All Forum Categories

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

All Forum Posts by: Andreas Mueller

Andreas Mueller has started 49 posts and replied 177 times.

Post: STR analysis for Nashville, TN

Post: STR analysis for Nashville, TN

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Average STRs yes are "overpopulated," (ie for a given place you are getting lesss rent than get 3+ years ago).

But the stand-out STRs are soaking up all the business. My clients buying STRs who make them stand out/amazing/unique rentals in Nashville are absolutely killing it.

You can't be average and expect above-average cash flow just because it's an STR.

Real estate is professionalized. This isn't 2014 anymore.

Post: The Market Lives in the Future

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Quote from @Tenzapa Wakombe:

I love this post! I work within the Middle Tennessee market that includes Nashville so this is definitely an insightful post for investors wanting to park their money into real estate in Tennessee!

Thanks Tenzapa.

Post: How to Pick Your Real Estate Market?

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Thanks Taylor.

Post: How to Pick Your Real Estate Market?

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to my Skeptical Blog right here on BP! A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today?

Growth vs Cash Flow. Let's fight it out!

Today’s Read Time: 10 minutes

The Weekly 3 in News:

- - Housing Will ‘Unfreeze’ in Weeks and 2% Inflation Will Return. "The housing market is stuck now, but I would expect that the housing market, sometime in the next few weeks, is going to unfreeze…it is Trump’s economy in 6-12 months -Treasury Secretary Scott Bessent (Bloomberg)."

- - Active housing inventory for sale is rising on a year-over-year basis in all 50 states. Time for investors to dive in. (Resiclub).

- - Housing Hotspots for 2025, according to the National Association of Realtors. Hint: they missed a few, but a good list ().

Today’s Interest Rate: 6.74%

(👇.13% from this time last week, 30-yr mortgage)Today, we’re talkin’ how to pick your market to invest in. Tampa or Seattle? Austin or Nashville? Charleston or Denver? Growth market vs cash flow? It’s all about the market metrics.

First a quick look at the rent growth vs supply scare.

Let’s get into it.

In General…Growth is Good

Choosing the right city is critical because it directly impacts the success and profitability of your investment. Cities vary widely in terms of economic growth, population trends, job markets, and housing demand—all of which influence property values and rental income potential. A well-chosen city to invest in can offer strong appreciation, consistent cash flow, and lower risk, while a poorly chosen one might leave you with stagnant properties or high vacancies.

Now many folks just think about cash flow and rent growth when selecting a market. This is no doubt important. But, it’s not everything and the data can be misleading.

Before we get into our main topic: growth markets vs cash flow markets (its a fun one:) I want to address the current hullabaloo of rent growth/losses as it relates to supply, which has been much “doomered” in the news.

Folks I talk to often focus too much on rent growth as a key metric, but beware… it's nuanced.

Now don’t get me wrong. Renovating a slumlord’s scary 4-plex into something habitable ain’t cheap (I’ve done it many times). An investor needs to generate a return for spending the money and taking the risk to turn that place into a something a tenant would love to live in. So over time they need to be able to raise the rents to keep up with the market and cover their insurance, property tax, repair, maintenance, vacancy, landscaping etc…costs (all of which have been inflating markedly).

And yes, certain markets are growing rents faster than others, but watch out!

If you only look at rent growth and cash flow, you are likely missing the forrest for the trees.

Why?

Supply. If housing supply is growing in a city it will suppress (or even depress) rent growth. But housing supply growth is a good sign. It is a key signal of a city’s population and economic growth.

