Market Trends & Data

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated about 1 year ago on .

Real Estate Market Update: Insurance companies are hiking rates 20%+ in 2024!

Hello all and welcome to the new year! It's January 10th, 2024 and here is a brief, hopefully insightful, dive into real estate and financial markets.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Interest Rates: Down Sooner, or Later?

- - Consumer Update: What is the Qualified Mortgage and Why Does it Matter for the Real Estate Market?

- - Property Insurance Alert - Many Premiums Increasing in 2024

Today’s Interest Rate: 6.80%

(☝️ .03% from this time last week, 30-yr mortgage) The Weekly 3: Data and News to Keep You Informed- ADUs Gain Momentum Nationwide: Accessory Dwelling Units (ADUs) are growing in popularity, especially with the rise of the work-from-home trend as a way to offset mortgage costs from high interest rates (JBREC)

- The housing market’s ‘lock-in effect’ is very real: Most sellers are buyers, naturally they have to move once they sell their home. 3% interest rates mean they won’t sell until rates come down (Fortune).

- Yellen Declares US Economy Has Achieved Soft Landing: Too soon to declare mission accomplished? (Janet Yellen)

Mortgage interest rates were essentially flat this week, but down 60 basis points (.6%) from last month. As we saw last week, despite interest rates beginning 2023 at 6.2%, housing prices ended up 4.8% YoY in October, according to Case-Shiller. Nov / December numbers are still being tabulated nationwide but this number should hold. And in my home market of Nashville, TN the data is out (thank you real estate license). We were up 8.5% YoY, ~ double. Interest rates are still too damn high for a healthy market, but just like politics, all real estate is local, and certain areas continue to emerge from the 2022 real estate recession nicely. Not everyone can, but those who can afford the higher mortgage are taking advantage of low-er prices today. I.e. if home prices increase 5% as they did last year and the average home in America is now $431,000 - that same home will be worth $452k January 2025. Put another way, those able to buy today will be $21k richer that those who wait. By doing nothing.

My Thoughts5% home price appreciation is a conservative number, for 2024 and 2025. In my opinion, higher interest rates are suppressing housing prices, which are keeping demand on the sidelines, especially for the newest, largest generation who are now looking to form a household and move out of mom and dads (or their 8 dude group frat house, said my 26 year old self).

Case in point, holiday mortgage demand was strong this year. Last week mortgage applications and refinancing demand was up 5.6% and 18.8% respectively (Mortgage Bankers Association).

So where do “the experts” think rates are going from here? We have a super special poll for that. According to the Fannie Mae Home Price Expectations Survey - comprised of 100 experts across the housing and mortgage industry and academia - rates should settle at 5.7%. Hot take, IMO, the “experts” are off. Bond spread regression to the historical mean alone should get us to 5.65%. Once the Fed stops trying the engineer the economy, and cuts rates, I think we settle at 5% or slightly below, in 18 months. Disagree? Feel free to tweet / DM at me! Bring it.

