All Forum Posts by: Andreas Mueller

Andreas Mueller has started 66 posts and replied 242 times.

Post: How Investors Build Wealth in Real Estate

Post: How Investors Build Wealth in Real Estate

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

Thanks Joel!

Post: How Investors Build Wealth in Real Estate

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

Thanks Chris!

Post: Why Should the Fed Cut Rates at All?

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

Welcome to my weekly skeptical investor forum, right here on BP! A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - Project Update: North Nashville Duplex

- - Why Should the Fed Cut Rates at All?

- - The Setup for Spring Season

- - My Skeptical Take

The Weekly 3: News, Data and Education to Keep You Informed

- - Warnings flashing of ‘froth’ in crypto and stocks as S&P 500 valuation surpasses 2000 levels ().

- - China is issuing record debt to stave off recession, while the US bull market continues (Wallerstein).

- - Texas vs California Home Construction. It’s not even close (FT).

-----------------------------

Today’s Interest Rate: 6.93%

(👆.21, from this time last week, 30-yr mortgage) -----------------------------Today we’re talking: housing market, interest rates, and a quick update on my latest rehab and rent project. The setup for a bullish Spring real estate season is palpable.

Let’s get into it.

Project Update: North Nashville Duplex

Construction has begun on a cozy duplex I picked up in North Nashville a couple months ago, a lovely little transitioning neighborhood just an 8-min Uber to downtown (yes “cozy” is real estate parlance for small, but it will be cozy!). You can see the development in the area is in full swing. The gray home to the left is on the market for $550k, to put things in perspective (it’s a 4 bed / 3 bath, 2000 sq/ft, with modest finishes).

North Nashville

North Nashville

This place was a little bit of a disaster zone, which is why I love it 🤠. A kitchen fire in the back unit got a little out of control and burned up to the roof. The previous owner started to repair it.

Looks a little rough, but we’ll get her all fixed up.

Exterior work just got going. Paint, trim, full perimeter fencing, 2 gates and landscaping are starting. There will also be a new front deck (and back deck eventually), and a small covered porch with a hipped roof.

In that burnt-out back unit, we have started the transformation! I designed a little U-shaped kitchen to fit right in the space. To maximize the sq/ft (and save cashola) and give it a more spacey feel, I’m doing open shelving instead of upper cabinets and the countertops will extend all the way to the near wall, fully covering the front load washer and dryer units, which also have their home in the kitchen. But when we are done it’s going to look sleek and intentional.

Painting has started on the interior (Benjamin Moore - Smoke Embers in case you were curious), as has flooring and lighting. The lighting is a little dark in the picture but this will be a lovely/bright kitchen and living room for our next resident.

The home is a duplex with 2 bed / 1 bath, on each side.

That light is going to go, don’t worry :)

That light is going to go, don’t worry :)

The scope of work is pretty much everything: kitchens, bathrooms, flooring, gutters, deck, fencing etc…, except for most of the windows and walls/drywall, which I was able to save (except for the front unit, which had some rough popcorn ceiling).

The kitchen should look something like this render:

There wasn’t room for a dishwasher and what I felt was enough cabinet space so I’m going without for the first time in one of these smaller units. How do you feel about that? Heck, I hand wash my dishes mostly at home anyway.

I am targeting a February move-in. Rents should be a modest $1500 per side, depending on the time of year I’m able to get it on market. Spring is best obviously so we may be a little early, but that’s ok.

Any burning thoughts? Let me know in the comments!

Ok, that was fun. Now let’s get to the market update.

Market Update

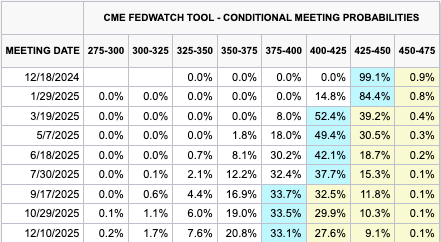

For the second time in as many months, the Federal Reserve is on deck this Wednesday with a decision on whether to cut the Federal Funds Rate.

Over the last few weeks, Fed board members have been signaling that a cut is in the making. That would mark the third rate cut in a row, a full percentage point lower since they started cutting in September.

I have to admit, my prediction a month ago of a more restrictive Fed was wrong. I said they would pause and they went full steam ahead, albeit with a small .25% cut. I was early, but I do now think they will pause cuts starting with their next meeting on January 29th (just 9 days after the inauguration).

Folks in the press are already calling this month’s rate cut a “hawkish cut,” meaning that Fed Chair Jerome Powell will take time in his press conference tomorrow to downplay the speed at which the Fed will cut rates in 2025. The Bond market agrees with that assessment and is dubious there will be more than 2 total cuts in 2025.

Why Cut at All?

Some are saying, why is the Fed cutting at all? (myself included).

The stock market, gold, Bitcoin, and most real estate are all at all-time highs.