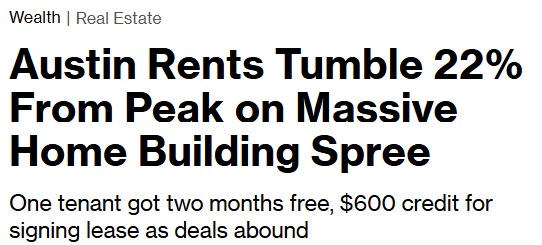

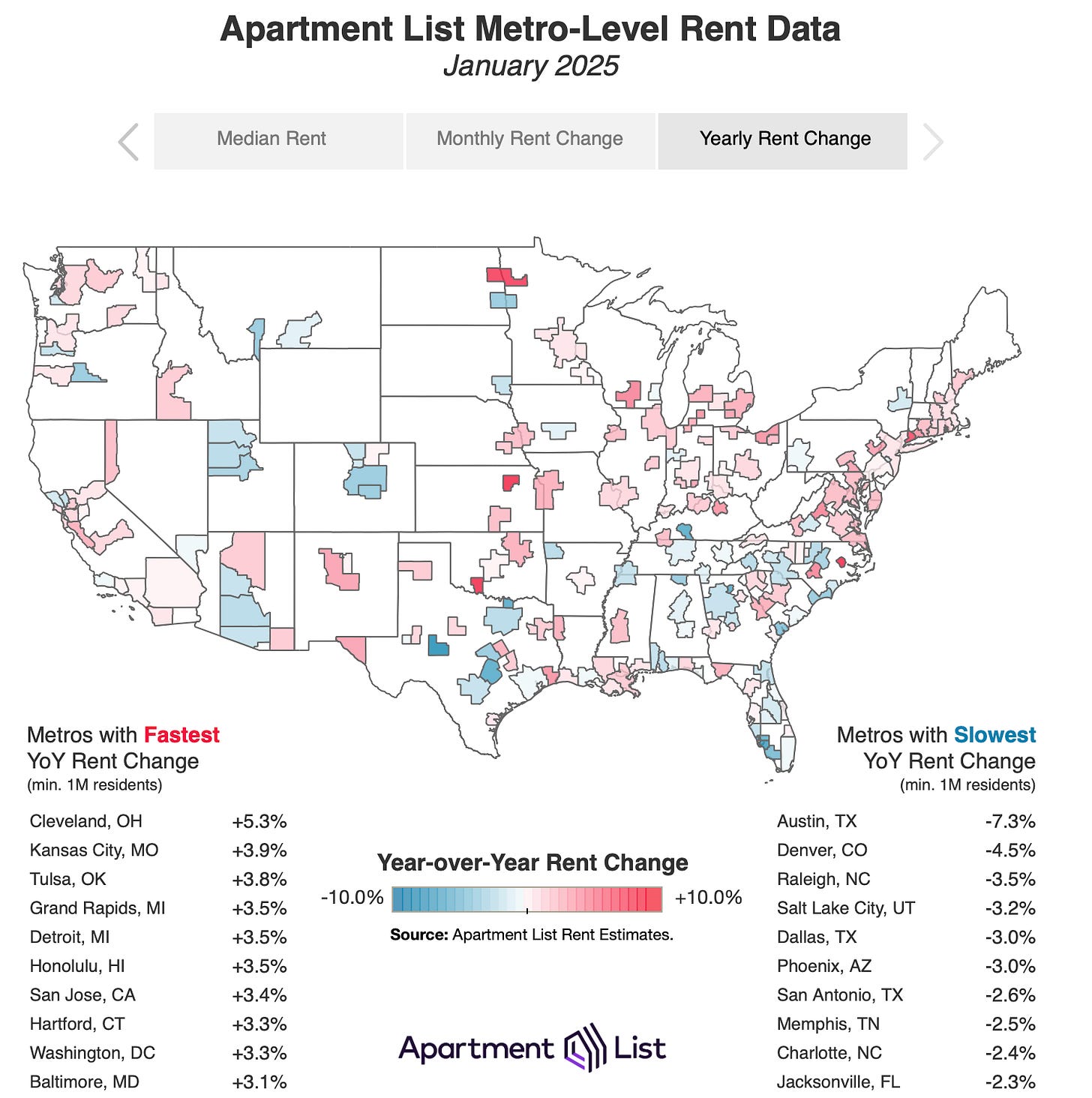

For example: Austin is a solid city to invest in. But recently it experienced significant housing supply surge, particularly apartment unit growth, causing rents to come back to earth. This is great for housing affordability, and a strong sign of a healthy market. We can’t have housing prices double and rents up in kind.

But if you looked only at the YoY rent metrics it would send you into a panic! Rents are down? AHHHHH.

First off, in general, nationwide, rent growth hit 8% YoY 2 years ago. That was not sustainable and had to come down. Some markets built more than others so they went down faster (Austin).

And rent growth is still elevated at ~4%, 33% higher than the historical average (although wage growth is still higher than rent growth, barely).

This is… dare I say…. transitory. And something very important is about to happen to housing supply.

