but I wanted you to be aware that they exist.

That’s it for this week. If you are interested in digging deeper into any of these ideas or just want to talk real estate investing - which I always love doing - don’t hesitate to reach out. You can message me directly right here on BP!

Again, stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Green Shoots in the Housing Market for 2024

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

BP Compatriots! Welcome to my weekly post on all things real estate, coming at you from Nashville, TN. Every week I bring you a brief, hopefully insightful, dive into real estate and financial markets, for all you tubular dudes and dudettes out there.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - U.S. GDP - Growing Like Micro-Greens ↗️

- - Home Prices in 2024 - Up 5%+

- - Local Market Exam - Nashville, TN

- - The Bottom Line

- - Federal Reserve Keeps Rates Steady in January. Does not yet see inflation under control and may be “unlikely” for March. (@JasonFurman).

- - Egypt, Ethiopia, Iran, Saudi Arabia and the UAE have confirmed they are joining the BRICS bloc of countries, strengthening the trading alliance. Current members are: Brazil, Russia, China, India and South Africa. Argentina declined to join despite the invitation. (Reuters).

- - Mortgage purchase applications fall -11.4%. Small sample and WoW numbers, but something to watch carefully. High rates are still suppressing demand (ResiClub).

Today’s Interest Rate: 6.75%

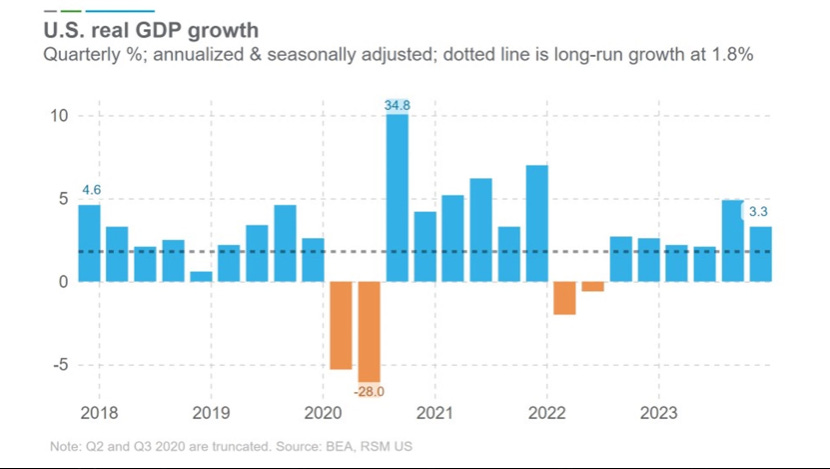

(👇 .17% from this time last week, 30-yr mortgage) U.S. Economy Grew Rapidly in 2023Much of the news coverage this week has focused on the strong U.S. GDP numbers. Rightly so, it was much greener than expected. Let’s dive in.

Year-on-year, the U.S. Economy expanded at 3.1% (2.5% real), significantly above “trend growth” of ~2%. And ended up 3.3% in Q4. Credit where credit is due, the predictions for recession in 2023 were wrong (or pre-mature, which is the same thing). The 400 PhD economists at the Federal Reserve predicted sluggish economic growth, and we ended up growing at 6x their prediction (WSJ). Wowza. What happened, Robert M. Adams? (see my take on risk management at the end of this article).

Perhaps the biggest takeaway is relative growth. The U.S. economy outpaced all other advanced economies last year, and it wasn’t close. You can bet the predictions are going to start rolling in. Already, economists at the IMF are predicting the US to be in pole position in 2024.

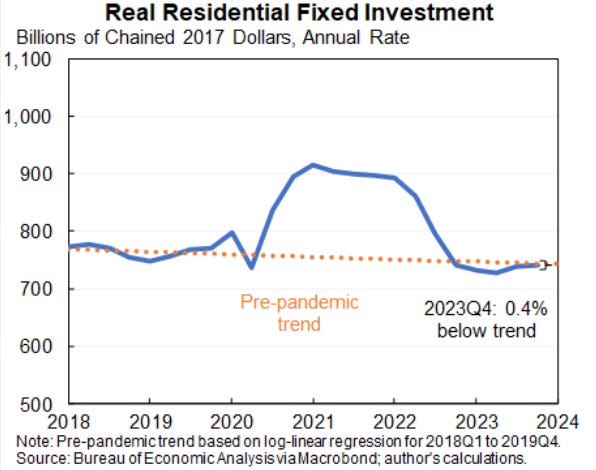

Real Estate Investment: a Weak Point in the GDP Numbers

Real Estate Investment: a Weak Point in the GDP Numbers

One data point I’d like to pull out of the strong GDP numbers is Residential Fixed Investment, i.e. purchases, remodeling of private real estate and equipment (your HVAC system), broker fees etc…owned by landlords and rented to tenants. It’s been paltry, near flat for the last year, after falling 17.4% in 2022.

High rates crushed U.S. real estate investment and led to a housing recession in 2022-Q1 2023. The GDP numbers for 2023 show the housing market is still in recovery.

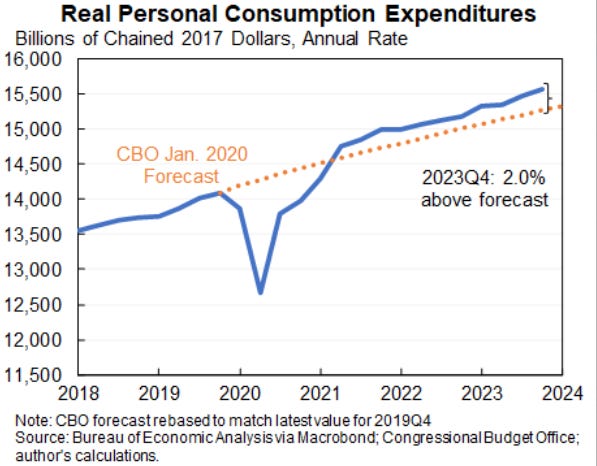

The Fed’s monetary policy has (inadvertently) hyper-targeted the real estate market. Not so much on our Amazon carts Consumers, they spendin, they spendin!

Home Prices

Home Prices

Despite restrictive monetary policy, home prices rose 5%+ last year and are continuing up and to the right. In my hometown of Nashville, we are up more than 9% YoY. This, a result of low supply, again despite high interest rates suppressing demand. Great for homeowners, not so great for homebuyers.

What’s in store for home prices in 2024? Industry analysts are getting more and more convinced it’s going to be a banner year. Both Goldman Sachs and Moodys Analytics just revised their home price forecast model up.

- - Goldman - home prices will be up 5% in 2024, 2.5x+ their previous 1.9%.

- - Moodys Analytics - home prices will be flat, “sideways” for a while, down -.4%, a large revision up from previously -4.4%. This is one of the mroe conservative calls.

- - Altos Research - home prices were up 6-7% YoY in January. And should be up 10% YoY in Q2.

- - Fannie Mae - home prices are expected to rise 3.2% in 2024.

With the supply of new homes, especially the largest cohort - existing homes -remaining low, pent up demand is likely “pent’ing up” on itself. More and more young adults are coming of age, and are ready to start a family, buy a home, and move out of their parent’s future home office. But even with the homebuilders increasing their output, it’s just not enough. For example, in FY2023 homebuilder Lennar increased its deliveries YoY by 10%, to 73,087 homes, and expects to do so again in 2024.

One potential factor is the availability of land for development. “America has a lot of land, local governments have been making it more difficult to obtain development approvals, and also make land expensive to develop.” (John Burns Research)

Thus, home prices in 2024, likely up and to the right.

U.S. Mortgage Interest Rates:With the economy ostensibly humming along, what does this portend for us in the real estate market? How about interest rates? According to oft-cited economist Mark Zandi, “[The Fed’s] got everything they need to start cutting rates…It’s just a question of precisely when.”

Goldman agrees, in its home price revision, the investment bank also now sees mortgage interest rates falling to 6.3% by the end of 2024.

However, when will we start to see rate cuts? IMO we are still looking at a June timeframe. But, regardless of when the Fed cut rates, it may be just as pertinent to think also about how fast. Even if they start in March, how many and at what % will they make said cuts in 2024? IMO, we are likely to see 3 cuts this year (.25% each). It may be until year-end 2025 when we are back to mortgage rates in the 5’s%, which could keep even more young households on the sidelines until then.

So far, the Fed, IMO, likely does not see a cause for easing monetary policy sooner and/or faster. Inflation and unemployment are remaining within the Fed’s preferred ranges. Core PCE inflation is looking decent, running at 2.1% last month and 2.9% YoY. This week’s jobs report shows a labor market in decent health: jobs openings and hiring rates are near the historical average, although trending down. Layoffs were flat in December at 1%. If there is something to watch, it could be the quits rates, which are falling and are now below 2019 levels, a potential signal of a tightening labor market.

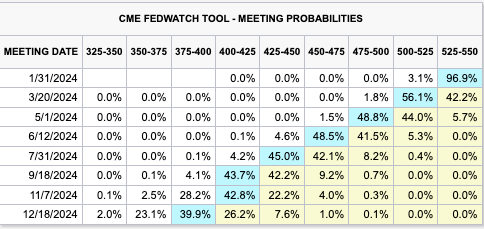

But don’t tell that to the market. Fed Fund futures are now pointing to a 57.8% of a rate cut in March and 94.3% chance in June. Up 10% from last week (CME).

Nashville Market Exam

Nashville Market Exam

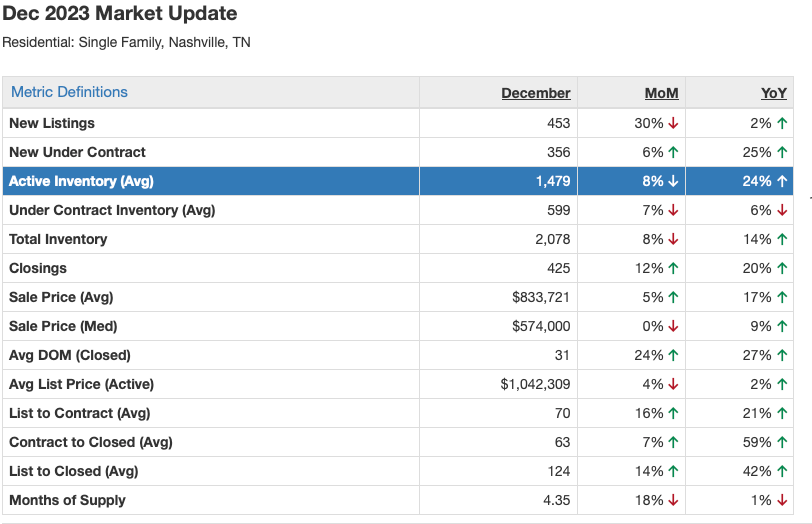

Let’s take a look at a snapshot of the housing market today, to illustrate how the market is doing, using my home market of Nashville as an example:

- - Active inventory is low but much higher than last year, up 24% YoY, indicating strong momentum into the 2024 spring season. Total inventory is up 14%.

- - Home closings are up 20% YoY

- - Sales Price (median) is up 9% YoY

- - Homes are sitting longer, average days on market is 31, up 27% YoY. And the average full listing to closed sales cycle for a home is up 42% to 124 days. Anecdotally I am seeing delayed closings due to loan shopping, tight lending standards and more price negotiating.

What’s next for 2024? MoM numbers are signaling positive results, although 1 month a trend does not make. I will keep a sharp eye out and re-exam the next 2 months, which should give a clearer picture. IMO, supply is just too low and there are too many buyers looking for homes. Anecdotally, I have more investors calling me looking for property than ever.