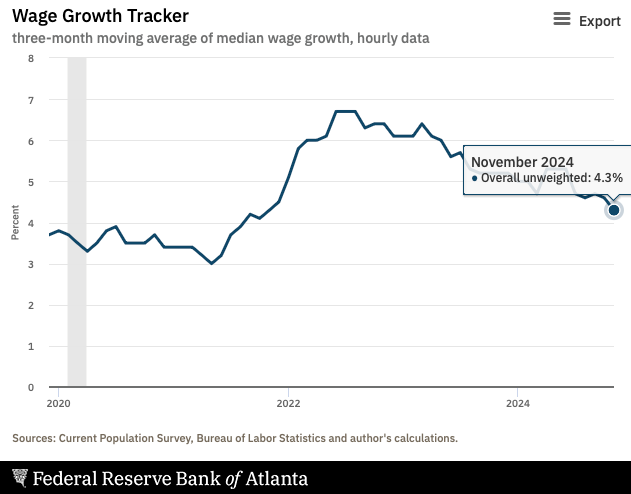

The economy is rocking, we have full employment (~4% unemployment) and wage growth is still at 4%.

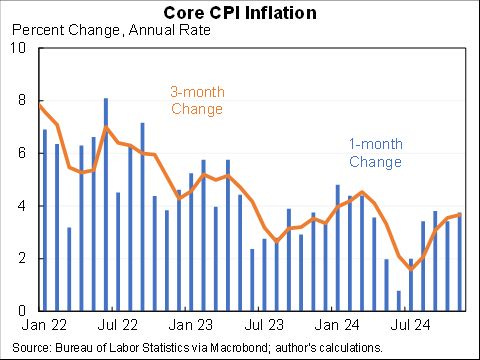

Case in point: Inflation is still sticky, like my sourdough bread leaven.

Core CPI levels came in this week a touch higher than expected: 1 month: 3.8%, 3 months: 3.7%, 6 months: 2.9%, and 12 months: 3.3%. The trend is down, but hovering just south of 4%.

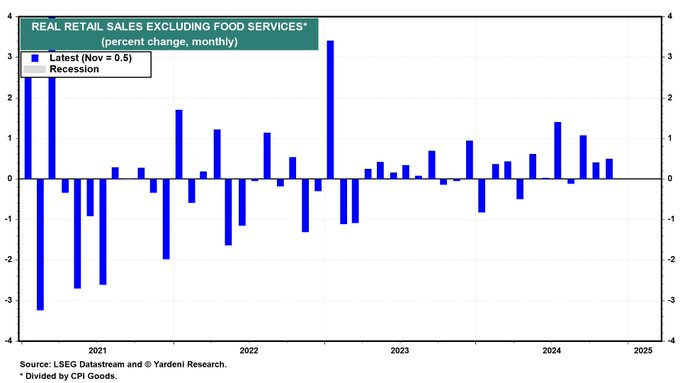

And the consumer is spending this holiday season. Retail sales so far are +.7% MoM and +3.8% YoY.

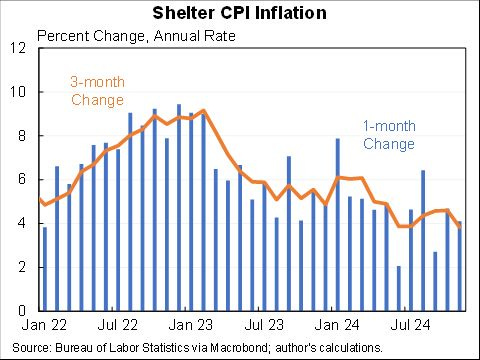

Some good disinflationary news: shelter growth is on the way down, which we do need frankly, and I say this as a landlord. Rents can’t realistically continue to appreciate at the rate they were if we are to maintain a healthy housing sector. Progress has been made since the 2022/23 highs but need to further come in. Shelter growth is still higher than overall inflation, at 4%.

So maybe, the Fed has interest rates around where they should be in the cycle?

One example of the hot U.S. economy: wages. Wage growth is still running at over 4%, above core inflation.

