All Forum Categories

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

All Forum Posts by: Andreas Mueller

Andreas Mueller has started 49 posts and replied 177 times.

Post: Taxes for Rent by the Room House Hack (Can I take a PAL?)

Post: Taxes for Rent by the Room House Hack (Can I take a PAL?)

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Nothing to add to tax side. Just want to say great strategy! had 2 clients buy places to House Hack and rent by the room. Good on ya!

Post: Interest rates Higher for Longer? Good.

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

In the words of famed real estate mogul / investor Barbara Corcoran.....

"If rates go down just another percentage point, that's what I'm hoping for by year-end, prices are going to go through the roof...Everyone will come out and buy. There are probably 10 buyers on the sidelines waiting for interest rates to come down that are actually active in the market. So everybody's going to charge the market...I wouldn't be surprised if real estate went up by another 8 or 10% if interest rates come down."

Post: Interest rates Higher for Longer? Good.

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to A Skeptical Dude’s Take on Real Estate: a frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Coming at you live from Nashville, fueled by today’s amazing beef jerky and caffeine of choice. No AI generated content here folks. Nie!

Today We’re Talkin:

- - The Weekly 3 - News and Data

- - Interest rates Higher for Longer? Good.

- - Bad Government Fiscal Policy is Driving Inflation

- - Nashville is Just Getting Started. A Closer Look.

- - The Skeptics Take: Bad Vibes in the Market? Good.

- - “On current facts, a rate cut in June would be a dangerous and egregious error comparable to the errors the Federal Reserve was making in the summer of 2021. We do not need rate cuts right now.” (Larry Summers)

- - Boston Dynamic just unveiled their newest Atlas robot. This is not a render. Wow (MKBHD).

- - Nashville is Booming. But like all growth cities, affordability is worse. We need incentives to boost supply of new homes and light housing density (ResiClub).

Today’s Interest Rate: 7.50%

(WAY☝️from this time last week! 30-yr mortgage) Interest rates Higher for Longer? Good.Well what a week. Rates are up nearly 1/2%.

What do I think?

As one of my favorite men on this whole earth, Jocko Willink, is fond of responding when a seemingly unsavory thing /problem happens. “Good.”

Spill your coffee? Good, now you get a fresh cup. Got beat? Good, time to learn/get better. Interest rates high? Good, market normalizing (keep reading).

When something is wrong, or going bad, there is always going to be some good that comes from it, or and advantage that YOU need to find. Always. The power of is a remarkable thing.

So what’s good about high interest rates? They suppress demand for homes, build inventory of available properties, crowd out HGTV posers, and allow for us real estate investors and first time homeboys to negotiate for a better price. If you can stomach that 7.5% mortgage for 12-18 months, you will be able to refinance to a lower rate, having bought an asset for less than its market value. Good. Disagree with this? Message me, I always like a healthy debate.

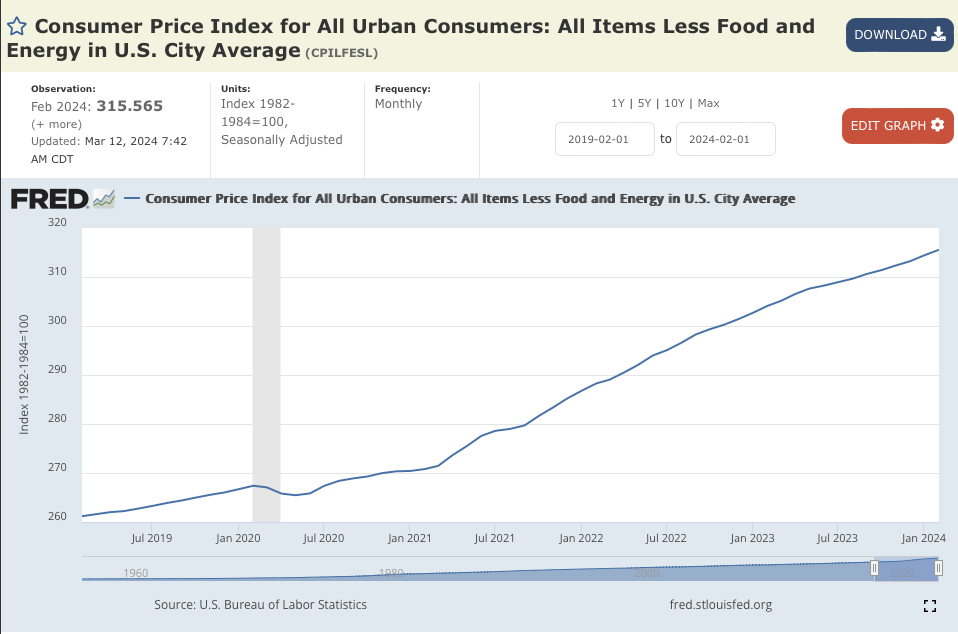

A Quick Word on InflationLast week was a big week for economic data, most notably consumer and producer inflation data (CPI and PPI). While consumer prices came in hotter than expected (for the 3rd month in a row) and markets roiled on the news, producer/wholesale prices came in lower MoM , coincidently by the same amount. (.1%), and +2.1% YoY. PPI is the preferred measurement tracked by the Federal Reserve.

But I loath merely tracking the inflation horse race like much of the media enjoys doing. So let’s just say this on the topic and be done with it: inflation is higher than we would like and is remaining sticky. It’s going to be volatile and right now that trend is hotter. IMO this is because of government fiscal policy, ie spending.

Bad Government Fiscal Policy is Driving InflationDeficit spending is a snake eating its tail: deficit spending → more inflation → higher interest rates to slow inflation = more inflation = keep interest rates higher → debt more expensive / accelerates…..repeat.

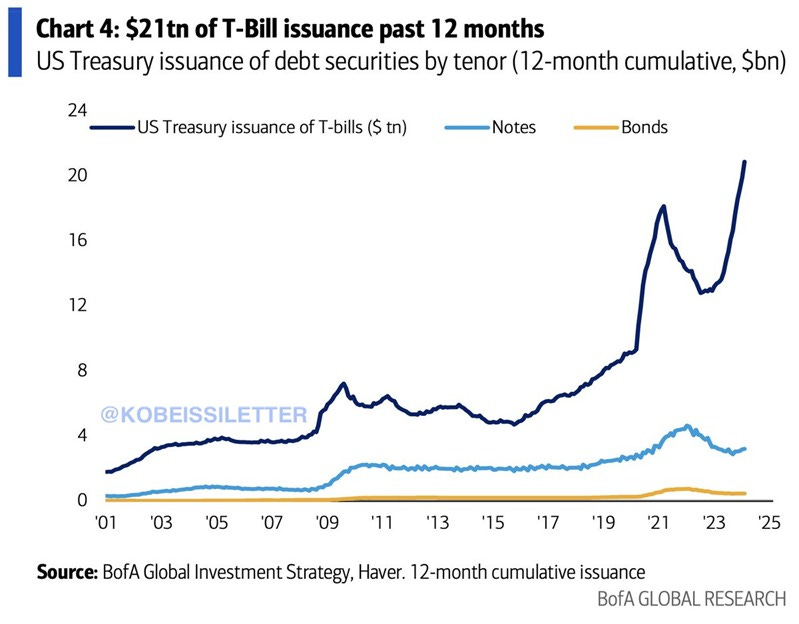

The US debt has is currently rising by $1 trillion every 100 days, or roughly the budget of our entire defense budget (which is larger than the next 10 countries combined). In one year, the US Treasury Dept issued $21 trillion in treasury bills to fund the spending of the federal government (Kobeissi). Lot’s of folks (mostly rich) are making real money from Uncle Sam, gettin that government paper! (must watch).

Hey Congress. Ease off the gas pedal will ya?

So, you think today’s prices are too high …?

You’re gonna love these prices in 5 years.

A Closer Look: TennesseeLet’s switch gears, and do a brief, closer look at a part of the US that is doing quite well: my home base of Tennessee. Yes, I’m biased, but it's my article, so we’re going to check out Tennessee and use tons of semicolons, which my former boss (hi Nick) always redlined. No more semicolon handcuffs!

But I digress…

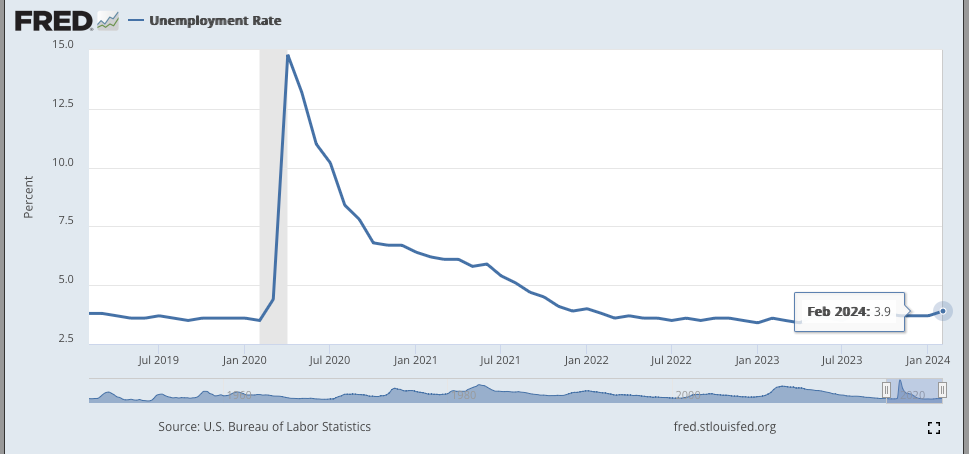

For backdrop, despite high inflation, the labor market is holding up well. Unemployment is ~steady at 3.8% and new unemployment filings fell 11k last week. Within that data, only 6 states increased their hiring from last month, led by Florida (56,000). But the runner up? The 3x smaller state of Tennessee (35,000).