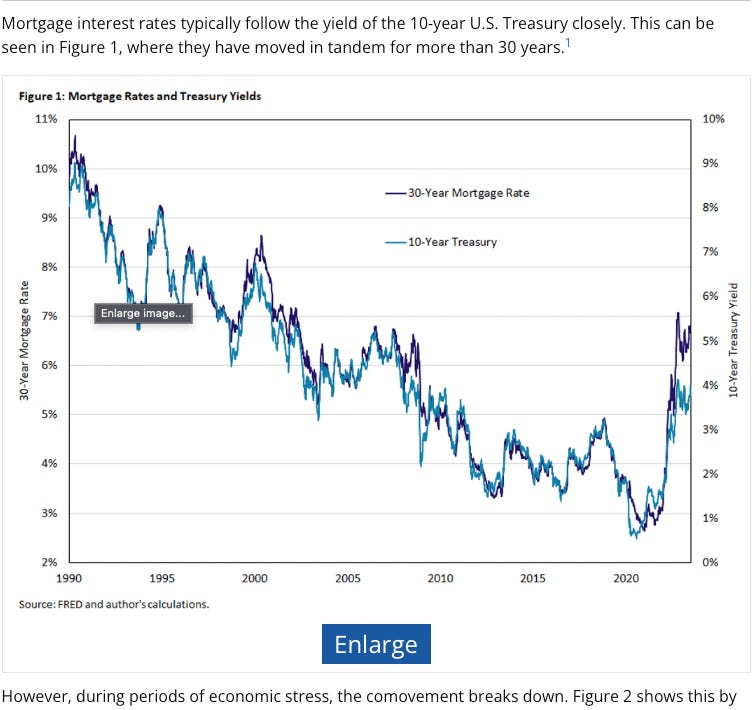

Chart of Historical bond / mortgage spreads

Chart of Historical bond / mortgage spreads

What do consumers think? They haven’t a clue… In December, 31% of consumers indicated that they expect mortgage rates to go down, 31% expect them to go up, and 36% expect rates to remain the same (Fannie Mae). Until this shifts towards cuts, available existing home supply will remain low. Of course consumers surveys are notfor making predictions, but they do matter. It’s a good directional signal for consumer confidence and the consumer is 2/3 of the US economy. And for the record anyone who tells you they know for sure what going to happen in the future is either lying, lazy or stupid.

How fast will rates drop 2024-2025? Well, that’s even harder to predict. The bond market is pricing in 6-7 rate cuts (.25% each) in 2024. The Fed has said they expect to do 3. In the end, it will depend on the strength of the economy, most likely the labor market. If unemployment remains below 5%, I would argue we have a longer cycle of rate cuts: 2 in 2024 and 4+ in 2025, with the cycle ending in mid-2026. This is the skeptical approach, dudes and dudettes, and I recommend you always plan for lower expectation, like Robert DeNiro’s character in Heat said, “Don't let yourself get attached to anything you are no willing to walk out on in thirty seconds flat if you feel the heat around the corner." Always have a plan for the tough times.

To which, U.S. Treasury Secretary Janet Yellen says…hold my beer, saying last week, “What we’re seeing now I think we can describe as a soft landing.” Soooo, mission accomplished? 😬 For its part the Fed is taking a much more skeptical approach. And Yellen’s comment was a departure from her previous comments where the said she saw only “a path” for a soft landing. (As a reminder, a soft landing is—loosely—when inflation recedes without a coinciding recession.)

