All Forum Categories

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

All Forum Posts by: Andreas Mueller

Andreas Mueller has started 58 posts and replied 212 times.

Post: Is the Fed Done Cutting For 2024?

Post: Is the Fed Done Cutting For 2024?

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Quote from @Bruce Lynn:

The Fed doesn't control mortgage rates, and I'm not even sure they influence inflation and unemployment any more. I think they've lost control of most of their tools. The most stubborn parts of inflation may start to increase again...food, fuel, rent.

Bruce, I hope, for our sake, they can maintain some control.

Much appreciate you engaging in the comments!

Post: Is the Fed Done Cutting For 2024?

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Welcome to the Skeptical Investor Blog, right here on BP! A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - Interest Rates are Threatening Even Higher

- - It’s Inflation Stupid: Federal Debt Matters

- - None and Done? The Fed be Done Cutting Rates for the Year

- - My Skeptical Take

The Weekly 3: News, Data and Education to Keep You Informed

- - Six major US metros have seen YoY home price declines. New Orleans (-4%), Austin (-4%), San Antonio (-2.7%), Tampa (-.5%), Jacksonville (-.3%) and Dallas (-.3%) (Nixon).

- - The US government now spends just as much on interest payments as it does on defense expenses. The latter defends our country, the former destroys it (Pomp).

- - Home Affordability is Difficult, and it’s Not Getting any Better. To return to pre-2020 housing affordability 1) incomes would have to spike 60%, or 2) home prices would have to fall 38%. Neither seems likely (Lambert).

Interest Rates are Threatening Even Higher

Well, what a difference 30 days makes.

The Fed cut interest rates by a larger than expected .5%, and after a few days of celebration (yay!), the market is now calling their bluff (boooo!).

Specifically, the bond market. It does not believe we are out of the recession/inflation woods yet.

So, it has grabbed the wheel and turned this car around, like a frustrated dad with 5 kids on the way to the amusement park!

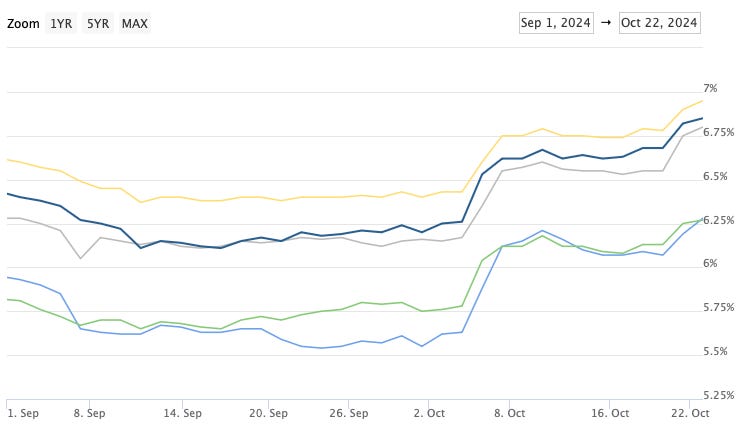

Mortgage rates, which track the 10yr Treasury bond, have reacted in kind, up .73% from their September lows, following the Fed rate cut.

Mortgage Rates Sept-Oct, 2024

Why?

Investors have sold off Treasuries over resurgent inflation concerns and reckless fiscal spending (also inflationary). If you are a bond/debt investor, you hate inflation because it erodes your interest rate earnings.

The Fed Can’t Repair the Housing Market

As a reminder, the Fed does not control mortgage rates.

Mortgages are predominantly influenced by the market demand for 10yr Treasury bonds, not the Federal Reserve's adjustments to its short-term Fed-Funds rate (that’s actually what they do when they “cut interest rates.” The 10yr Treasury and 30yr mortgage are competing assets investors buy in the marketplace, expecting a return for their expected risk. If investors expect higher risk to the economy, they buy 10-yr Treasuries. If the future seems less risky, they buy 30-yr mortgages. Investors also sell Treasuries if they see inflation on the horizon, which would erode their returns (yes yes, this is all oversimplified, hold your comments angry-web).

The Housing market is a difficult issue, with many moving parts. The two primary drivers for a healthy market are the supply of homes and the cost of debt to purchase those homes. So, the Fed can’t unilaterally repair the housing market, but it can assist with cheaper debt (ie interest rates).

Last month Fed Chair Powell made some salient points on this topic precisely, saying:

“The real issue with housing is that we have had, and are on track to continue to have, not enough housing… and where are we going to get the supply? And this is not something the Fed can really fix.”

And he continued:

“But as we normalize rates, I think you’ll see the housing market normalize. Ultimately by getting inflation broadly down and rates normalized and getting the housing cycle normalized, that is the best thing we can do for householders. And the supply question will have to be dealt with by the market, and also by the government.”

So, in short, while they can’t repair the broken housing market, they are a major piece. This is likely a relatively short-term problem, but unfortunately homebuyers / sellers are caught right in the middle.

It’s Inflation Stupid: Federal Debt Matters

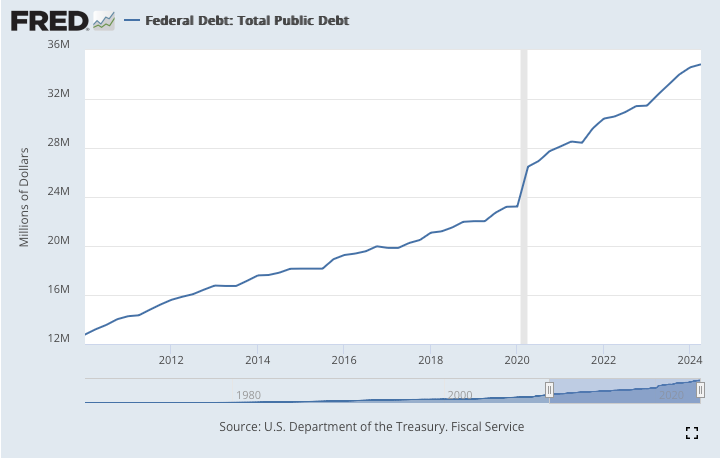

US federal debt is absolutely out of control. Unquelled, it will bring higher inflation and higher mortgage rates. The number is staggering: $35 trillion and growing, faster than our economy.

And as I am reminded daily on my news feeds, we are in a Presidential election cycle. Even without any additional spending, the next president is on track to spend an additional $10+ Trillion over 4 years. Add that number to the wild spending promises from both Presidential Candidates, which are stacking up under the Christmas Tree, and you have a recipe for inflation disaster.

Each of those nicely wrapped boxes is a future fiscal time bomb, ready to explode.

Why does Good Economic News Mean Bad Market News?

All this being said, for now, the overall US economy looks to be holding strong, especially when compared to the rest of the larger world economies.

But back in August, a doddery jobs report may have spooked the Fed after sending markets sharply downward. Yet, in the months since, most jobs and inflation reports have come up roses.

And we just had a very positive jobs report. Employers added 254,000 jobs in September and unemployment ticked down to 4.1%, both better than expected. Plus, this past month's employment was revised up. As was gross national income, personal income and the personal savings rate. September 2024 CPI inflation now sits at 2.4%, close to the Fed’s 2% target.

Now most folks would think: “yay, more jobs!,” but, again, the bond market interpreted this news as either: a potential return to inflation or an extended timeline for the Fed to cut rates. After all, why cut rates quickly if the economy is doing well and jobs are plentiful? This risk is driving the sale in 10yr Treasuries; and thus, mortgage rates.

Bonds are selling off again today.

We are still in a precarious economic time, so good economic news may be “too good,” and bad for debt markets. And mortgages are debt.

Muah! Now that’s some real economics charcuterie for ya.

None and Done? Is the Fed Done Cutting Rates for the Year?

The bond market’s concern with future inflation is likely shared by the Fed. Perhaps they even slightly regret cutting rates by a full .5% in September.

So, could the Fed decide to pause here for a while?