Bottom Line

At the end of 2022, I counted myself solidly in the bearish camp. I thought we were for sure headed for a recession as a result of monetary policy. I was on tilt. We did get a housing market recession in 2022, but that did not continue into 23’.

Of course, we all can be Eddie Bauer quarterbacks Monday after the Superbowl. Predicting where any market will go is hard. Nay, impossible. Don’t try to do it. Instead, have a plan…I absolutely had more hedges in place to manage my risk at the beginning of 2023, but kept it at that. I didn’t fire sale my property or stock market holdings. [What did I do to protect my downside? You’ll have to take some initiative. Shoot me a note, and ask :)]

And speaking of the stock market, well, it’s wild. Like tiger on the plains of Africa chasing a naked guy with a stick, wild. Which is why I prefer real estate. It’s a relatively stable and reliable market with above average growth and tax advantaged gains. The stock market on the other hand? Well…Fun fact, over the last 30 years, 50% of all returns in the stock market came in just 10 days of trading. And if you missed on the best 30 days in the market, well… your returns would be an astonishing 83% lower. Totally insane. Last year was a banner year. The S&P was up 25%. What about 2024? Who knows. In fact, just this week, JP Morgan called the current stock market similar to the DotCom Bubble. It’s been up up up for a while now, due for one of its cyclical avalanches. But again who knows… That’s why I stay aware, I stay optimistic, and of course…

I stay skeptical.

Most Interesting Tweet(s) of the WeekYou can now get ultra-fast internet almost anywhere in the world, via “space lasers.”

Property Highlight

Moving in Nashville? Check out this must see budget friendly 2 bed / 1 bath close to Vanderbilt in the rolling trees of Green Hills. A Neighborhood. Close to Whole Foods, Trader Joes, Hillsboro Pike shopping and restaurants. This would be the perfect little cottage for Nashville living. $1900/mo.

That’s it for this week. If you are interested in digging deeper into any of these ideas or just want to talk real estate investing - which I always love doing - don’t hesitate to reach out. You can message me direct, right here on BP.

Again, stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: A Skeptical Dude's Market Analysis - January 24th, 2024

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Hello BP compatriots and welcome to another edition on my real estate market analysis, coming at you from Nashville, TN. Every week I try to bring you a brief, hopefully insightful, dive into real estate and financial markets, for all you kick *** dudes and dudettes out there.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Interest Rates: the State of Play

- - Inflation Spotlight: How Auto Insurance Premiums Affect the Housing Market

- - A Skeptics Take: Money Supply Flashing Red Alert

- - The Bottom Line

- - 45% of Real Estate Agents who own their Firms Having Trouble Paying Rent on their Offices (Alignable).

- - US Stock Market Hits Record High. Stocks are continuing their recent advance, with the S&P 500 on track to make its fourth record high in as many days (Barrons).

- - Tens of Thousands in Layoffs already in 2024. eBay, Blackrock, Twitch, Unity, Wayfair, Unity, CitiGroup…(@GRDecter).

- - * Bonus * - Shipping through Panama Canal Plunges Back to COVID Low. $270 billion traffic jam (Bloomberg).

Today’s Interest Rate: 6.92%

(☝️ .15% from this time last week, 30-yr mortgage)Interest Rates: Will Remain Range Bound, until they Aren’t

Following the Federal Reserve’s holiday announcement that their restrictive posture in 2024 will become less restrictive, mortgage interest rates (and Treasury yields) dipped a full 1%. Since then rates have creeped up, likely from lingering inflation / wage growth concerns in the bond market.

Bear in mind, the Fed has NOT yet “pivoted.” Their policies have not yet changed from “restrictive” to “accommodating.” Nor have their policies changed to “less-restrictive.” They have merely begun to look over the horizon, and sometime in 2024 they expect to ease restrictions. They are still in a highly restrictive state. It may not be until 2025 that the Fed considers its policies accommodating.

As the market waits in anticipation for the Fed to act, trying to guess when this may be, rates will likely be volatile, yet range bound. For now, that range seems to be 6.2% - 7% (30yr mortgage). For its part, mortgage buyer Fannie Mae now expects mortgage rates to be 6.4% in Q1 2024 and 6.2% in Q2, down from 7% and 6.8% respectively when it released projections 2 months ago.

Additionally, the spread for mortgage rates above the 10-yr Treasury bond remains historically high and likely will continue to do so until the bond market feels better about inflation (more on the latter, below). Homebuyers have taken some notice. Mortgage applications, while still very low historically, have seen a 3-week positive trend upward and an 8-week trend, seasonally adjusted.

So When will the Fed Cut Rates then?Last week we talked about when the Fed may start cutting rates. At the time, the bond market was pricing in a 97.4% chance of a rate cut in March - and a mind-bogglingly high 6-8 rate cuts in 2024 (though down from 6-9 a month ago). Every meeting a rate cut, on average, and at over 50% chance. We disagreed, saying it was more likely they would start in June. Since then, the bond traders are now signaling that same sentiment.

We are down to a 43% chance of a cut in March and 82% chance in June.

Will the Fed be ‘forced’ into cutting rates? Only if the economy starts to slide, which Bank of America CEO Brian Moynihan thinks may happen, predicting 4 rate cuts this year and in 2025 to “avoid tipping the economy over.”

Counter point: Economists are touting a strong labor market, which is inflationary and will delay interest rate cuts. Wage growth is outpacing inflation across all wage tiers. It should be noted, strong (but not out of control) wage growth is good for the economy, I’m not hoping for doom and gloom. But, we Skeptics always keep an eye out.

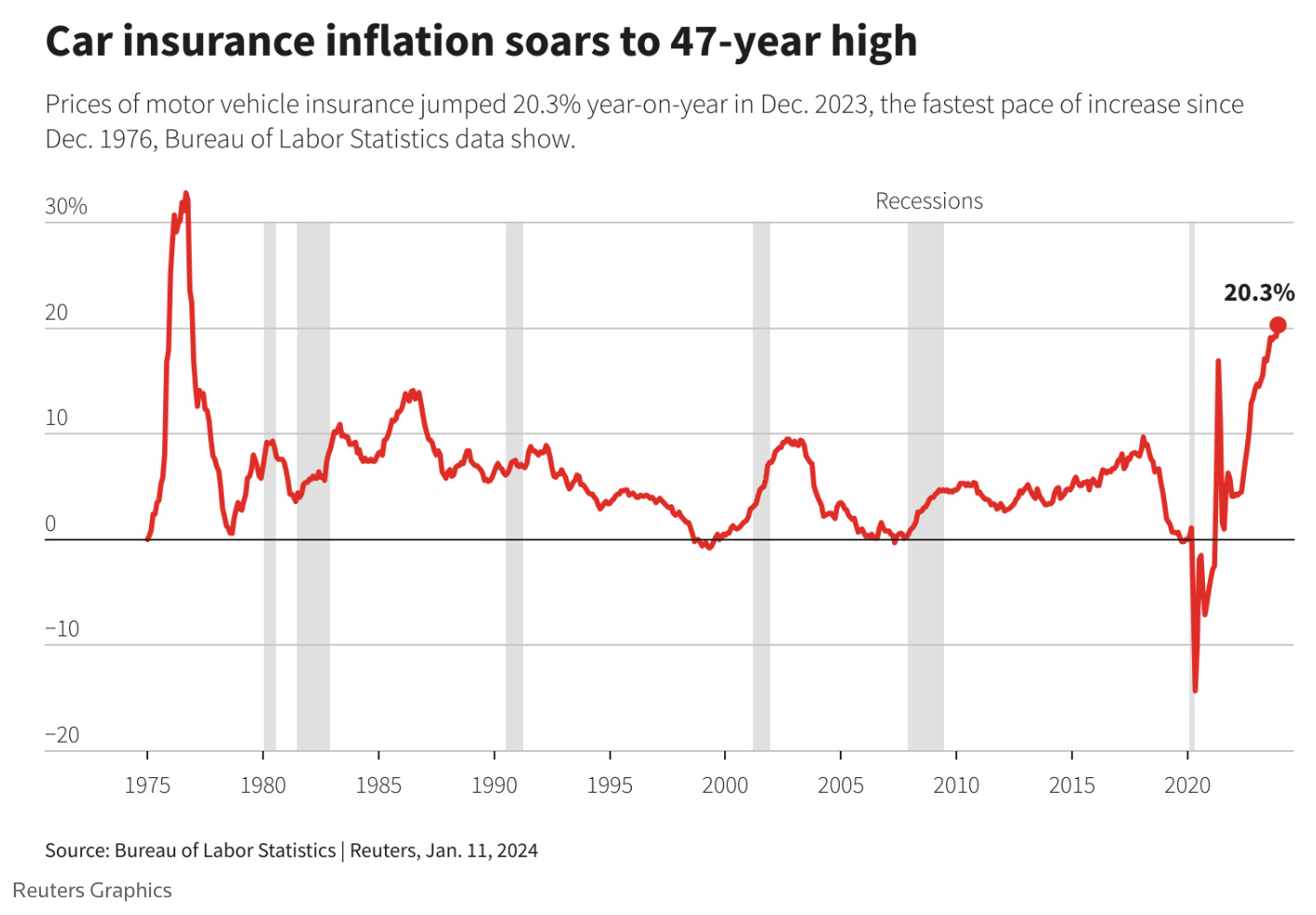

One reason for a hesitant bond market, and thus stubbornly high mortgage to Treasury yield spreads, is inflation expectations. If inflation remains high, even though it has come down from über-high levels, bond yields and mortgage rates will remain elevated. Let’s look at one corner of the inflation front: auto insurance.

Now, we already examined home insurance inflation a few weeks back, and unfortunately, auto insurance premiums are also going wild. For partially the same reasons, like reinsurer costs due to increased disasters - and some new ones.

In short: 2023 saw auto insurance premiums jump 20+%, average premiums are now $2019/yr. The highest levels since the 1970s.

And some industry analysts are projecting premiums to increase another 12.6% in 2024. Hopefully this doesn’t affect my late-night Uber ride? 😬😬😬 (it will).

And watch out on the road folks, in 2023 5.7% of households didn’t have car insurance, up 8% YoY.

Why this Matters for Real EstateIndirectly this is a signal of overall stubborn inflation; directly, this does matter for the real estate industry. Why? Insurance markets are submarkets of the larger US economy. Higher auto insurance premiums result, assuming no foul play, from underlying costs increasing, such as from higher manufacturing costs, which mean manufacturing costs for other things like building materials are also likely to go up. Same with labor costs. Case in point: auto repair costs (parts & labor) were up almost 20% YoY, and cars are more expensive to replace in today’s market. The average new car costs $48,759. And, don’t blame ‘expensive electric vehicles’ for increased premiums (not that I care either way, but I hear this argument a lot). In 2023 the average electric car became cheaper than the average new gas car. For example: A new Tesla Y (the best selling car in the US and the world) is $3,700 below the average auto price of roughly $48,759 (Bloomberg).

Exogenous side effects can also affect both auto insurance, and….home values! For instance, higher car theft in an area/zip/city can be a factor in depressing home values. In 2023, auto were up ~34% in 2023.