CNBC recently did their Cities of Success expose on US cities that are booming with a wide variety of activity. The first city they visited? Nashville. And it’s not just because of the music or tourism industry, which is what most folks think about when they think of Nashville (who spend $27 million / day). It’s heavy manufacturing, finance industry, health care, Tech Giant presence, 3 pro sports teams (and hopefully an MLB team), zero state income tax, and nearly 1100 companies have located to nashville in the last decade. Let’s dig in.

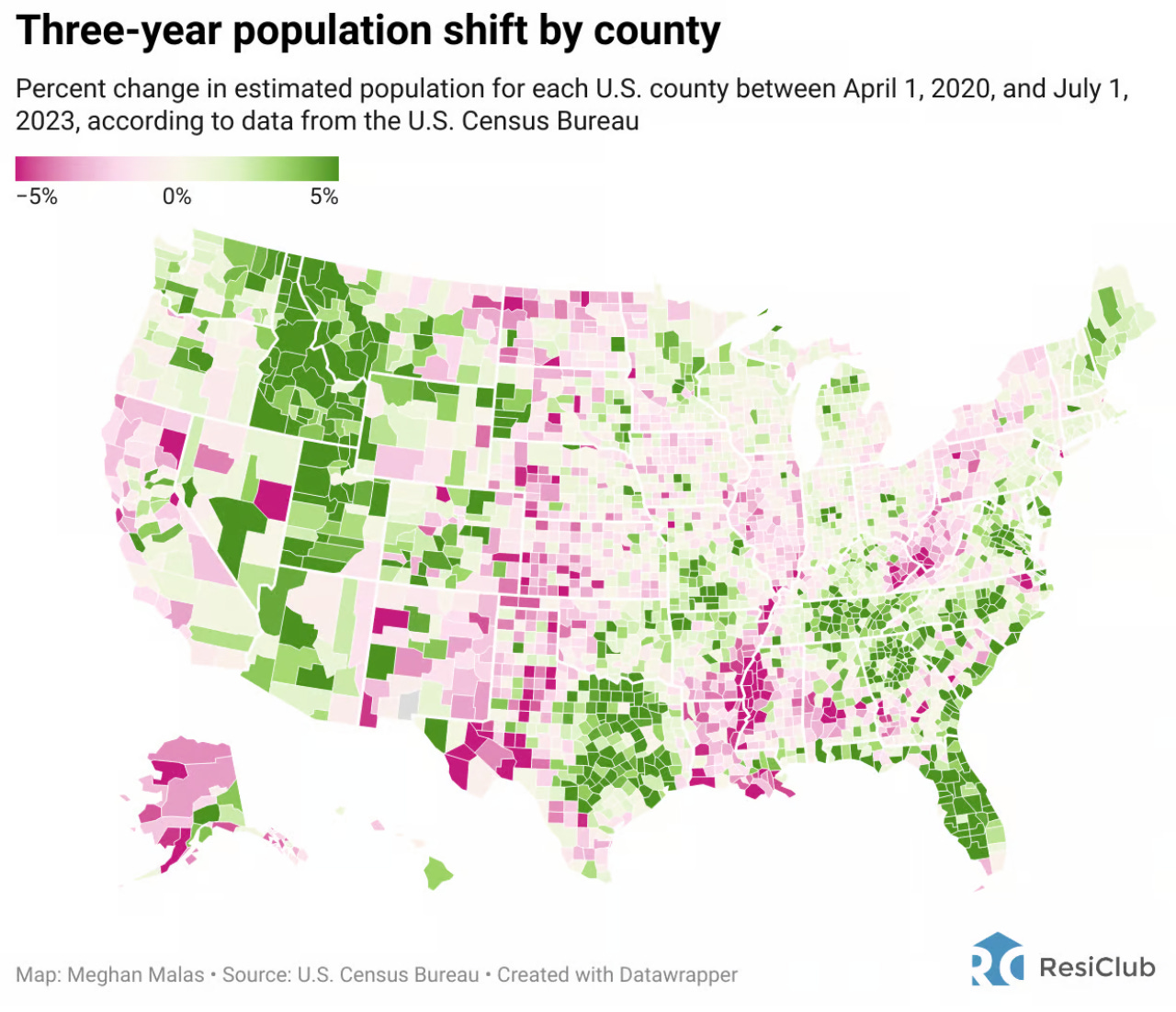

Steady Population Growth

Steady Population Growth

Tennessee is growing, steadily for decades and is one of a handful of states that have continued to do so in nearly every corner of the state. This, without having a housing bubble or other economic meltdown, like some counties in Utah, Texas, California, Washington etc…2022 was particularly strong as folks flocked to the state

Heavy Manufacturing is booming near Nashville: Both GM and Ford have / are building their new EV battery plants here. Just this week Ultium Cells (GM+LG) delivered the first cells to GM from its plant just south of Nashville. GM (and Nissan) have their auto plants nearby as well. It’s also the home of manufacturing for 3M, Bridgestone, A.O. Smith, Tyson, Schneider Electric, Hankook Tire, General Mills, Mars…to name a few (Chamber).

Food!

“I’ve cooked whole hog in a lot of places, but none quite like Broadway,”

Tennessee is known for its’ BBQ, mainly in Memphis. But that is steadily growing in Nashville, which is finally a burgeoning foodie city. Case in point: James Beard Award-winning chef Rodney Scott is opening his newest BBQ joint right on the downtown strip. Whole Hog BBQ.

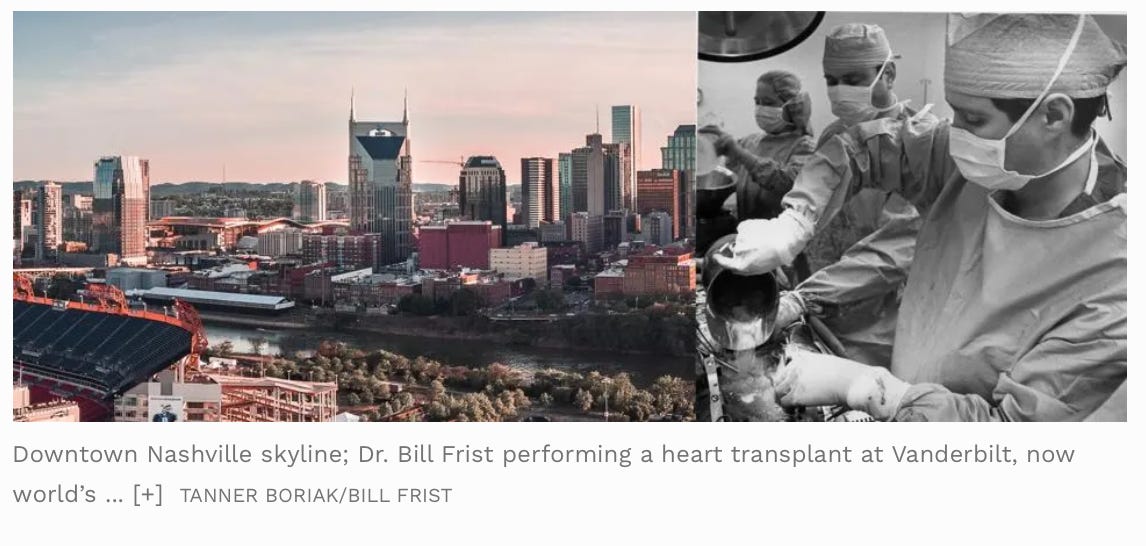

Health care is one of the largest industries in Nashville, and the US.

Health care is one of the largest industries in Nashville, and the US.

Health Care brings in $67 billion annually to the area, 7x the size of the entertainment industry. More than 500 health companies are located in the Nashville area. HCA has 35 million patient encounters annually, more than any. Vanderbilt Health is one of the top heart transplant programs in the world, something many of us, myself included, may need in the future. And it’s not just about private business. Nashville is home to two major medical schools, Meharry Medical College and Vanderbilt University Medical Center. Vanderbilt is the largest clinical training center in the Southeast, with over 1,000 residents and clinical fellows training in more than 100 specialties.

Here is a fantastic write up of health care services and its growth in Nashville (Forbes).

I could go on and on. We didn’t even get to the new waterfront or Titans stadium developments, but I’ll stop there, for now :) We’ve got jobs for every type of interest and a deep entrepreneurial spirit. Oh and did I forget to mention 0% state income / low property tax, limited government regulatory interference and pro-real estate policies for developers/investors?

