Updated over 2 years ago on .

- Real Estate Agent

- Nashville, TN

- 178

- Votes |

- 353

- Posts

Will massive apartment unit growth affect single family home rentals?

Welcome BP compatriots! Another installment of my weekly brief, hopefully insightful, dive into real estate and financial markets, for all the kick *** dudes and dudettes out there.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Interest Rates: What to Expect?

- - Housing Prices and Supply: Effects from Massive Apartment Unit Growth

- - Tangent Alert! Cancer Rates are up since 1980 at an alarming rate. The cause? Likely the food companies adding sugar / crap to food.

- - The Bottom Line - My Take on Markets

- - Government Releases Experimental “New Tenant Rent Index:” A new measure of rental rates; shows rents are down the last few months. (BLS)

- - 25% chance of Recession in 2024. But economy will likely outperform estimates. (Moody’s)

- - Foreclosures and Bankruptcies Remain Low: Be wary of numbers like 700% increase, that’s because they were paused during COVID. (Housing Wire)

Today’s Interest Rate: 6.77%

(👇 .03% from this time last week, 30-yr mortgage) Interest Rate: CPI, Mortgage Spreads…What to Expect?Inflation numbers released last week by the Bureau of Labor Statistics showed that U.S. (CPI) inflation rose 0.3% in December, after rising .1% in November, a touch stronger than consensus analysts’ expectations. Of note, shelter continued to rise in December, contributing over half of the monthly increase (up .5%, and up 6.2% YoY). In aggregate, this puts 2023 inflation at 3.4%. We are staedily coming down, but, IMO, still too high. Adding to this, retail and food service sales released today were up $709.9 billion, up 0.6% MoM in December and 5.6% YoY. Why do inflation and retail sales matter? The Federal Reserve likely needs to see lower inflation to start cutting interest rates in March. Retail sales are an indicator of consumer strength.

IMO: Stronger than preferred inflation data and a robust labor market (unemplyment remaining low / strong consumer) = Fed does not cut rates in March. The Feds rate cutting committee, the FOMC, will remain data dependent, track leading indicators, and will err on the side of being late to cut, rather than early. Nobody can time the market, but my inclination is for a first rate cut to occur in June, 3 in total this year, at 25 BPS each (.25% x 3 = .75% in 2024). This belief is not religion. My opinions are strong, yet moderately held. Make sure to tune in to A Skeptical Dude each week to keep up to date on the market’s latest and get my analysis. You can follow here or here.

For it’s part, the bond market is still pricing in a 97.4% chance of a rate cut in March - and a mind-bogglingly high 6-8 rate cuts in 2024 (though down from 6-9 a month ago). Every meeting a rate cut, on average and at over 50% chance. What do bond traders know that the Fed doesn’t? Well they just started using computers so… that’s probably pretty neat for them.

What do the Experts / Analysts / Financial Institutions Think?- - Goldman Sachs: “We continue to expect the first rate cut in March, and 5 cuts total in 2024”

- - JP Morgan : Cuts to start “Middle of the year” and then “grinding lower”

in 2024. - - Mark Zandi: 4 rate cuts in 2024. (ResiClub)

