Welcome fellow BP Compatriots! I thought I would share my brief, hopefully insightful, dive into real estate and financial markets.

Today I'm talkin’ the topsy-turvy mortgage market, consumer sentiment, Mayo lattes?, and I take a closer look at my home market of Nashville.

Today’s Interest Rate: 7.46%

(👇 .42%! from this time last week, 30-yr mortgage)

Market Ruminations

Mortgage interest rates dropped considerably in the last 7 days, a well-welcomed reprieve from seemingly ever-increasing rates. I was sick of sounding like a broken record, talking about broken records.

Mortgage rates are determined by trading in the bond market, which take cues from many sources. For instance, yesterday, weak economic data in Europe put downward pressure on rates globally and perceived dovish comments from Federal Reserve speakers allowed bonds to hold the gains. The average mortgage lender was able to offer lower rates nearly every day for the last week. We aren’t out of the jungle yet, far far from it, but it’s directionally positive.

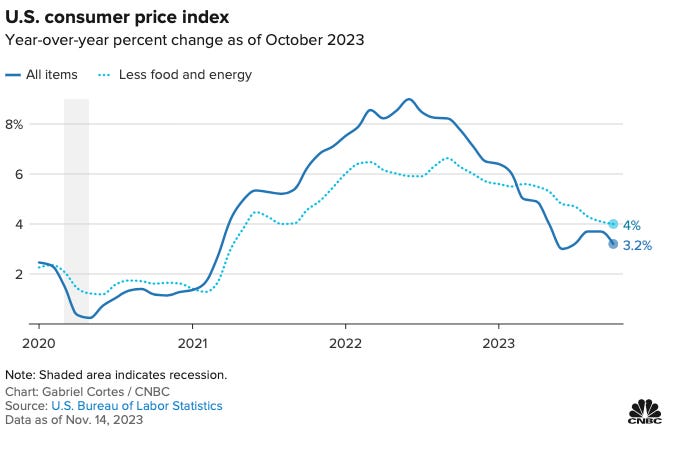

The US economy is humming along, remaining resilient in the face of high costs of capital/interest rates. Deflation is slowly ticking down the various price indexes, despite personal consumption remaining strong. Core PCE was however down to 3.7% in September, the lowest reading since Q2 2021. Not yet the 2% the Fed would like but again, directionally positive.

The Fed, while not increasing interest rates during their meeting last week, are quietly continuing Quantitative Tightening. Each month, the Fed has allowed $60 billion in Treasuries to mature and roll off their balance sheet. As the Treasury continues to issue new bonds to fund Congress’ tremendous appetite for government spending, we should continue to see volatility in the bond market, and by extension, mortgage rates. The next 2 months should tell us a lot about 2024.