Economist Ed Yardeni (one of the talented ones :) ) believes the Fed is on a path for “none and done,” no more rate cut rates for the rest of 2024.

This is a seemingly bold prediction, but I would argue it is looking increasingly less so.

In a concise presentation, he asserts that the economy is performing better than expected and the sentiment amongst investors is positive. There is no impetus to cut rates.

My Skeptical Take:

Is a return to elevated inflation a real risk?

Yes. It’s not likely, but yes it’s a real risk. And a dramatically higher risk if the Federal Government doesn't stop the printing press. We will have a new President in 2025. It’s up to them, working with Congress, to determine our fiscal future.

For the Fed, a return to high inflation is a worst-case scenario; I think they will be measured over the next 12 months.

Does the Fed have regrets about being so aggressive? I don’t think they are regretful, per se, but they may adjust their posture. The Yardeni piece (above) swayed me. So, I’m changing my mind. I’m now a little more bullish on the economy, and thus bearish on the pace of rate cuts. I’m revising my prediction of two more cuts this year to just one (.25%), likely in December. I think the economy continues its on-trend growth, oil prices are still low (albeit threatened by geopolitical tensions), and the job market continues to surprise to the upside. There will be noise in the stock market and in the press, especially in the next 3 weeks of election season, but the trend will remain positive for the next 5-6 months.

Former Treasury Secretary Larry Summers is also cautiously skeptical on rate cuts. He sees the Fed taking the cautious/slow approach to rate cuts, even going so far by calling the larger .5% cut a “mistake,” while pointing out that wage growth is strong, above 2019 levels, which could risk inflation returning.

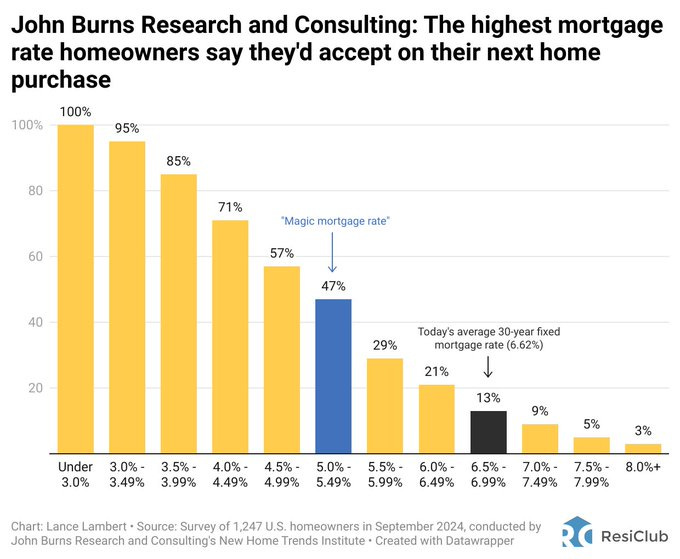

So What’s Next for Mortgage Rates?My prediction for rates in 2025 has not changed. I think we hit hit 5.5%. I am more bullish on lower rates than most investment banks / economists, many of whom are calling for ~5.9% by Q4 2025. IMO, 5.5% is the “magic” mortgage rate, where folks are no longer sitting on the sidelines of homebuying using rates as a main reason for waiting. A recent survey of homeowners seems to agree.

With rates maintaining their elevated position, homebuyers and sellers are likely to hibernate for the Winter and Skip till’ Spring. Activity this late Fall and Winter will be suppressed and inventory should rise more.

BUT….If you are an investor, you can hack your way through all the noise and find that deal. Those selling a property today will be waiting 2x as long for a buyer. Sharpen your pencil and find that deal that is sitting on the market.

Be greedy when others are fearful.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Please Share this Article!

It takes hours to write this weekly article, and they will always remain free. All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

What, did you think I was going to send you a Starbucks gift card? 😅

Post: High Home Price got you down? It's More than Just Supply and Demand

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Welcome to my weekly Investor Newsletter. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - All the “whys” for High Home Prices

- - Home Prices, it’s more than just supply and demand.

- - Generation Toolbelt. LFG!

- - Bring Back Home Ec!

- - My Skeptical Take.

Fuel for the Day: Greens! I actually make my own greens smoothy / drink often but when I am on a writing heater and don’t want to pause, I grab some AG1. Good stuff, really good. Gets my brain firing.

The Weekly 3: News, Data and Education to Keep You Informed

- - Folks are Skipping Till to Spring to Buy. Rates are coming down in a few months, and buyers know it (, ).

- - Refinancing is starting back up again. But you ain’t seen nothing yet (ResiClub).

- - Book Recommendation: Bubble in the Sun: The Florida Boom of the 1920s and How It Brought on the Great Depression. The 1920s in Florida was a time of excess, immense wealth, and precipitous collapse. It was the largest human migration in American history, far exceeding that of the West. And it was real estate speculation here that helped cause the Great Depression. This is a must for your library, something to re-read again and again (Knowlton).

Today’s Interest Rate: 6.25%

(☝️.06, from this time last week, 30-yr mortgage)

Guten Morgan investors. It’s a lovely day to talk real estate. Let’s get into it.

Last week was all about rate cuts. But it’s going to be a while for mortgage rates to come down (as I’ve written about), so for now let’s put that on the back burner and talk about something poignant.

Home Prices.

Why are Home Prices This High?The primary reason for the price of anything is simple supply and demand. (And we will get into significant secondary reasons below, keep reading!)

In the case of housing: we have ample demand (and more on the sidelines waiting to jump in once rates tick down) and not enough supply. Not even close.

Supply is currently short 1.5 million housing units of what is needed to keep up with demand.

Increasing Supply Works!Case in point, in 2017-2019 while facing a severe housing shortage, Minneapolis enacted its 2040 Plan, becoming, “the first major U.S. city to end single-family exclusive zoning, opening the door for developers to build multifamily buildings on lots where a single-family home used to be (NBC).”

The result? Supply UP!

A Pew Research report found that between 2017 and 2022 - the beginning of the Minneapolis 2040 plan - “housing stock grew by 12% in the city, compared to 4% statewide. An NBC News measure of home buying difficulty shows that Hennepin County, where Minneapolis is located, is the second-easiest county to buy a home in compared to the seven counties adjacent to it — even though Hennepin is the most populous county in the state.”

Great damn job Minneapolis!!!!

What Else is Contributing to Home Prices?Supply and demand this is not the whole story. Home prices are higher than they normally would be even in these tight market conditions.

Tell me why!

Well, I don’t mind if I do.

Home prices have been amplified because of the increased costs for builders to actually build a home in the US, mainly:

- Inflation (materials and labor).

- Regulatory burdens.

Let’s look at both:

Inflation

Prices for everything necessary to build a home - including building materials and hourly labor - are much much more expensive. These higher prices are likely permanent, as prices rarely deflate (and that can cause a whole other set of economic problems).

I have written at length about the case and effects of inflation. In short, inflation is caused by policies and spending (not consumers or businesses). And over the last few years, we went on quite the money printing spree.

More than $10 Trillion!

You can read all about what the US did in my previous article on the subject here.

It’s a doozy.

For now, just know we had a few years of much higher than normal inflation and it caused permanent damage in the form of higher input prices to build a home.

Regulations

The second cost of a home is regulatory policy. Especially for large development (ie apartment and condo buildings), where many of our housing units come from.

Building housing is subject to a significant array of regulatory costs, including a broad range of fees, permits, reviews, and other requirements imposed at different stages of the development and the construction process, with both a direct cost and a time/delay cost.

In fact, according to a recent study, regulation “imposed by all levels of government accounts for an average of 40.6 % of development costs (NAHB, O’Leary).”

Apartment developers in particular are subject to a variety of regulations across all levels of government. They include: zoning requirements, building codes, impact fees, permitting requirements, design standards, public land requirements, and federal Occupational Safety and Health Administration regulations and other labor requirements. Unfortunately, many regulations, such as design standards, go far beyond important safety concerns, and impose costly mandates on developers that drive housing costs higher. Others are duplicative and require resources to confirm compliance with multiple regulators with overlapping jurisdictions.