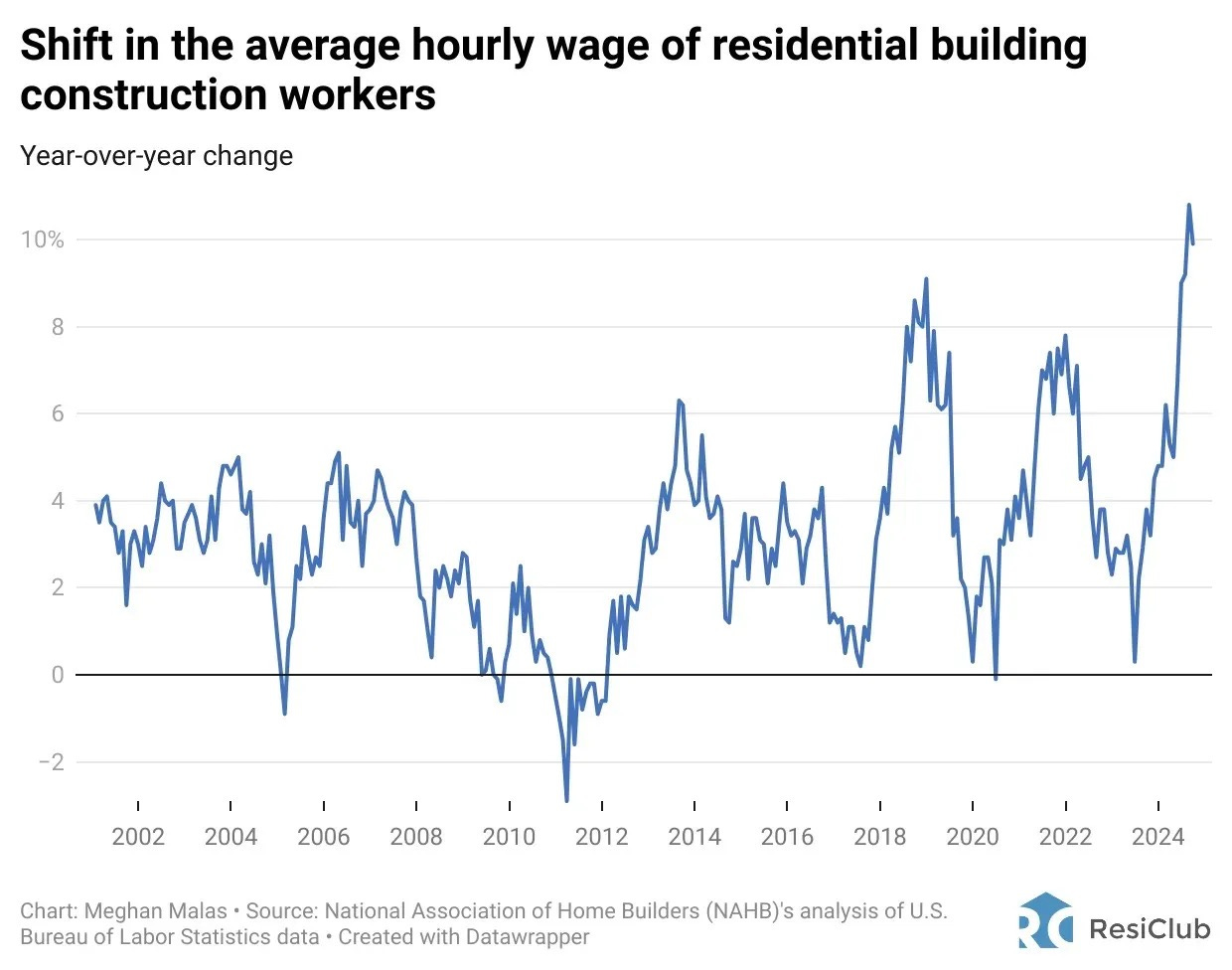

This permeates to all workers, including the construction trades, and thus, to the price/cost of homes. In fact, construction wages have far outperformed average wage growth in the last 2 years.

According to the National Association of Home Builders (NAHB), average hourly wages for residential construction workers rose 10.8% between August 2023 and August 2024, the largest YoY jump since the BLS started tracking the data.

This is no surprise. I’m seeing double this frankly in most trades.

Could wages be making a top?

Normally I would say absolutely, looking at the above chart. But the NAHB also reiterated evidence of an ongoing labor shortage, saying, “The ongoing skilled labor shortage in the construction labor market and lingering inflation impacts account for the recent acceleration in wage growth.”

For now, the hot market is still rolling. I personally know several blue-collar millionaires from HVAC techs to plumbers. If you sweat for a living, there is good money to be made.

My Skeptical Take:

I’ll do a 2025 prediction post in the coming weeks, but for now, I’ll just say that all signs are pointing in the ☝️ direction.

I’m bullish going into 2025.

But my skeptical spider senses are starting to flash.

In the next 100 days, I do think we take a little breather, or as the finance folks like to say, a correction. We have been on such a tear, that it is appropriate that we see a bit of a pullback, likely starting with the the stock market and filtering down into the real estate market. Folks feel less rich and pull back when stocks and their 401k’s are flashing a bit of red. For investors, this makes this winter a great time to acquire your next deal.

To be clear, any correction, in my opinion, will not be related to an economic slowdown, but rather the opposite. Because there have been such significant gains in the markets this year (unless you are a bond investor😬) fund/asset managers and stock traders will likely do some portfolio rebalancing in January, selling winners, and locking in tremendous 2024 gains. I bet they wait until January or February so they don’t have to pay the tax on those gains for another year (which is why we may be seeing less selling this month than in a normal cycle).

Counterpoint: On the other hand there is jubilation in the streets.

Well, street.

Wall Street, that is.