Mortgage Market Status Update

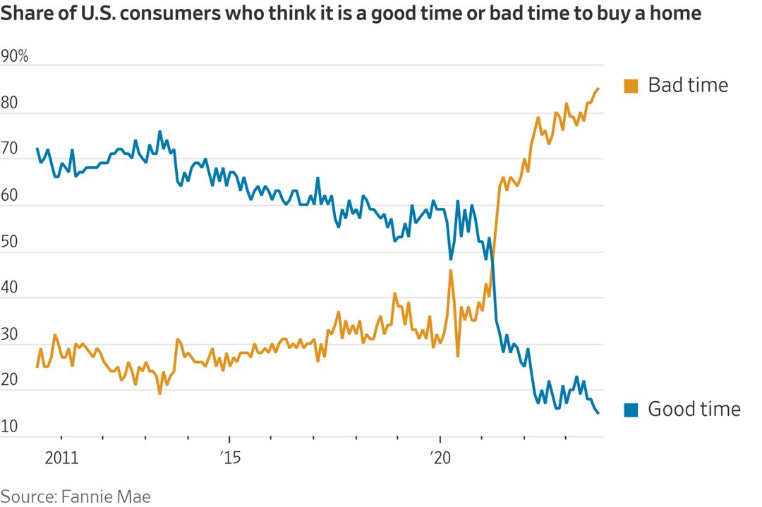

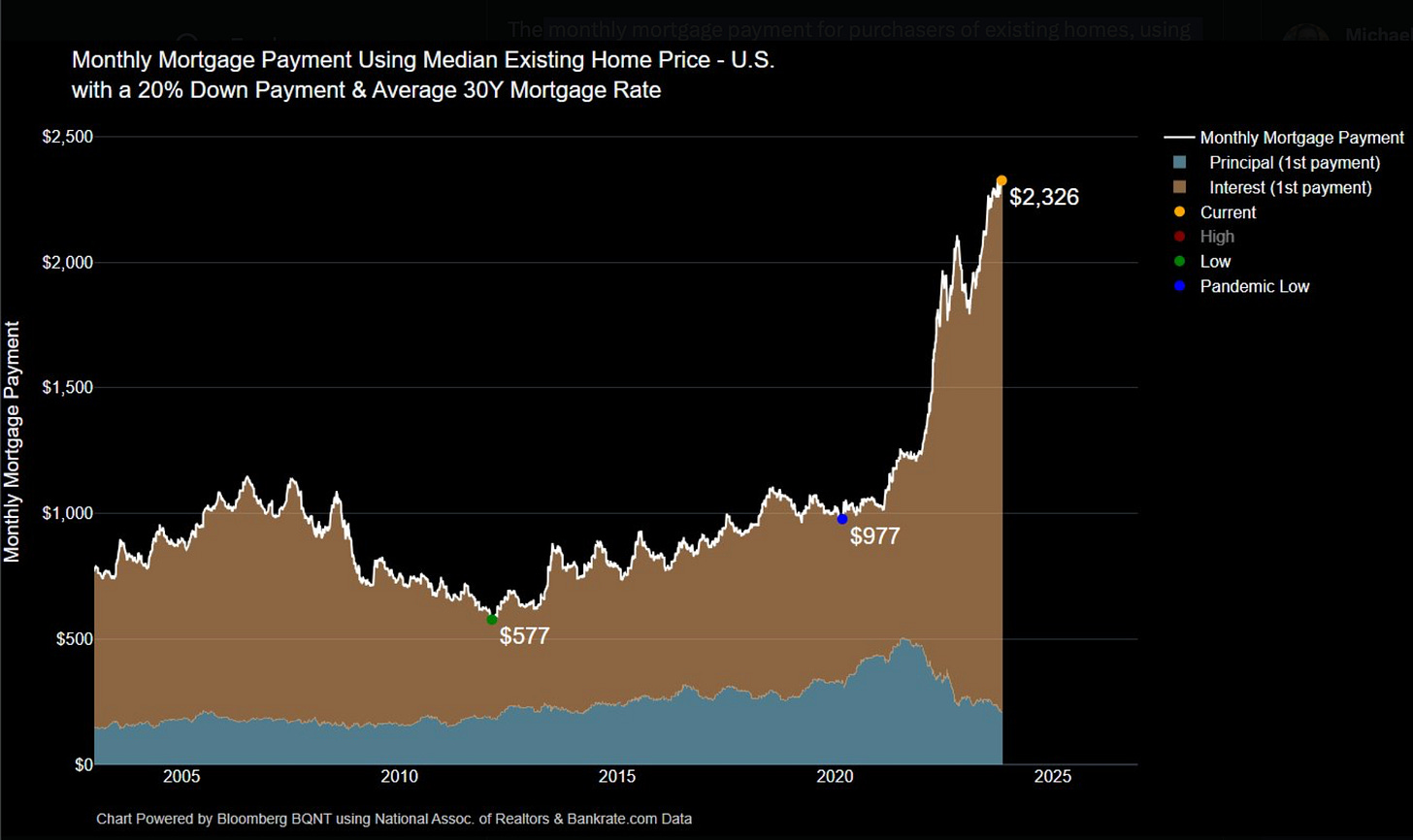

Average monthly mortgage payments (existing homes) are still elevated, a record high $2,326, a substantial increase from $977 in March 2020. But that's not the story….