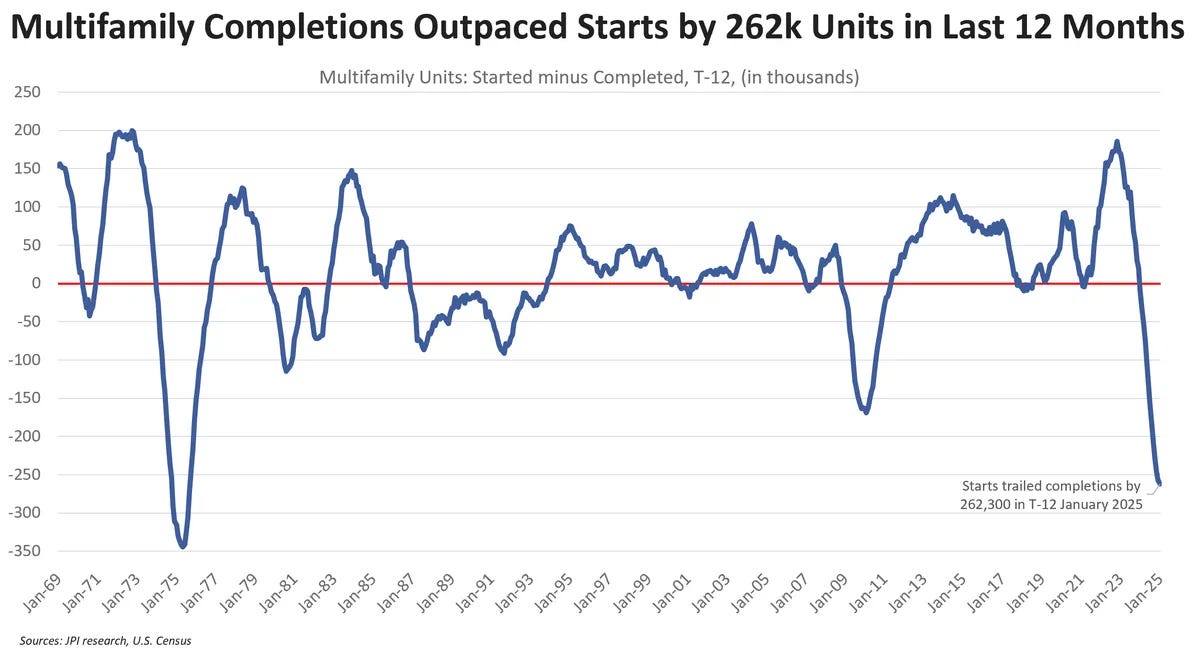

The supply of available housing units will soon fall off a cliff.

Why?

Apartment completions are at a record high today, but apartment starts are at a record low.

Why?

4 years ago we had ~0% interest rates followed buy 2+ years of wildly high interest rates.