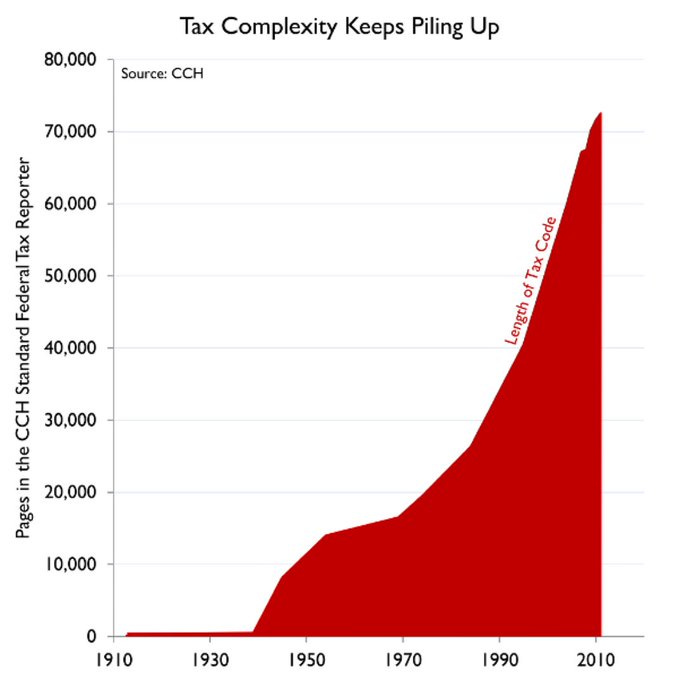

The fervor in the air is palpable. Business leaders can’t stop talking about this “pro-business administration” that is coming on January 20th. They see a renewal of the current business tax rates, regulation and permitting rules getting slashed, tax code being simplified, and federal deficits on a one-way ticket down the elevator (which are a longterm drag on economic productivity).

Just look at the growth in tax code complexity over the last 20 years. Holy hell.

This is totally regressive. For me, this is just a few extra bucks I have to pay to the CPA industrial complex. But if you can’t afford that you don’t get to take advantage of the tax code complexity.

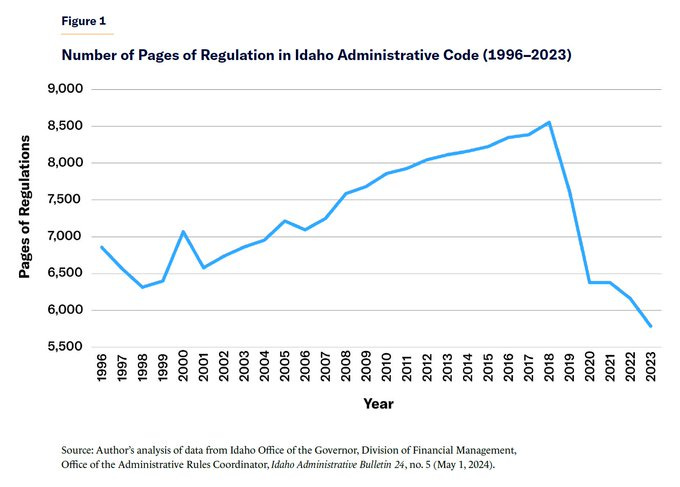

And for all the naysayers (myself sometimes included!) who say deregulation is possible.

Idaho says, “hold my beer.”

You go Idaho!

All this is to say, the US may have a very auspicious directive in the making.

Thoughts on two perceived tale risks: deportations and tariffs.

A quick non-political note on two topics I can’t seem to avoid: mass-deportation and tariffs.

I am not concerned about the saber-rattling from the TV talking heads about “mass deportation” and “tariffs.” I view these as fear-mongering, and it makes me bristle. Looking into my crystal ball - which I still keep in my closet from my previous life on Capitol Hill - neither of these risks have a realistic path to a meaningful economic effect. To be sure, both deportations and tariffs will likely be carried out, but they will most likely be minute in scale vs US GDP. These are political wins the administration wants from promises made on the campaign trail.

So beware of these (and other forthcoming) dog whistles, they will lead you astray, fighting imaginary ghosts.

But I digress…

I am feeling hopeful that government can get its butt in gear and make meaningful change, both in size and complexity, with help from both sides of the aisle. This doesn’t need to be all at once, and can be done one bite at a time. I bet we see a steady stream of government efficiency statements, cuts, proposals, updates etc… sprinkled out into the media every few weeks all next year. This will be bullish for markets.

As then Senator Everett Dirksen is quoted as saying:

“A billion here, a billion there, pretty soon, you're talking real money.”

-Everett Dirksen

For us real estate investors, I think the setup for the Spring will be there. Aptly-timed when another rate cut likely in the offing.

“But, what if inflation does rear its ugly head Andreas…?”

Good for real estate owners. Property values up.

“Ok, well, what if these economic signals are not a sign of a normalizing economy, but of one that may be approaching recession….?”

Good for real estate seekers. Interest rates will plummet and you can refinance that property, lock in 30 years of low interest rates, pull out equity, and buy another! (aka the BRRR method).

But, if you stay on the sidelines, acting fearful and not greedy, you will reap the benefits of neither.

Again I do think we see an early pullback in 2025, in the first 100 days.

But long term, I can’t hope to be a little giddy, always with a skeptical eye toward the horizon, of course.

Be cautious out there. Always protect your downside.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Andreas Mueller

Post: How Investors Build Wealth in Real Estate

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

Thanks for the up votes all!