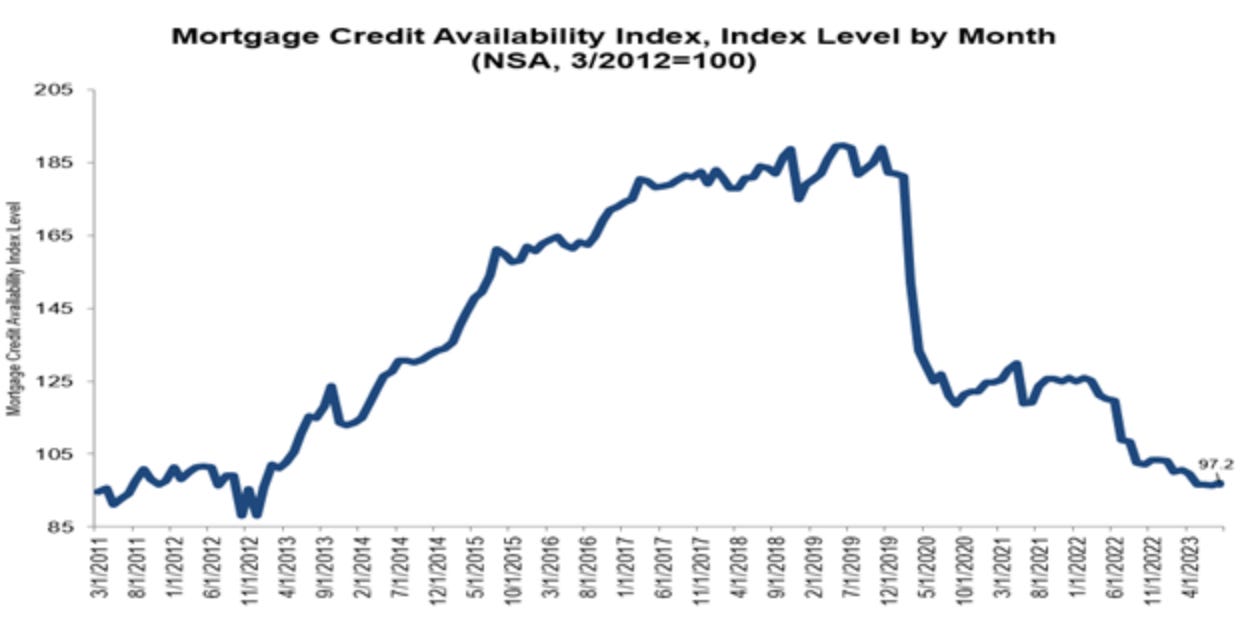

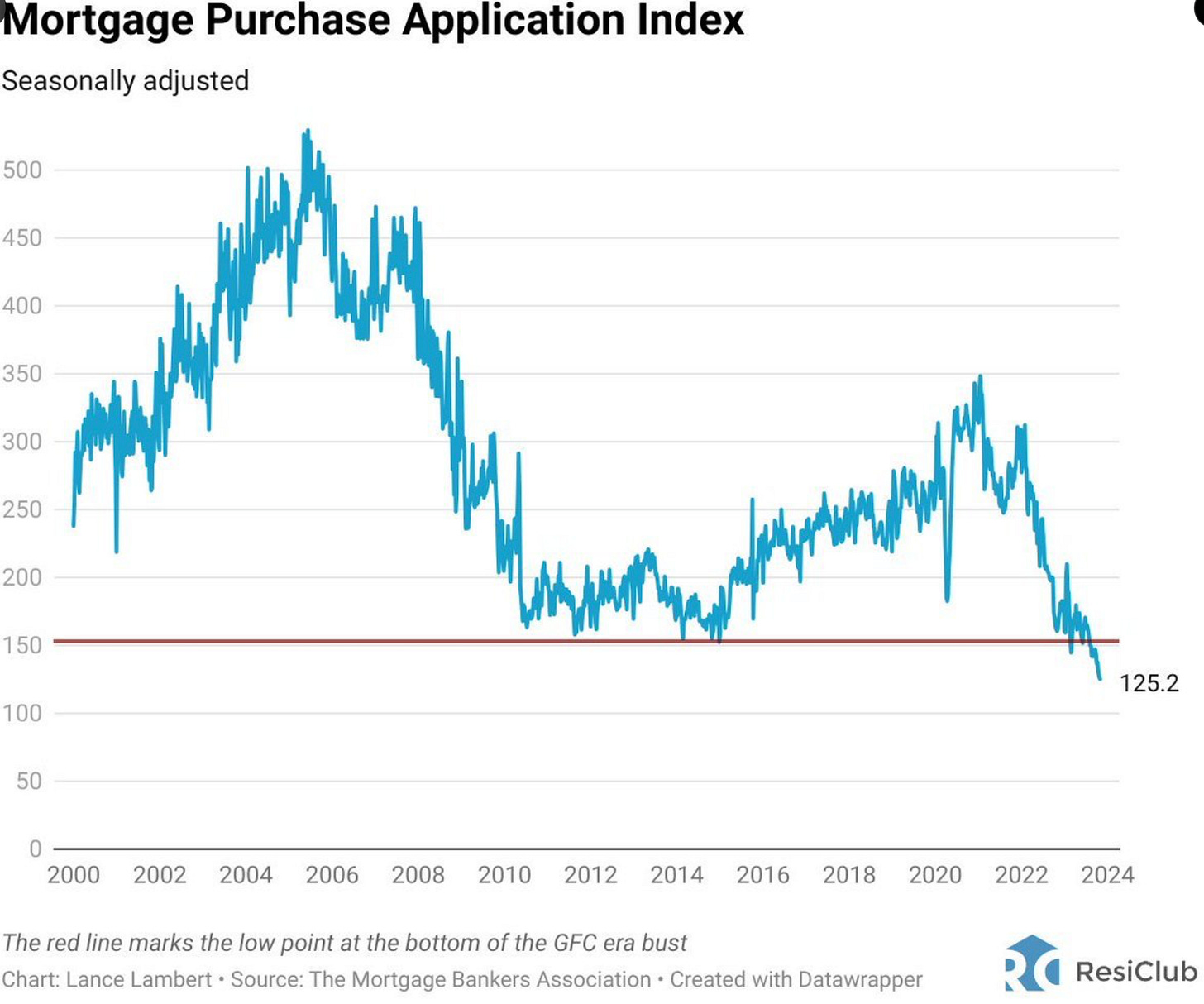

The mortgage market as a whole is in complete and absolute disarray. This week mortgage applications hit a low not seen since 1995.

One result: mortgage industry employment is down 20%. Why? Higher interest rates = fewer loans and higher costs. The Senior Loan Officer Survey this week cited “uncertain economic outlook” and “deterioration in the credit quality of loans and collateral.” But… banks reported being “more likely to approve credit card loan applications.” Really? (more on this below).

And Some lending institutions are even trying to claw back hiring bonuses previously given to employees! (great WSJ article).

What’s happening in the mortgage industry? A LOT of distrress is leading to mergers and firings, in just the last few weeks, this happened: (Big credit to @NewsLambert)

- Lower to acquire Universal Lending retail and wholesale operations (11/1/23)

- Trustar Mortgage acquired by Archer Mortgage, LLC (11/1/23)

- People’s Bank of Commerce to exit residential mortgage lending (10/27/23)

- BMO Bank cutting 228 jobs in Northern California (10/25/23)

- Homestar Financial to wind down operations (10/25/23)

- City National Bank layoffs in Los Angeles total 71 (10/23/23)

- Hometown Lenders layoffs (10/12/23)

- First Savings Bank to lay off 135 mortgage workers (10/4/23)

- Wesley Mortgage absorbs competitor Colten Mortgage (10/4/23)

- Cenlar to lay off 85 in Ewing, NJ (10/2/23)

- Rithm Capital to acquire Computershare Mortgage Services Inc. (10/2/23)

- Wells Fargo cut 525 jobs in South Carolina (9/28/23)

- Better Mortgage lays off additional employees (9/22/23)

- The Graystone Company has acquired Direct Mortgage (9/13/23)

- Flyhomes to purchase certain assets of Home Sale Assured (9/13/23)

- Divvy Homes to cut 95 jobs in San Francisco (9/11/23)

- Farmers-Merchants Bank to sell three branches to focus on core mortgage business (9/11/23)

- It goes on…..The mortgage industry is in a starkly deep recession.

And RIP refinances, unless you are holding an even higher interest rate loan (like a construction/bridge loan or hard money, or perhaps you just fixed your credit. Then by all means).