Suffice it to say, come visit!

The Skeptics Take:

I remain quite positive on the real estate market, although certain asset markets may be experiencing turmoil. Stock and bond markets are taking the inflation news with zero grains of salt. Stocks have so far fallen ~4% MoM and long dated treasuries are down ~4.2%. I have to reiterate again this week: Mr Market may be starting to realize something further than just today’s inflation rate. It may be that the Fed may never get inflation under 2%. IMO the new 5-yr avg base rate for the Fed is going to be 2.5%-3%. And I officially lowered my rate cut prediction last week to 2 cuts (from 3) in 2024, at .25-50% each (while the bond market is also pricing in just 2 cuts, from 6).

On Interest rates: Ironically, high interest rates may actually be helpful to help us return to a more normal real estate market. But there are many other options that governments can take to incentivize productive behavior. Here is a short list in the time it takes to finish my coffee:

- - STOP deficit spending at the current rate. Current young generations are shouldering this inflation and we now see the consequences. The Congress and Administration need to really get our fiscal house in order. It’s been too long since ideological opposites Bill Clinton and Newt Gingrich were able to strike a budget deal. Why can’t we do that again? Not to get political, but getting involved in new wars is not helping.

- - Incentivize supply of new homes, NOT demand (as the current Administration housing plans do). We don’t need housing programs that give folks $ or provide incentives to BUY homes. That is counterproductive. We need to boost supply.

- - Crack down on the building regulatory, permitting etc…process. This one is on states. Time is money.

- Incentivize medium density / small Multifamily development. CA (and other states) are starting to do this. Good damn job CA.

- - RV and Mobile home parks. Incentivize their utility costs and construction. There is nothing wrong with this type of living. I would go as far to say “Mobile Home Parks are the last true affordable housing.” - Andreas S. Mueller (I don’t own any, but I want to).

I have more, but finger workout for the day, done.

What are yours?

That’s it for this week. If you are interested in talking real estate investing and digging deeper into any of these ideas don’t hesitate to reach out! I always like a rigorous discussion and helping fellow real estate investors.

Looking for a realtor in the Nashville area? Shoot me a note! We work with the best here, all specialize in helping INVESTORS find great properties.

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: A Skeptical Real Estate Investor - Inflation is up, now it's a Trend.

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Thanks @Marian Huish, glad you liked! Ha. AI isn't that snarky. Yet...

Post: A Skeptical Real Estate Investor - Inflation is up, now it's a Trend.

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to A Skeptical Dude’s Take on Real Estate: a weekly frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Coming at you live from Nashville, no AI generated content here folks.

Today We’re Talkin:

- -The Weekly 3 - News and Data

- -Inflation Report Today!

- -Real Estate Doomsdayers be Damned!

- -I am …. Postive?

- -The Skeptics Take: Good Vibes in the Market.

- -11 Studies, 1 Conclusion: Housing market is underbuilt (ResiClub).

- -Would the Fed actually RAISE rates? Possibly, if inflation keeps rising (Bloomberg).

- -President Biden says Fed will Cut Rates this year. "Before the year is out there’ll be a rate cut.” (Bloomberg)

Today’s Interest Rate: 7.06%

(Flat from this time last week, 30-yr mortgage)Today is a big day for us folks in the arena, it’s inflation day for consumer prices (CPI). Price action today will be heavily watched, more than usual. We have had 2 months of higher than expected inflation numbers. So according to NBA Jam rules, we are “heating up.” A hot inflation number for March, a trend it would make. And many believe, myself included, that if the Federal Reserve sees a trend up in inflation, they will be less inclined to lower interest rates. After, all, why would they? The economy is humming and we have very low unemployment (3.8%).

So get to it Skeptical Dude! What does today’s CPI number tell us?

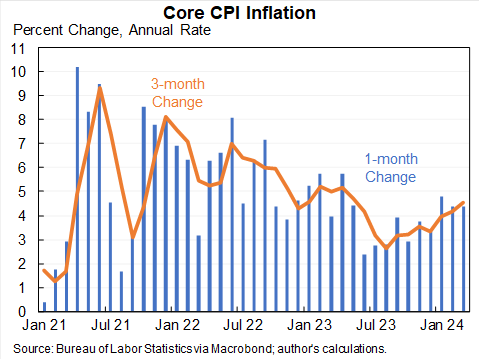

January and February were not seasonal irregularities. CPI was up 3.5% YoY.

This was hotter than all estimates by the big financial institutions and higher than CPI in February (3.4%):

- Kalshi: 3.4%

- Barclays: 3.4%

- Citigroup: 3.4%

- Deutsche Bank: 3.4%

- Goldman Sachs: 3.4%

- JP Morgan: 3.4%

- Morgan Stanley: 3.4%

- UBS: 3.4%

- Bank of America: 3.3%

Core CPI has risen at a 4.6% annual rate, faster than any three month period from August 1991 to 2020 (Furman).

In the words of oft-cited economist Mark Zandi of Moodies Analytics… “Ugh. March CPI was a bummer…”

Ditto.

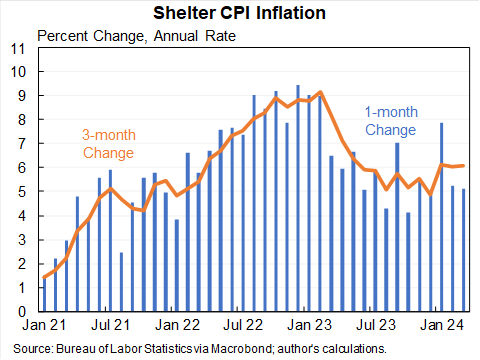

Shelter inflation is one of the major forecasts by economists watched by real estate investors. And the assumptions most economists made in projecting inflation numbers these past few months was that shelter would come down from its 9% to the 2-3% range. It hasn’t; in fact, it seems to have bottomed / plateaued at 5.5%. In fact, in fact… core goods (stuff you can buy) are underperforming services (people do/provide labor for you). In fact, In fact, in fact…Much of services’ increase is shelter. Shelter and gas prices were more than half the monthly increase for all items measured in the CPI for March.

Of note, recently you may have read quite a lot about the tremendous apartment unit growth we are in the midst of (as I have written about). But it hasn’t had a significant effect above the market’s ability to absorb that supply. Anecdotally, in Nashville, where we are in the middle of an apartment supply “surge,” rents are not ebbing. Not for anyone I know. This despite article upon article of impending supply doom!