Further, the study noted that “[Three quarters (74.5%) of housing developers said they encountered “Not In My Backyard” (NIMBY) opposition to a proposed development, adding ~ 5.6% to total development costs and an additional 7.4 month delay.]”

Wow.

This is why both presidential candidates are talking about the need to reform housing regulations on the campaign trail.

It seems that innovation in the construction technology space, and thus labor productivity, is an area for significant improvement.

Productivity in virtually all industries is accelerating over time, leaving construction in the stone ages.

We don't really build homes that differently than we did 100 years ago.

Why?

We need investment in construction technology and government needs to green-light it asap.

It’s just too expensive to build a home!

Gen Z is Gettin Handy

One glimmer of hope is the new Generation Z folks are getting interested in the trades. Gen Z is becoming known as Generation Toolbelt.

Love it!

A fantastic Wall Street Journal article reviews the renewed interest in vocational training, manufacturing and hands-on labor fields.

From the article:

“Demand for trade apprenticeships, which let students combine work experience with a course of study often paid for by employers, has boomed. In a survey of high school and college-age people by software firm Jobber last year, 75 percent said they would be interested in vocational schools offering paid, on-the-job training (WSJ).”

And this idea of blue collar career interest was recently discussed on the All In Podcast, which includes a group of prominent Venture Capitalists. They make a great point about the “premium of human service.” This is something that won’t be disrupted by AI; in fact, it could be a catalyst.

There is a role for government and investors here. We need more startups, funding and pro-business policies in traditionally blue-collar industries!

And I’ll go a step further.

What Happened to Home Ec?Frankly, it’s a shame we don’t have Home Ec anymore. Teaching personal finance, woodshop, home repair, car repair (the mechanical part) and cooking should be required at every high school. A full yearlong class. And it often is not on the top of lists for parents to pass on to their kids anymore. Young folks just aren’t handy anymore. I took apart my TV (a few times, and the toaster) when I was 11 and after a little parental lecture, they encouraged it (this time with Goodwill appliances). We should all be teaching our kids (and other little family members aka nieces and nephews) this stuff too. It’s about thinking through problems, being resourceful, critical thinking etc… not necessarily that you will be a contractor (but it could be).

So I say, bring back Home EC!My Skeptical Take:

The US economy seems to be chugging along well, at least for now. GDP is up 3% YOY, unemployment is historically low at 4% (and even better here in Nashville at 2.9%). Inflation is ticking down and is likely at the Fed’s 2% target, which we will see in hindsight. Prices for staples are down a bit from their high and their inflation has slowed considerably, particularly in gas and many groceries. It is true that home prices have never been higher, but this also means most homeowners have more equity in their homes than ever. An average of $300,000 in equity in fact.

Rates are on the way down, meaning Spring will likely bring a new wave of demand to the market and folks will look to refinance their home, taking cash out to pay for life needs, and also likely to splurge on new toys. This point should be emphasized. Fortunate homeowners will very much be flush with future cash. Equity in homes is multiple Trillions that people will tap in the next 12-18 months. This money will be spent throughout the economy.

I am Skeptical that the US economy will have a Goldilocks recovery in the next 18 months. Specifically, I am concerned that the relatively positive state of the current economy may be a lingering result of the stimulative drugs Uncle Sam slipped in our martini. Consumer spending is 2/3 of the economy and it’s hard to ignore the sheer volume of free dollars the federal government pumped, and is continuing to pump, into the economy. $10 Trillion dollars worth. Folks will spend those dollars. In addition to my point above on tapping trillions in home equity.

When the drugs stop, or at least abate, it will be time for the come-down.

Keep a Skeptical eye out. And it could be something international that sparks it. It is unfortunately a tumultuous time in many parts of the world.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Please Share this Article!It takes several hours to write this weekly article, and they will always remain free. All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

* I write this myself and get it out for you all on the same day. Apologize in advance for the likely errata. Don’t have a team of editors, yet.

** The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and do not constitute financial advice.

Post: New to real estate investing, looking to build connections

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Michael, we represent buyer investors here in Nashville. Happy to chat anytime!

And, if it's helpful, our we put out a weekly financial real estate column here on BP. Check it out! (Always free of course).

https://www.biggerpockets.com/member-blogs/15226/103921-home...

-Andreas

Post: Newbie trying to get a start in real estate investing

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

90 folks per day move and 16.8 million tourists visit Nashville every year. Join the party!

Post: Buyers are Skipping till Spring, and Savvy Investors are having their Pick

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Welcome to the Investor Agent Newsletter. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - Are Buyer’s Skipping till Spring?

- - How the Savvy Investors are Positioning.

- - My Skeptical Take.

Fuel for the Day: Found this great coffee from Olde Brooklyn Coffee. Silky smooth and grinds with the rich scent of chocolate. ☕

The Weekly 3: News, Data and Education to Keep You Informed- - “The US economy is not facing a recession,” says Apollo chief economist Torsten Sløk. Sløk cites strong employment data, wage growth, and consumer spending as key indicators. Corporate profits are at record highs, and GDP growth is projected at 2.1% for Q3, suggesting continued growth ahead (BI).

- - Maned Spaceflight is back! Polaris Dawn just launched and will bring humans to the highest orbital altitude since Apollo in 1972. More than 3x further than the International Space Station (SpaceX).

- - Book Recommendation: Long-Distance Real Estate Investing. I’ve recommended this before, and it’s a bit out of date with new software that automates much these days, but with prices only going higher, many investors are looking outside their expensive market for their next real estate deal. Can’t recommend this book any higher for new investors.

Today’s Interest Rate: 6.22%

(👇.18, from this time last week, 30-yr mortgage)Guten Morgan investors. It’s a lovely day to talk real estate.

Let’s get into it.

Skipping till SpringGet excited! Interest rates will soon begin the pilgrimage down from their ugly nest atop the mountain. But the welcome spectre of rate cuts in just over a week now has homebuyers/sellers thinking… Perhaps the grass may be greener in the Spring?

I described the above to AI and well, this is what we got. Ha. AI is getting there, but it ain’t there yet.

I described the above to AI and well, this is what we got. Ha. AI is getting there, but it ain’t there yet.

So, if they can wait, they are. Pending home sales fell 5.5% during July and the data so far is showing another decline in August (NAR). I expect this to continue through the winter.

Lower activity will translate into higher inventory levels, which will continue their melt up for another 5 or so months. Buyers are Skipping till Spring, anticipating those cuts. Heck, if they waited this long, and it’s soon to be winter, what’s another few months?

Investor Tip: Look out for more ugly existing homes to snatch up.

Investor Tip: Look out for more ugly existing homes to snatch up.

Homes in need of a renovation should start to slowly accumulate on the market. The spread between the supply of existing homes and new homes is at a historical high, close to double what it should be. This is because the 2020-2021 ultra-low interest rate policies incentivized homebuilding and at the same time disincentivized exiting home sales as folks refinanced their mortgages only to have interest rates explode higher 1 year later (2022-present) locking them into that home and preventing them from selling and then buying another (remember, most sellers are buyers).