Consumers

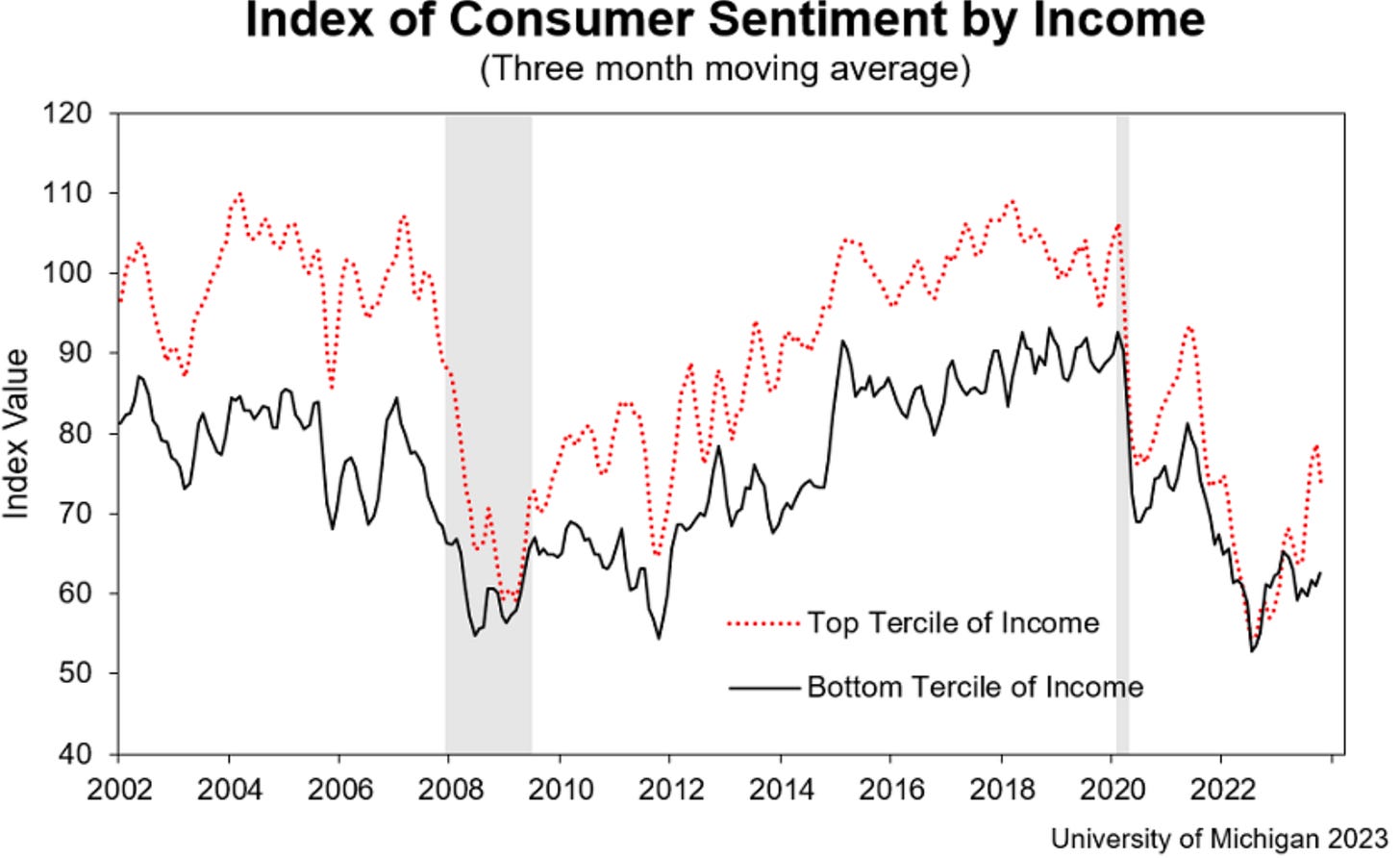

So how are consumers feeling? After 2 months of flat readings, consumer sentiment fell about 6% this October. This decline was driven by consumers concerned about deteriorating stock holdings, business conditions (plunged 16%) and expectations over personal finances (fell 8%), reflecting ongoing concerns about inflation and uncertainty over headline news abroad. Inflation expectations for 2024 reversed, rising to 4.2% from 3.2% last month, the highest reading since May. Long-run inflation expectations edged up from 2.8% last month to 3.0% this month. Again this is sentiment not actual. But the signs of uncertainty can become self-fulfilling and could be leading indicators.