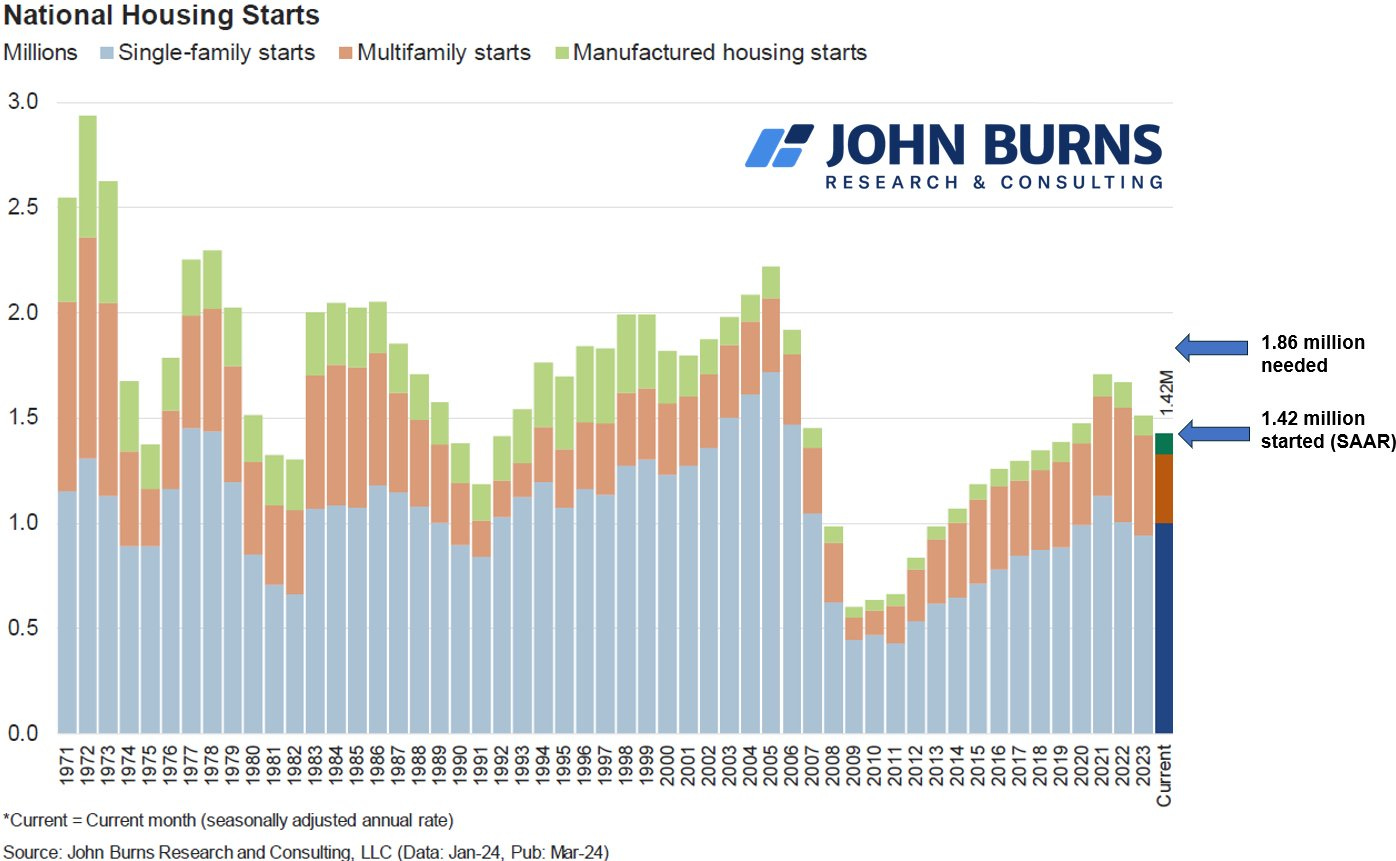

Slight Tangent!By the way doomsdayers…. a “surge” of housing supply is good thing. The US housing market is deficient in its supplyfor homes and apartments both, which is why price growth hasn’t abated. If we had more supply, that would be great for these things you may remember…people. “To keep up with annual demand, the US needs 1.86M new homes (for-sale and for-rent) per year through 2033, based on underlying demographics and current undersupply. We're currently starting homes at a [rate] of 1.42 million homes, ~400K fewer than needed.” (JBRE)

Real estate investors are long term thinkers and are a part of their community. We need a healthy supply of homes. It’s not healthy for the longterm viability of the/a housing market to be structurally undersupplied. The benefit of raising rents in the short term, on the back of strong demand, is far outweighed by a potential structural supply problem over the longterm. Those backs will break. Plus, high inflation and shelter costs hurt productivity, damaging economic growth. Large multifamily developer/operator worried about a high vacancy rate? It’s your fault if you built into your numbers ever exploding rent growth. That’s on you. Skeptic investors know you have to be conservative in your rent projections and ensure resiliency in a potential downturn.

Speaking of which. There are soooo many of these doom / salacious articles re: housing apartment supply. Like this one. And this one… and this one…

Are you wanting for an economic crash?

Blah, gets me fired up! I need more coffee now. Side note, just tried a new coffee this week: Death Wish coffee. It’s fantastic, super bold. Especially the dark roast. Highly recommend.

But I digress….

The Market may be Sniffing Something OutAs it stands today, the stock and bond markets are taking the inflation news with zero grains of salt. Stocks have so far fallen +1% and long dated treasuries are down +1.5%.

The market may be starting to realize something else than just inflation. It may be that the Fed may never get inflation under 2%.

So what? Why do I care? You are too Skeptical, Dude.Well, to complete the sentence of Mark Zandi above…. “Ugh. March CPI was a bummer… and will surely delay the Fed’s first rate cut.”

I agree.

I am officially revising my rate cut estimate for 2024 from three .25% cuts to two .25% cuts. While the Fed may cut in June or July, to signal to the market all is healthy and / or to provide confidence (or for us conspiracy theorists because it’s an election year), they will then pause. Mortgage interest rates will remain elevated for a longer time period and I am estimating we won’t be back to an attractive rate - below 6%, where folks storm back to the market and feel comfortable leaving their home w/ a low interest rate mortgage - until the 2nd or 3rd quarter 2025. I would say 5-5.5% is the sweet spot for when folks will demand will rush back, partially due to mortgage payment affordability and partly psychological, after seeing both 8% rates and 2% rates in just the last handful of years. JBREC has a great chart on this:

Higher for longer interest rates could be a GOOD thing for the real estate investors.

Higher for longer interest rates could be a GOOD thing for the real estate investors.

High interest rates will continue to suppress demand for homes, build inventory, and allow for buyers to better negotiate for home prices. If they are able to afford that 7% mortgage for 1-2 years, they can then refinance having bought an asset for under what it will be worth in a “normal” market.

In the words of famed real estate mogul / investor Barbara Corcoran:

"If rates go down just another percentage point, that's what I'm hoping for by year-end, prices are going to go through the roof...Everyone will come out and buy. There are probably 10 buyers on the sidelines waiting for interest rates to come down that are actually active in the market. So everybody's going to charge the market...I wouldn't be surprised if real estate went up by another 8 or 10% if interest rates come down."

The Skeptics Take:

I remain quite positive on the real estate market, and asset markets in general.

Inflation has risen a few months in a row, but barely, and much of that growth is concentrated as of late. We are still likely on the down slope, but it will be more cross-country vs slalom. Up, down, flat, up, flat, down, down, repeat…

And to quote Economist Mark Zandi for the third time today, “[The Fed’s] got everything they need to start cutting rates…It’s just a question of precisely when.”

The housing market is improving, the supply of homes on the market is up double digits this month, and in my business I am seeing a healthy spring flow of demand for both homebuyers and investors. Very healthy. I had a few multiple offers last week. That was 2021 nostalgic.

Home prices, like wages, aren’t likely to go down (deflation) but we are likely to see the rate of increase slow as the Fed keeps rates restrictive (lower inflation, disinflation). I am still on alert for stagflation. This last longer than folks think + harm labor market = stagflation. Labor numbers remain important to watch. So far not though.

But for now, call me positive. It’s Spring! Get out there and start doing. My home market of Nashville is heating up, literally. And I bet your local market is too.

Don’t be an armchair sourpuss critic. It’s time to get in the arena.That’s it for this week. If you are interested in talking real estate investing especially here in Nashville, reach out! You can message me right here on BP.

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: On Tap This Week - Housing Inventory Data Deep Dive

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to A Skeptical Dude’s Take on Real Estate: a frank, hopefully insightful, dive into real estate and financial markets, from one real estate investor to another.

Coming at you live from Nashville, TN.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - When will the Fed cut rates? Why not now? Mortgages be too damn High!

- - Housing Inventory Data Deep Dive.

- - Tangent - Gas Station Air Compressors are a scam!

- - The Bottom Line - Good time to Buy?

The Weekly 3: News and Data to Keep You Informed

Today’s Interest Rate: 7.06%

(☝️ .15% from this time last week, 30-yr mortgage)Bah, we are back to a 7 handle. I was hoping interest rates might start to melt-lower but alas, it was not meant to be.

Interest Rates: The Trend is your FriendSo do we know where are interest rates headed from here? Not exactly.

And anyone that tells you different is one of two things:… lying or stupid. Especially the online Gurus. Just like the stock market, nobody can predict when it will go up or go down. Too many variables. Not even Warren Buffett and Charlie Munger can, or even attempt, to do this. It’s “impossible and stupid.”

But we can analyze trends. The stock market trends up, over the long term, ~8%. And the economy is cyclical. The economic machine, as complex as it is, moves in cycles. So the right question is, where are we in the cycle, and thus, is it more likely for interest rates to be on the up trend or down trend?

So now that we’ve found the right question, what is the answer? Well that’s difficult too.

I’ll take a stab at it.

We are most likely on the down slope. But we aren’t downhill skiing, it's more cross-country. A little up, little flat, little more down, repeat…

Economist Mark Zandi agrees, “[The Fed’s] got everything they need to start cutting rates…It’s just a question of precisely when.”

Why Hasn’t the Fed Cut Rates?

Inflation and unemployment are their primary signals and are telling a very different story. Inflation is not ebbing. PPI, the Fed’s preferred measure of inflation, popped up last month, and PCE, CPI and PPI have been resilient to up in the face of the fastest interest rate increases in history and Quantitative Tightening, where the Fed stops buying corporate and government debt to reduce liquidity in the economy and slow financial markets. Economy resilient, yes, but that also means prices continue to creep up. Moreover, the market has been surprised by higher than expected inflation numbers this year. Year to date, we have seen 6 negative inflation prints, 4 positive, and 2 flat prints. Markets hate surprises. It is also contributing to high bond spreads (and thus higher mortgage rates).

How about employment? This week’s ADP jobs report shows a steady labor market, a little different than last week. Nothing special but steady. US companies added 184,000 jobs across most job categories and wages rose, the most since July.

Without a drop in inflation and a labor market that remains steady, the Fed doesn’t have the signal to cut rates. Why? Their restrictive policy hasn’t worked (yet). So why ease and risk, in all likelihood, a reaccelerating of the asset markets, most likely the stock market, and for sure the real estate market. This could create a bubble or even worse, run away inflation.

You think eggs are expensive now? Well you may live to see a real life golden goose.

The Fed is in a very difficult position. Should they cut rates?

Steve Eisman (ala the Big Short, played by Steve Cornell), is pushing for the Fed to not cut rates, saying it could create a bloated stock market and potential crash. I agree, and as I said last week we could be in an era of the dreaded Stagflation. But rates are killing the housing market, which is at historically low inventories. Lowering rates would bring back some affordability for monthly mortgages for homebuyers.