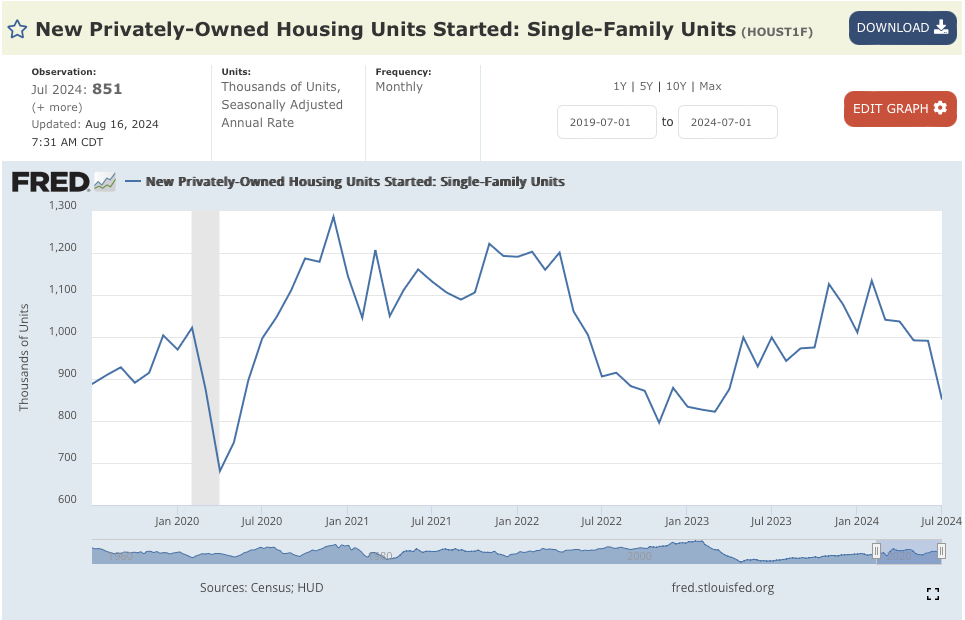

Although that is not to say new homes aren’t coming on the market, it’s just not enough. Single family housing starts are low, and moving lower fast into the winter cycle.

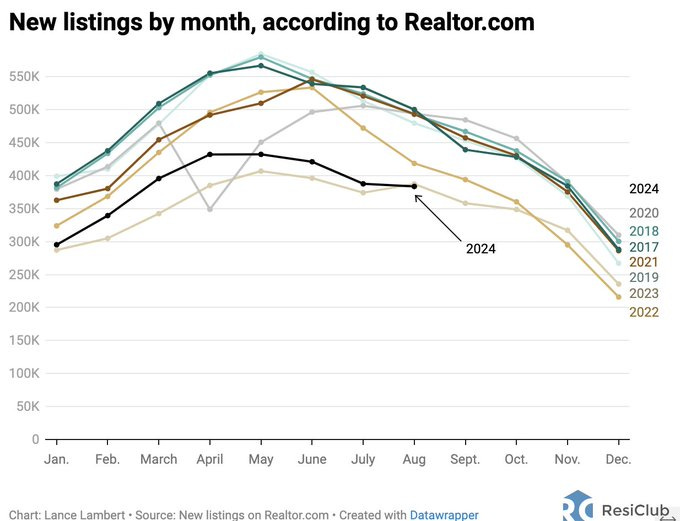

Inventory is up but Seller’s aren’t Waiting Either

Inventory is up but Seller’s aren’t Waiting Either

Importantly, median (and mean) home prices are up YoY. And many sellers are not accepting, on average, drastically lower offers. They are also waiting. Inventory is rising because demand has cooled and homes are sitting longer, not from new listings.

ResiClub

ResiClub

Case in point: if their property doesn’t sell, sellers are taking them off the market. Canceled listings are at a 5-year high and increasing into Winter. For more on the whyof canceled listings, check out this quick talk from Altos Research. A nice short analysis on the months ahead.

Canceled Listing #s

So, What’s the Point Again?

Canceled Listing #s

So, What’s the Point Again?

All this is good, very good.

Why?

For homebuyers and investors alike, it will produce the perfect cocktail to snatch a deal! Especially on that ugly home.

We should all take a moment to be in the present. We are likely experiencing one of the strongest buyers’ markets in the last 12 years, right on the tail-end of high interest rates and a homebuyer that is tired of it all. Close your eyes. Take a breath. And remember where you were when you had this opportunity in real estate.

A Worn Out HomebuyerAt this point, after a long 2+ years of inflation and high interest rates, homebuyers are resigned to sit on the sidelines until they can get motivated again. We see this in the moving data. A stat I found interesting: 57% of apartment tenants are renewing their leases, the highest in a decade. Starter-homebuying is expensive relative to historical levels and interest rates have been taking a toll on the psyche of homebuyers.

So, they are Skipping till Spring (or when your lease ends in 2025) and just renting.

JBREC

JBREC

Anecdotally, I have several tenants who are young couples and were originally planning a move-out this year into a starter home. They want to start a family. But are frustrated with prices, interest rates, and the process in general. They all just renewed their lease this summer.

So for investors, and homebuyers who have remained resilient (props to you!), in my opinion, will are starting a new multi-year bull market in real estate.

And you have a 5 month head start.

Remember we are still highly supply constrained relative to total demand, despite this pocket of inventory we are seeing.

Many more homebuyers (and sellers, remember) are waiting for rates to drop, now that the reality of lower rates by Spring is setting in. Pending home sales show us they are taking their foot off the pedal.

Anecdotally, I just picked up another great deal on an ugly house in the country that had been sitting on market. After some elbow grease, this is going to turn into a smokin’ hot deal. I’ll be looking for my next one in November.

My Skeptical Take:

I want to emphasize, once again I know, the unique state of play for the real estate market.

We are currently experiencing a Hot Rate Cut Summer-Fall.

But many buyers are Skipping till Spring.

If you are looking to invest, don’t get stuck in analysis paralysis. Take action.

You have a 5 month head start.

For the Federal Reserve, I expect their first rate cut in one week, by .25%. And the $46 trillion U.S. bond market agrees. In anticipation of rate cuts and a potentially slower economy, in the last 30 days, the 10-yr treasury has come down to 3.629%, with the 30-yr mortgage at 6.22% today. A spread of 259 bps. And I will continue to remind you all of this, if the spread between the two was at normal / historical levels (175 bps), we would be at an interest rate of 5.37% today. Even before the first rate cut. This means that it is within the realm of possibilities for interest rates to end up in the low 5’s, sometime next year.

Forced Sellers this WinterAnother reason why this the present time is such a great time for us investors. Real estate is cyclical/seasonal, and most activity is in the Spring. Folks selling in the off months, especially in the slow winter months, have a much higher likelihood of being “forced sellers,” in other words they’re selling for some life event reason. A move, a death, debt issues, divorce, job change, etc…. They have to sell and they wont be taking the home off the market, they will be reducing price.

Add to this, a housing inventory that is at 2019 levels, and buyers skipping till Spring, and we have quite a cocktail of opportunity for those looking to pick up a deal.

Find Fall DealsSo when are others are enjoying the pumpkin patches and apple picking, the savvy investor is hard at work in the office, scouring listings, running numbers and talking to expert investor-agents to find that Fall deal.

When will Demand Roar Back?This also begs the question, how long will this last? When is demand going to roar back?

Move over March Madness, its going to be Makin’ Moves March in 2025! (I’m full of alterations today, and plenty of coffee).

That should be about the time rates are near or under 6.0% and should be timed perfectly with the hot Spring real estate cycle.

Will Rates go under 6%? Yes.A note, and I’ve said this before. I vehemently disagree with the National Association of Realtors, which claims rates will stop at 6%. Their chief economist Lawrence Yun has lost touch with the market. And you know what they say about economists….

…Well I’ll let renowned mathematician, trader, investor, philosopher, and author of The Black Swan Nassim Taleb tell you, in the colorful way that only he can:

“Those with brains and no balls become mathematicians, those with balls and no brains join the mafia, those with no balls and no brains become economists.” — Nassim Taleb

Boom.

Keep a skeptical eye on statements from economists. It’s a lot of guess work and ego involved.

Again, the spectre of rate cuts and economic worries, mixed with inventory rising is the perfect storm of opportunity for investors. Sharpen your pencils, real estate deals are going to be plentiful for the next 5+ months, likely until interest rates have a 5-handle, IMO.

So don’t Skip till Spring. Put down that apple picking basket. And start running your numbers!

Oh and call your friendly Investor-Agent :)

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße,

Please Share this Article!It takes several hours to write this weekly article, and they will always remain free. All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

Contact Us Here in Nashville!If you are interested in talking real estate investing and digging deeper into any of these ideas don’t hesitate to reach out! I always like a rigorous discussion and helping fellow real estate investors.