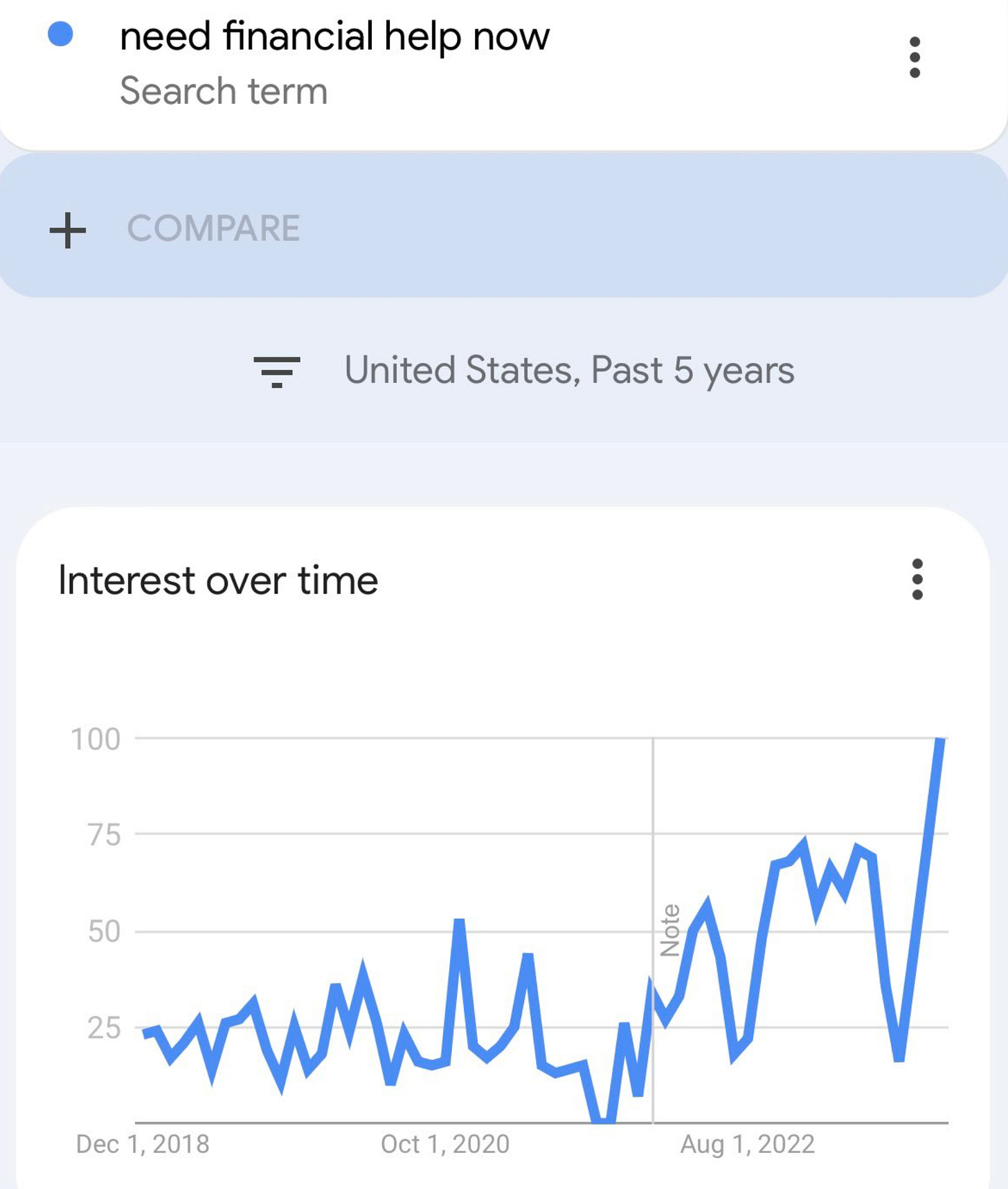

Anecdotally, google searches for the phrase “need financial help now” are straight up and to the right. 😱

A Closer Look: Nashville Market

It wouldn’t be my opinion without a little flavor from Nashville in the mix from time to time…Below is a quick snapshot of the economy in the Nashville area for October.

TANGENT! The Tennessee Titans have a new quarterback, rookie Will Levis, who took over after an injury to starting quarterback Ryan Tannehill, and he has an interesting coffee routine: he puts mayonnaise in his coffee. Not kidding. But! Before you laugh and spit up your own coffee like I did, this little quirk recently earned him a lifetime sponsorship by Hellmann’s brand. (and he threw 4 touchdowns during his debut). Amazing. When will your coffee shop add Mayo Lattee to the menu? Probably better than almond milk (sorry, yuck!).

Ok, I Digress…..

Back to Nashville:

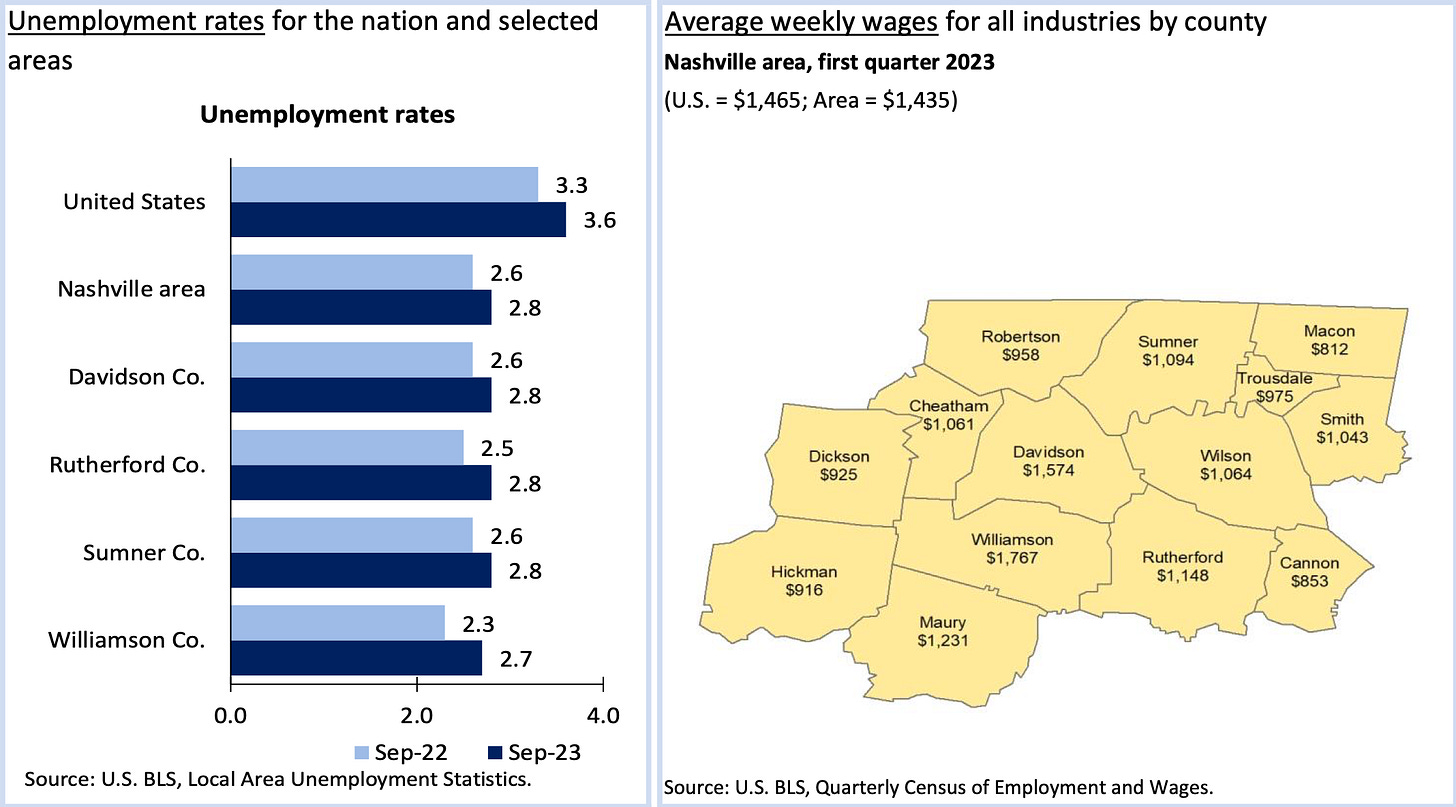

For October, unemployment in Nashville ticked up slightly to 2.8%, in lockstep with national increases due to tight/expensive credit, but still remained nearly 1% lower than the national average. Average weekly wages were at $1574, 7% higher than the national average.

EditSign

EditSign

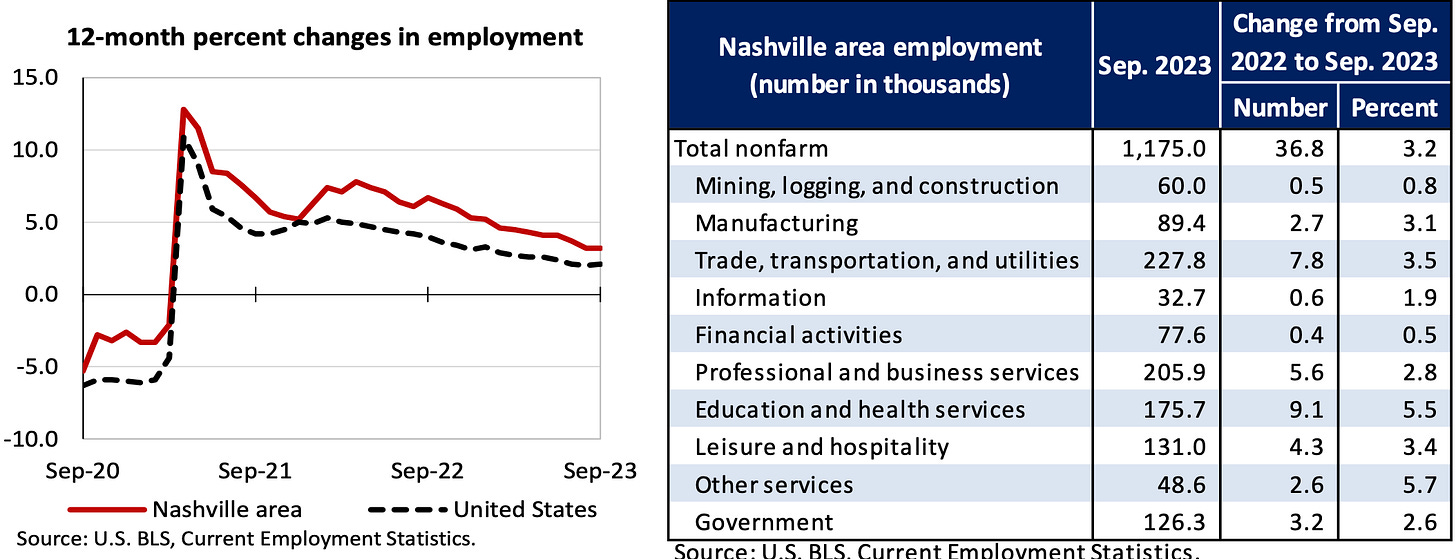

Emplyemnt was positive across nearly all categories, most notably in Education and Health services.

EditSign

EditSign

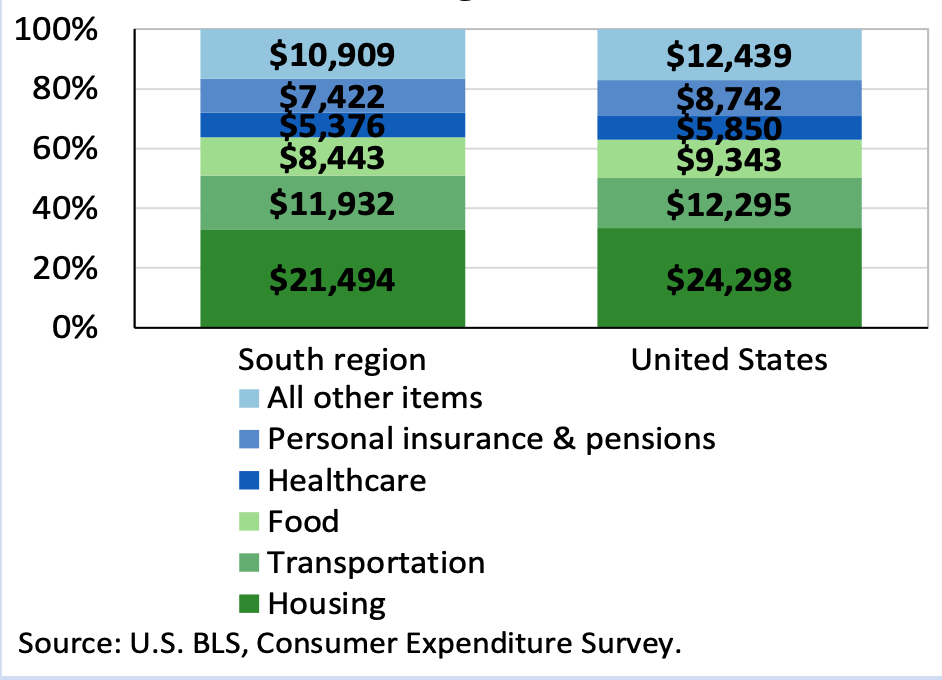

Average spending distribution remained lower than overall US, and despite the rapid growth in the City over the last 3 years, spending on housing costs is still lower than the national average by 11%.