What’s better, juice the stock market or housing market?

The value of the US stock market is ~$50.8 Trillion. Cutting rates now while the economy is humming and inflation is still strong could create a bubble, leading to a recession.

The value of the US real estate market is ~$52 Trillion (close to the same, fun fact). Keeping rates high could destroy capital intensive activities and businesses. Leading to stagflation and bankruptcies. Bad times for Commercial real estate, small businesses, car buying, and just the average Jane trying to buy a house for the fam. Anything that you need a loan to operate/buy/grow.

The Fed may be damned if you do, damned if you don’t….

But What do the “Experts” Think?

You know how I feel about experts… but consensus thinking is helpful to monitor for us Skeptics. Here is what they are saying:

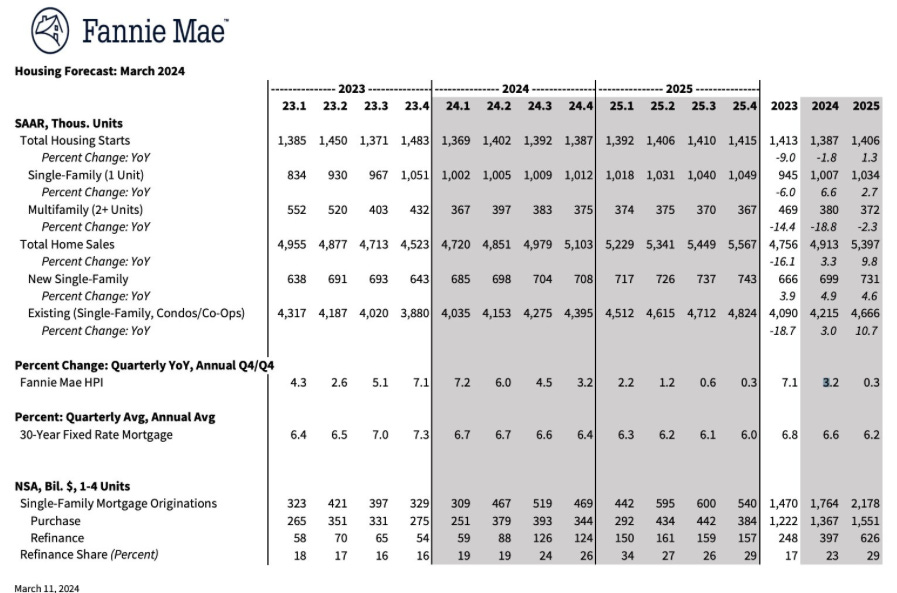

The Mortgage Bankers continues to forecast a higher 6%+ mortgage rate for 2024.

Fannie Mae (and Freddie Mac) recently revised their predictions to higher in 2024 as well: 6.7% in Q2 2024 (previously 6.3%) 6.6% in Q3 2024 (previously 6.1%) 6.4% in Q4 2024 (previously 5.9%).

Wells Fargo: 6.65% in Q2 2024, 6.45% in Q3 2024, 6.15% in Q4 2024. I.e. the Fed and bond markets will remain higher and restrictive.

The Fed is Bad at Predicting % rates

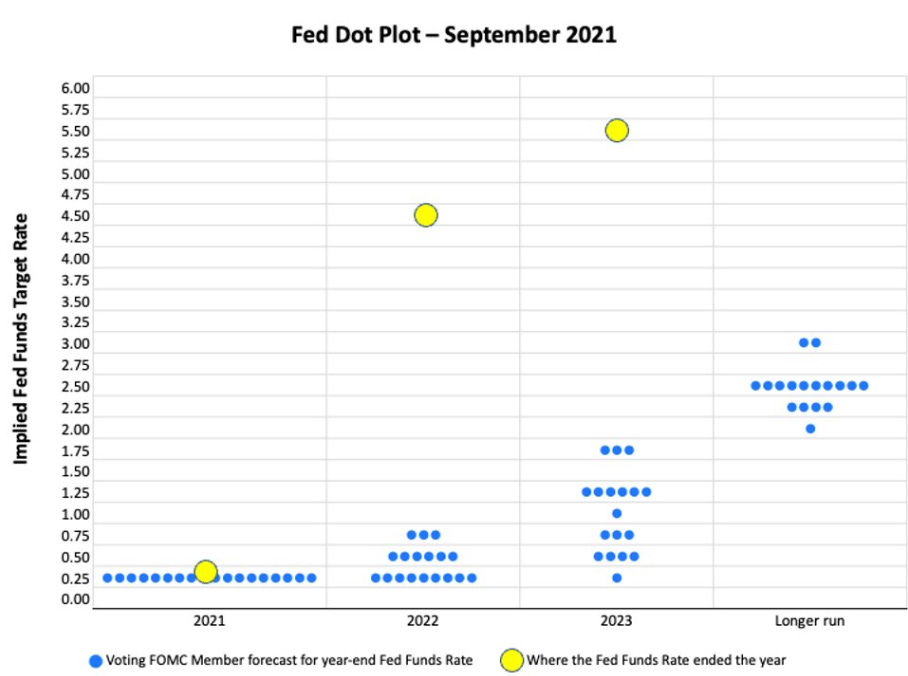

All that being said, the Fed has been just terrible at forecasting to the public what interest rates will be. In Sept 2021, the Fed predicted rates would end 2022 at 0.5% and 2023 at 1%. They were only off by a massive 4% for 2022 and 4.5% in 2023. So take predictions by the “experts” with a crystal-sized grain of salt.

TANGENT Alert! - Gas Station Air Compressors are a Scam

Have you too noticed that your Honda’s tire is a little low and tried to use a gas station air compressor station lately?

If so then you know… they are a legit scam!

I went to 5 last week to fill up my low tire. The result: 3 were completely broken, 1 shut off half way through and then broke, and 1 took my $4 and spit in my face. Want your money back? Well the air compressor station is always owned by a 3rd party, not the gas station. So they say “call this 1-800 number to get a refund,” which also doesn’t work….F%#*

I finally bit the bullet and got a $30 portable air compressor, great for my frequent long road-trips. Can’t recommend higher.

Freedom!

But I digress…

The Good News: Real Estate Market Supply is Picking UpBack to Real Estate. The good news is inventory of available homes is starting to pick up. This is extremely important on the road to returning to a more normal market.

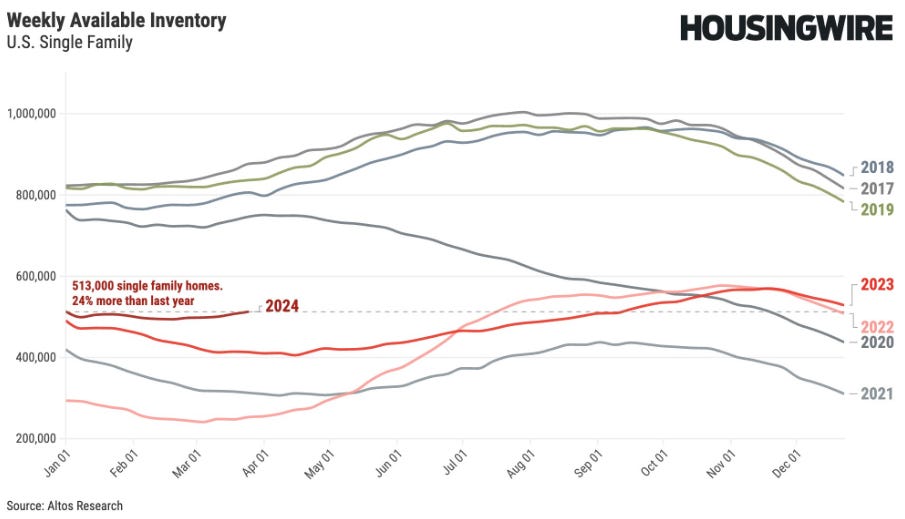

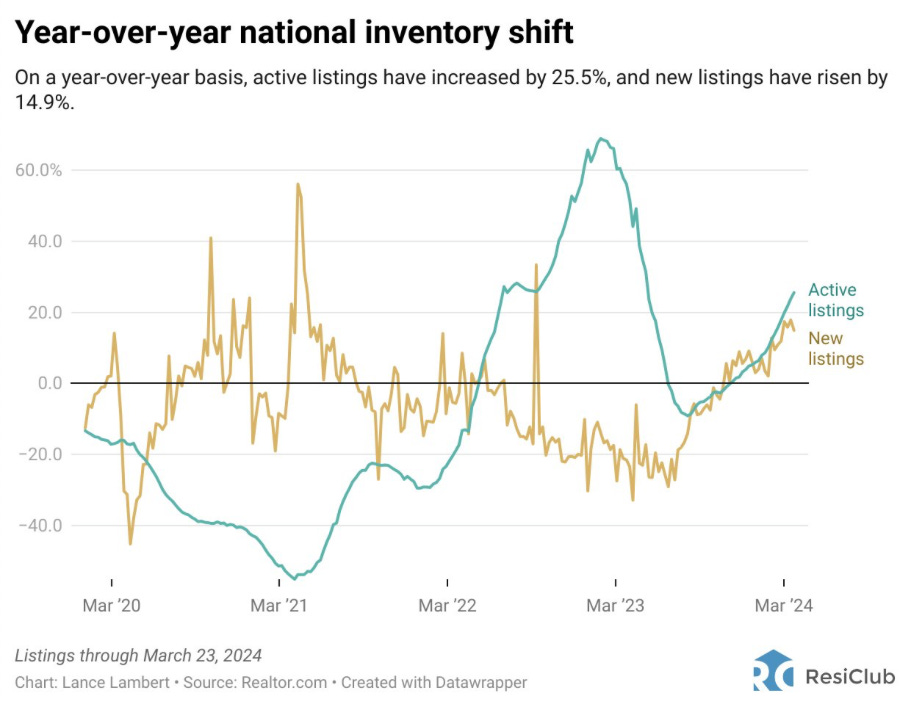

According to Altos Research/HousingWire : 513,000 single family homes are on the market: 24% YoY, and 102% than two years ago.