Looking for a market to invest in? There is always a bull market somewhere, and one of them is Nashville. Nashville has the lowest unemployment of any major metro, 90+ people per day move here and our city population is still under 700k. Plus, we have 3 professional sports teams, massive healthcare and entertainment industries, large tech and manufacturing operations at Ford, GM, 3M, Nissan, Bridgestone, Oracle etc…, world-class universities, and no state income tax, to name a few.

And these folks need housing!

* I write this myself and get it out for you all on the same day. Apologize in advance for the likley errata. Don’t have a team of editors, yet.

** The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Recession?! Says who?

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Welcome to my weekly post BP compatriots, where you'll get a frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - Recession?! Says who?

- - Economic Review.

- - Quick Nashville Update.

- - Tangent! - There are now more obese children, than malnourished. Wow.

- - My Skeptical Take.

------

Fuel for the Day: Joko’s sugar-free, nootropic, monk fruit blend to pep me up and get me into a flow state. Good human, good drink, with NO crap in it, highly recommend.

------The Weekly 3: News, Data and Education to Keep You Informed

- - Big shakeup at Bigger Pockets online real estate investor community. It appears BP is changing things up after being bought by a private equity group. David Greene is no longer the host and is doing his own podcast, although he will be a frequent guest. We will miss you!

- - Real estate in Dallas suburbs is weakening. Prices are falling and inventory is piling up (Nixon).

- - Education Recommendation: 15 Conversations with Real Estate Millionaires. A fantastic review of successful, everyday real estate investors, and how they did it. Highly recommend.

Today’s Interest Rate: 6.49% (Thursday)

(☝️.15%, from this time last week, 30-yr mortgage)Guten Morgan investors. It’s a lovely day to talk real estate. Let’s get into it.

The American economy remains resilient, corporate earnings are exceeding forecasts (albeit moderately), and real incomes are rising. This continues, despite last week’s yen carry trade tumult, which roiled stock market participants. True US GDP and hiring are slowing, but so is inflation; the perfect cocktail to gently coax the Fed into taking action.

Bob Englehart, Cagle Cartoons

Bob Englehart, Cagle Cartoons

Fed’s Eye is on Labor Markets

Now that inflation is near their target (and assuming it stays there this month), the Fed is on a labor market stakeout. Today, we got the Consumer Price Index numbers, which were right in line with expectations, at 2.9%. Importantly, shelter costs remain stubbornly high and were responsible for 90% of the current inflation increase. Food prices climbed 0.2% while energy was flat. Yesterday, we got the Producer Price Index (wholesaler) inflation numbers, which were on average cooler than expected (.1% vs .2%, MoM). In fact, MoM food and energy prices for producers were flat.

The slow trend of downward inflation continues.

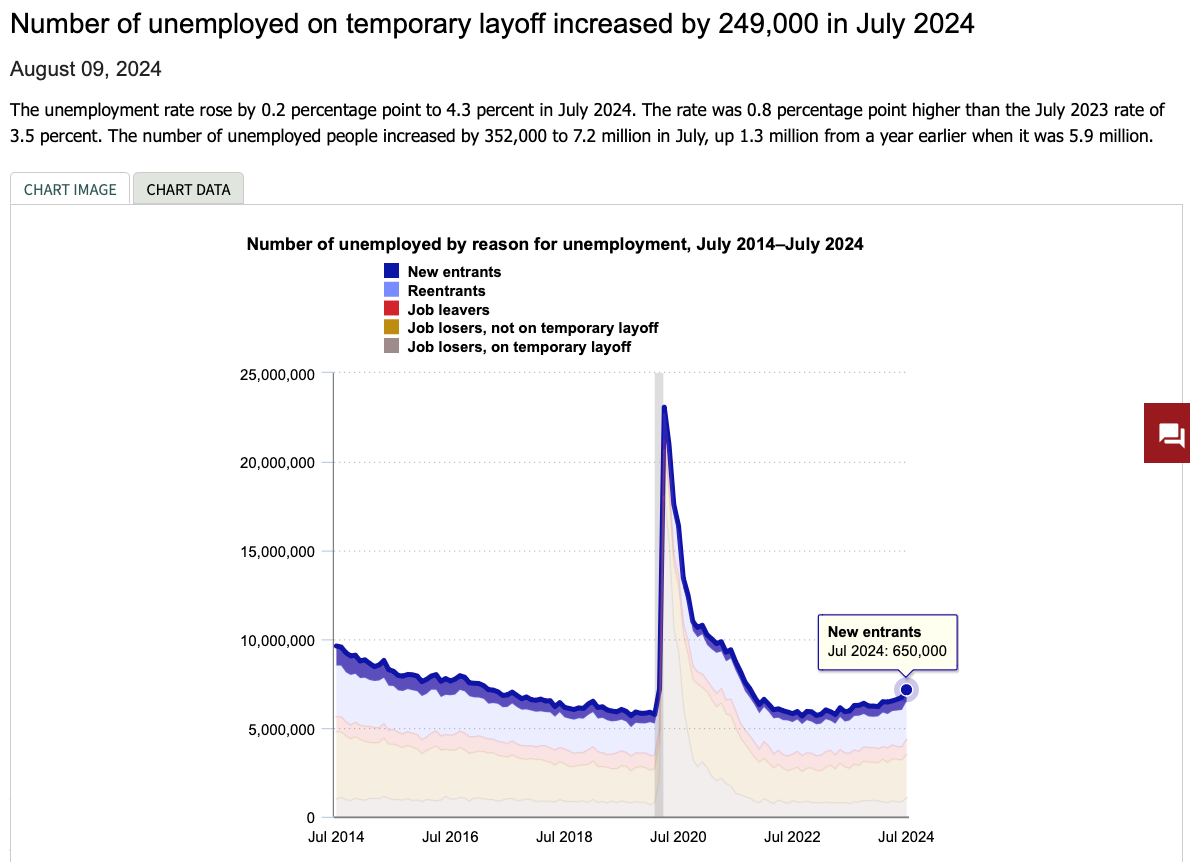

On the labor market side, unemployment ticked up .2% last month to 4.3%, still strong and what is considered “full employment,” which is generally around 5%. If we break above 5-5.25% we will start to get concerned about a slowdown in GDP, which may indicate a future recession. We will continue to monitor this.

Unemployment Types 8/9/24

Unemployment Types 8/9/24

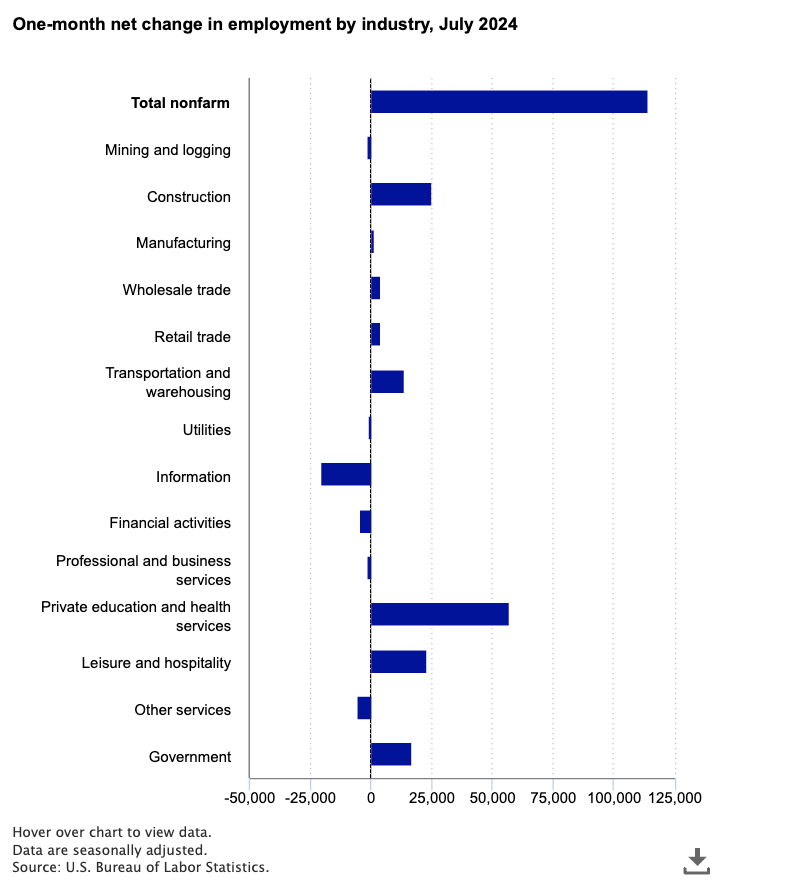

Looking at industry categories, health care, construction, government and transportation / warehousing were stand out gainers, while information / technology, finance and mining workers lost jobs in July. Of note, technology (aka information) was particularly weak.