Post: How Investors Build Wealth in Real Estate

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

To provide for our future and our families, we invest.

Investing is different than other moneymaking activities. It means each dollar we’ve allocated is working overtime on our behalf, not just sitting idle in an account as inflation saps it of its power. Investing means our dollars are like little worker bees, earning us $ when we’re at work, at the park, with our kids, on vacation and yes, even while we’re asleep.

This could mean buying stocks, bonds, real estate, contributing to one’s 401k, hiring a financial advisor (I hope not), fine art, crypto, collectables, classic cars, or investing in someone else’s fund, to name most.

I chose real estate (w/ some stocks and crypto too).

It’s used by the wealthy, the middle class, the young, the old and yes even the broke (I was both the latter, and I’ll tell you how).

It pays robust, consistent returns, but it’s more involved and time consuming than just clicking a buy button.

Real estate investors get paid for doing the work.

Real estate is a familiar to us but we may not know exactly how to do it. Roughly 65% of Americans own a home, while 60% own stocks. Heck, we’ve all likely had a nosey landlord at some point in our life. But owning a home where you live is not an investment. It’s not an asset; it’s a liability. You have to rent the property to others (aka put it into service) to reap the many gains of investing. And only 6.7% of Americans own rental property, according to IRS fillings. Moreover, while we’re on the topic, most all rental properties are owned by individuals or mom-and-pop businesses, not Wall Street. They own less than 3%. In this vein, real estate investors are really small business owners.

This is the Way These are the 5 Ways:

How Investors Make Money in Real Estate

Real estate pundits and online gurus often overly focus on one aspect of this business: cash flow. That’s a very limited view, and frankly, leaves out the juicy parts. After all, a roasted bird is so much more than just the white meat.

In fact, there are 5 primary ways investors make money in real estate. Cash flow is just one of them, and it begins as one of the smallest (keep reading).

To be clear, cash flow is important (or rather it becomes important), but it is not everything. Not even close. We don’t get into real estate for a dividend check. Returns from real estate are much more lucrative than that.

Hopefully, this article will reframe your perspective on wealth and why many investors choose to allocate a large portion of their wealth-building operation to real estate.

Let’s get into it.

(* Quick disclaimer, for the purposes of this article, this writer is referring to residential real estate: 1-4 unit residences. The scale / analysis does change for commercial real estate because of vastly different financing arrangements, and buyer/seller marketplace expectations etc... So we’ll save that for another day).

#1 - Natural Appreciation“Buy low sell high,” I’m sure most of you have heard the well-known adage. We invest in something we are confident will be more valuable in the future.

That’s appreciation in a nutshell.

The savvy investor must hone their senses and utilize the data to take advantage of an asset’s natural value/price appreciation. Natural means you don’t directly control it, but you can guide it. For instance, I am currently concentrating my investments in Nashville, TN. A city I have witnessed growing its population, # of businesses and GDP faster than the national average, while also maintaining a low unemployment rate and robust job creation. Further, within this city, I have learned the desirable areas to live, researched future developments, paid attention to criminal activity and researched the % historic change in property valuations. I have polled the barista, waiter and entrepreneur. I understand now where the path of growth is for the city and where real estate is likely to appreciate more than others.

The path of growth guides property appreciation.

This is how I prime my investment for success. It’s not a blind bet; but, it’s also not guaranteed. That is why investors get paid. We have to take risk, calculated risk, but risk nonetheless. The difference is, investors act when the odds are in their favor and if so, statistically over time, they will be successful.

As the late great Charlie Munger put it:

“The wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds. And the rest of the time, they don’t. It’s just that simple.”

— Charlie Munger

Remember, life isn’t baseball. You don’t have to swing. Munger’s business partner, this guy named Warren Buffett, is fond of saying:

“The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, ‘Swing, you bum!,’ ignore them.”

— Warren Buffett

The dichotomy illustrated above is that both patience and initiative are equally important qualities in the character of any successful investor.

Take heed.

To be clear, we don’t bet on appreciation per-say. Investors don’t gamble. We make decisions that will give us a high likelihood for success and take action. In a way, investors get paid for their shrewd judgement.

Real estate, like any investment, can decline in value. Munger emphasizes that if you can't tolerate a potential drop in your investment value, you're “likely to only achieve mediocre returns,” as great investments can experience significant short-term price fluctuations. Investors have to be able to stomach volatility. In fact, you should probably assume it will happen. Fortunately, real estate is known for being extremely consistent and declines in value are rare and short-lived. If an investor reacted to every little bump they would miss out on the tremendous long-term returns. Prices are like the weather (not the climate), they fluctuate.

Case-Shiller National Home Price Index, Historical

Case-Shiller National Home Price Index, Historical

And remember the above index is the average natural appreciation for the US. We endeavor to do better by picking a growth market/city, micro-targeting within that city and making sure we are in the path of growth.

Appreciation is how the majority of wealth/value is built in a real estate investment.

Not cash flow.

Remember this when calculating the total return on investment (ROI) in real estate.