The interesting part is that in 2022, mortgage rates and inventory were marching together higher quickly. At the time inventory was growing much faster than it is now. In 2023 supply growth slowed more, but started to catch back up toward the end of the year.

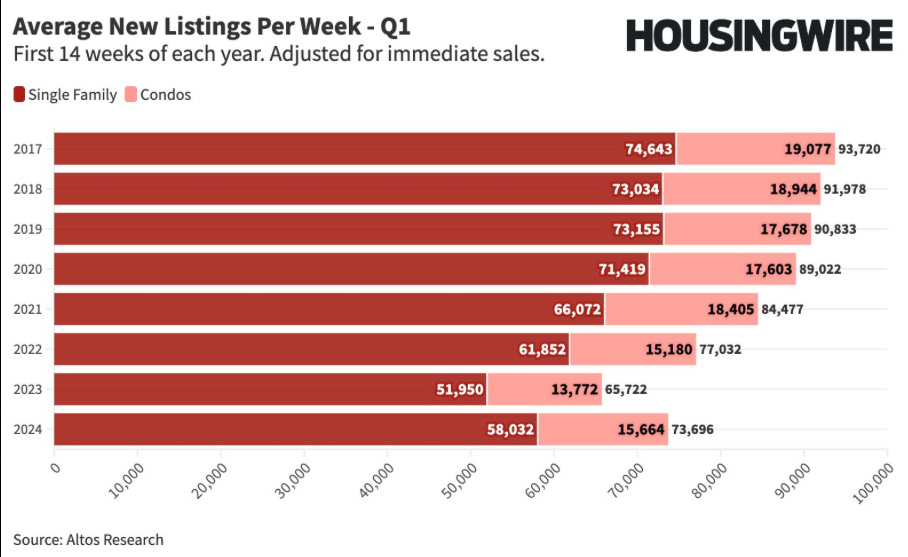

What about 2024? I agree with Los Altos’ analysis. I see supplies continuing an upward trend, albeit slower than one would like (up ~1% last week). There were 60,000 new listings and 17,000 sales, total new sellers are 14% more than in 2023. If we continue this trend, more sellers will mean more sales in 2024. But until the new listings rates gets back to closer to 80,000 per week in March, we’ll be below 2022 levels of housing activity. We currently stand at 8% more sales than 2023 but 15% fewer than this time in 2022.

Putting this in perspective see previous years’ new listings data, since 2017.

The trend is your friend. ☝️

This date is corroborated by housing analyst Lance Lambert. U.S. new listings +14.9% year-over-year U.S. active listings +25.5% year-over-year.

In my home city of Nashville. We are below trend, supply is extremely low and new listings are not growing as we are seeing on average in the US.

And…

The Bottom Line

In short, folks are feeling starting to feel kinda, a little, sorta more comfortable putting their home on the market, at least for these first few weeks in 2024. But not everywhere, like some growth markets like Nashville, where prices are more rapidly appreciating (we were up 9% last year, double the US average). Perhaps people are seeing prices marching higher and rates not moving, so they are worried they may have already “missed out” on buying home altogether?

Stop it. Don’t. That’s monkey brain thinking.

That’s not rigor. It may feel uncomfortable or risky to buy something that seems "expensive. But as I’ve written on in the past, assets (homes, stocks, bonds etc…) appreciate over the long term and, remember, you can’t time the market. Owning an investment property is much much better than keeping your money on the sidelines.

The Skeptics Take: I hear many “experts” talk bout how we need real estate transactions, new listings, inventory/supply etc… to increase in order to quell real estate prices.

But, let’s be real. Home prices, like wages, won’t go down.

They may stagnate but they wont meaningfully deflate. For once, I agree with über-annoying real estate Guru Dave Ramsay:

“If you’re thinking about buying a house… and you’re waiting on real estate prices to come down or interest rates to drop, don’t wait. Buy a house now if you’re ready. The prices aren’t going to come down, and you can always refinance the interest rate.”

So what are you left to do?

Just do it. Jump in. I am.

Most Interesting Tweet(s) of the WeekBreaking, Fed’s Powell sees inflation as too high still but the recent higher inflation numbers as “bumpy” but still overall trending down. I.e. Fed is likely to NOT increase rates more (some were worried) and will keep rates constant/higher for longer. The Fed’s posture is to wait for when to cut.

That’s it for this week. If you are interested in talking real estate investing and digging deeper into any of these ideas don’t hesitate to reach out! You can message me right here on BP. I always like helping investors.

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: The Fed's "No Landing" Scenario may mean Stagflation.

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to A Skeptical Dude’s Take on Real Estate: a frank, hopefully insightful, dive into real estate and financial markets, from one real estate investor to another. Coming at you live from Nashville, TN. Interested in Nashville real estate? Let's chat!

What am I listening to? - Classical music tracks from video games. They are actually pretty amazing. But yes….nerd alert.

Where am I? - An undisclosed location in Tennessee. Just a man, his laptop and his pooch.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Is Scary Stagflation Really Here?

- - The Bottom Line

- - Baltimore Bridge Collapse: the economic disruption doesn't look like a threat to broader supply chains. (AXIOS)

- - Broccoli Sprouts are Cancer Fighting! Study shows growing broccoli sprouts at home and consuming them daily counteracts carcinogenic effects of chemicals in food / environment. I’m putting this one here again this year. I’ve seen too many cases of cancer lately. Get some broccoli sprouts! (Amazon Link).

- - Nashville Waterfront Development Starts to Take Shape. 30 acres of mixed-use development on the East Bank, anchored by a $2.1 billion domed stadium for the Tennessee Titans. (BizJournal)

Today’s Interest Rate: 6.91%

(👇 .18% from this time last week, 30-yr mortgage) Economic CheckupThe economy is looking strong, and we always want to strongest economy we can get right? But, is it possible for it to be too strong? There actually is this weird scenario, just past goldilocks, and closer to Alice in Wonderland, where the economy keeps chugging along…. slowly, household incomes crawl ahead, corporate earnings play duck duck goose, unemployment (usually) rises and inflation stagnates. Economists call this Stagflation. You may hear folks also say the phrase “no landing,” referring to the Federal Reserve being able to avoid a recession but inflation remains. The two could actually become one.

It’s a no bueno situation.

Why is this bad? It is because the Federal Reserve and Federal Government may not be able to utilize their standard monetary and fiscal remedies for inflation or unemployment as effective bullets against stagflation. In fact, there is no agreement amongst economists on the best way to stop stagflation.

Stagflation, Are we There…Yet?A year ago economists, Wall Street’s smart money, and pretty much everyone that calls themselves an investor was predicting a recession. I will include myself in that camp. Screaming high / fast interest rates employed by the Fed, $10 Trillion in federal spending, extremely low home sales, corporate earnings revised lower and lower, inverted yield curve for Treasury Bonds, etc…, all indicated a recession on the horizon.

Fast forward to today, and these same folks have reversed. The US economy was able to plow through those storms and avoid negative GDP growth. The main factor, unemployment didn’t plummet along with everything else. We are still under 4%.

The consensus (my skeptical ears perk up when I hear that word) amongst the finance community then became a“soft landing.” Here we expect inflation to slowly fizzle and GDP to remain positive, but slow. This is still the predominant thinking.

We have had several months of steady everything. Inflation is not dropping as the Fed hopes. I fact PPI, the Fed’s preferred measure of inflation, popped up last month, and both CPI and PPI have been resilient in the face of the fastest interest rate increases in history and Quantitative Tightening, where the Fed stops buying corporate and government debt to reduce liquidity in the economy and slow financial markets. Again the US Economy is remaining quite resilient.

All things being equal, this would be good. But again, inflation is not abiding and unemployment, layoffs, job switching, job quitting (JOLTS) are all showing signs of worsening. These things are happening.

Now, 45% of investors believe the economy could head toward stagflation.

Now, does this mean we are headed to a crash, bang, scary, violent, bad, awful, wrong, impossible, disastrous, hate, worst, hell…. fill in the media headline hyperbole…problem? Not necessarily, and there is reason for much optimism. But us Skeptics are always on alert to protect our downside.