EditSign

EditSign

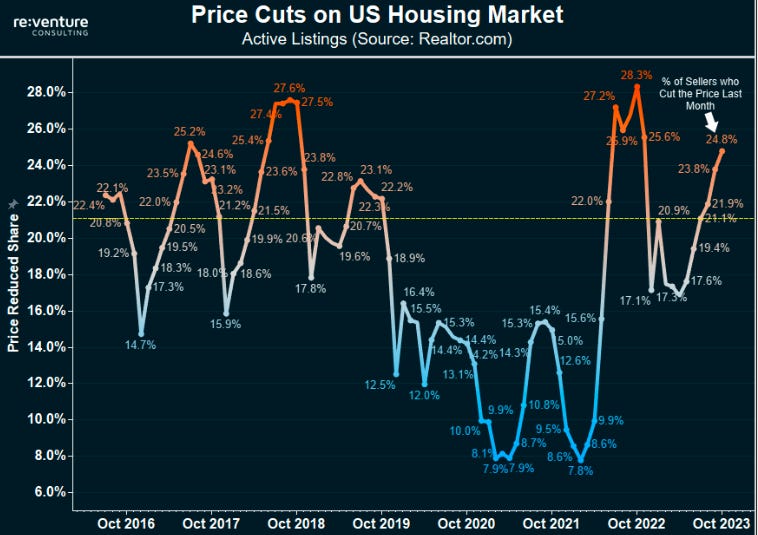

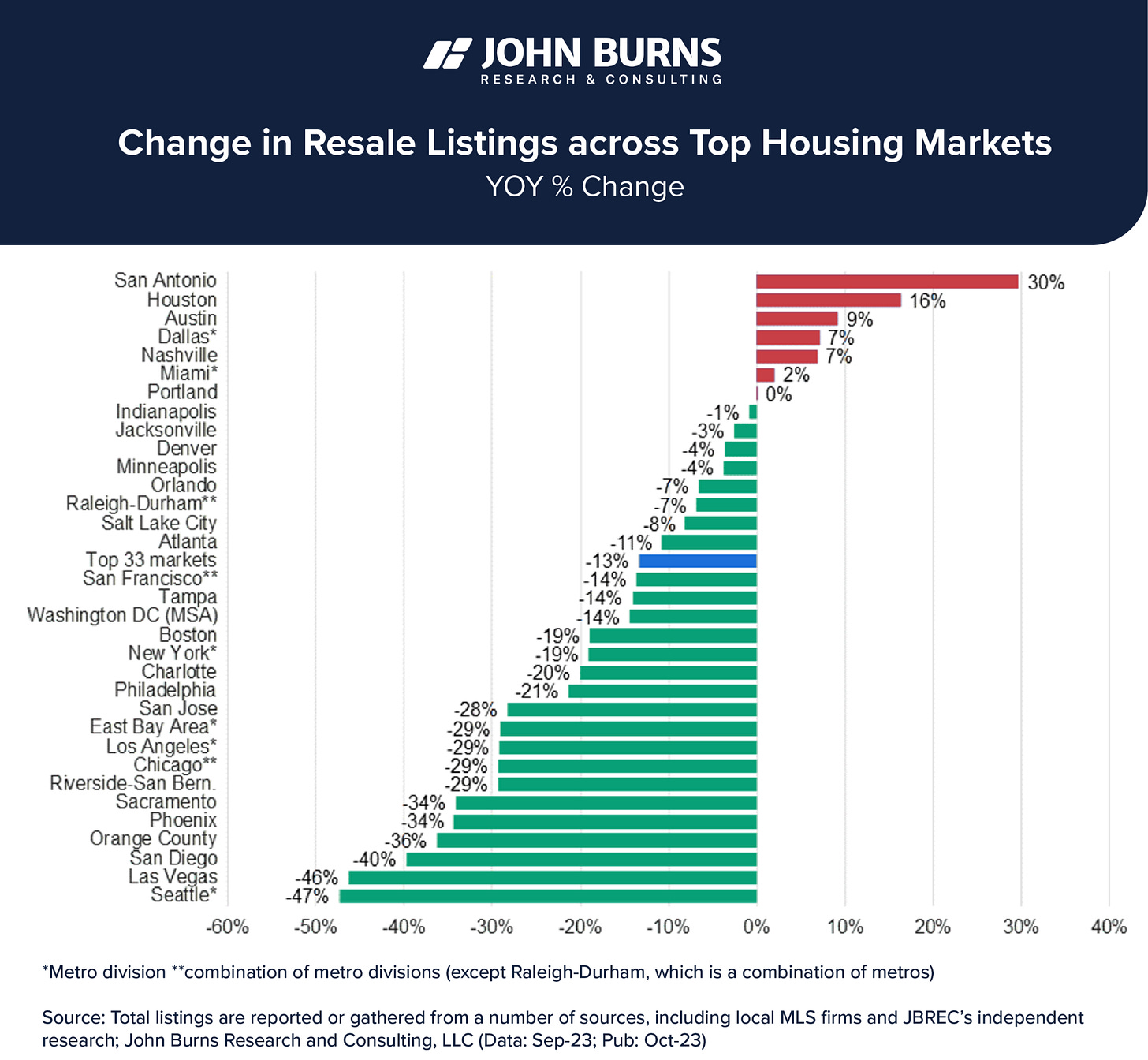

Real estate activity, unlike most markets, is remaining more energetic than most markets. YoY property listings were up 7%, while most markets retracted.

Nashville Development

Dozens of exciting real estate developments are popping up all over the city. Here are a few, curtesy of Beata Lorincz.