The Leverage Effect

Real estate is often purchased with a loan to cover the majority of the asset’s cost. For example, the typical investor loan requires a down payment of 25% of the total property cost. This is called leverage. And in this case, the leverage is 4 to 1.

Using leverage enables you to drastically improve your ROI. Let's say you purchase a property for $500,000 and it appreciates to $700,000, the investment has made a 40% return.

Not bad.

But you used leverage in the form of a loan from a bank, not all cash. Since you put down just 25% of $500,000 - or $125,000 - and the property appreciated $200,000 - you made 62.5% on the dollars you invested.

Even better.

Real estate in the US is often purchased with leverage for this reason, and also because it’s one of the easiest assets to get a loan for (because of government incentives / regulation, which I won’t get into here). The lending terms and interest rates for leverage in US real estate are extraordinary. Real estate often has the lowest relative interest rate when compared to most other types of consumer-facing loans.

We often take this for granted as Americans. In fact, the 30-year mortgage with a fixed interest rate is a distinctly American benefit. Most other countries do not have this. Not Canada, not he UK, not Japan…

Take advantage.

#2 - Principle Paydown (aka Cash Later)Another facet of using leverage, in addition to multiplying your investment’s return, is that you have to pay the mortgage back.

Crap!

But wait, this is actually a feature, not a flaw. Because it’s not the investor who is paying the mortgage, the debt is paid with the revenue the asset generates, in this case, the gross rents collected. Remember, a loan is broken into two parts: interest and principal, or the balance of the amount borrowed. Thus, every time the monthly mortgage is paid, the balance of the amount owed on that loan ticks down, and the equity value the investor owns ticks up (equity = assets - liabilities). And after 30-years (or whatever the term is on your loan) the balance is zero and the investor owns the entire asset outright.

Yay!

I think of principal paydown much as I do cash flow. But instead of that income being deposited into my checking account for immediate use, it is deposited in my property’s account for later use (or that I can borrow on now, more on that later).

Aka cash later. And it gets better.

At the start, the fraction of the mortgage that is principal is quite small. Typically just 1% annualized. The majority of the monthly payment goes towards the interest of the loan. So you aren’t putting much of a dent in the balance of the loan each month. But, in years 3, 5, 10… a larger, and larger, and larger portion goes towards paying down the principal and paying into your equity, particularly because of the way a loan is amortized, aka the process of writing down the value of a loan. This 1% quickly becomes 3%, then 5%, then 15%…

Cash later is very underrated in calculating real estate investment returns.

#3 - Forced AppreciationSimilar to natural appreciation, forced appreciation is increasing the value of an asset, but you control and can closely estimate it. We force appreciation when we add value to a property. In residential real estate, this is typically done via a renovation. But we can also improve the value of a property by fixing broken processes, removing bad management, working with the city to improve neighborhood blight, convincing a neighbor to stop parking their cars on the front lawn and clean up trash (yes, I’ve done this and wow what a difference in my property value :) etc…

Let’s focus on renovations, since it’s easiest to control and calculate. As a rule, I want a minimum 50% return on my construction dollar when I’m renovating a property. That means, if I spend $100,000 on renovations, I want the property to be worth at least $150,000 more afterward, if I were to put it on the market or want to refinance it. This means, typically, the larger the renovation the better, as long as I’m spending money judiciously. No gold bathtubs, we aren’t renovating the Taj Mahal. Deciding on a scope of work and what to spend money on is a skill that investors must hone.

Fortunately, we can calculate with high accuracy what our returns will be on a particular renovation. To do this we need to:

- Get quotes from contractors, and pick one;

- Add that cost to the price we paid for the property;

- Determine what price similarly renovated properties have recently sold for (we call this the ARV or after repair value). You can use Zillow to estimate this, or ask your real estate broker, which I recommend, as they likely have access to more data than you;

- Subtract the price of the home and renovation cost from the ARV to get our forced appreciation equity return. Voila!

For example: let's say we buy a home for $500,000 and put $100,000 into it. Based on the median ARV for sold comparable properties, we estimate it to be worth $675,000. Our total forced appreciation is $175,000, including $75,000 in equity returns. In other words, spending $100,000 to improve our asset made us $75,000 in equity or a 57.14% return on our construction dollars.

Nice.

You should also calculate this as a total leveraged return for the whole asset, like we did above, since we likely got a loan to purchase the property (and may have done so for the construction too, but i’ll assume not here). In this case, if we put 25% down ($125k) and paid for the renovation in cash ($100k) and the renovation returned $175k in forced appreciation, including a $75k equity return, this renovation brought us a 33% total return ($75k/$225k)!

I don't know where else you can confidently get a 50% value add return or a 33% total return. And the ROI is even better if you get the property for a great price, ie below market value, below comparable sales (aka comps). In our brokerage, we don't let our clients pay retail; I always aim to get them a property below the comps.

This is why a simple DIY / fixer-upper is so attractive to new investors. You can really hit the ground running and pay less for that renovation by doing some yourself. And when you start adding bedrooms, bathrooms, or overall square footage you should see even higher returns. Savvy investors look for properties where they can add value like this. The key is to look for properties with less than the ideal number of amenities (ie bathrooms etc…), and then add what they are lacking to create the most value.