For us real estate investors, if we are in a stagflation environment, we can expect that the Fed will keep interest rates at their current elevated levels or more slowly cut rates over the course of 2024/2025. Keep an eye on inflation and unemployment specifically. If we see inflation flatline / rise slightly and unemployment slowly rise, together, that could be a sign the economy is stagnating. Fed Chair Powell has now seen 2 months of hotter than expected inflation reports, saying at a March 20 press conference that these reports “haven’t really changed the overall story, which is that of inflation moving down gradually on a sometimes bumpy road toward 2%.” This may be the case, hopefully. But the data doesn't fully support this optimism and that they should be cutting interest rates. I agree with former Treasury Secretary Summers, who said “My sense is still that the [Federal Reserve] has itchy fingers to start cutting rates and I don’t fully get it.”

Remain on guard.

I’m a positive pessimist, I see opportunity everywhere and when my spidey-sense starts a flashing’ I pay close attention to certain indicators for signs I may want to button down the hatches (put money in money markets, ramp down stocks, buy more real estate assets, other fun strategies…), so here are a few more indicators to watch, all you smarty-pants Skeptics out there: (This is not financial advice).

Economic / Financial Indicators to Watch:- Stocks have had a fantastic run this year, up 10% and up 23% the last 6 months. If the Fed cuts rates in June I see this as bearish for stocks; but, bullish for real estate. And I’ll be bull riding bullish if they follow through with 1-2 more cuts this year and bond spreads ease.

- Speaking of stocks, it makes everyone feel rich (well the 60%+ of folks who own stocks). This may be one reason folks are willing to get back into crypto in a major way. And not just Bitcoin (which I own) but the “meme coins” too, it’s getting 2020/21 wild! There are also other reasons for bitcoin to be bullish, but not as much the alt-coins. Watch out. Bull markets create bullsh%t.

- On Real Estate. One of the major sticking points in this market is supply. We are at a 50 year low and 2022 we had a housing supply/sales recession (see here for my post on supply/demand). One indication to watch is housing sales and new listings, these will show if the liquidity is going back to the market. Homes sales increased significantly last month, 9.5% year on year. And inventory of available existing homes increased 5.8%. Both positives for the market. But one month doesn’t make a trend. Keep an eye on this. And by the way, prices went up, it’s never a perfect time to buy. If you are waiting on something to magically happen, well…

…. it’s going to be a long wait.

Bottom Line

Warren Buffett once said, “The first rule of an investment is don’t lose [money]. And the second rule of an investment is don’t forget the first rule. And that’s all the rules there are.”

Hear hear.

The Skeptics Take: The best way to maximize your upside is by protecting your downside. Protect that capital you have because getting it back is much harder. As a quick example, if the value of something (house, stock, asset…) goes down 33%, it will have to rise 50% just to get back to where it was. Go ahead, pull out your calculator. I’ll wait.

Protect your downside, watch your 6, trust but verify, invert always invert, avoiding stupidity is easier than seeking brilliance, avoid crazy at all costs… all reiterate the same basic idea. This is the golden principle for investing. After all, it’s your money. So it’s your responsibility.

Stay Skeptical, but positive. There is always opportunity.

Most Interesting Tweet(s) of the WeekWOW. I can’t stop looking at this amazing eagle.

That’s it for this week. If you are interested in digging deeper into any of these ideas or just want to talk real estate investing don’t hesitate to reach out. You can message me directly right here on Bigger Pockets. I'm also a realtor in Nashville and am the GP of Klout Capital.

Again, stay skeptical y'all.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: The Real Shrinkflation? It's not potato chips. It's....Real Estate.

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to my weekly article, which I dub 'A Skeptical Dude’s Take on Real Estate,' coming at you live from Nashville, TN. Every week I write a brief, hopefully insightful, dive into real estate and financial markets, for all you tubular dudes and dudettes out there.

What am I listening to? - 90’s Rap, getting my Monday started off right with a little Biggie.

Where am I? - Nashville coffee shop, Frothy Monkey on 51st. Fantastic latte. But the bacon the today was… meh. Y’all gotta make that fresh to order people.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Rate Cut Downgrade

- - The REAL Shrinkflation

- - In Case you Missed it: The President’s New Housing Proposals are Problematic

- - The Bottom Line

- - Inflation is remaining Stubborn. Prices for everyday things like eggs and shelter are rising faster again (Axios).

- - Broccoli Sprouts are Cancer Fighting? Study shows growing broccoli sprouts at home and consuming them daily counteracts carcinogenic effects of chemicals in food / environment (NIH, Amazon Link).

- - Nashville University Belmont Embracing AI in Education (NBJ).

Today’s Interest Rate: 7.09%

(☝️ .17% from this time last week, 30-yr mortgage)Well, crap. Mortgage interest rates are not “calming down” as I said last week. We are back up above 7%. Bond market did not like the inflation data that came out in the PPIat the end of last week and sold off. Mist!

Several of the ‘large finance houses’ took notice too, GoldmanSachs now sees 3 rate cuts, beginning in June. This is a revision from 4 cuts, beginning in March (and I believe this is their 3rd forecast revision showing fewer and delayed Fed rate cuts).

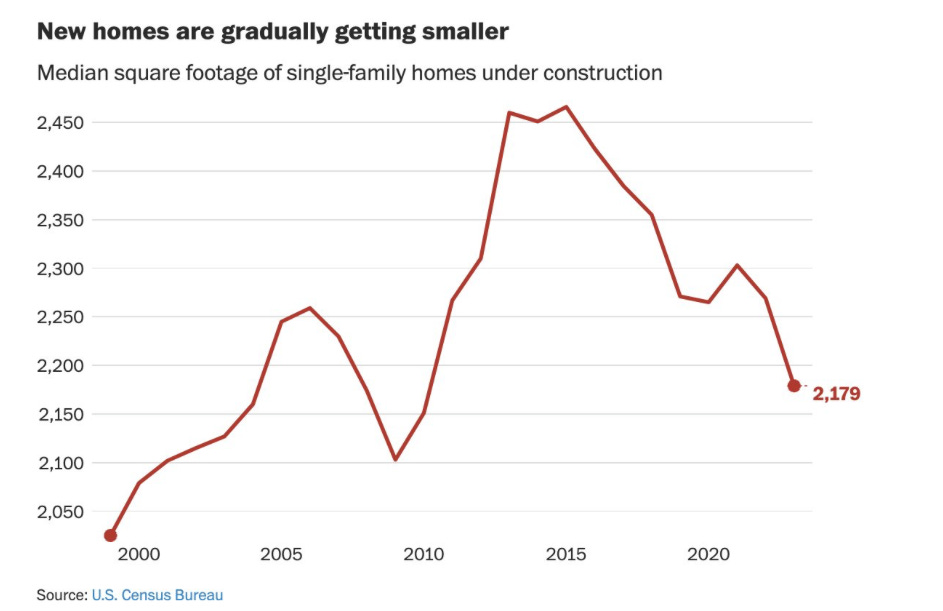

Shrinkflation

Shrinkflation

There is inflation and now we have “shrinkflation,” where something appears to not be as expensive / the same price but the size of the offering is now smaller/less. Even the President is talking about it, bringing it up both during the Super Bowl and again during his State of the Union address. But this topic has mainly been around consumer goods, “Hey my bag of Doritos is now 10% smaller” etc…. But you know what else is shrinking? New homes.

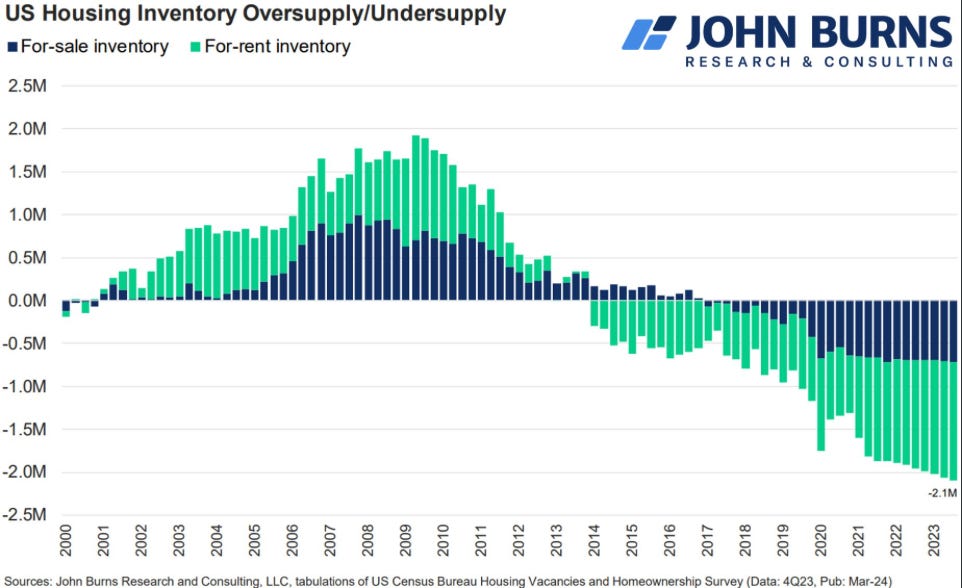

Housing Shrinkflation and Home PricesHomes are also getting smaller, well new homes that is. The median new home size is now 2179 sq/ft, down ~11% since 2013. However, we are seeing more townhomes being built, which often are smaller on average than a single lot / single family home.