Personal Anecdote: I just exited my last property investment in DC in the fall - a large renovated, yet typical, DC row-house I was renting out. I noticed home prices stagnating in my zip code, deteriorating tenant application quality and more and more anecdotal crime stories from my tenants and neighbors. My skeptical mind was flashing its Spider Senses. Was I crazy to leave a “growth market?” Then I saw this just the other week: “There were 6,829 thefts of motor vehicles last year — [a whopping] 82% increase from the previous year. In the first four days of 2024, 53 cars have already been stolen.” According to D.C. police data.

Holey moley! Everything is intertwined in our economy. Gotta keep your head on a swivel dudes and dudettes.

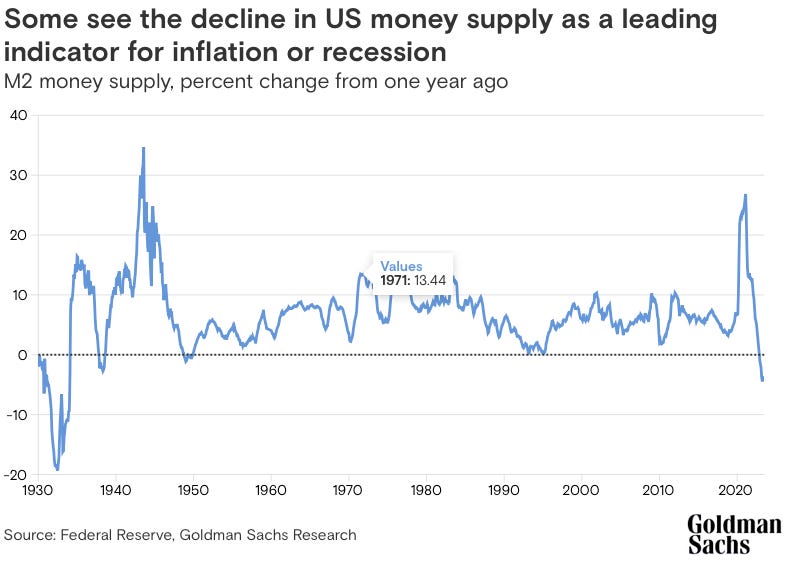

A Brief Skeptics Take: Money Supply Flashing RedOne historically significant indicator of potential recessions, the rate of change in the supply of money whirling around tin the economy, or M2, is officially flashing red (see M2 explanation here). In 2023 M2 declined by 2%, one of the largest annual declines on record. Rapid M2 declines have always signaled a recession is ahead (or happening).

Same is happening in the U.K. M2 plummeting.

Bottom Line

There is reason for optimism on interest rates, as long as the economy holds up, but it will likely be a gradual hike down. Slightly lower mortgage rates will slowly increase demand, accelerating when we get below 6%. Perhaps by Q1 2025. Housing supply main gain over 2023, but will remain lower than demand, propping up home prices.

On Home Prices: As we said last week, the housing market should appreciate more in 2024 than 2023, particularly in growth markets and with rates that likely peaked last year. Zillow, in just the last month, totally reversed its prediction for 2024, forecasting that home prices would appreciate +3.5%, from -.1%. Digging into these numbers, housing analyst Lance Lambert sees the only major national laggareds as the California Bay Area, and much of Lousianna.

Nevertheless, this Skeptical Dude is remaining cautious, a wider mortgage-Treasury bond spread is cyclical and unfortunately usually occurs during periods of economic market stress. I am also watching the M2 numbers like a hawk. An extremely important alert is now flashing in the US and UK, signaling an economic slowdown. Case in point, Goldman Sachs economists recently expressed concern over the labor market, saying, “[there are] three somewhat concerning developments. First, the pace of gross hiring has slowed dramatically .. Second, .. the hiring rate argues for a further drop in job openings in the first half .. Third, .. we find a higher risk of labor market deterioration today than in 2019, with the probability of a 4-5% unemployment rate within twelve months estimated at nearly 20%.” And large financial instututions are shedding employees, nearly 17,000 across Wells Fargo, Bank of America, and Citi (Reuters). Labor markets are the primary data area the Fed is watching to signal if rates need to be cut.

In other words….Stay alert and stay skeptical, all you dudes and dudettes.

Most Interesting Tweet(s) of the WeekWell, despite everything, we could be in this situation….way worse.

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me direct right here on BP.

Again stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Will massive apartment unit growth affect single family home rentals?

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Welcome BP compatriots! Another installment of my weekly brief, hopefully insightful, dive into real estate and financial markets, for all the kick *** dudes and dudettes out there.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Interest Rates: What to Expect?

- - Housing Prices and Supply: Effects from Massive Apartment Unit Growth

- - Tangent Alert! Cancer Rates are up since 1980 at an alarming rate. The cause? Likely the food companies adding sugar / crap to food.

- - The Bottom Line - My Take on Markets

- - Government Releases Experimental “New Tenant Rent Index:” A new measure of rental rates; shows rents are down the last few months. (BLS)

- - 25% chance of Recession in 2024. But economy will likely outperform estimates. (Moody’s)

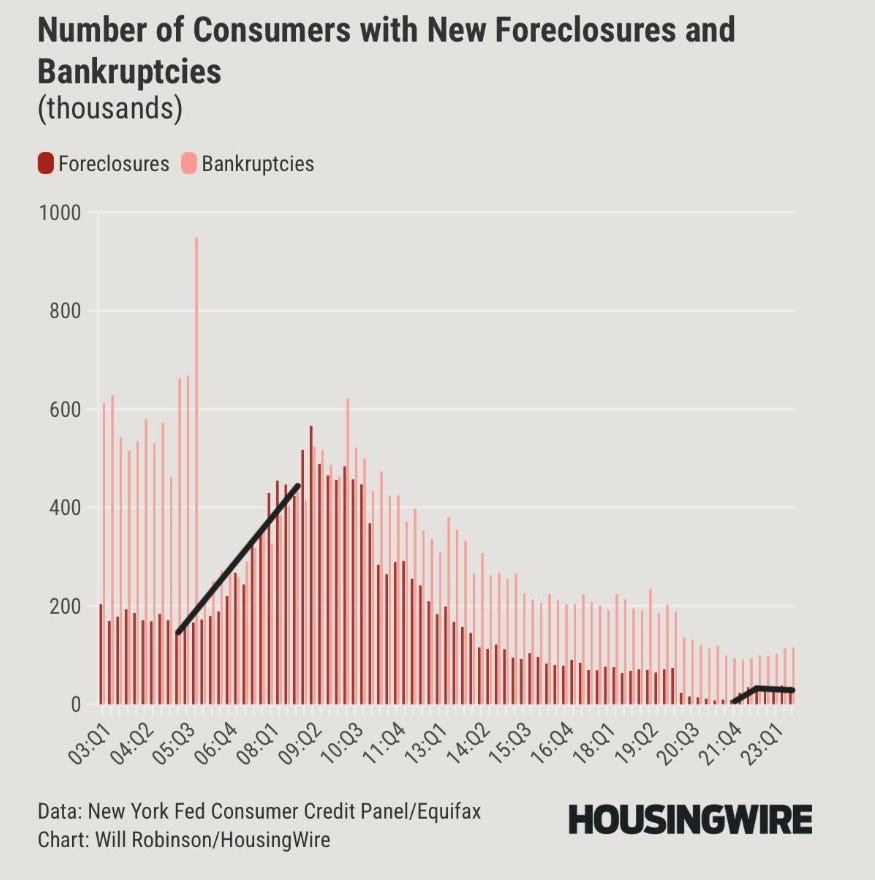

- - Foreclosures and Bankruptcies Remain Low: Be wary of numbers like 700% increase, that’s because they were paused during COVID. (Housing Wire)

Today’s Interest Rate: 6.77%

(👇 .03% from this time last week, 30-yr mortgage) Interest Rate: CPI, Mortgage Spreads…What to Expect?Inflation numbers released last week by the Bureau of Labor Statistics showed that U.S. (CPI) inflation rose 0.3% in December, after rising .1% in November, a touch stronger than consensus analysts’ expectations. Of note, shelter continued to rise in December, contributing over half of the monthly increase (up .5%, and up 6.2% YoY). In aggregate, this puts 2023 inflation at 3.4%. We are staedily coming down, but, IMO, still too high. Adding to this, retail and food service sales released today were up $709.9 billion, up 0.6% MoM in December and 5.6% YoY. Why do inflation and retail sales matter? The Federal Reserve likely needs to see lower inflation to start cutting interest rates in March. Retail sales are an indicator of consumer strength.

IMO: Stronger than preferred inflation data and a robust labor market (unemplyment remaining low / strong consumer) = Fed does not cut rates in March. The Feds rate cutting committee, the FOMC, will remain data dependent, track leading indicators, and will err on the side of being late to cut, rather than early. Nobody can time the market, but my inclination is for a first rate cut to occur in June, 3 in total this year, at 25 BPS each (.25% x 3 = .75% in 2024). This belief is not religion. My opinions are strong, yet moderately held. Make sure to tune in to A Skeptical Dude each week to keep up to date on the market’s latest and get my analysis. You can follow here or here.

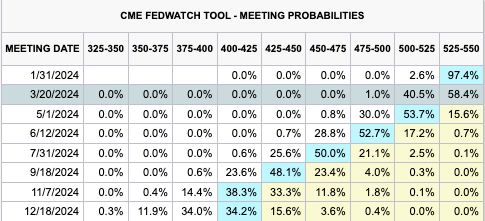

For it’s part, the bond market is still pricing in a 97.4% chance of a rate cut in March - and a mind-bogglingly high 6-8 rate cuts in 2024 (though down from 6-9 a month ago). Every meeting a rate cut, on average and at over 50% chance. What do bond traders know that the Fed doesn’t? Well they just started using computers so… that’s probably pretty neat for them.

What do the Experts / Analysts / Financial Institutions Think?- - Goldman Sachs: “We continue to expect the first rate cut in March, and 5 cuts total in 2024”

- - JP Morgan : Cuts to start “Middle of the year” and then “grinding lower”

in 2024. - - Mark Zandi: 4 rate cuts in 2024. (ResiClub)

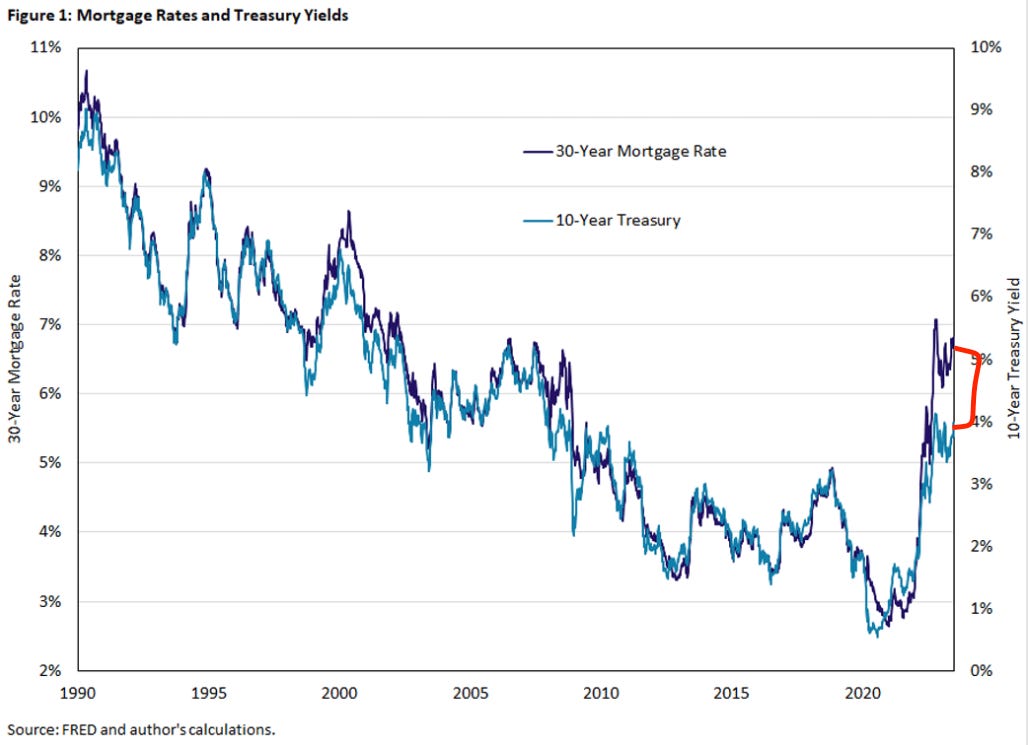

As we have highlighted before, in a normally functioning market, the 10-year Treasury rate closely tracks 30-yr mortgage rates. However, the difference between the two, the Spread, — has risen from 1.70% in January 2022 to 4.108% as of today, while the average 30-year fixed mortgage rate has jumped from 3.22% in January 2022 to 6.77% as of Thursday. The current spread between the 10-yr Treasury and 30-yr mortgage is therefore 2.662, much higher than the historical 1.74.