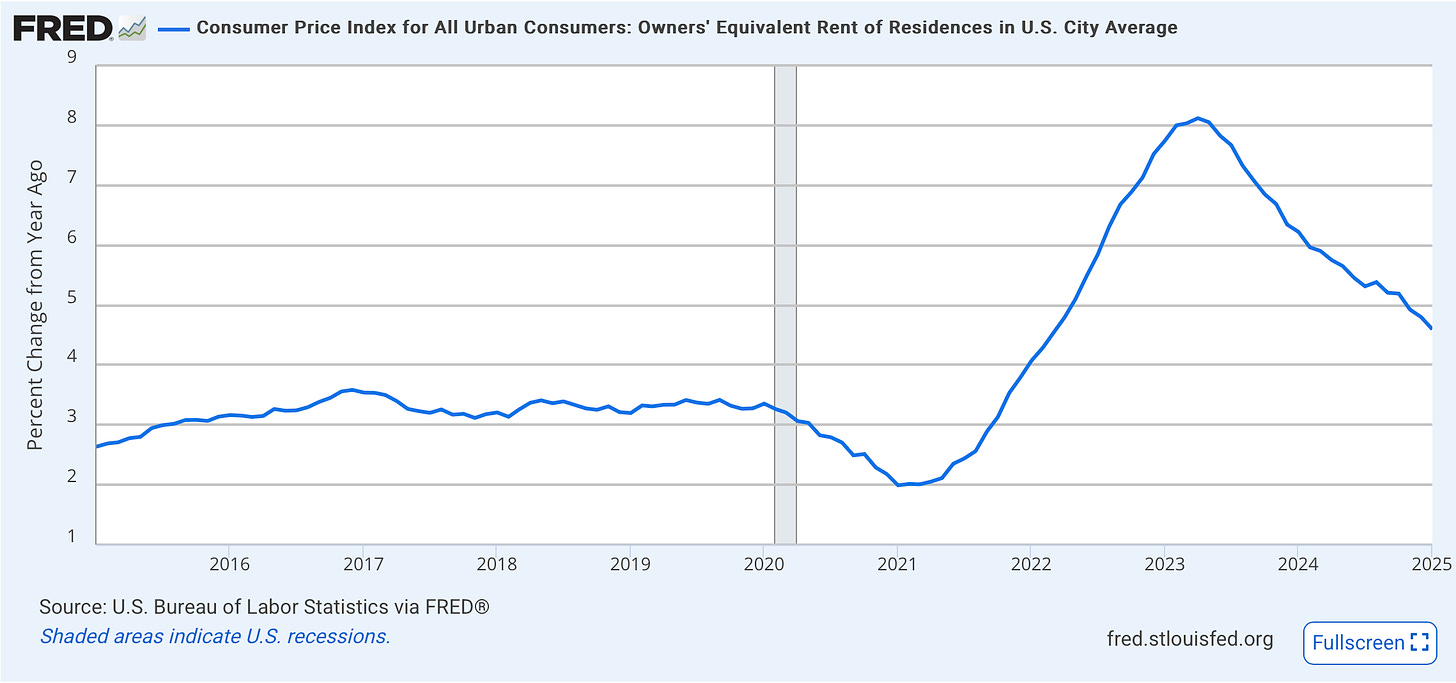

Here is a snapshot of apartment rent growth data nationwide.

And detailed chart for apartment rent growth:

And single family home rent growth.

(source: Madera residential research via housing economist Jay Parsons)

High rent growth also trends to the smaller markets. So don’t be too swayed by those shinny objects. Smaller markets normally increase rents faster than large markets. And while these ternary markets can be wonderful investments, they are also likely higher risk, with fewer employers or a small number of large anchor employers, which if they left/closed, would crash the market. *cough* Detroit *cough*

Fun fact, Detroit just grew its population for the first time since 1957…wow.

So let’s look at some key metrics for picking your target real estate market.

Housing Market Metrics

In general, and in this humble (not really) investor’s opinion, there are two general market types. Growth markets and cash flow markets.

Well actually three: Uninvestable markets. Yuck.

I do not focus on cash flow markets, which we normally find in the midwest (but not always, no offense Indiana!). What is a cash flow market? You guessed it, cash flow/cash on cash return is higher (at least at first) than you will find in a growth market, maybe even double, say 12% vs 6%. The problem with these markets is, by our definition, the natural appreciation of the property is slower and the forced equity appreciation when we renovate/develop property has lower margins/returns, on average.

But this depends on your strategy and life needs. For example: if someone is 65, it may make more sense to buy for immediate cash flow, or even sell/exchange their growth market properties and plow that capital into cash flow markets.

Disclaimer: We are talking about averages and likelihood here these are broad categories. Of course you can get a deal anywhere that has one or the other or both. Hell you can get a deal that is all three! ☝️growth, ☝️cash flow and yet completely uninvestable (aka super ☝️risk: disaster prone, crime, next to your ex-wife… you get it).

“We should always be deal dependent,” as I like to tell clients. But in general I focus on growth markets to maximize my return across the 5 ways investors make money in real estate: natural appreciation, forced appreciation, depreciation, principle pay down and cash flow. Most of the wealth your property generates over time will not be from cash flow, especially in the beginning. It will be from the appreciation categories. And it’s not even close, in my opinion. *(I wrote a whole article on the 5 ways, if you are interested in further reading DM me and Ill shoot it over to you).

The cash flow value trap.

Growth markets actually bring higher cash flow/CoC returns, it just takes time.

Wait what?

Cash flow (and principle pay down) becomes very interesting over time as the property rent appreciation compounds. Cash flow is like a house plant. It starts out small. You have to nurture it. But over time, it grows. You raise rents. Yet, your long-term debt stays fixed (thank you America). Yes, property taxes and insurance (especially in some parts of the country, watch out) will tick up, but rent increases will cover those costs. So by investing in a growth market you don’t miss out on cash flow, it just comes later. And because you are in a growth market, you will be able to raise rents faster. So over time, even cash flow will likely be higher in the end.

So how should we measure housing markets?Ok, now all that mumbo jumbo is out of the way, let’s get into it!