Feature Development: Neuhoff

(* Fun fact, in German “Neu” means new and “hoffen” is to hope. Pretty deep for a real estate development.)

In 2019, developer New City Properties acquired a 14-acre site in Nashville’s Germantown neighborhood, on the western bank of Cumberland River. The site comprised buildings that used to house a meat packing facility built in the 1920s. In mid-2021, the company joined forces with Cousins Properties and entered into a joint venture partnership to develop Neuhoff, a new mixed-used development. Cousin’s $275 million investment secured a 50 percent ownership in the project’s first and second phases.

The first phase is set to include 388,000 square feet of office space, 60,000 square feet of retail and 542 multifamily units, a new 14-story office building, as well as the adaptive reuse of an existing structure dubbed the “curved building.”

John Clifford, founding principal at S9 Architecture—the studio behind the design of Neuhoff—told MHN that the development establishes a new sub-neighborhood that connects Germantown in the north, south and west. The project’s other main goals include maintaining the slaughterhouse buildings, as well as creating public access to the river.

For more Nashville developments, see her fantastic article here.

Bottom Line

High cost of capital be damned, the US economy, and even more so my local market in Nashville, remain strong. Robust GDP growth and deflation, albeit slow, are holding into the holiday season. Consumers have uncertainty yet continue spending. This is good.

But much uncertainty remains. Take consumers for instance, yes they are continuing spending, but is it mostly plastic? Today, US consumers, since 2019, acquired 70 million more credit cards. 70 million in 4 years?! Really? Do we all have Costanza wallets? Holy cow!

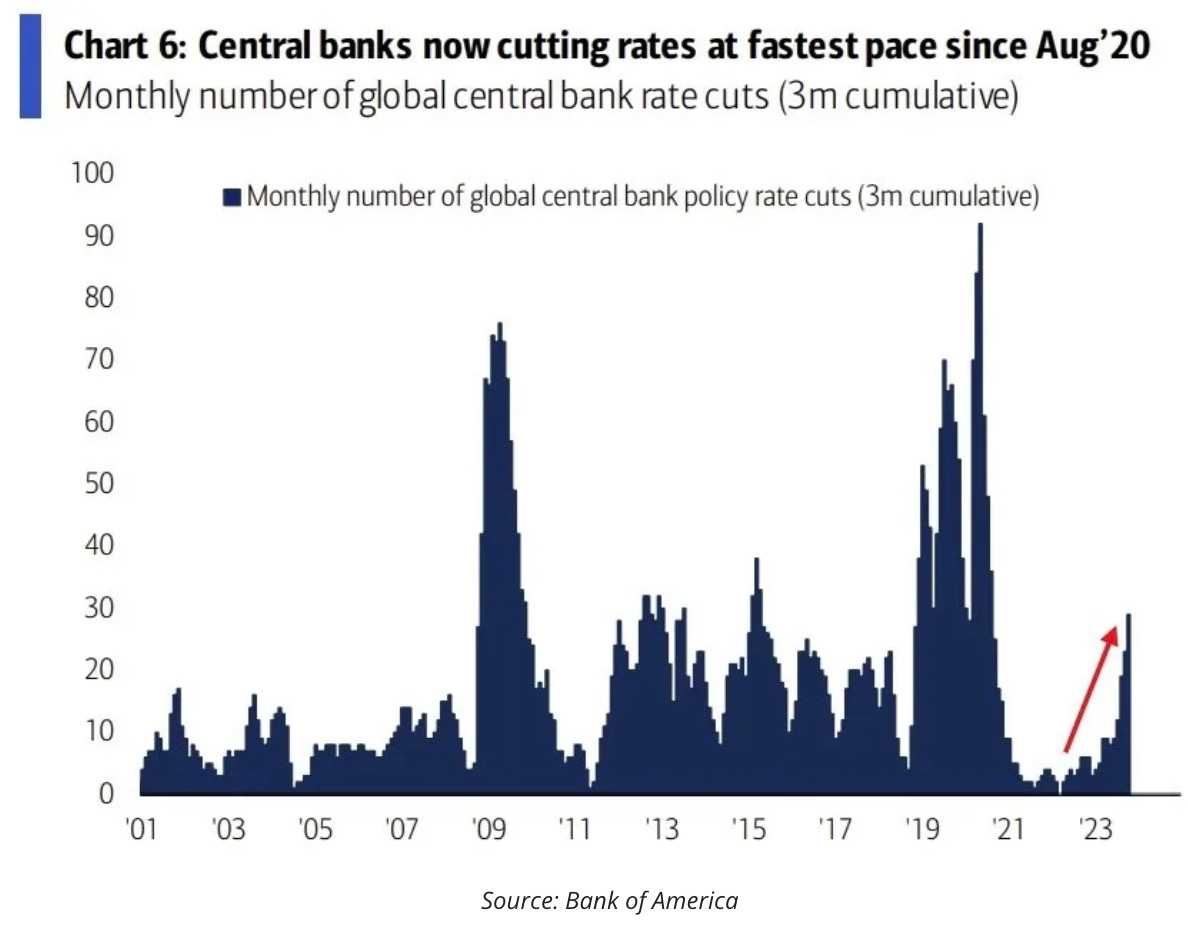

I am still of the opinion that something in the economy “breaks.” It’s more likely than not. In 6-10 months, something requires the Fed to act, which results in lower mortgage (and bond) rates. However, for those who can afford the higher mortgages for the next year, keep on alert for potentially once in a lifetime real estate deals.

Case in point, central banks around the world are now cutting interest rates at the fastest pace since 2020.

Are you looking to start investing in real estate and need to find deals that pencil out? I highly recommend this FREE tool to find a real estate agent that understands investors. Most agents suck. This is a great resource.

Great deals are out there.

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me directly!

Until next time, stay skeptical.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.