Employment MoM

Employment MoM

Interest Rates Start to👇 in September.

It is expected that the Fed cuts rates in September, by .25%. But not yet, not in August. And don’t count on an emergency meeting / rate cut, like some of the TV personalities are calling for.

That is fiction.

Fortunately, the bond market is starting to do the Fed’s job for them. In the last 30 days, the 10-yr treasury has come down to 3.83%, with the 30-yr mortgage now at 6.49. A spread of 266 bps. And I will continue to remind you all of this, if the spread between the two was at historical levels (175 bps), we would be at an interest rate of 5.58% today. Even before the first rate cut. This means that it is within the realm of possibilities for interest rates to end up at 5%, sometime next year. I vehemently disagree with the National Association of Realtors, which claims rates will stay around 6%. Their chief economist Lawrence Yun has lost touch with the market. Keep a Skeptical eye on them.

It’s Morning for the Real EstateIf you're looking for signs of a crash / slowdown in the economy, you won't find it in real estate, especially the rental market. Overall demand for rentals, despite rents at historical highs, is strong, with wages growing fast (see above). Of course, again, we will be watching the labor market to for signs of weakening past what we view as ‘normalizing.’

And it’s here that we have to talk about something important. Sentiment. For some reason, there is a feeling of negativity about the economy, stock market and generally about life. My thoughts? I blame the election cycle, and the divisive politics on both sides blaming each other for inflation and stoking fears about the end of democracy. Really?

STOP.This will be an unpopular take, given most of us have picked a “team,” but we will be just fine no matter who wins. Vote for who you want and let’s move on to real sh!t that’s happening in our world, like generating wealth for you and your family through real estate.

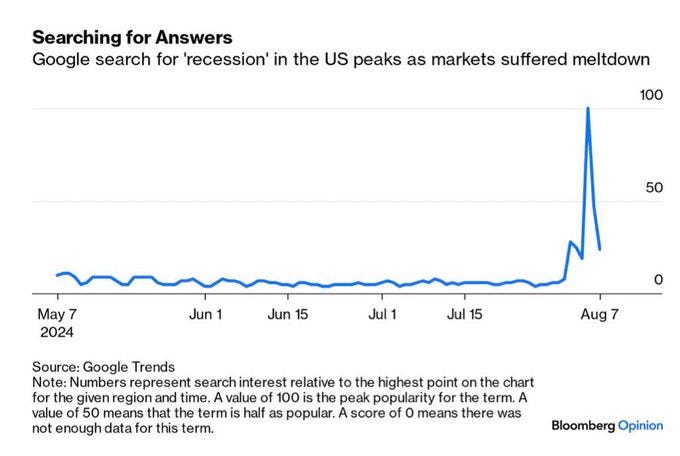

Case in point, there is a massive, gaping disconnect in sentiment between individuals and business leaders. Individuals think the world is ending, and business leaders see the clouds of past recession fears parting. This is a telling positive signal, IMO.

Example: Google searches by individuals for the word “recession” are spiking…

Yet mentions of recession fears from CEOs doing business in the real world are down, and have been, consistently, for the last year.

So how Should We Posture? Bullish.

So how Should We Posture? Bullish.

5 Letters for everyone out there: R-E-L-A-X. We’re going to be ok. In fact, this may be one of the greatest times to buy real estate in my 40-yr lifetime. As I have said before, I believe we are at the beginning of a new 10-yr bull market. There is too much pent-up demand, like a coiled cobra, ready to spring once interest rates tick down.

Here are 3 pieces of evidence:

- - An anecdote, from Redfin: “Recent mortgage rate drops have created an optimal window of time to buy a home before competition and prices pick up….Don’t wait to buy; buyers who were scared off by high rates are poised to enter the market, which may boost prices.”

- - Another anecdote, from my investments: lower rates and higher inventory (aka choices) are bringing out the investors. I had 3 multiple-offer situations last month. First time in over a year.

- - Last anecdote, from a survey of rental investors (ResiClub and LendingOne).

Key survey findings: “Most single-family landlords … are cautiously optimistic, expecting a balanced single-family rental market over the next 12 months. Many plan to buy properties, raise rents, and anticipate rising home prices and falling interest rates. 60% of single-family landlords say they’ll likely buy at least one investment property over the next 12 months.” “And 76% of single-family landlords expect to raise their rents over the next 12 months—including 35% who say the increase will be over 4.0%.”

Very positive market signals.

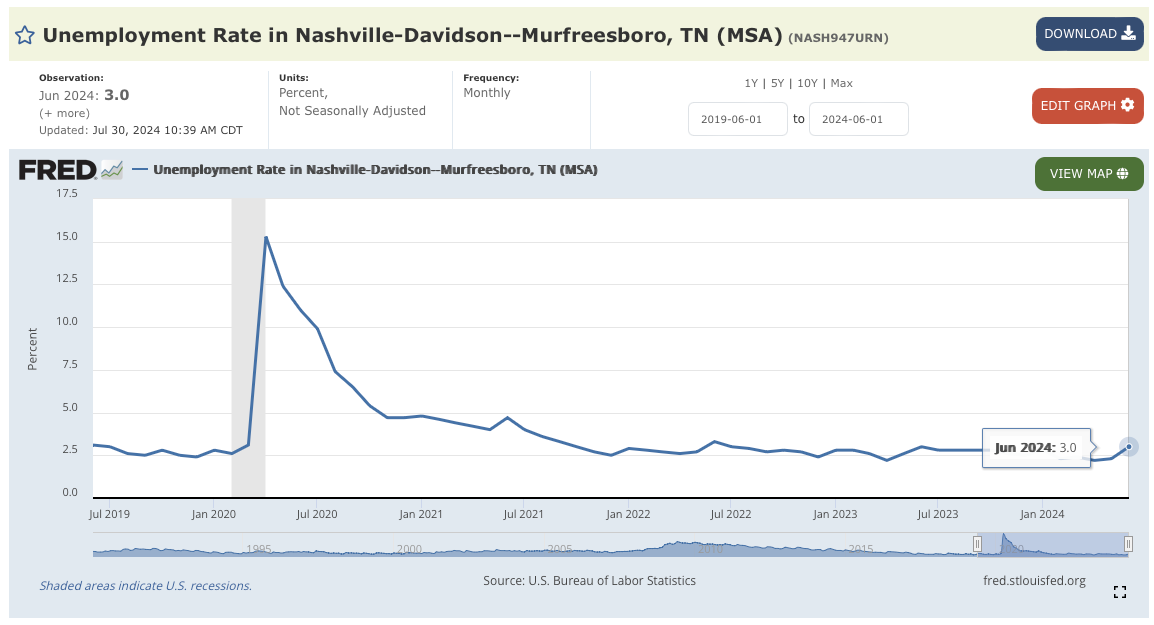

Nashville: A Closer LookSpeaking of labor markets, remember that all real estate is local. And Nashville is one of those steady growth markets that have endured, no matter the macro-headwinds.