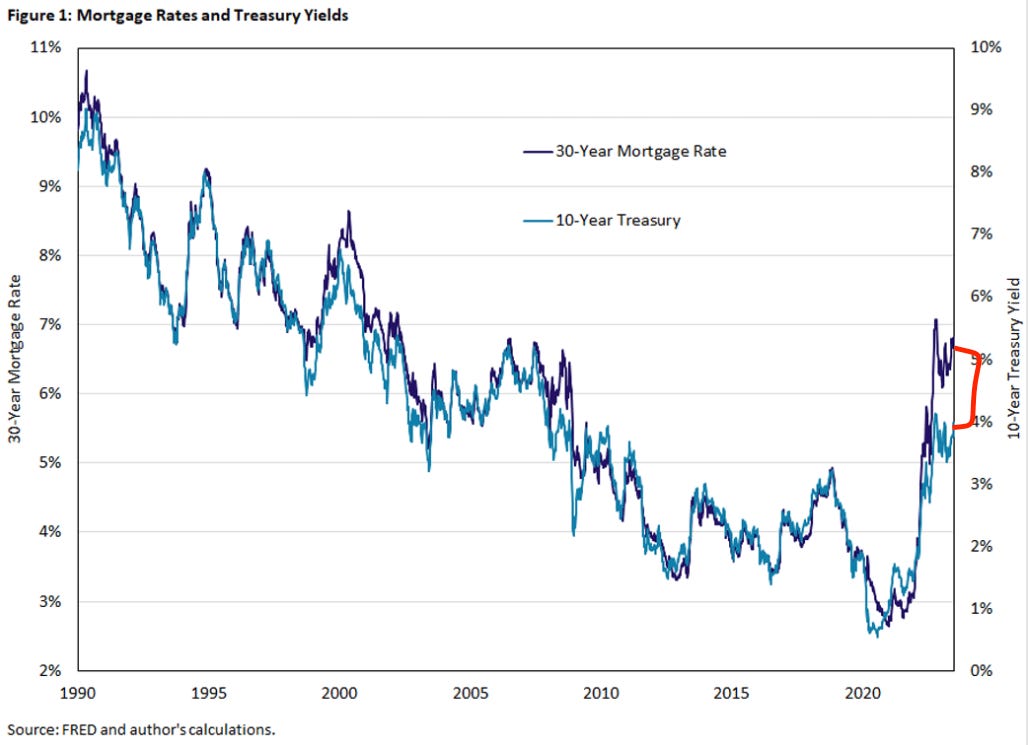

As we have highlighted before, in a normally functioning market, the 10-year Treasury rate closely tracks 30-yr mortgage rates. However, the difference between the two, the Spread, — has risen from 1.70% in January 2022 to 4.108% as of today, while the average 30-year fixed mortgage rate has jumped from 3.22% in January 2022 to 6.77% as of Thursday. The current spread between the 10-yr Treasury and 30-yr mortgage is therefore 2.662, much higher than the historical 1.74.

Why does this matter? If markets were functioning normally, at the historical average spread of 1.74, mortgage rates would be 5.848% today.

The Experts’ Take?

The Experts’ Take?

- - The Mortgage Bankers Association expects spreads to fall to 190 bps, Q4 2025.

- - Fannie Mae expects spreads to fall to 180 bps, Q4 2025.

When will the market for Treasuries and mortgage backed securities normalize, reducing the spreads, and when will the Fed cut rates? IMO, these market mechanics will likely not happen until mid-2024 and even then will likely grind lower, slowly. But combine lower spreads with Fed rate cuts in the witches cauldron and we have an optimistic 12-18 month outlook brewing, it is highly likely that mortgage rates will be lower in 2024 and even lower still in 2025.

***For us uber-finance nerds out there, a good article from the NY FED on understanding mortgage spreads in detail. Its a bit dated but contains a great explanation. And the author has a fantastic name, if I do say so myself :)

Home Prices in 2024? Likely continue up.Since the housing sector slipped into recession in the second half of 2022, after seeing a wild run-up in home prices during the COVID housing boom, prices are up. Most local markets bottomed January 2023. Depending on the data you look at, 2023 saw home prices rise 3% - 6%, near-ish the historical average. Of course, all real estate is local. In my home market of Nashville, we are up 9% since December 2022.

What am I thinking for 2024 & 2025?5% home price appreciation is a solid conservative number, for 2024 and 2025. In my opinion, higher interest rates are still throttling housing prices, keeping demand on the sidelines, especially for the newest, largest generation who are now looking to form a household and move out of mom and dads (or their 8 dude group frat house, said my 26 year old self). Home Prices in growth markets (Nashville, Dallas, Tampa etc…) will be higher in 2024. And every day rates & prices remain high, the number of homebuyers standing on the sideline, just waiting for the coach to put them in the game, builds and builds. When rates decrease and folks feel like they can pull the trigger, expect prices to punch up, likely 2x the current rate. IMO.

What about supply of available homes? Is there hope?