#4 - Tax DepreciationYes, your property is appreciating, in value, but it is also slowly deteriorating, literally, which means you have to spend money to repair and maintain it. The government recognizes this, and much like equipment or durable goods a business owns, you can depreciate the value of the asset, thereby deducting a percentage of the property’s total cost from your taxes. For residential real estate, the IRS allows rental property investors to deduct 3.636% of the value of the structure of a property each year over 27.5 years. For example, if the value of my real estate is $500,000 and the land is assessed by the tax man at $100,000, the value of the structure is $400,000. Thus, you can deduct $400,000 * .03636 = $14,544.00 off my taxes every year. In practice, depreciation is used by the savvy investor to shield much of the cash flow earned from taxation. You can also accelerate this depreciation, but I’m not getting into that here. (* Required legal disclaimer: I’m not a CPA and this is not financial advice).

Your Primary Residence is Not an Asset, It’s a LiabilityThis is as good place as any to make this point. You can cannot depreciate a home you are living in (yes there are some nuanced exceptions but I’m not getting into that here). This is one of the fundamental reasons why owning your primary residence should not be considered an asset or investment, even if you happen to make a net profit selling it in the future.

Think of it this way: if you took that same money and bought a rental property instead, which you could depreciate, add value and raise rents on over time, while at the same renting your primary residence, you would make a significantly higher return, and have cash flow you could reinvest.

There is an old adage, “[rent where you live, rent-out what you own].”

Don’t get me wrong, it is amazing to own your own home. I do. But that is an emotional decision, not a financial one. I like owning my own home. I don’t want a landlord telling me what I can and cannot do (one reason I stay away from condos and HOAs too). I have a dog. I may get a few chickens. I have a garden. I park my car in any spot I want to. Tomorrow, I’ve actually got a pretty nice little Saturday planned, we’re going to go to Home Depot, buy some wallpaper, maybe get some flooring, stuff like that. Maybe Bed Bath and Beyond, I don’t know… I don’t know if we’ll have enough time!! (bonus points for getting that reference :).

So what have we learned?

Is owning where I live maximizing my returns?

No.

I would make more money if I moved out, rented-out my home and rented my primary residence. And even more money if I moved out my cars from the garage, finished the basement and added two more bedrooms, maybe a bathroom.

Now that’s adding value. :)

#5 - Cash Flow (aka Cash Now)Lastly, we have cash flow, or Net Operating Income (NOI). This is how much cash is available each month after taking the difference between all money coming in and going out, including loan payments, maintenance, taxes, insurance, management fees, repairs, other expenses etc… (ok, technically NOI is not the exact same as cash flow, and is actually a more accurate definition as cash flow is actually a more broad calculation in business. But, in residential real estate parlance they are often used interchangeably, so I won’t go into the difference here. Just know there are technical differences).

Put simply, how much cash is in your property’s checking account each month after you pay for expenses? If you have more money in the account, congrats! You are in the black, as they say. You are cash flow positive.

Now, you don’t have to be cash flow positive to invest in real estate and make serious money, but it sure does help. I’ve had a few places where, in the beginning (first 2 years) I was not in the black. They “lost” money each month. But the areas were so hot, the properties appreciated 22%, or several hundred thousand dollars, which is why I bought them. It would literally take me decades to make a fraction of that return in cash flow. And, since I own a portfolio of properties, I could use the negative cash flow to offset cash flow gains from other properties I own, lowering my taxes.

Cash flow is key, I don’t recommend negatively cash flowing unless you deeply understand the risk. Cash flow de-risks your leveraged investments so you don’t get into trouble, can’t pay the mortgage and the bank forecloses on your home.

That would be no bueno.

Cash Flow EvolvesAs you can tell, I am intentionally downplaying the importance of cash flow, at least in the beginning. Cash flow is like a house plant. It starts out small. You have to nurture it. But over time, it grows. You raise rents. Yet, your long-term debt stays fixed (thank you America). Yes, property taxes and insurance (especially in some parts of the country, watch out) will tick up, but rent increases should cover those costs.

Do you buy real estate with the intention of holding a property for only 1 year?

No. We are investors.

That’s not why we do this (unless you are flipping, which is not investing, thats a separate business / job and is taxed at a much higher rate to boot).

So as it grows, cash flow becomes much more important later. In fact, I would argue… it evolves.

Cash flow grows slowly over time until BAM!…something very powerful happens…The mortgage just…disappears.

It’s been 30 years, you now own the property free and clear. But….how many properties do you own now? If you have been slowly, conservatively acquiring and renting out properties you may own 5, 10, 30+ properties? Without any fancy tricks or schemes.

Now you have some serious cash flow. And each year another loan vanishes.

At this age in your life, cash flow is important. Cash flow is how you retire. Social Security is not reliable, and was not purpose build for retirement. Don’t rely on it.