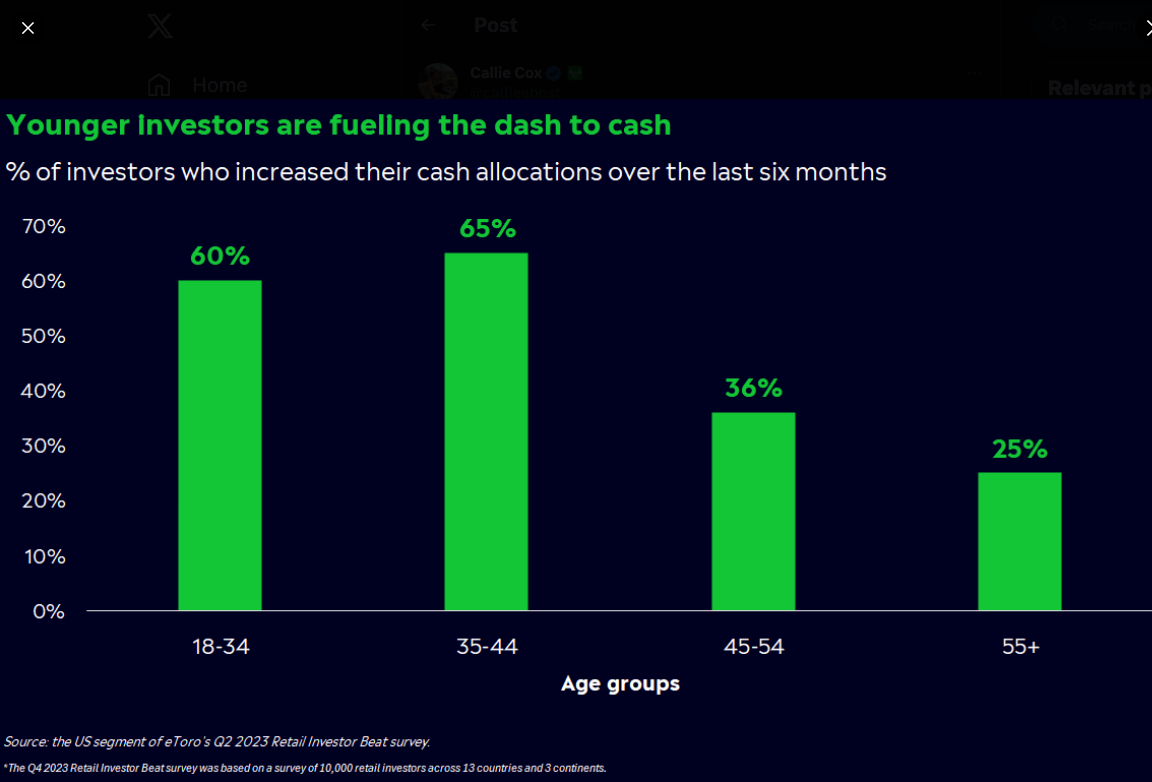

The consumer may be prepping for the “Heat,” by stacking some cash. Of Gen Z and Millenials - those likely looking to purchase a home and are more affected by rates remaining high - are stacking cash. 63% have increased their cash allocations in the last 6 months (vs. just 27% of investors 45 or older) (eToro, @callieabost).

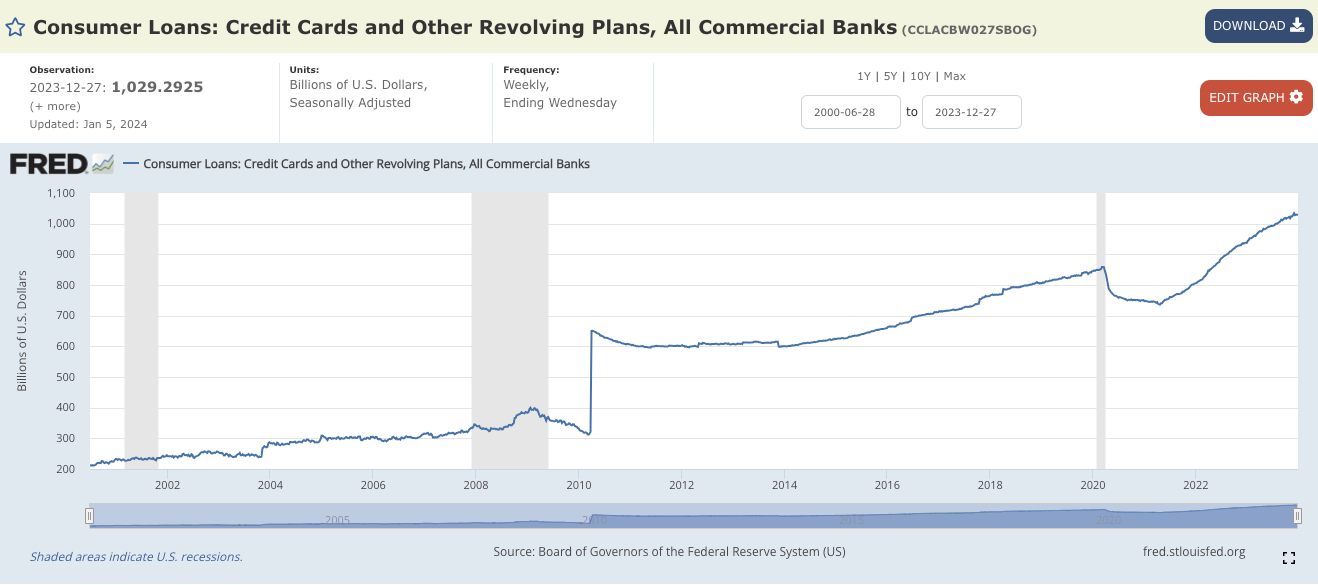

Counterpoint: US consumers now have a record $1 trillion in credit card debt, according to the Fed. And as you can see below, this amount spikes during times of economic tumult. Another indicator to watch as the Fed navigates 2024. Yellen’s soft landing call seems highly pre-mature, IMO.

Counter Counter point: unlike the last recession in ‘08-’09 (not counting the 2 seconds during 2020 government imposed lockdowns) we now have the Qualified Mortgage law. And for those of us reading this because we are interested in the housing market, this REALLY matters because if the economy goes to sh!^ the housing market will remain far more resilient.