For example: unemployment in the Nashville metro area is far below the national average, at just 3%

Nashville has a robust labor market, with heavy manufacturing, technology, entertainment, and health care jobs.

People make and so stuff here.

Today, Nashville still has about 2 job postings for every unemployed person. We aren’t overheating like other markets, just steady growth. And folks continue to relocate here for a better quality of life.

Nashville Development Update

Very cool new development just breaking ground downtown.

“1010 Church St. will. now be known as Paramount (60 stories, 750', 360 apts., 140 condos, 517 capacity garage). It will be Nashville's tallest tower when complete. Foundation work is currently underway (NashUrbanPlanet).”

Our skyline continues its evolution. Amazing.

Sharing is caring. Don’t forget to share this article with a friend, or even a frenemy. :)

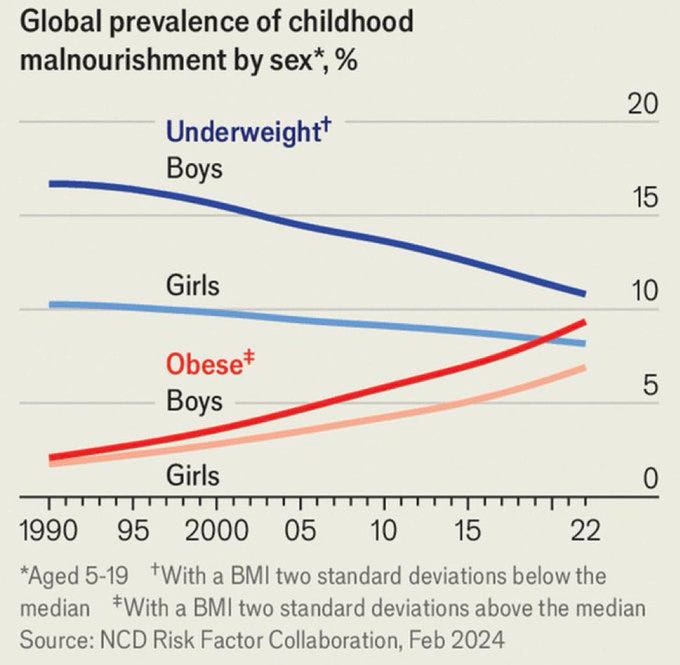

TANGENT!

There are now more obese young folks globally, than malnourished ones.Really?!?!

Global levels of obesity for children and adolescents aged five to 19 years surpassed those for moderately and severely underweight youth from the same age group in 2022 (WHO).

In a world of overabundance, wealthy countries are screwing it all up, and those without, are still very much without.

In light of this, perhaps we all should consider 2 things:

- - Donating to UNICEF to help a child in need.

- - Cutting sugar out of your and your child’s diet. It’s not easy I know, the food companies put it in everything. Literally everything. When you can, as much as you can, COOK! Perhaps watch a free cooking show/chef on YouTube (here are 32 10-minute, simple recipes from Chef Gordon Ramsay) and make some simple recipes at home where you can control the ingredients.

It’s fun, healthier, and far cheaper anyway.

But I digress…

My Skeptical Take:

Business is good. But inflation still be too damn high.

Fortunately, this too shall pass.

Hourly wages are growing faster than inflation, and business sentiment is in a year long positive trend, including small businesses which just reported today as extremely bullish, the highest since February 2022.

People need a home, and they can’t hold out much longer. In my experience, consumers can typically change behavior for about 6 months, then they revert to mean. Cost has prevented this reversion; so homebuyers are stacking on the sidelines ready to buy a home and form a household. Inflation is trending down, as are interest rates. The negative sentiment of the election will soon pass.

It is about to be Morning in Real Estate.

Let’s get after it.

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße,

Please Share this Article!It takes several hours to write this article, and they will always remain free. All I ask is that you share it with 1 friend. If you do, you will get two gifts: free education for one of your friends and good karma for helping to grow the community. You can share it here:

Share The Nashville Investor Agent Newsletter

Contact Us Here in Nashville!If you are interested in talking real estate investing and digging deeper into any of these ideas don’t hesitate to reach out! I always like a rigorous discussion and helping fellow real estate investors.

Looking for a market to invest in? There is always a bull market somewhere, and one of them is Nashville, where we are seeing record tourism this year. 99 people per day move to Nashville and our city population is still under 700k. 3 professional sports teams, massive health care and entertainment industries, more than a dozen colleges….Look for bullish drivers like this.

Looking for a realtor in the Nashville area? We work with the best here who specialize in helping investors find great properties.

* I write this myself and get it out for you all in the same day. Apologize in advance for any typos / syntax errors. Don’t have a team of editors, yet :).

** The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Nashville Contractor Recommendations?

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Happy to share a few as well, congrats on the Reno!

Post: Is the 1031 Exchange at Risk? Inside the Court's Chevron Decision.

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Welcome to A Skeptical Dude’s Take on Real Estate: a frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Coming at you live from Nashville, TN.

Fuel for the day: I realized one thing I should be buying in bulk is coffee, I sure have enough. So I picked up a 5lb bag from Black Rifle. Highly recommend if you want to save a few shekels.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - Fed Comments by Jerome Powell

- - A Skeptical Look: The Chevron Decision Could be a Big F*$%*%g Deal!

- - The Skeptics Take.

- - The mortgage market is experiencing a severe recession. It's one of the worst mortgage downturns in history. Mortgage purchase apps are at the lowest levels of the post 1995 era (Lambert).

- - Love high-speed rail AND Taylor Swift? Well you are in luck. The high-speed rail ride to Miami will have sign along trains to her next concert. (Trains)

- - Are Homebuyers OK with Small Lots? A record 65% of new single-family detached homes sold in 2023 were built on lots under 9,000 square feet, per the latest Survey of Construction (SOC). Unclear how many home buyers want/will accept lots that small. Or just keep renting/waiting (mortgagetruth).

Today’s Interest Rate: 6.99%

(👇 .09%, from this time last week, 30-yr mortgage)Briefly, because I want to get right to our main topic of today’s newsletter, a few comments on what Jerome Powell said on inflation this week.

Speaking in front of the Senate Banking Committee yesterday, Powell was questioned about everything from inflation to odd political issues and grandstanding. The takeaway?

In short,

- - Powell is serious about smashing inflation, saying of the inflation in the 1970’s: “People [the Fed] didnt get in there and get it done, so inflation kept coming back.”

- - Powell is not going to come to the rescue of the housing market. When asked about it and if in his opinion we should build more “affordable / workforce housing.” He responded: “This is a job for you. But let me say this, I am aware that housing is in short supply.”

Powell also reiterated that:

- - unemployment while still low is steadily notching higher;

- - job and wage growth while still strong are steadily moderating;

- - inflation is moderating, on trend, and the Fed’s target of 2% is on the horizon.

The Bottom like: I still think we get interest rate cuts in September, and a second one after the election. It is becoming harder to justify a restrictive 5.5% federal funds rate.

The Chevron and Loper Decision

A new Supreme Court Decision may Hopefully Bring Clarity and Efficiency to the Mortgage and Housing Market.

A recent Supreme Court ruling may bring impactful regulatory changes to the housing market, and people aren’t talking about it.

So, let us.

First, what’s the Chevron doctrine?

For nearly 40 years the courts have been of the opinion that they should defer to a federal agency / regulator and rely on their interpretation of a law, if it is ambiguous or unclear.

No longer.

Now, courts will provide a check on federal regulators. From the decision: "Courts must exercise their independent judgment in deciding whether an agency has acted within its statutory authority. " More specifically, on June 28, 2024, the Supreme Court overruled the previous Chevron framework in the Loper decision (H.K. Law). Previously, under the Chevron doctrine, when a court determined that a statute was ambiguous or that Congress had not directly addressed the precise issue in writing a given law, the Court, rather than applying their interpretation of the law, would instead defer to the regulatory agency’s interpretation.