Why does this matter? If markets were functioning normally, at the historical average spread of 1.74, mortgage rates would be 5.848% today.

The Experts’ Take?

The Experts’ Take?

- - The Mortgage Bankers Association expects spreads to fall to 190 bps, Q4 2025.

- - Fannie Mae expects spreads to fall to 180 bps, Q4 2025.

When will the market for Treasuries and mortgage backed securities normalize, reducing the spreads, and when will the Fed cut rates? IMO, these market mechanics will likely not happen until mid-2024 and even then will likely grind lower, slowly. But combine lower spreads with Fed rate cuts in the witches cauldron and we have an optimistic 12-18 month outlook brewing, it is highly likely that mortgage rates will be lower in 2024 and even lower still in 2025.

***For us uber-finance nerds out there, a good article from the NY FED on understanding mortgage spreads in detail. Its a bit dated but contains a great explanation. And the author has a fantastic name, if I do say so myself :)

Home Prices in 2024? Likely continue up.Since the housing sector slipped into recession in the second half of 2022, after seeing a wild run-up in home prices during the COVID housing boom, prices are up. Most local markets bottomed January 2023. Depending on the data you look at, 2023 saw home prices rise 3% - 6%, near-ish the historical average. Of course, all real estate is local. In my home market of Nashville, we are up 9% since December 2022.

What am I thinking for 2024 & 2025?5% home price appreciation is a solid conservative number, for 2024 and 2025. In my opinion, higher interest rates are still throttling housing prices, keeping demand on the sidelines, especially for the newest, largest generation who are now looking to form a household and move out of mom and dads (or their 8 dude group frat house, said my 26 year old self). Home Prices in growth markets (Nashville, Dallas, Tampa etc…) will be higher in 2024. And every day rates & prices remain high, the number of homebuyers standing on the sideline, just waiting for the coach to put them in the game, builds and builds. When rates decrease and folks feel like they can pull the trigger, expect prices to punch up, likely 2x the current rate. IMO.

What about supply of available homes? Is there hope?

There just aren’t enough homes for folks to buy. The mortgage rate shock of the last few years didn’t = increased supply of listings. This is because 2 main sources of supply were/are being suffocated: 1) existing owners who were/are locked into 3% mortages, and 2) delinquencies/foreclosures which were/are still very low. Anyone who was at risk of foreclosure was likely able to sell their home for a positive gain pre-foreclosure. And 3), while new construction supply did increase, it’s still a minority of overall sales and not enough to move the entire market.

As you can see, builders did jump head first in to the market, when housing demand boomed during COVID. But we are now flat, and were underbuilding for years. Keep in mind it takes a while to build a house (2-3 years from start/land/permiting to finish).

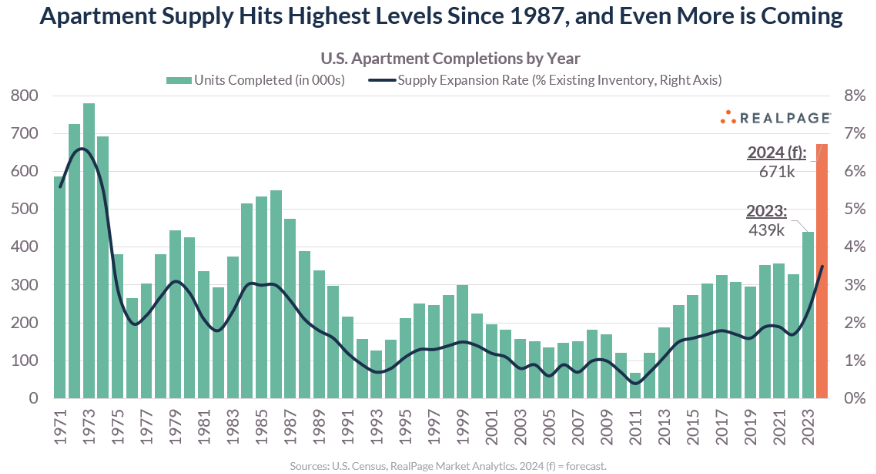

Housing Growth: ApartmentsOne important note: overall housing may not see an insignificant (but not sufficient) increased supply in one sector: multifamily apartments. While not exactly the ideal single family home you can purchase for your family/investment, it will put pressure on shelter prices. The catch? The pipeline of apartments coming on the market is spiking in 2024, but will plummet in the coming 2 years. Let’s review:

New apartment supply was at its highest level in 2023 (since 1987), more than 439,000 units came to market. “Here's the intriguing part: Last year was just the warm-up act,” says housing analyst Lance Lambert. According to forecasts from @RealPage property management, 671,953 apartment units are projected to be completed in 2024 (the highest since 1974).

While this is only about a 3.5% increase to overall apartment numbers, this should have an affect on apartment rent growth, or even rent declines in the sector (RealPage). “Most of the multifamily supply expected to come online this year will be in fast-growing Sun Belt markets, including Nashville, Austin, and Dallas.” Interesting. Since I’m on the ground in Nashville, I have to comment. Strong apartment growth here has not translated into lower rents in the single family or small multifamily sector here; in fact, quite the opposite. Home rents are appreciating more than inflation, particularly as home ownership costs such as insurance and building materials increase. For it’s part, Invitation Homes, America's largest single-family home landlord, saw the same in 2023, reporting a 6.2% increase in single family rents. Of note: I am only talking about single family or small multifamily (2-4 unit) homes.

2025 is a Much Different Story for Apartment Construction.

2025 is a Much Different Story for Apartment Construction.

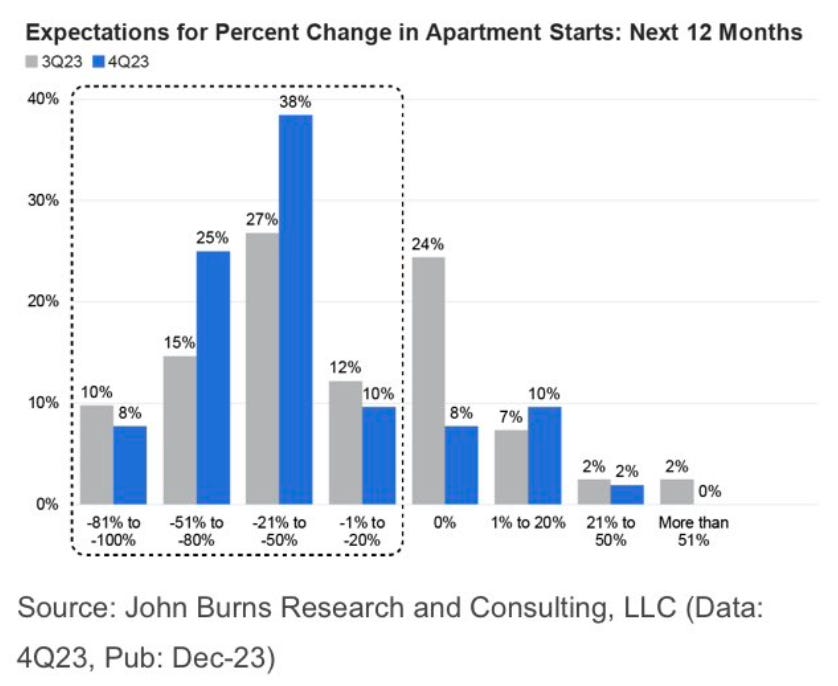

According the RealPage, “the [2023-24] wave of supply is resulting from construction starts that began back when rent growth and occupancy rates were at/near record highs… and consequently, [apartment] starts have plunged. Supply will drop way off in 2025-26.” One-third of apartment developers surveyed in December expect new apartment starts to fall by more than 50% over the next 12 months, up from 25% when they asked 3 months ago (John Burns).

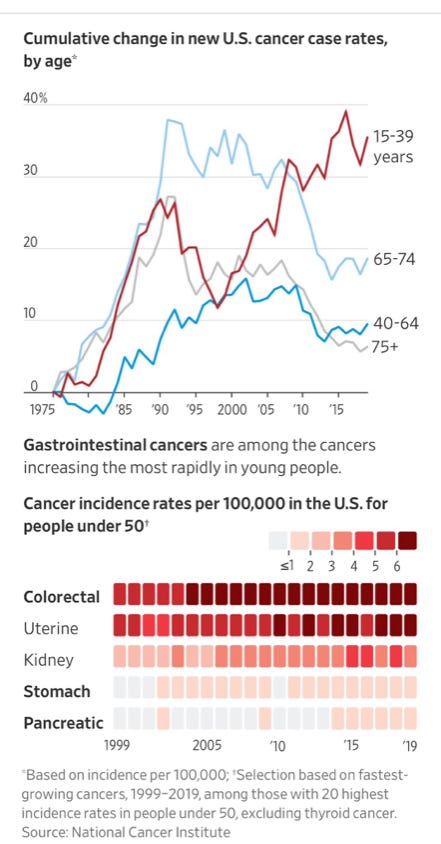

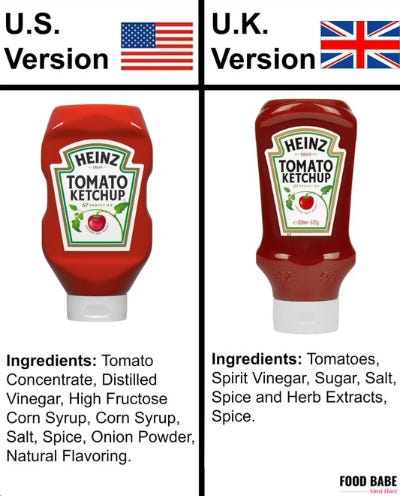

* TANGENT Alert - U.S. Cancer Rates are Drastically Higher sine 1970s -Why? Food Companies are Roofying our Food with Sugar.

* TANGENT Alert - U.S. Cancer Rates are Drastically Higher sine 1970s -Why? Food Companies are Roofying our Food with Sugar.

We’ve been duped for decades about food: Turns out sugar isn’t benign. It’s the real poison. Fats aren’t actually bad. They are essential. Carbs aren’t terrible. Sugar activates cancer mechanisims (NIH). There are now 250+ names for sugar, to try to “trick” folks into thinking it’s not in our food. I can’t recommend this discussion with Neuroscientist Dr. Andrew Huberman and Endocrinologist Dr. Robert Lustig. The clinical data is out. Sugar (especially w/o fiber) is poison.