But it does take time. Real estate is not a get rich quick scheme. Anyone who says otherwise is lying. Don’t listen to the gurus. Investments grow slowly and compound over time. And don’t forget our old friend depreciation. Again, we only pay taxes on our cash flow after we account for that depreciation / tax deduction (3.636% / yr). The result? Investors pay very little taxes on the cash flow income. Especially in the beginning.

So I recommend not chasing cash flow early. Allow it to grow and evolve into a big green monster. Of course, if you find a great deal that can net you higher returns early, by all means jump on it. But chasing cash flow as priority #1 will likely suck you into either one of two things: high risk D-class neighborhoods and underperforming markets that will under-appreciate. That’s how folks achieve mediocre results, or worse, lose their shirt.

In investing, Rule #1 is never lose money. Rule #2? See Rule #1.

Protecting your downside is more important than maximizing your upside.

Cash Flow Buys You More Real EstateAs your cash flow grows, you can use it to buy more real estate. As your rents tick up, you can choose to refinance: replace the mortgage with a larger one it can now support, and pull equity out of the property in the form of cash. The best part, the cash you pull out is debt, not profits, so you pay no taxes on it. Zero. You can then use those funds to purchase more real estate. I have properties I have owned for a long time in great areas that I have refinanced multiple times. Real estate mogul Barbara Corcoran has spoken about this same tactic. She has one property she has refinanced 9 times over the decades.

What did she do with that tax-free cash?…

“[I prefer to refinance and pull money out]. I’m talking about a lot of money back out. I’m not saying I had a mortgage of $200,000, I put 250 on it. I would wait five years. For the $200,000 I would then put an $850,000 mortgage on put in my pocket. Listen, refinancing is the way you really get rich in holding real estate that’s what I never like to sell. It’s just a bank that’s going to keep on giving. That’s how I look, I feel like I’m in the banking business, but I have real estate to back it up.”

— Barbara Corcoran

Growth Markets > Cash Flow MarketsThe above is why savvy investors seek growth markets. The ability to add value, grow rents, and refinance an appreciating property. This is also called the BRRRR method, as coined by David Greene.

So, when I’m looking to invest I want an area where assets supply is low/constricted and/or demand is strong/growing, population is increasing, unemployment is low, job openings are attracting new workers, wages are growing, and the property is in the path of growth.

My Skeptical Take:

Real estate allows an investor to buy and control a large asset, while only paying for a small percentage of its cost. The asset pays for itself, the investor makes an ever-growing income each month, the asset’s value can be forcibly appreciated, they build immense wealth and pay little in tax.

Remind me why only 6.7% of the population does this?

Well, three is one catch, conventionally (no pun intended) you need money to buy real estate. Saving 25% for a down payment + closing costs is nothing to scoff at. And yes hold your responses, there are creating financing strategies to buying real estate such as owner financing, subject-to, raising capital, partnerships, syndications etc…but I’m not going to get into those here. I’m talking classic, tried-and-true - and yes potentially more conservative - real estate investing. To grow immense wealth it doesn’t need to be complicated or risky. You just need to Work, Save, Invest, Repeat…WSIR! (Not a cool acronym I'm afraid, let me workshop it)

To succeed you have to be, as Theodore Roosevelt put it, “In the Arena.”

We all want to grow our wealth for our us and families. The only question is, what are you going to do about it?

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Andreas Mueller

Post: Investor starting BP journey

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

Welcome to TN, the water is warm.

Highly recommend Nashville. Fun fact, we have the lowest unemployment rate in ant top 25 major city.

Post: 2025 Predictions & Thoughts For The Nashville Market

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

It's Morning in Nashville, what a great time to witness this city growing up. At only -700k population, it has the lowest unemployment of any top 25 city, and those folks need homes. We just pass a transit referendum too, which will finally allow matching money to flow to the city for the first time.

Zero tax state, no insurance or property tax issues like FL and TX.

Couldn't agree more Luka and Tyler.

Plus: TN is top 3 in net inflows too. COVID was not a fad, folks keep moving here.

And here is the latest BLS report.

On the election: Trump in the WH wont make a difference. I see no causation. Im hopeful we can get some housing supply policies, everything on the campaign trail was net boosting housing demand, which we have enough of.

Post: Top 5 Locations in Nashville to Flip

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

My 2 centss:

Antioch is have some crime issues, I'd stay away till it gets better. It may be too early, which is the same as being wrong. Several clients had shooting issues lately. Im out.

LOVE Madison though, great call Luka.

Post: Land Deals For Builders

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

We have several land deals in Nashville. Contact me for more info.

Post: Is the Fed Done Cutting For 2024?

- Real Estate Agent

- Nashville, TN

- Posts 305

- Votes 155

Quote from @Andrew Syrios:

I think the economy is going to soften and there will be a lot of pressure on the Fed to lower rates, which I think they'll do. Long term with baby boomers retiring (and passing away) I think we'll see rates go up, but I think they'll probably dip down a bit more in 2025.

Hopefully, they dont tick up too much, for all us investors' sake.

Much appreciate you engaging in the comments!