In other words, the courts will now interpret whether regulators are acting lawfully in applying new regulations instead of allowing them decide themselves, again when the law is reasonably unclear. The Supreme Court has now made clear that it "remains the responsibility of the court to decide whether the law means what the agency says (H.K. Law)."

A Double-Edged Sword?Thinking objectively and trying to remain intellectually honest, the Chevron decision likely cuts both ways. Although I do on the whole, today, think this was the right decision. However, the original ruling allowed federal regulators to function efficiently, which they cannot if every interpretative gray area in the law requires a court decision.

But, Chevron also allows federal regulators to be judge, jury and executioner in matters of law. So, IF the agency is working in the public interest, we would want them to exercise broad interpretations of a given law. For instance, in regulating chemical companies to not pollute with new novel chemicals in our rivers and oceans, without needing a new law from Congress.

But when corporate interests or lobbyists (trying to stay a-political!), or frankly just well-intentioned government regulators looking to stay active in their bureaucracy (I have personally seen this) get involved, then that same interpretive leeway gives the regulator even more power at the expense of the public interest. Think, the USDA brining armed feds to shut down Amish farmers for selling their unpasteurized milk, or the FDA allowing harmful chemical additives in our food that are banned in hundreds of other countries.

And too often, businesses complain about a lack of clarity in a given regulator or lack of regulation. For example, in many instances, the regulator does not reveal how to stay within the law. The federal agencies don't have to do that. They just have to say that you broke the law, and no explanation is really needed. Think the Crypto industry, who is literally begging for clear regulations.

One example: Coinbase just sued the SEC for a lack of transparency in their regulatory policy, saying that “Financial regulators have used multiple tools at their disposal to try to cripple the digital-asset industry.” And noting that the SEC “has claimed sweeping authority, but refuses to provide any rules, let alone consistent or coherent ones.”

Got it?

Ok, So what’s the big deal with overturning Chevron for Real Estate?The Court's decision in Loper will create a sea change in administrative law with wide-ranging implications and potential opportunities for highly regulated industries, like the real estate.

This will create an opportunity for more efficiency and lower costs in the real estate economy. It also means more time is needed to see how new challenges in the Courts will affect things like Fair Housing, HUD and FHA regulations / costs.

In short, if you are operating in a business that touches any part of the housing economy, this likely will affect you. Startups, bankers, mortgage lenders, home builders, technology companies, new finance / fintech, estate planners, CPAs, wealth managers….. all will be highly affected.

But don’t take my word for it, let’s see what a few industry professionals are saying of the Loper decision:

- Mortgage bankers - “The [Loper] decision… will be welcome news to the mortgage industry. One of the principal industry concerns about the vast power granted to the Consumer Financial Protection Bureau was that these powers were too insulated from review….The ruling sends a crystal-clear message to federal agencies that their powers are not unlimited…We would not be at this point today if government agencies were more prudent and consistent about staying within their statutory authorities, grounding their rulemakings in empirical facts, and heeding appropriate procedural safeguards…Instead, too frequently, our regulators appear to be chasing headlines and short-term political wins.”

- National Association of Homebuilders - “Today’s Supreme Court ruling is an important step forward to advance meaningful regulatory reform because it means that federal agencies can no longer continuously change the law – and the intent of Congress – by implementing their own interpretation of statutes as long as the interpretation is viewed as being ‘reasonable.’…Today’s ruling that overturns Chevron means that federal agencies will now have less discretion to impose new regulations that Congress did not clearly authorize.”

- Real estate attorneys - "The most specific [impact] is in the multifamily context because they're living under the Fair Housing Act, and that statue is very broad and ambiguous, and HUD in particular has had a great deal of latitude in setting guidance and bringing enforcement as to what they believe should be the law even though it's not congressionally written as such."

- And here is an anecdote from a mortgage lender: “I work in mortgage and I think this is huge for us. We would call the CFPB for clarification on what was/wasn’t allowed for advertising and they would refuse to answer, but would give us $10,000+ dollar fines if we guessed it wrong (@mortgagenmore).”

The Loper decision will likely lead to a surge in challenges to IRS authority / rule making. The IRS has made thousands of interpretations of tax policy. Heck, my CPA and I regularly discuss and are forced to make our own assumptions on how the IRS may interpret something in our real estate taxes, if we were to get audited. It’s super unclear. And there are so many small carveouts for special interests in IRS interpretations. For example: Is the 1031 exchange at risk? Should we even allow it and does it help or hurt consumers? According to the IRS, “Gain deferred in a like-kind exchange under IRC Section 1031 is tax-deferred, but it is not tax-free.” However, in practice it often is a tax-free exchange when applied to real estate. Will this change?

On Real Estate Transactions CostsWhy is it so expensive to even do a real estate transaction? What are all these fees and why are they continually going up? Why am I forced to buy title insurance that insures the lender, not me? Will the CFPB install new regulations or fewer? Will those lower costs or increase the burden on lenders, which I have to pay for? Why is recording the deed with the county so expensive, can we use technology (like crypto) to make this process more efficient? Why does it often take 3-4 years to build something?

You can see how this gets complex quick.

On Building Big Infrastructure in the USAAnd, if I may be so bold, a note on larger infrastructure that obviously affects the real estate economy: What about large infrastructure project that get bogged down in litigation? Can we start building bridges, roads, electric infrastructure, high-speed rail, and large impressive buildings in this country again?…

It took 13.5 months to build this in 1930. Let that sink in.

Empire State Building

Empire State Building

…These are just a few of my thoughts bouncing around in my noggin. And there are probably hundreds of positive use cases we aren’t even thinking about today. We need more startups in the industry!

The Skeptics Take:

Business craves clarity, and there is a hope across industries that allowing the courts back in to check the Executive Branch will help ease the perceived burden of overregulation.

But time will tell.

Anecdotally, I witness much frustration in the mortgage industry. I hear often that lenders often don’t know why a regulator interprets the law this or that way. Nor do they always provide explanation for their decisions. One can imagine this makes it difficult (ie more costly) when adequate guidance is not given. Businesses don’t operate well with uncertainty, in this case mortgage lenders. So one would hope that this provides certainty of what regulations are and are not lawful.

Technology in banking, particularly at “FinTech” finance / bank companies that do not have a physical presence has been often difficult to start / operate. This ruling may be helpful in allowing more alternative lending institutions participating in the housing market. Using Bitcoin and cryptocurrencies to purchase real estate and, perhaps even more importantly, creating Smart Contracts or Tokenization to record real estate ownership etc… comes to mind. These ideas would create efficiencies in the real estate transaction, lowering costs to purchase real estate, and also to democratize its ownership. To date the regulators have not given adequate guidance, or just flat out banned, many technologies.

Objectively, and on the whole, it seems quite odd that the Chevron doctrine was in place for so long. And I get that in the 1980s the worry was that the courts would be activist so the Supreme Court decided to instill the power of deference in the Federal regulator. But, isn’t this how checks and balances work? Isn’t this why we have 3 branches of government who have equal power to check the other? Seems crazy that we have allowed regulators for 40 years to ostensibly be judge jury and executioner.

Lastly, it is important to note that the previous Chevron regime only applies when a regulator acts in the void, when they make a rule that the law does not reasonably address. As the third branch of government, Congress can always act to change / clarify for businesses and regulators the law they originally wrote.

But on the whole, is Loper as a positive opportunity for decreasing regulatory burden on businesses and consumers alike.

But, Congress, please keep a watchful eye, ok?

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße,

-Andreas

P.S. Just a lovely scene. (And where I wish I was typing this from).

@valentynedreams

@valentynedreams

* I write this myself and get it out for you all in the same day. Apologize in advance for any typos / syntax errors. Don’t have a team of editors, yet :).

** The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: Newbie mistake - risks associated with installing unpermitted bathroom?

- Real Estate Agent

- Nashville, TN

- Posts 266

- Votes 143

Highly recommend you get it permitted! And Nashville / Davison county is not California. If you are straight with them they will work with you. My 2 cents.