Cancer in the areas of the body that process sugar and produce / affect insulin are up in a way that is endemic.

Why do Americans have a particular propensity for obesity / cancer? It’s our food. Let’s take ketchup for example. Now, this food is usually always high in sugar BUT just look at the extreme difference. Same company, “same product.” Ever been to Europe? Folks are not as overwight as in the US, and the sad thing is that it may not be our fault.

Sorry, got on my high horse right there. I digress….

Bottom Line

There is reason for optimism on interest rates. All this being said, this Skeptical Dude is remaining cautious, a wider spread is cyclical and unfortunately usually occurs during periods of financial market stress, such as when the economy slips into a recession. And spreads could be wider for longer than the market is planning for. One of the reasons spreads will remain elevated is MBS investors don’t want to buy, concerned that future lower rates will result in refinancing of mortgages to lower rates, a risk for these investors called early prepayment. MBS investors want to see refinances (prepayments) slow. Thus Skeptics, we should remain cautions of becoming overly bullish by assuming mortgage rates will be lower in the next 3-6 months. Additionally, the Fed stopped buying MBS when they started tightening in 2022, removing a massive buyer from the marketplace.

Further Thoughts: Barring a Black Swan event, the housing market should appreciate more in 2024 than 2023, particularly in growth markets. Falling mortgage rates will (slowly) increase demand, accelerating when we get below 6%. Housing supply will remain lower than demand, propping up prices regardless of rates.

In other words….Stay alert, stay skeptical, all you dudes and dudettes.

Most Interesting Tweet(s) of the WeekOptimistic for 2024, cautious for the next 4+ months. Agree.

AND

Ok, now I want a really potbelly pig...major FOMO.

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me directly on BP! I try to answer all the messages I get.

Again stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Real Estate Market Update: Insurance companies are hiking rates 20%+ in 2024!

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Hello all and welcome to the new year! It's January 10th, 2024 and here is a brief, hopefully insightful, dive into real estate and financial markets.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Interest Rates: Down Sooner, or Later?

- - Consumer Update: What is the Qualified Mortgage and Why Does it Matter for the Real Estate Market?

- - Property Insurance Alert - Many Premiums Increasing in 2024

Today’s Interest Rate: 6.80%

(☝️ .03% from this time last week, 30-yr mortgage) The Weekly 3: Data and News to Keep You Informed- ADUs Gain Momentum Nationwide: Accessory Dwelling Units (ADUs) are growing in popularity, especially with the rise of the work-from-home trend as a way to offset mortgage costs from high interest rates (JBREC)

- The housing market’s ‘lock-in effect’ is very real: Most sellers are buyers, naturally they have to move once they sell their home. 3% interest rates mean they won’t sell until rates come down (Fortune).

- Yellen Declares US Economy Has Achieved Soft Landing: Too soon to declare mission accomplished? (Janet Yellen)

Mortgage interest rates were essentially flat this week, but down 60 basis points (.6%) from last month. As we saw last week, despite interest rates beginning 2023 at 6.2%, housing prices ended up 4.8% YoY in October, according to Case-Shiller. Nov / December numbers are still being tabulated nationwide but this number should hold. And in my home market of Nashville, TN the data is out (thank you real estate license). We were up 8.5% YoY, ~ double. Interest rates are still too damn high for a healthy market, but just like politics, all real estate is local, and certain areas continue to emerge from the 2022 real estate recession nicely. Not everyone can, but those who can afford the higher mortgage are taking advantage of low-er prices today. I.e. if home prices increase 5% as they did last year and the average home in America is now $431,000 - that same home will be worth $452k January 2025. Put another way, those able to buy today will be $21k richer that those who wait. By doing nothing.

My Thoughts5% home price appreciation is a conservative number, for 2024 and 2025. In my opinion, higher interest rates are suppressing housing prices, which are keeping demand on the sidelines, especially for the newest, largest generation who are now looking to form a household and move out of mom and dads (or their 8 dude group frat house, said my 26 year old self).

Case in point, holiday mortgage demand was strong this year. Last week mortgage applications and refinancing demand was up 5.6% and 18.8% respectively (Mortgage Bankers Association).

So where do “the experts” think rates are going from here? We have a super special poll for that. According to the Fannie Mae Home Price Expectations Survey - comprised of 100 experts across the housing and mortgage industry and academia - rates should settle at 5.7%. Hot take, IMO, the “experts” are off. Bond spread regression to the historical mean alone should get us to 5.65%. Once the Fed stops trying the engineer the economy, and cuts rates, I think we settle at 5% or slightly below, in 18 months. Disagree? Feel free to tweet / DM at me! Bring it.

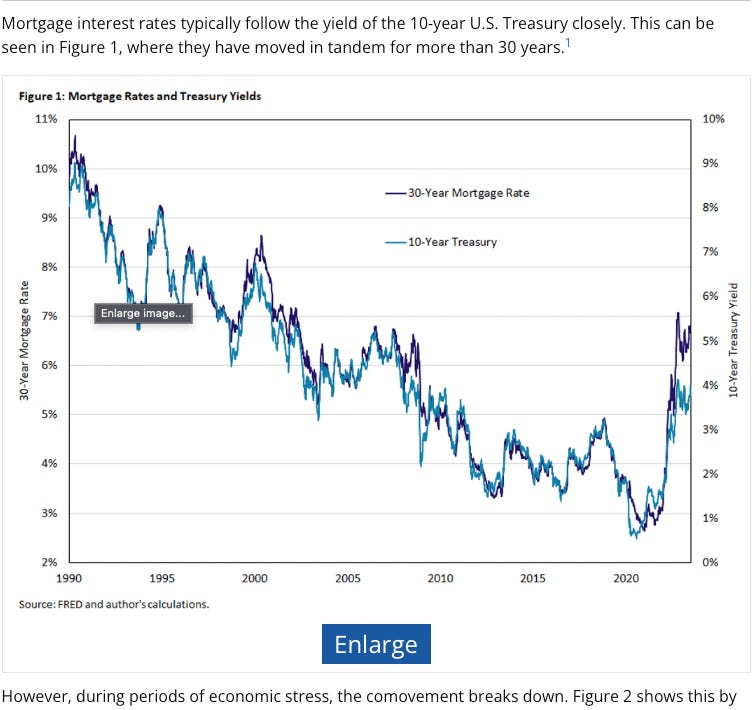

Chart of Historical bond / mortgage spreads

Chart of Historical bond / mortgage spreads

What do consumers think? They haven’t a clue… In December, 31% of consumers indicated that they expect mortgage rates to go down, 31% expect them to go up, and 36% expect rates to remain the same (Fannie Mae). Until this shifts towards cuts, available existing home supply will remain low. Of course consumers surveys are notfor making predictions, but they do matter. It’s a good directional signal for consumer confidence and the consumer is 2/3 of the US economy. And for the record anyone who tells you they know for sure what going to happen in the future is either lying, lazy or stupid.

How fast will rates drop 2024-2025? Well, that’s even harder to predict. The bond market is pricing in 6-7 rate cuts (.25% each) in 2024. The Fed has said they expect to do 3. In the end, it will depend on the strength of the economy, most likely the labor market. If unemployment remains below 5%, I would argue we have a longer cycle of rate cuts: 2 in 2024 and 4+ in 2025, with the cycle ending in mid-2026. This is the skeptical approach, dudes and dudettes, and I recommend you always plan for lower expectation, like Robert DeNiro’s character in Heat said, “Don't let yourself get attached to anything you are no willing to walk out on in thirty seconds flat if you feel the heat around the corner." Always have a plan for the tough times.

To which, U.S. Treasury Secretary Janet Yellen says…hold my beer, saying last week, “What we’re seeing now I think we can describe as a soft landing.” Soooo, mission accomplished? 😬 For its part the Fed is taking a much more skeptical approach. And Yellen’s comment was a departure from her previous comments where the said she saw only “a path” for a soft landing. (As a reminder, a soft landing is—loosely—when inflation recedes without a coinciding recession.)

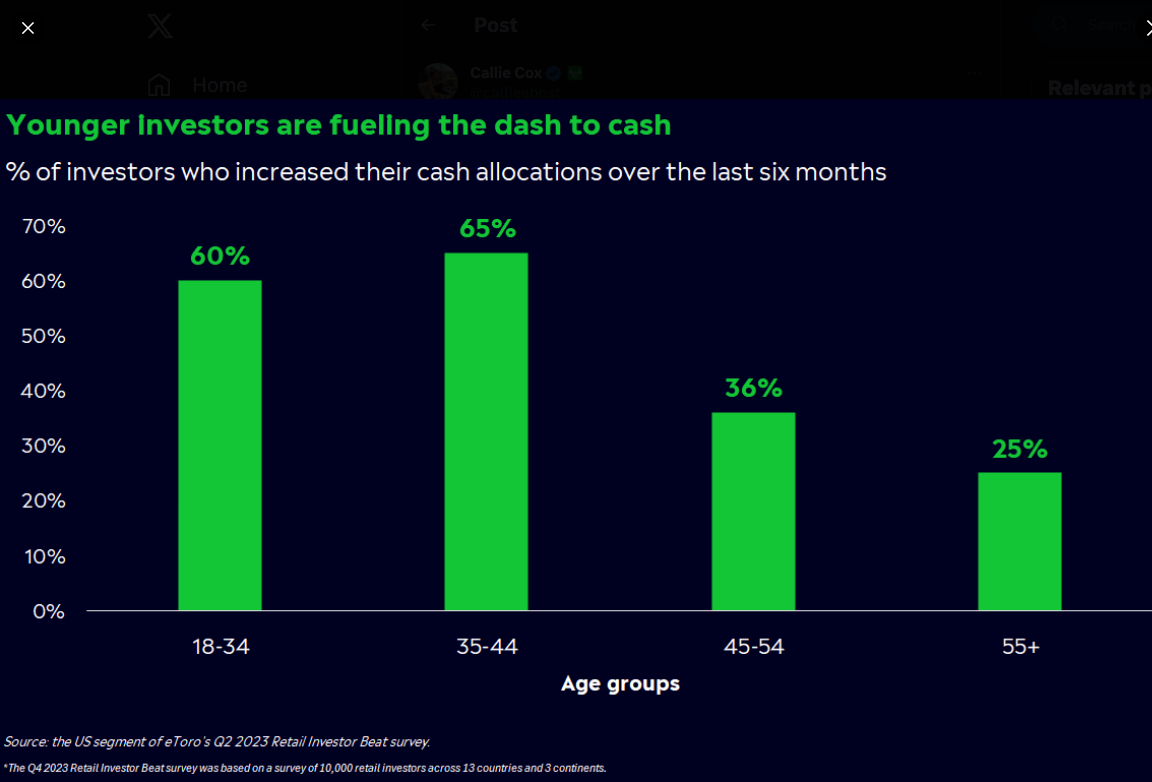

The consumer may be prepping for the “Heat,” by stacking some cash. Of Gen Z and Millenials - those likely looking to purchase a home and are more affected by rates remaining high - are stacking cash. 63% have increased their cash allocations in the last 6 months (vs. just 27% of investors 45 or older) (eToro, @callieabost).