Again, this will somewhat depend on your preferences, risk appetite, age, family status and investment goals…BUT, I would argue there are a several foundational items the savvy real estate investor looking in a growth market should always include:

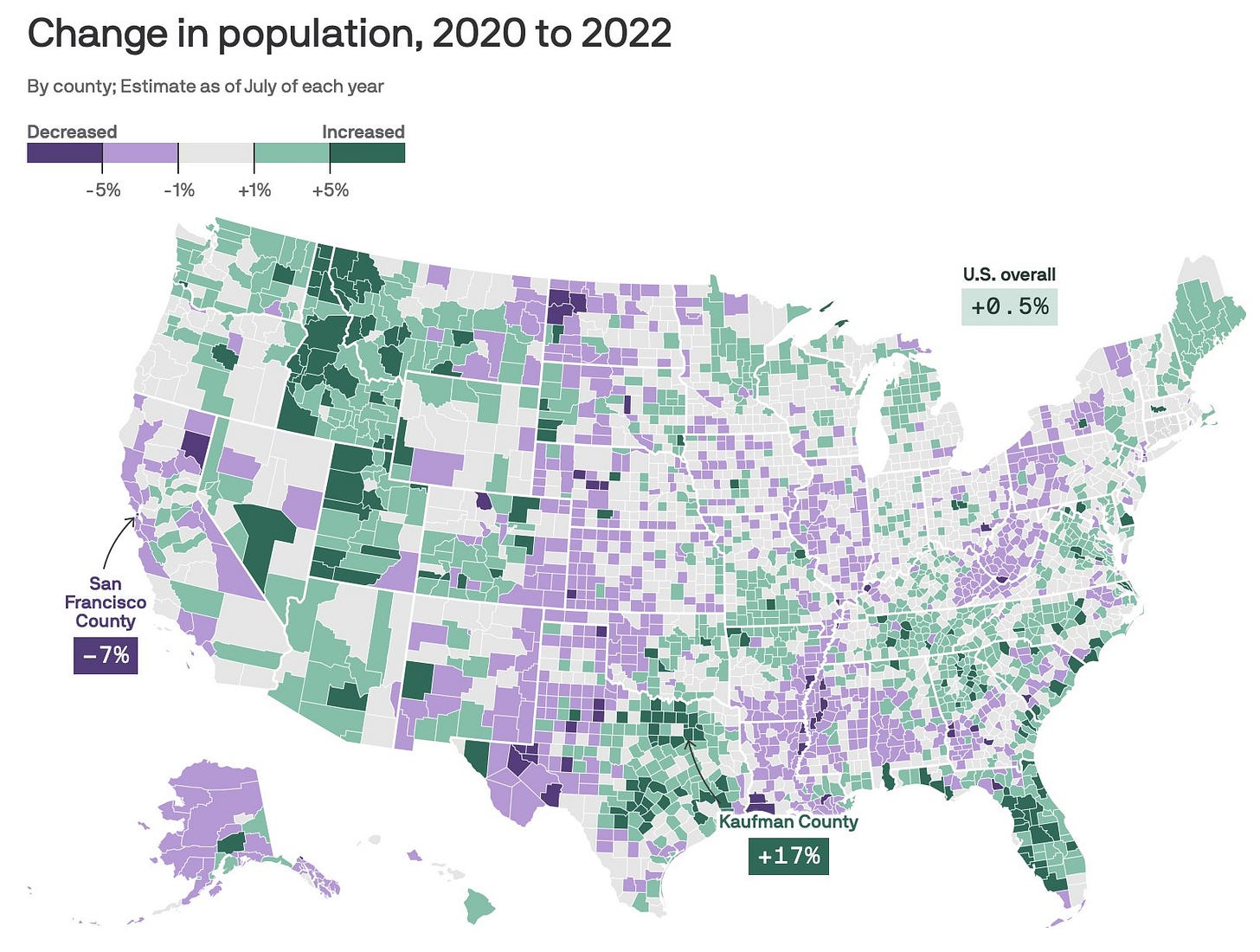

- -Population growth trending up. This, and the next metric, are the basic prerequisites for what makes a growth market and are what I focus on when I choose a market. Population growth directly impacts all the below metrics and is a primary signal for housing demand (see chart). At its center, that’s all real estate is. Buy in growth areas, were people not only want to live but are actively moving to. Investors should always track population trends and sell when you see this dip. Case in point: Two years ago I sold my last investment property in DC and redeployed to Nashville. I saw the downward trend happening. It ended up being one of the best financial moves I’ve made.