Price are still up however. Why you ask? Supply is low low low. High interest rates body-slammed supply numbers in 2022, as I detailed last week. This was part of the “most significant homes sales crash ever, and still, in 2024, homes sales are trending at all-time lows,” says economist Logan Mohtashami. Active homes for sale normally are 2-2.5 million. Today, we are at less than half that, 1 million. And when we had our last housing crash it was a very unique time. Housing inventory was at 4 million. So we are in a very different time today. This is why the housing market, in terms of home prices, has remained so robust despite high interest rates.

If we want to slow the rapid appreciation of home prices, we need more supply. The cost of homes, rent, shelter etc… is still outpacing wages and most types of goods/services. We see this in the inflation data. We need to tame prices and to do that we need more supply. One year ago, housing economists said the U.S. housing market was “undersupplied by 1.7 million homes.” Now, they say that number is 2.1 million.

Home prices continue to appreciate too rapidly. I say this as a real estate investor, who benefits from home price appreciation. But I have long term thinking, not quarter to quarter. The last few years is not normal. For a long term healthy market (which I would argue is most important) we should prefer a more steady / predictable price appreciation, not something this rapid. Something will break. I don’t know what, but something will.

Can we roll back prices?In short, no. And you DON’T want that. For home prices to disinflate back to 2019 levels, home prices would have to crash 41%. Millions of homeowners would then be underwater on their mortgage - owing more than it is worth - and would likely foreclose / declare bankruptcy, creating a credit crisis, unemployment would spike to 10%+ and on and on… No, no the price of homes, and really everything we pay for, is here to stay. This is the long-term price of inflation (no pun intended). What we should want is for the rate of price appreciation (inflation) to level off in the 2-4% / yr range. That’s what the Fed is trying to do for total inflation (their number is 2% but that may be difficult for a while) by raising their Fed Funds rate.

You want to know what the real shrinkflation is? It’s combining the inflation numbers with the higher cost of credit/borrowing. Remember, the Fed raised rates because of high inflation. So both things were happening at the same time since 2022. So, for example, rather than the peak of 9% inflation last year, adding the cost of credit on top of that we actually peaked at 18% last year. This cost of debt comes through where people have to borrow to afford the item, like a car, or business Capex and of course, a home. This explains why consumer sentiment has remained depressed despite unemployment being extremely low and inflation is down dramatically (9% to 3.2%).

Y’all likely know this already. You have seen it for 3 years in your daily lives, when you go to the store, or buy a used car, try to buy a home, order parts for your widget company etc…So in summary, prices are here to stay and we need more homes to be built, likely catalyzed by proper incentives / less onerous regulation.

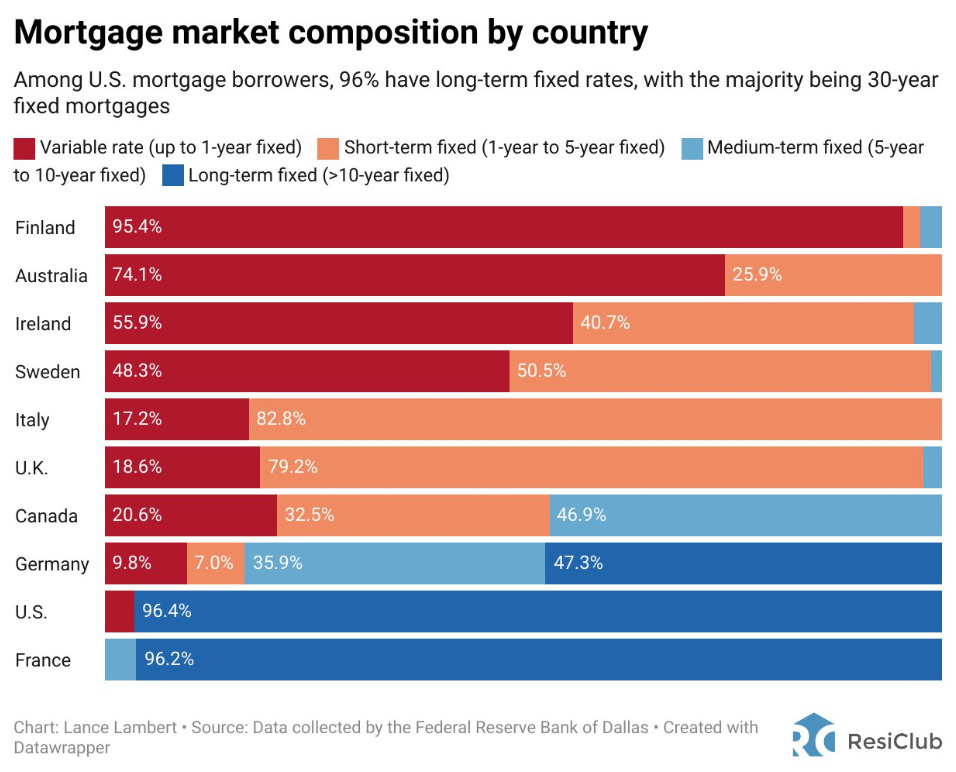

Well all that Sucks, What’s the Positive?It should be said, we are extremely fortunate here in the US. We have this thing called the 30-yr fixed mortgage, primarily because of the structure of the mortgage market with government backed mortgage securities. And since the qualified mortgage law in 2010, these loans have remained solid, and thus, so has the mortgage securities market. I don’t say this often, but good job U.S. Congress / government! (Better late than never, full disclosure I was working in Congress at this time).

So, unlike the 2008 Great Financial Crisis, today we don’t have high homeowner distress, which result in distressed sales and home price cliff dives. This dearth of distress is another reason today’s home prices will remain elevated to stable, despite higher mortgage rates. What could pierce the housing market armor? Unemployment spiking up, it’s the great equalizer. This is why the dreaded recession is often talked about, it usually portends high unemployment, which is an economic killer.

If you were in most of the other highly developed countries in the world, you would likely have a variable mortgage rate that would suddenly change on you when interest rates change, the Mr. Hyde of mortgages. “In the UK ‘more than a million households will see a significant jump in monthly payments’ this year as ‘the next batch of UK homeowners to have their mortgages repriced are preparing to make personal sacrifices”(Bloomberg). Imagine your mortgage going from $1500 to $3000? Just look at the % of mortgages in other countries that have variable rates:

God Bless America.

In Case you Missed it: The President’s New Housing Proposals are ProblematicSince it was a big f*$%ing deal headline, I’m re-linking my analysis of the President’s housing proposals he unveiled last week during the State of the Union. Worth a read for all you prospective homeowners/investors.

Bottom Line

There is always reason to be positive!

The Skeptics Take: America is Amazing. Some countries may have faster growth in good times, but über-crash in bad times. Long-term fixed debt calms the short term market volatility. So while things may seem difficult right now, remember the US is doing absolutely fantastic compared to everyone else. Hell, ~99% of mortgages in United Kingdom, Finland, Australia, Ireland, and Canada are short term, variable debt. Verrückt! Times may seem tough right now. Everything costs more than just 1, 2, 3 years ago. And not just a little, a lot! But unemployment is at record lows, literally the lowest ever. And despite high inflation and the necessary reaction of high rates (even though it was the government that caused the inflation in the first place) the economy is humming, stock market up, home prices for homeowners have contributed immensely to their net worth, technology is doing amazing things and providing ample opportunity for those born into less fortunate situations to escape and succeed.

Life is good. And as my dad used to say, “this too shall pass.”

In other words, Stay Skeptical but positive y’all. There is always opportunity.

Most Interesting Tweet(s) of the WeekKids these days! Looks like a helicopter parent situation. Pull up those bootstraps little birdie.

That’s it for this week. If you are interested in digging deeper into any of these ideas or just want to talk real estate investing - which I always love doing - don’t hesitate to reach out. You can email me direct, I try to answer all the emails I get personally. [email protected]

Again, stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Post: The President’s New Housing Proposals are .... Problematic

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

@Carlos Ptriawan you got it my friend! We need something to help supply, ironic that these proposals will make the problem they are trying to fix worse. Thanks for the comment.

Quote from @Carlos Ptriawan:

i agree it's problematic, they want people to sell their home LOL but if folks are selling then they have to buy again with higher interest rate, i meant, it's not a smart decision.

they could just offer 35 year mortgage rate or gov. buydown rate for the first 2 years that would help little.

Post: The President’s New Housing Proposals are .... Problematic

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Thanks Jonathan! Yes for my fund that I GP and for my personal investments we are leaning in to this soft-er market for buyers and pickup up great deals. Just the MLS has been great actually. Mostly small multifamily, which do well here in Nashville.

How about y'all?

Appreciate the read!