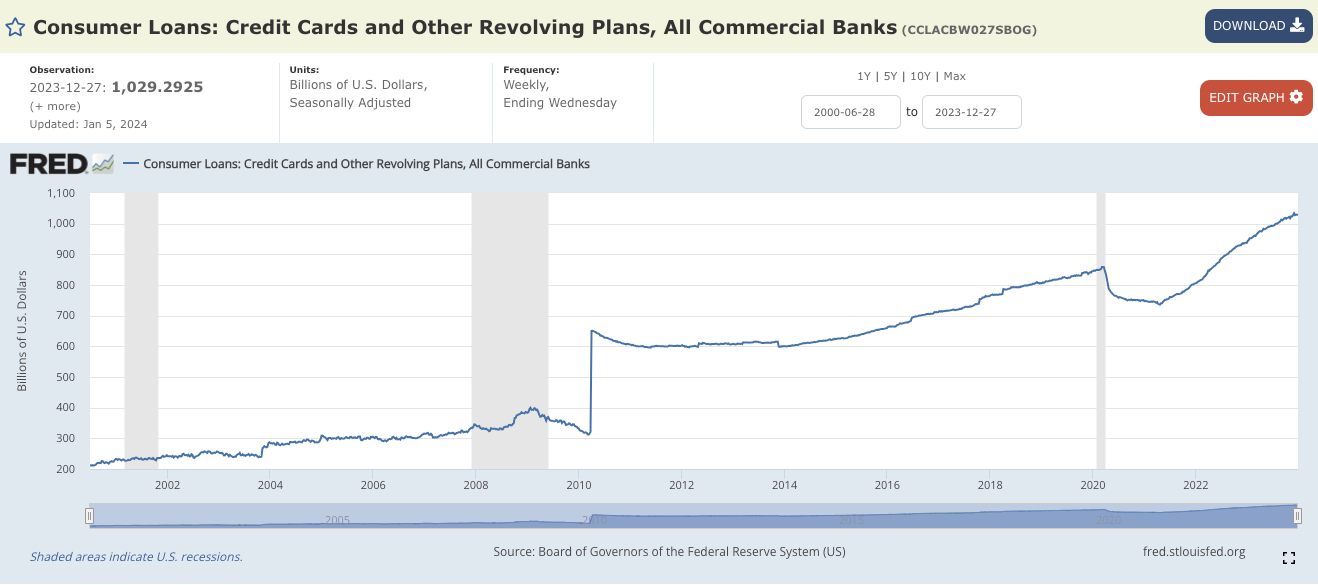

Counterpoint: US consumers now have a record $1 trillion in credit card debt, according to the Fed. And as you can see below, this amount spikes during times of economic tumult. Another indicator to watch as the Fed navigates 2024. Yellen’s soft landing call seems highly pre-mature, IMO.

Counter Counter point: unlike the last recession in ‘08-’09 (not counting the 2 seconds during 2020 government imposed lockdowns) we now have the Qualified Mortgage law. And for those of us reading this because we are interested in the housing market, this REALLY matters because if the economy goes to sh!^ the housing market will remain far more resilient.

What’s qualified mortgage? In short, “The Ability-to-Repay/Qualified Mortgage Rule (ATR/QM Rule) requires a creditor to make a reasonable, good faith determination of a consumer's ability to repay a residential mortgage loan according to its terms (Bureau of Consumer Financial Protection).” Why does it matter? You must watch this brilliant scene from the movie The Big Short to fully understand:

As one of my favorite cheeky analysts Logan Mohtashami(@LoganMohtashami) is fond of saying, the 2010 “Qualified Mortgage Matters. This means everyone [homebuyers] is more legit now than at any time in history.” “[Leading up the the Great Recession (2005-2008) unemployment was low and falling; yet, foreclosures and bankruptcies were rising.]”

Before 2010, banks/lenders literally didn’t do this…Really… it was insane, and I was working as a staffer in Congress when we realized this. This is not the place for politics but let’s just say folks were asleep at the wheel. Nuts.

So what’s the point? We now have rising consumer debt levels and low unemployment, which one could argue is similar to the lead up to the Great Recession. The difference is the housing market will be more resilient to an economic slowdown/downturn. The Qualified Mortgage matters.

Insurance Shockwave on the WayHome insurance is slated to increase significantly in 2024, especially in areas with above average weather events: read TX, CA, FL. Case in point, State Farm will raise rates 20% in CA starting March 15th, 2024. State Farm is the largest home insurer in CA (SF Chronicle). And in FL, premiums increased 102% the last three years, 3x the national average (Insurance Information Institute). Worried about your home’s/business’s insurance premiums? Get this free report here from First Street Foundation, showing at risk areas of the US.

Do you live outside CA, TX or FL? You won’t escape the projected increases. In fact, their situation affects your insurance prices, just like your health care insurance costs are also directly related to the health care needs of others. Why? Well, in brief, insurance is about distributing risk. And insurance companies have an app for that. They purchase reinsurance, to insure the insurer (and some rely heavily on re-insurance, like I believe startup Lemonade does, allowing them to “very capital light mode”). This means, when an insurer makes a claim with their reinsurer, who also reisnurers other insurance companies, the price of reinsurance goes up, which the insurer passes on to you. I know that reads like word salad but stay with me. So, for example, insurance company 1, 2 and 3 uses reinsurance Bravo Company. So if insurance Company 1 has to pay out claims, say for the latest disaster in FL, and is reinsured by Bravo Company, Bravo Company will likely raise rates not just on Insurance 1, but also 2 and 3, distributing their risk and recouping costs. This is how even a hurricane Mexico can increase your insurance rates win New York.

Nationwide, the insurance industry predicts that "We're going to see double-digit increases again in 2024. We don't have an exact number at this point, but we're hopeful it will be much lower than 42% [the increase in 2023] (Insurance Information Institute)." For us real estate investors / landlords, insurance premiums mean cash flow compression, resulting in the unfortunate fact, passing on some of that cost on in the form of rent increases to our residents. No bueno.

Anecdotally, I was just texting with my insurance broker, who is fantastic if you need someone and are in the South, and who let me know it’s just a new reality. We are seeing premium increases across the board amongst all insurers in 2024. From her: “One thing a lot of carriers are doing to try and combat the losses is moving to a percentage deductible (meaning 1 or 2% of the dwelling amount). Overall, the insurance carriers need to make sure they are still bringing in enough money to be able to pay for these huge catastrophic claims that are happening more and more frequently.” A note on messing with your deductible: your lender has to approve any larger deductible and has their own standards for coverage, so make sure to check with them first! Don’t learn that the hard way. And make sure they are covering the cost to rebuild the home in case of catastrophe, not just calculating it based on current value.

When my properties renew this April, it’s going to be painful.

Bottom Line

2024 will be action packed, to say the least. Will GDP slow? What will happen to rates? Will the Fed be able to bring us in for a landing? (or have they already) Oh by the way, there is a Presidential Election 🤦….Regardless, we all can make moves to protect our downside. For instance, you can call your insurer and find out if they are increasing rates significantly in 2024. Then do what I do with my cable/cell/streaming company, go quote shopping.

Are you looking to invest in real estate in 2024? Start saving / setting aside / raising that money now. I believe we should see at least a couple rate cuts, and housing supply should tick up. More deals should be out there to be had. But be careful of building into your numbers lower rate assumptions that are overly optimistic. And remain cautious of tail risk (low likelihood, high consequence events).

In other words….Stay skeptical all you dudes and dudettes.

Most Interesting Tweet of the WeekOn the nose. This made me spit up my coffee laughing. #smallwindowsandwhiteplease

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me direct, I try to answer all the comments I get.

Again stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Mortgage rates can approach 5.5% in 2024, even if the Fed doesn't cut rates.

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Happy 2024 BP Compatriots! Congrats, you made it 😉.

First post of the new year, where if you haven't read one of mine in the past, I do a brief, hopefully insightful, dive into real estate and financial markets. Plus something Nashville related, my home market :).

Today We’re Talkin:

- - Quick Data and News Items of the Week

- - Interest Rates: Is sub 5.5% in 2024 Possible? YES.

- - Consumer Update: rents disinflating but home sales down. Most homebuyers still on sidelines.

- - Tangent! What is the Federal Government Doing?

- - CNBC Special on Nashville: In case you missed it.

Today’s Interest Rate: 6.77%

(☝️ .16% from this time last week, 30-yr mortgage) 3 Curated Items: Data and News to Keep You Informed- 1 - Consumer remains resilient: Personal Income (+.4%) and spending (+.2%) increased in December (BEA)

- 2 - New Homes Sales Down, But a Rise Expected in ‘24 + Gains in residential construction spending and construction job openings (Homebuilders)

- 3 - Home Insurance will continue to rise faster than inflation + State Farm will raise rates 20% in CA starting March 15th, 2024. TX, FL also inflating rapidly. (SF Chronicle)

Interest Rates: Down Soon to ~5.5%?

Rates were up this week, but down on average these last 30 days. What will this do to home prices? 2023 ended up 4.8% YoY, the strongest annual gain seen in 2023, according to Case-Shiller. December numbers are still being tabulated nationwide but this number should hold relatively constant. In my home market of Nashville the data is out however, we were up 8.5% YoY. Interest rates are still too damn high but those able to buy are taking advantage.