Buy Green

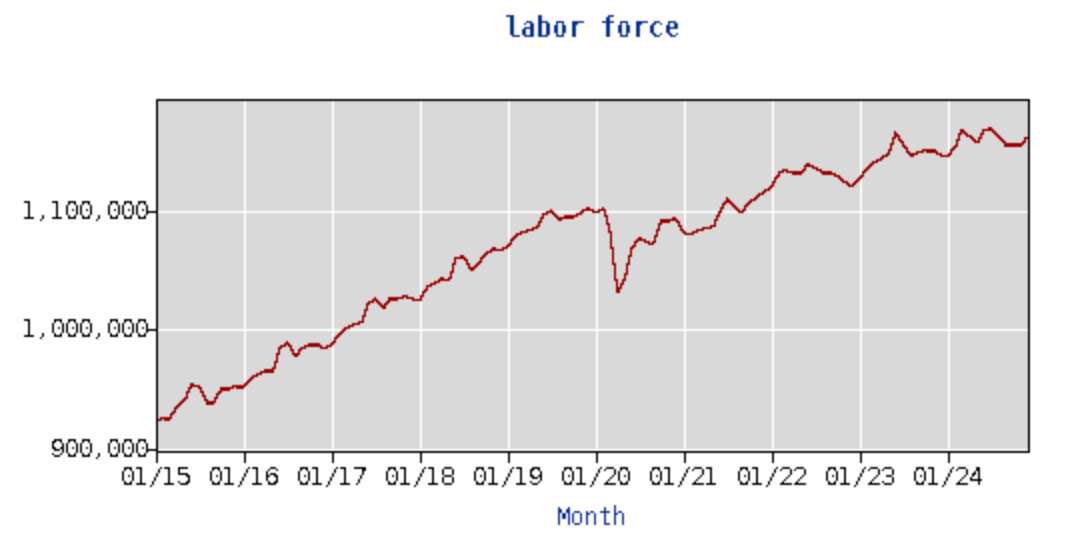

Buy Green - -Civilian labor force. I want to see this trending up and to the right. A growing number of working folks in the arena is a key filter for me when selecting a metro. If this is decreasing (seasonally adjusted/non US recession), beware! (note: labor force is different than employment. Labor force = employed + unemployed but looking). Nashville chart below.

Nashville labor force 10-yr chart

Nashville labor force 10-yr chart

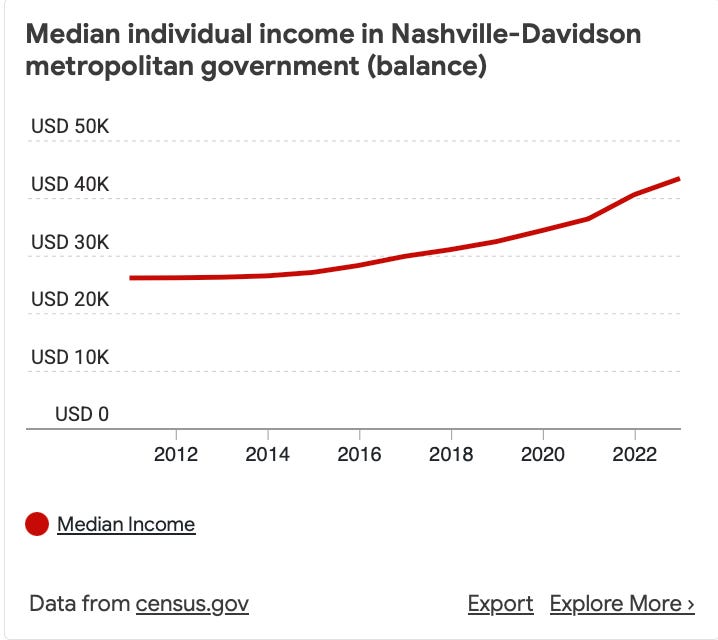

- -Individual income. A city with a growing individual income level is a big green flag for me. It signals a cycle that can supercharge investment returns.

- -Rising incomes = people have more purchasing power. That translates to higher demand for housing, whether it’s buying homes or renting apartments, which can drive up property values and rental rates. Growing income levels signal stability and opportunity. If folks are earning more, it’s likely tied to new businesses/industries moving in/expanding and is often correlated with infrastructure improvements, better schools, and overall quality-of-life upgrades—think parks, transit, and nightlife. These make the city a magnet for more residents, keeping your property in demand long-term. A stagnant or declining income level? That’s a black flag, and I’d steer clear. You want a market where the tide’s lifting all boats, not sinking the ship.

Nashville income growth

Nashville income growth

- -Economic Growth/Stability. This one is obvious and important. A city’s overall economic health ensures resilience during downturns, protecting your investment. A diverse economy and mix of businesses reduces reliance on a single industry or employer. Look for low unemployment, economic diversity, and a history of stability during recessions.