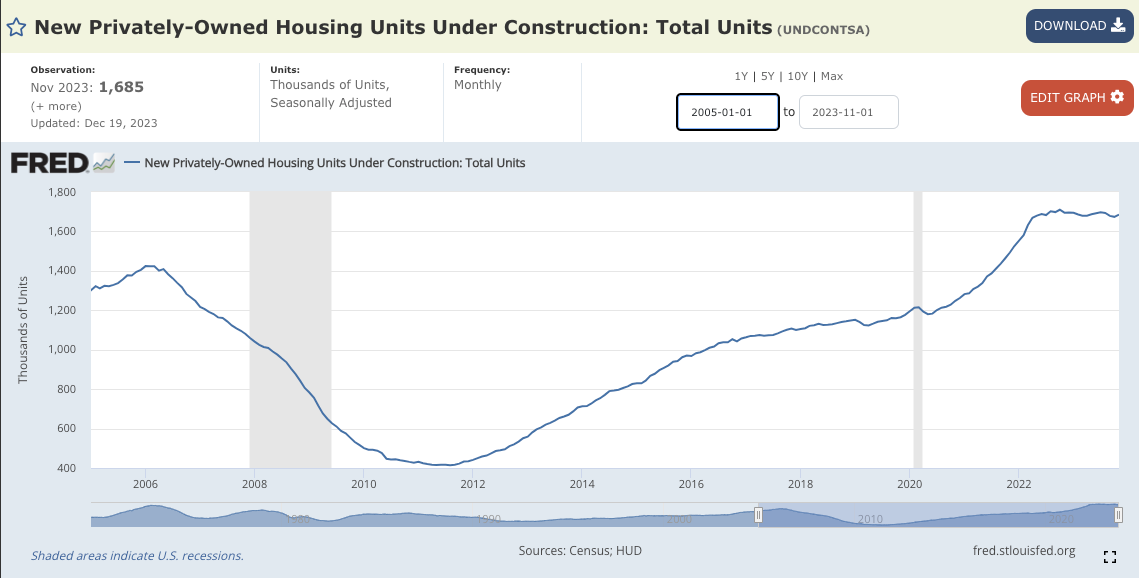

There just aren’t enough homes for folks to buy. The mortgage rate shock of the last few years didn’t = increased supply of listings. This is because 2 main sources of supply were/are being suffocated: 1) existing owners who were/are locked into 3% mortages, and 2) delinquencies/foreclosures which were/are still very low. Anyone who was at risk of foreclosure was likely able to sell their home for a positive gain pre-foreclosure. And 3), while new construction supply did increase, it’s still a minority of overall sales and not enough to move the entire market.

As you can see, builders did jump head first in to the market, when housing demand boomed during COVID. But we are now flat, and were underbuilding for years. Keep in mind it takes a while to build a house (2-3 years from start/land/permiting to finish).

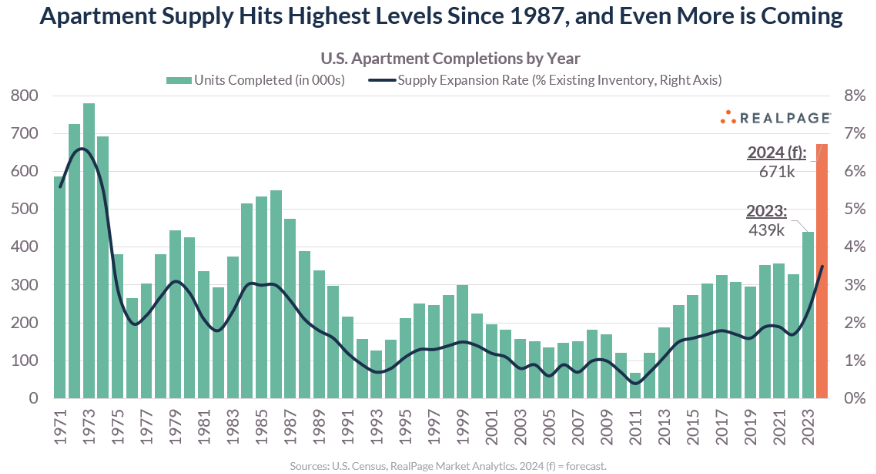

Housing Growth: ApartmentsOne important note: overall housing may not see an insignificant (but not sufficient) increased supply in one sector: multifamily apartments. While not exactly the ideal single family home you can purchase for your family/investment, it will put pressure on shelter prices. The catch? The pipeline of apartments coming on the market is spiking in 2024, but will plummet in the coming 2 years. Let’s review:

New apartment supply was at its highest level in 2023 (since 1987), more than 439,000 units came to market. “Here's the intriguing part: Last year was just the warm-up act,” says housing analyst Lance Lambert. According to forecasts from @RealPage property management, 671,953 apartment units are projected to be completed in 2024 (the highest since 1974).

While this is only about a 3.5% increase to overall apartment numbers, this should have an affect on apartment rent growth, or even rent declines in the sector (RealPage). “Most of the multifamily supply expected to come online this year will be in fast-growing Sun Belt markets, including Nashville, Austin, and Dallas.” Interesting. Since I’m on the ground in Nashville, I have to comment. Strong apartment growth here has not translated into lower rents in the single family or small multifamily sector here; in fact, quite the opposite. Home rents are appreciating more than inflation, particularly as home ownership costs such as insurance and building materials increase. For it’s part, Invitation Homes, America's largest single-family home landlord, saw the same in 2023, reporting a 6.2% increase in single family rents. Of note: I am only talking about single family or small multifamily (2-4 unit) homes.

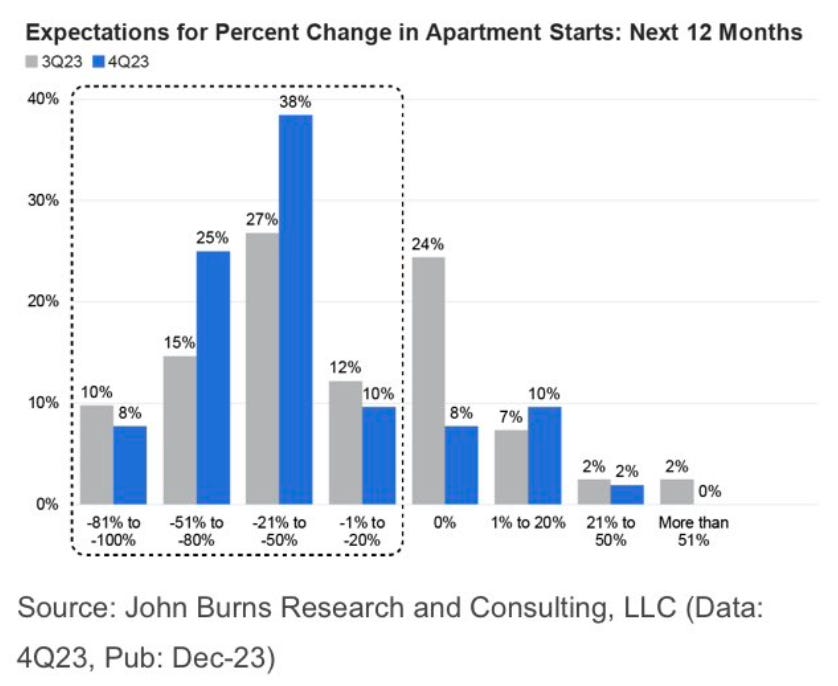

2025 is a Much Different Story for Apartment Construction.

2025 is a Much Different Story for Apartment Construction.

According the RealPage, “the [2023-24] wave of supply is resulting from construction starts that began back when rent growth and occupancy rates were at/near record highs… and consequently, [apartment] starts have plunged. Supply will drop way off in 2025-26.” One-third of apartment developers surveyed in December expect new apartment starts to fall by more than 50% over the next 12 months, up from 25% when they asked 3 months ago (John Burns).