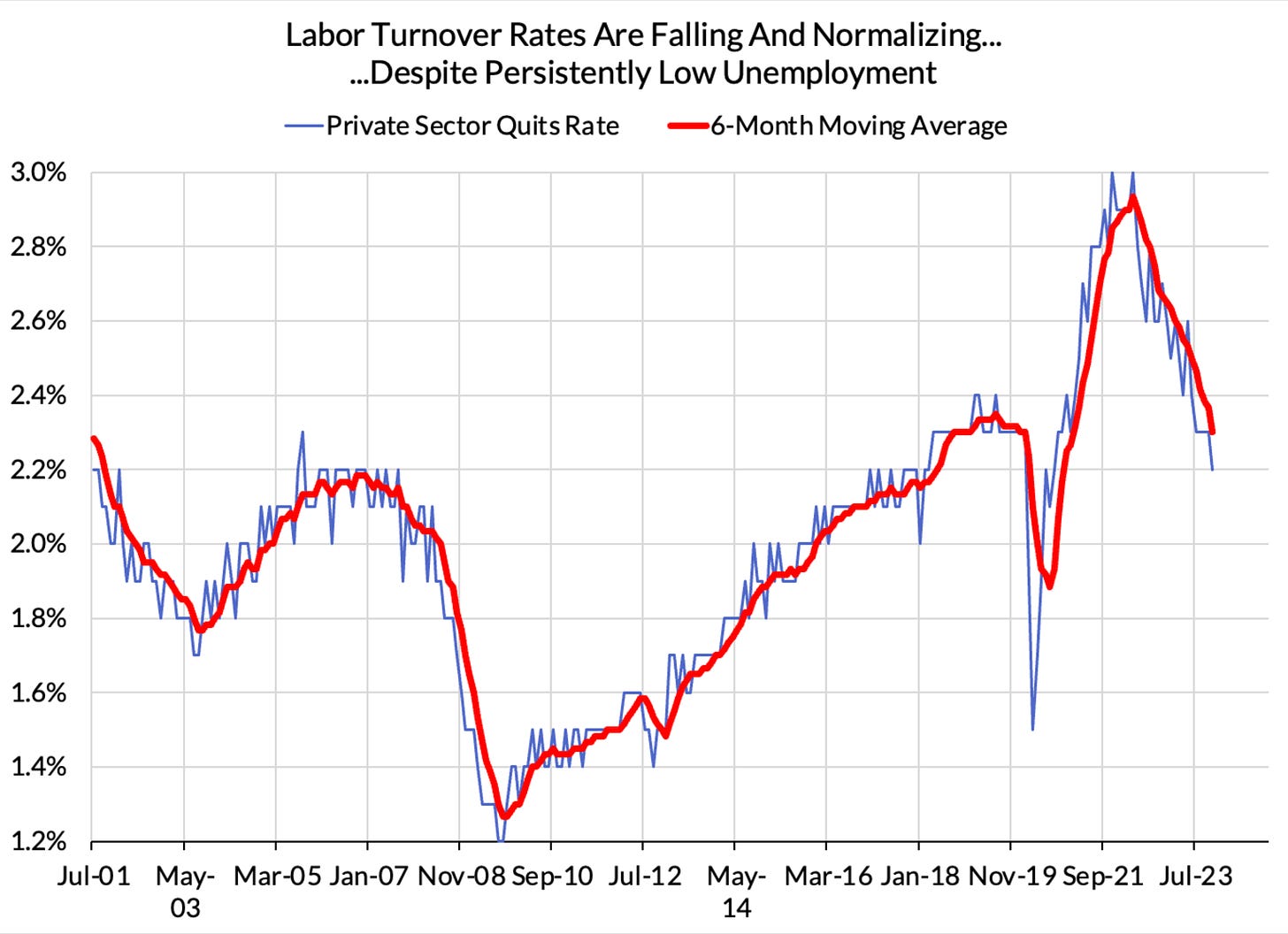

What’s next for interest rates? The 40,000+ employees at the Federal Reserve (still an insane number to me) are probably watching labor markets most closely for signs of cooling. Fortunately, we did see this week some Jack Frost, which should keep the Fed on its course to stepping down rates in 2024: we are now at a pre-COVID job quits.

Look out Lower Mortgage Rates - Is sub 5.5% in 2024 Possible? YES.

Economists will also be watching the bond market, most notably the 10-year Treasury yield. 30-yr mortgage rates track the 10-year and the spread between the two is still historically high. The current difference (“spread”) between the two is 287 basis points (or 2.78%). The historic average “normal” spread is ~175 bps. So if mortgage spreads “normalized,” regressing to the historic mean, and the Fed did nothing from today to lower interest rates, the 30-yr mortgage would be 5.65%. In other words, if the bond market cooperates and the economy doesn’t overinflated, rates should be close to 5.65% in 2024 even without the Fed cutting.

Today’s rates: 10-yr Treasury Yield - 3.90%, 30-yr Mortgage Rate - 6.77%.

My Thoughts10-yr / 30yr spread can go up from here of course. The current spread of 287 is down since spring 2023 where it hit a whopping 330 bps. IMO, spreads will go lower in 2024, but we do need to observe a cooling labor market (and continued lower inflation).

We are emerging out of a real estate recession and so far the data show slowing key indicators, good news for rates. As long as we don’t see a spike in unemployment above 5% and inflation doesn’t tick up above 3% by Q3, the 2024 environment should bring back demand for homes. Again, the Fed says it’s cutting 3 times, the market says it will cut 6 times. IMO 2024 should bring rates somewhere in the 4.75% - 5.5% range.

This insight is HUGE. But keep a watchful eye. (and keep reading my posts 🙂)

The Consumer - MixedSome thoughts/data on the consumer.

Consumer sentiment was way up (14%) in December, reversing all declines from the previous four months. “These trends are rooted in substantial improvements in how consumers view the trajectory of inflation” and likely due to dropping mortgage rates, IMO.

But…

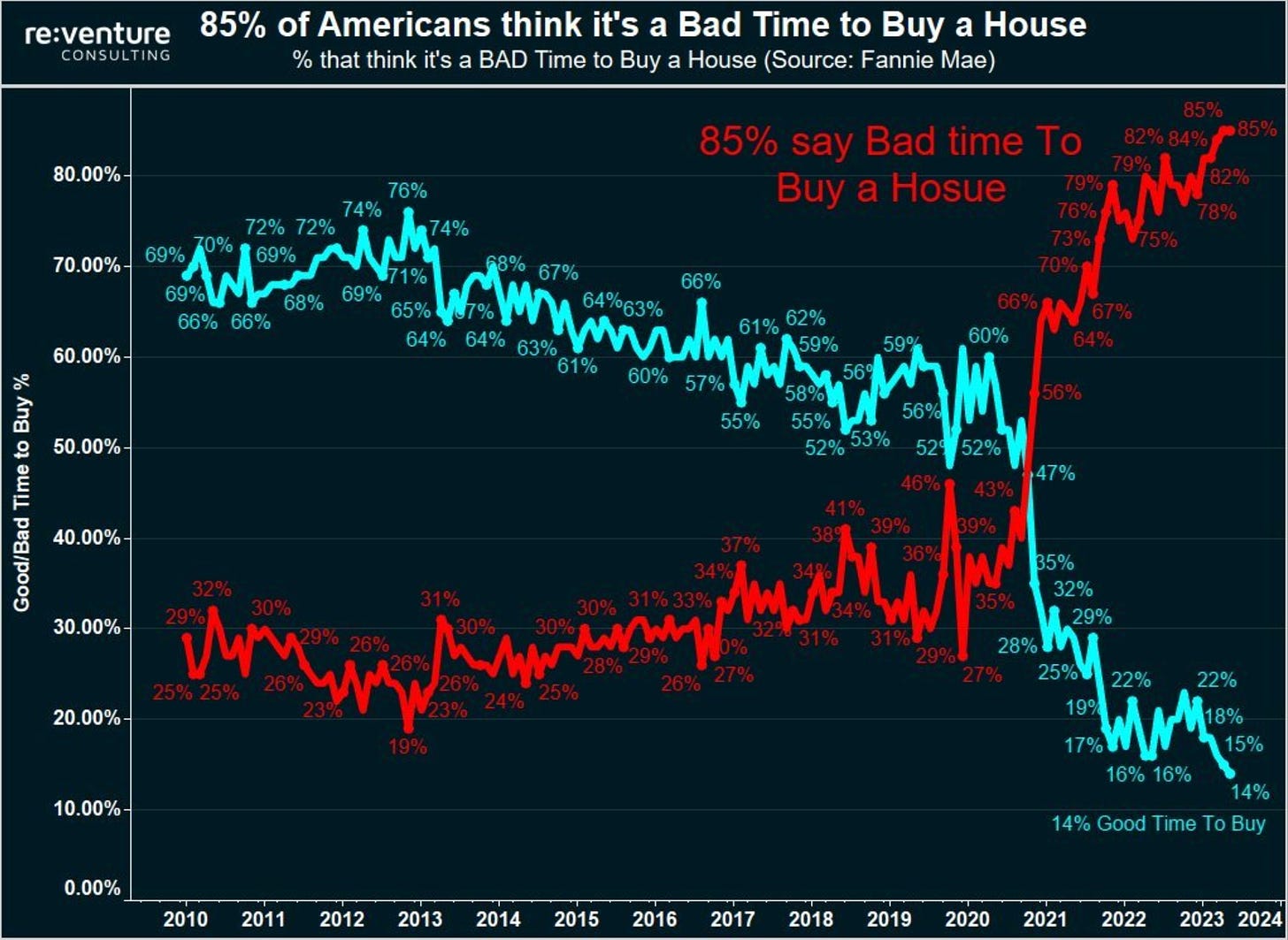

A record 85% of Americans now say it's a bad time to buy a house, according to Reventure. Two years ago, 30% of Americans thought it was a bad time to buy a home. Even in 2008, during the worst housing crisis of all time, this metric did not top 85%.

Millennials (ages 26 to 42), the largest potential buyer of homes, are still on the sidelines. Damn I’m technically a millennial? Although I Identify as a latchkey Gen X-er 😁. I digress….

Millennials, have been hit hard financially and are facing a housing market with high interest rates and low inventory. Many are choosing to rent, and rents are showing signs of disinflation. In fact, median U.S. “asking rent fell 2% year over year in November to $1,967—the biggest decline since 02/2020.” (Redfin)

My Quick Take: Redfin cited a building boom as the culprit but that hasn’t been my experience in Nashville, despite having the most apartments under construction in the country. Rents are still rising, but are disinflating. (I’m referring to single family and small multifamily homes. Now apartments/condos, which I don’t track as closely).

In 2022, millennials were the largest generation of homebuyers, accounting for 43% of all purchases. But that number fell to 28% in 2023. (Business Insider)