What’s qualified mortgage? In short, “The Ability-to-Repay/Qualified Mortgage Rule (ATR/QM Rule) requires a creditor to make a reasonable, good faith determination of a consumer's ability to repay a residential mortgage loan according to its terms (Bureau of Consumer Financial Protection).” Why does it matter? You must watch this brilliant scene from the movie The Big Short to fully understand:

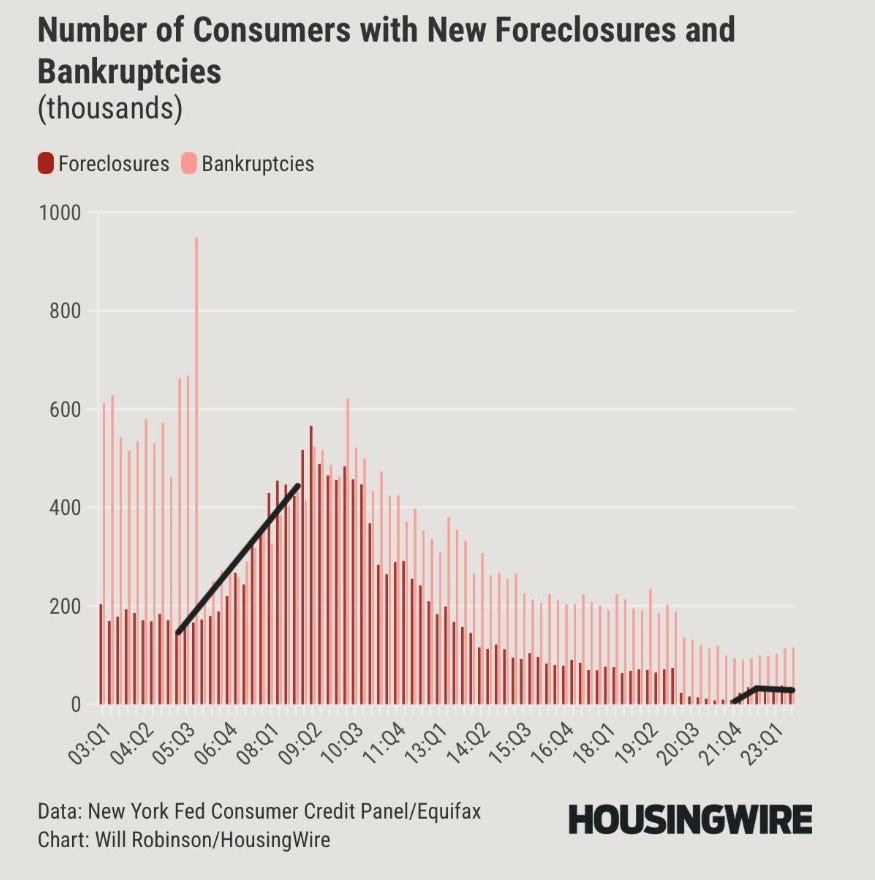

As one of my favorite cheeky analysts Logan Mohtashami(@LoganMohtashami) is fond of saying, the 2010 “Qualified Mortgage Matters. This means everyone [homebuyers] is more legit now than at any time in history.” “[Leading up the the Great Recession (2005-2008) unemployment was low and falling; yet, foreclosures and bankruptcies were rising.]”

Before 2010, banks/lenders literally didn’t do this…Really… it was insane, and I was working as a staffer in Congress when we realized this. This is not the place for politics but let’s just say folks were asleep at the wheel. Nuts.

So what’s the point? We now have rising consumer debt levels and low unemployment, which one could argue is similar to the lead up to the Great Recession. The difference is the housing market will be more resilient to an economic slowdown/downturn. The Qualified Mortgage matters.