- -Home price and forced appreciation. In general, anything above 5% long-term is healthy growth, which is higher than the US Case-Shiller average. I look for this to be a long term trend of 10+ years. You can force this by renovating or developing your property. Renovated properties also naturally appreciate faster. And in growth markets you will get a higher return for adding value to the property. I like to set a baseline of a 50% return on my construction dollar when I renovate. For example: if I spend $50k on a renovation I need the property to appreciate at a minimum of $75k. I normally shoot for 100% return as my goal, or $100k appreciation, in this example. This is very hard to do at this level in a cash flow market. And I don’t know any other investment vehicle where you can get an almost guaranteed 50% return. How? Because you can calculate the return fairly accurately. You know the comparable property values to estimate your buy price, you have an estimate for construction and you know the comparable sold properties once removed in the area (After Repair Value, ARV). The difference is your forced equity appreciation (ARV- (purchase price+construction costs) = forced equity appreciation). *** Important note! Keeping construction costs down within your necessary scope of work is THE most important skill to hone as an investor/developer. This is where **** can go sideways fast.

- -Rental Yields. Again, rental yields are important. But not the most important. Cash flow is like a house plant. It starts out small. You have to nurture it. But over time, it grows. You raise rents. Yet, your long-term debt stays fixed (thank you 30-yr mortgage, only in America). I look for 3%+ as a baseline. But beware. Large supply influxes can skew the data (see above).

- -Insurance Problems? Is insurance expensive? Is actually obtaining insurance difficult? Are insurance agencies leaving the state? Insurance troubles can make a market uninvestable. Make sure you are baking your insurance costs in your analysis and weighing the risk of environmental catastrophe. This can affect everything from rentability to profitability to refinancing to long-term appreciation.

- -Infrastructure Development. Investments in transportation, schools, and public services enhance a city’s appeal, increasing property values and attracting residents. Look for planned / ongoing projects like new highways, transit systems, city development plans are a great resource.

- -Favorable regulatory environment. Is the state/city landlord friendly? This can make or break you as an investor-operator, and is another reason some markets are uninvestable. It’s like the city/state politicians think landlords are evil. I look for places that are firm but fair, like Tennessee. Additionally, favorable zoning laws and property taxes are of course important, particularly for developers, and can make larger projects much more attractive.

- -Quality of Life. Hell, dont forget this, do folks actually want to live there? Or are they there because they have to only to move to the burbs/another state in a few years *cough* Washington DC *cough*. Good schools, healthcare, low crime, recreational opportunities etc… attract residents, supporting property values.

There are more I’m missing here. What else is important to you? Drop me a note.

My Skeptical Take:

As the great hip-hop group Wu-Tang once rapped about “Cash rules everything around me, CREAM get the money, dollar dollar bill y’all…”

True that.

But beware of the cash flow value trap.

Just like stock market investors buy blue chip and small-cap stocks, so do real estate investors, who buy in major metro markets and in smaller tertiary markets. In growth markets and in cash flow markets. On may be more volatile and one more stable. One focuses on long term growth and one on shorter term higher returns. The choice is yours really, and is based on your risk appetite and investment goals. IF you decide to go into something higher risk, perhaps consider diversifying so you don’t get caught naked when the tide goes out.

Monitor your investments everyone. Especially if you have a property manager telling you everything is roses. You may still be getting that same rental check but how is the asset doing? Are there any emerging local trends that may cause concern? How can you asset manage the property better? For example: It may make sense to build a deck or landscape the backyard to keep top-quality residents and / or increase rents. In a high mortgage interest rate environment reinvesting in your current properties may make more sense than buying another property. I’m doing this now for my portfolio and our property management clients.

Do you think there is a problem in a market you are already invested in? Is growth slowing or can you get a higher return on equity in another property? Should you redeploy?

Look at the metrics above. Run the numbers, double check that every dollar you have is still a little worker bee making you the highest return on equity, even when you’re sleeping. A great book on this is “

But sometimes, success in real estate is not a hard science. It’s a soft skill, where how you behave is more important than what you know. If your numbers look good don’t panic unless there is reason to. In 2009 I had a few properties that I had to drop rents and a few I was just under construction on. But I didn’t flinch. I didn’t sell out at the bottom. I wasn’t over-leveraged. As I know from much experience, pretty much without exception, that you can always tell an ultimately good investor from a bad one by this simple test:

Equanimity. Or as the Finnish people say, sisu!

I love the Nashville market. Am I biased? Totally. But for good reason. It checks all the above boxes. And I’m putting my money where my mouth is.