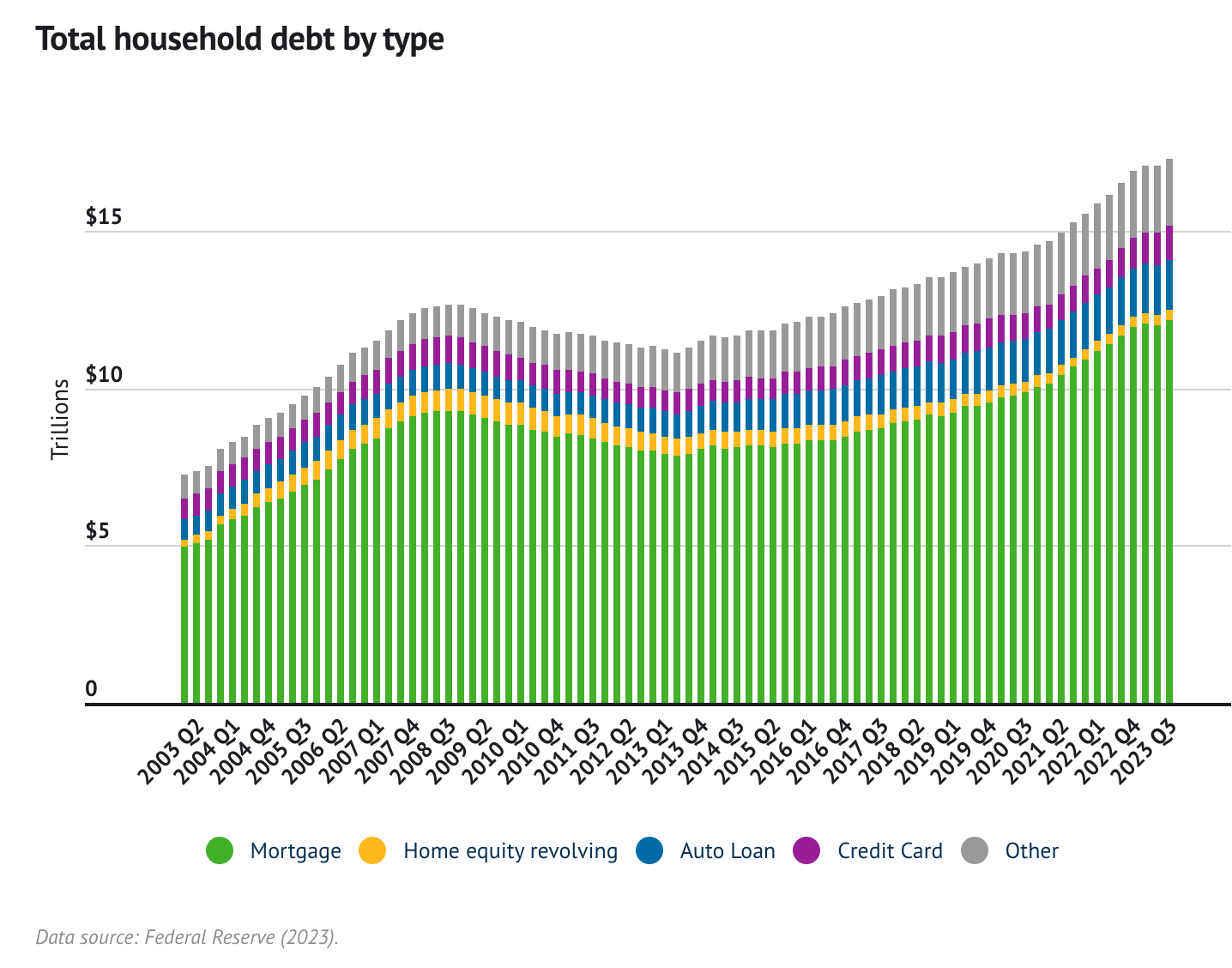

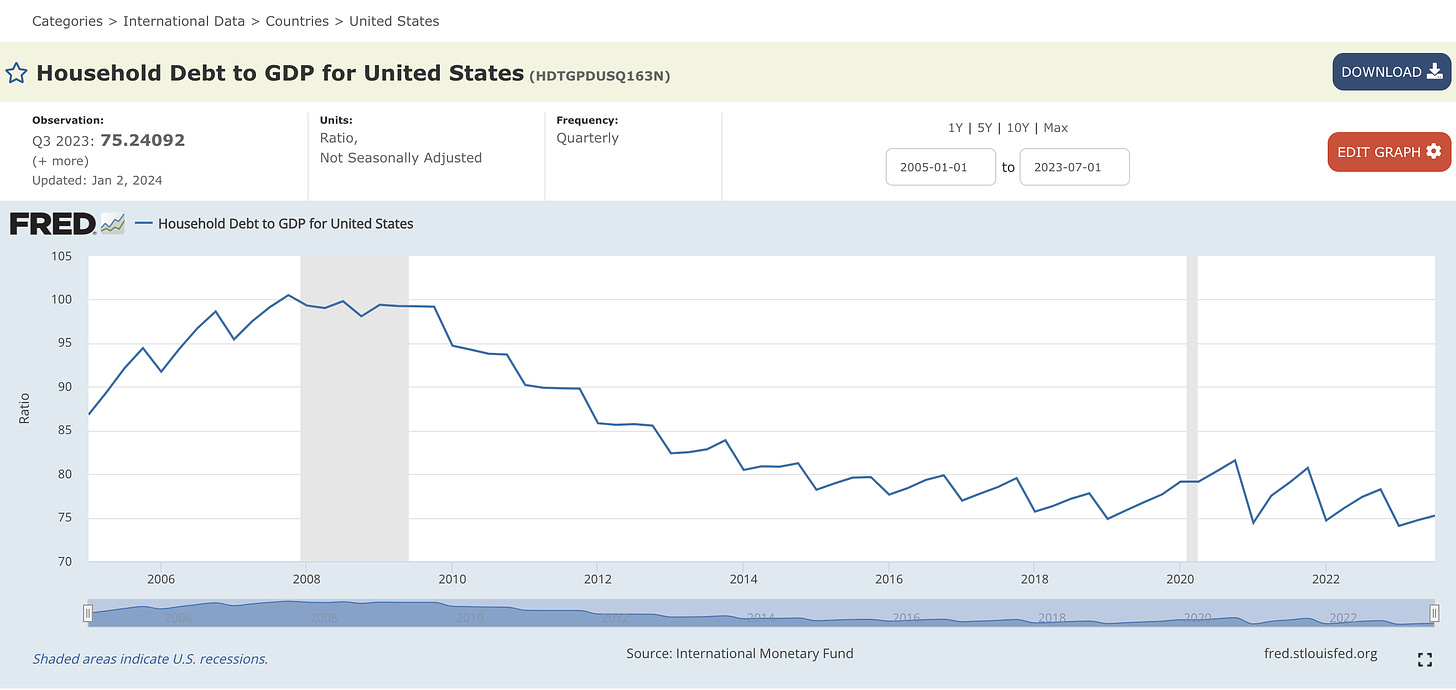

Additionally, total household debt is rising higher.

As are credit card defaults. Although still at historical lows.

So all considering, the consumer is looking in decent shape.

** TANGET Alert!

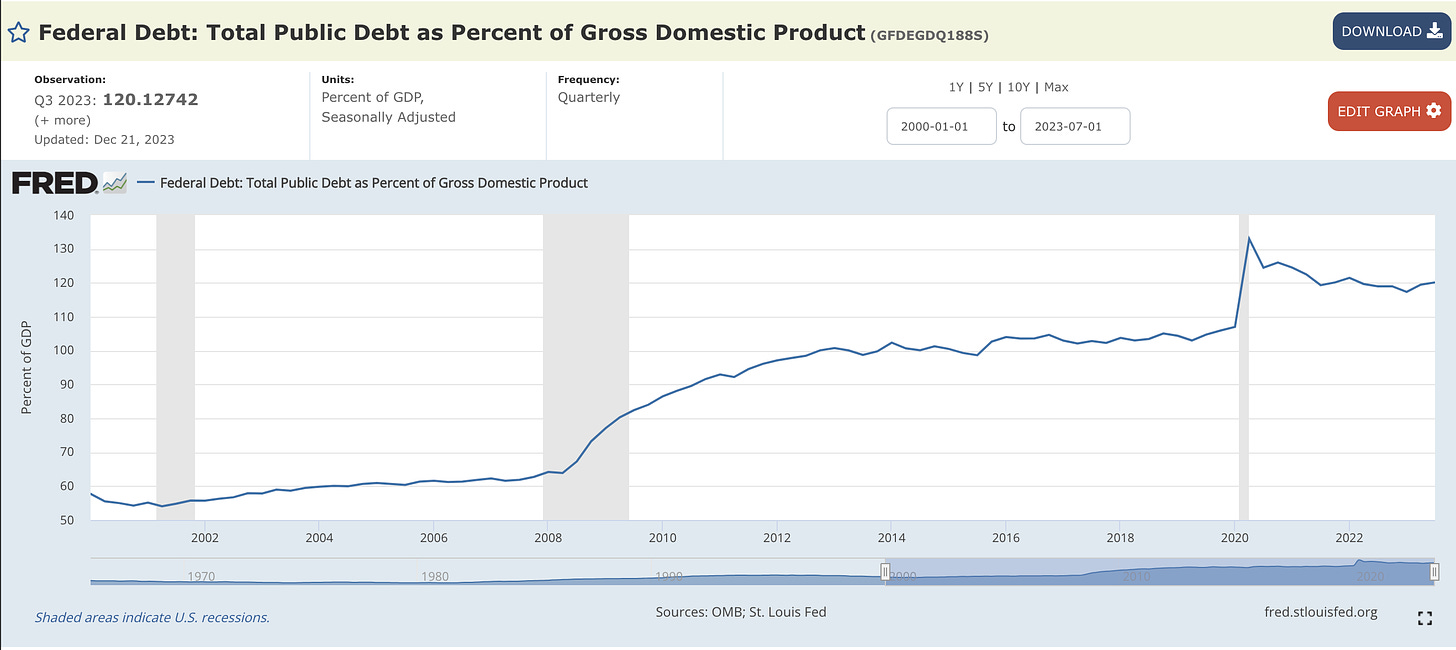

BUT, compared to the Federal Government’s books… well. Take a look at Household Debt to GDP and Federal Debt to GDP. Who looks like they are in more trouble?

Now look at Household Debt to GDP. Lower.

Looks like the Consumer learned their lesson after 2008 (and in fairness banks/congress did do some good here to put credit rules in place, like the Qualified Mortgage). The US National Debt is now past $34 Trillion! Up a whopping $ 29 Trillion since 2000. Insane….

But I digress…

One silver lining: it looks like this largest investment-aged demo is at least putting their money to work, even if they can’t invest in a home. The number of Americans who own stocks is at an all time high; 58% of households, according to the Federal Reserve, as reported by

Unusual Whales (a great Twitter follow). Especially if you are in California, where only 15% of Californians can afford a home. As a result, home sales are at a 16 year low. Homebuyers are leaving Los Angeles more than any other metro area in the country, however, the total migration out of cites has slowed considerably, driven by COVID policies.

Probably not used to seeing California colored red :)

In case you missed it: Nashville CNBC SpecialJust in case you missed last week’s newsletter. This is a great series, and they started with my home of Nashville! More of these to come around the country. Stay tuned.

Cities of Success: Nashville. A CNBC Exclusive on the growing city. (TV subscription needed, but should be available soon widely).

Bottom Line

2024 will likely be a banner year for real estate, if you have the dry powder. Start saving / setting aside / raising that money now. We should see 3-6 rate cuts, and housing demand / home sales should tick up. But be careful of building into your numbers debt service and mortgage rates that are too bullish. Keep those numbers skeptical.

To quote the late giant Sam Zell, “Real estate isn’t just about buildings as inanimate objects. It often reflects the pulse of the nation.” Pay attention to what’s happening in your local market and in the economy around you. Talk to business owners, waiters, bartenders, subcontractors. 2024 may be a volatile year, protect your downside.

Most Interesting Tweet of the WeekYuck. Hey @nerdwallet, I know your business is based on ads from lenders/banks/credit card companies that pay for your crappy site that has more pop-ups/ads than a porn site, but…maybe don’t promote stuff like this? It’s predatory and reeks of 2008.

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me directly right here on BP!

Stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Anywhere left to invest in inexpensive real estate ?

- Real Estate Agent

- Nashville, TN

- Posts 224

- Votes 110

Tennessee, 10-20 min outside Nashville is in your buy box. Happy to show you properties and see if it meets all your number requirements! Send me a Message. And good luck regardless! -Andreas

Quote from @Becca F.:

Quote from @Account Closed:

Quote from @Michelle Backer:

Anywhere I can buy property still for cheap

Possible good investment?

Iowa? Nebraska?

I have not been keeping up lately although now i am.

I live in NYC.

As Sam pointed out, cheap is subjective. For people who live in coastal California or NYC, buying a $450,000 to $500,000 is "cheap" compared to buying a $1+ million property but to someone in less expensive state, that might not be cheap. I would say $500,000 for a SFH or duplex, I think is reasonable if I were to spend it on an appreciating city/state (e.g. California, Nevada, Arizona, Florida, Texas, Nashville Tennessee) but those would be negative cash flow right now as long term rentals unless I'm doing MTR or STR - I'm buying off the MLS or using an agent, no wholesalers, no tax liens, etc..

I wouldn't call $500,000 cheap - I use sub $200,000 as my parameter for "cheap" and if I'm not in a severely negative cash flow (-$100 to -$150 at most for first 2 years at current interest rates) but it's hard to tell since I can't predict precisely how many tenant turnovers, capital expenses, how much my property taxes/insurance will go up, repairs I would have on a renovated Class C Midwest property that's 100 years old over 10 year time span. My recent 2 Indy purchases were a renovated $130,000 SFH (rented out for 6 months now) and $132,600 (still needs repairs before being rented out). And I'm hoping these Class C will become Class B and appreciate as there's more development. I'm considering 1031 exchanging 3 Indy properties in the future back to one California or Nevada property. Will cheap cost me more in the long run?

Not sure where that map is from but wouldn't Miami or Orlando areas and parts of Colorado (Denver, Boulder) and Utah (Salt Lake City, Park City) be considered "not cheap" so would be in red? What was the cutoff purchase price or current market values used to establish "cheap"?