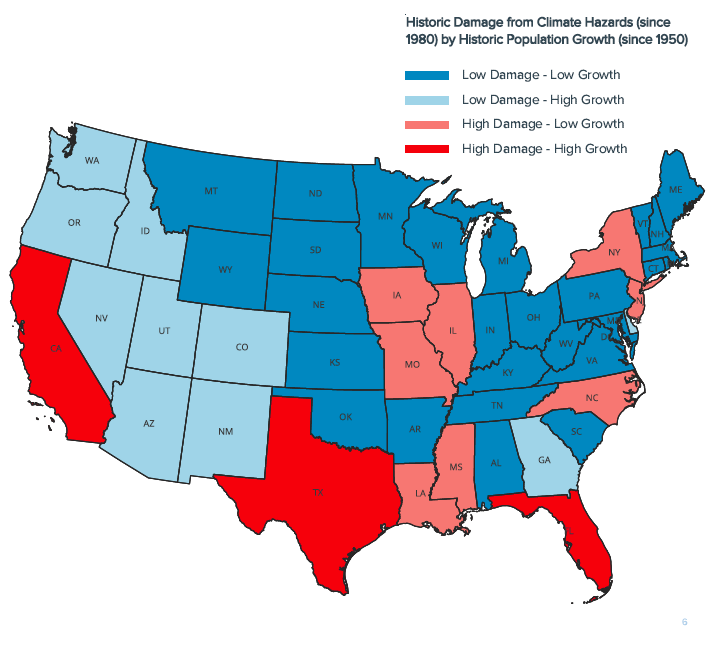

Insurance Shockwave on the WayHome insurance is slated to increase significantly in 2024, especially in areas with above average weather events: read TX, CA, FL. Case in point, State Farm will raise rates 20% in CA starting March 15th, 2024. State Farm is the largest home insurer in CA (SF Chronicle). And in FL, premiums increased 102% the last three years, 3x the national average (Insurance Information Institute). Worried about your home’s/business’s insurance premiums? Get this free report here from First Street Foundation, showing at risk areas of the US.

Do you live outside CA, TX or FL? You won’t escape the projected increases. In fact, their situation affects your insurance prices, just like your health care insurance costs are also directly related to the health care needs of others. Why? Well, in brief, insurance is about distributing risk. And insurance companies have an app for that. They purchase reinsurance, to insure the insurer (and some rely heavily on re-insurance, like I believe startup Lemonade does, allowing them to “very capital light mode”). This means, when an insurer makes a claim with their reinsurer, who also reisnurers other insurance companies, the price of reinsurance goes up, which the insurer passes on to you. I know that reads like word salad but stay with me. So, for example, insurance company 1, 2 and 3 uses reinsurance Bravo Company. So if insurance Company 1 has to pay out claims, say for the latest disaster in FL, and is reinsured by Bravo Company, Bravo Company will likely raise rates not just on Insurance 1, but also 2 and 3, distributing their risk and recouping costs. This is how even a hurricane Mexico can increase your insurance rates win New York.

Nationwide, the insurance industry predicts that "We're going to see double-digit increases again in 2024. We don't have an exact number at this point, but we're hopeful it will be much lower than 42% [the increase in 2023] (Insurance Information Institute)." For us real estate investors / landlords, insurance premiums mean cash flow compression, resulting in the unfortunate fact, passing on some of that cost on in the form of rent increases to our residents. No bueno.

Anecdotally, I was just texting with my insurance broker, who is fantastic if you need someone and are in the South, and who let me know it’s just a new reality. We are seeing premium increases across the board amongst all insurers in 2024. From her: “One thing a lot of carriers are doing to try and combat the losses is moving to a percentage deductible (meaning 1 or 2% of the dwelling amount). Overall, the insurance carriers need to make sure they are still bringing in enough money to be able to pay for these huge catastrophic claims that are happening more and more frequently.” A note on messing with your deductible: your lender has to approve any larger deductible and has their own standards for coverage, so make sure to check with them first! Don’t learn that the hard way. And make sure they are covering the cost to rebuild the home in case of catastrophe, not just calculating it based on current value.

When my properties renew this April, it’s going to be painful.

Bottom Line

2024 will be action packed, to say the least. Will GDP slow? What will happen to rates? Will the Fed be able to bring us in for a landing? (or have they already) Oh by the way, there is a Presidential Election 🤦….Regardless, we all can make moves to protect our downside. For instance, you can call your insurer and find out if they are increasing rates significantly in 2024. Then do what I do with my cable/cell/streaming company, go quote shopping.

Are you looking to invest in real estate in 2024? Start saving / setting aside / raising that money now. I believe we should see at least a couple rate cuts, and housing supply should tick up. More deals should be out there to be had. But be careful of building into your numbers lower rate assumptions that are overly optimistic. And remain cautious of tail risk (low likelihood, high consequence events).

In other words….Stay skeptical all you dudes and dudettes.

Most Interesting Tweet of the WeekOn the nose. This made me spit up my coffee laughing. #smallwindowsandwhiteplease

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me direct, I try to answer all the comments I get.

Again stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

- Andreas Mueller