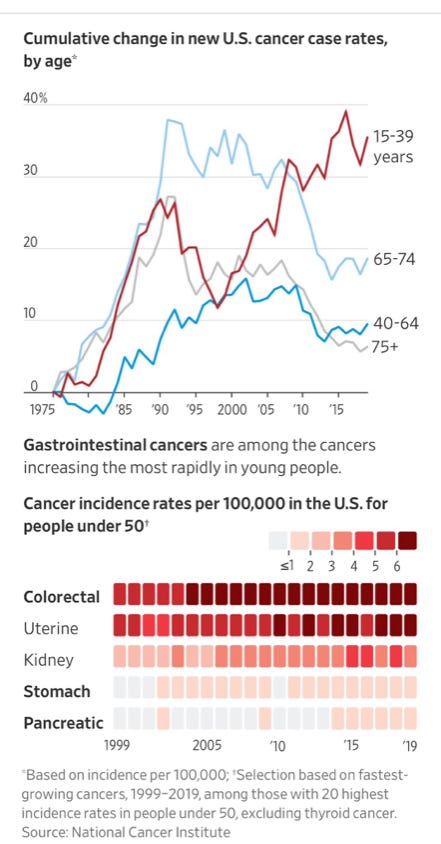

* TANGENT Alert - U.S. Cancer Rates are Drastically Higher sine 1970s -Why? Food Companies are Roofying our Food with Sugar.

* TANGENT Alert - U.S. Cancer Rates are Drastically Higher sine 1970s -Why? Food Companies are Roofying our Food with Sugar.

We’ve been duped for decades about food: Turns out sugar isn’t benign. It’s the real poison. Fats aren’t actually bad. They are essential. Carbs aren’t terrible. Sugar activates cancer mechanisims (NIH). There are now 250+ names for sugar, to try to “trick” folks into thinking it’s not in our food. I can’t recommend this discussion with Neuroscientist Dr. Andrew Huberman and Endocrinologist Dr. Robert Lustig. The clinical data is out. Sugar (especially w/o fiber) is poison.

Cancer in the areas of the body that process sugar and produce / affect insulin are up in a way that is endemic.

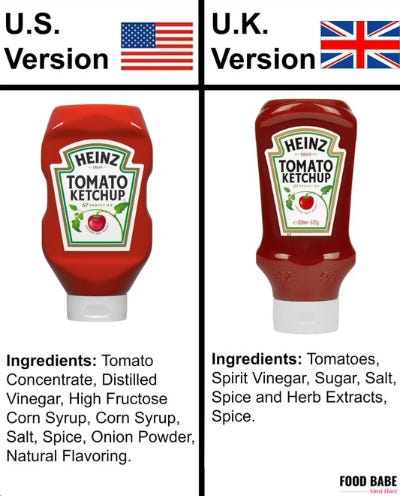

Why do Americans have a particular propensity for obesity / cancer? It’s our food. Let’s take ketchup for example. Now, this food is usually always high in sugar BUT just look at the extreme difference. Same company, “same product.” Ever been to Europe? Folks are not as overwight as in the US, and the sad thing is that it may not be our fault.

Sorry, got on my high horse right there. I digress….

Bottom Line

There is reason for optimism on interest rates. All this being said, this Skeptical Dude is remaining cautious, a wider spread is cyclical and unfortunately usually occurs during periods of financial market stress, such as when the economy slips into a recession. And spreads could be wider for longer than the market is planning for. One of the reasons spreads will remain elevated is MBS investors don’t want to buy, concerned that future lower rates will result in refinancing of mortgages to lower rates, a risk for these investors called early prepayment. MBS investors want to see refinances (prepayments) slow. Thus Skeptics, we should remain cautions of becoming overly bullish by assuming mortgage rates will be lower in the next 3-6 months. Additionally, the Fed stopped buying MBS when they started tightening in 2022, removing a massive buyer from the marketplace.

Further Thoughts: Barring a Black Swan event, the housing market should appreciate more in 2024 than 2023, particularly in growth markets. Falling mortgage rates will (slowly) increase demand, accelerating when we get below 6%. Housing supply will remain lower than demand, propping up prices regardless of rates.

In other words….Stay alert, stay skeptical, all you dudes and dudettes.

Most Interesting Tweet(s) of the WeekOptimistic for 2024, cautious for the next 4+ months. Agree.

AND

Ok, now I want a really potbelly pig...major FOMO.

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me directly on BP! I try to answer all the messages I get.

Again stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

- Andreas Mueller