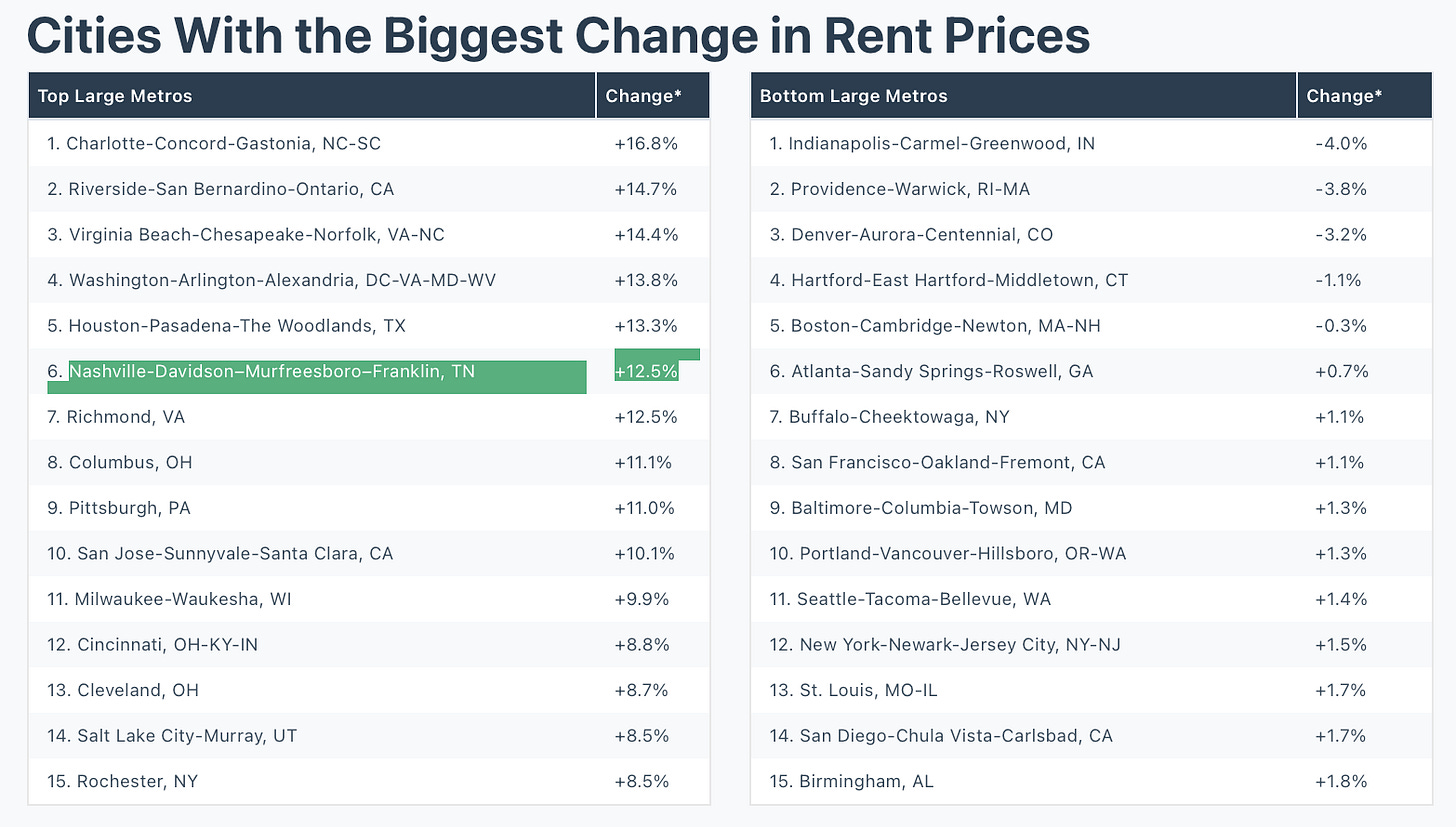

Labor force growth? check. GDP growth? Housing price growth? Check. Check. Rent growth? Check. Tourist destination? 18 million visited last year. Check. Super fun? Check.

Do I like smaller/tertiary markets?

In general, I personally stick with the larger metros that are experiencing population, labor force and economic growth. My home market of Nashville is fantastic. It has the lowest unemployment of ANY of the top 25 major cities, strong employment growth, robust GDP, and decent rents.

However, there are some notable exceptions where I may take additional risk and I feel I have asymmetrical knowledge, like some tertiary markets around where I live and have personal experience with. But there, I go higher risk barbell approach. I look for really really small cities that are in some way easily connected or a result of the outgrowth to larger anchor metro areas. For instance, I love Madison and Ashland City, two tiny towns in the Nashville metro. Ashland City’s population is only 5500, and is 30 min from Nashville.

It’s all about aligning the city’s characteristics with your investment goals—whether you’re chasing cash flow, appreciation, or a flip. Research the above market metrics. Pick wrong, and you’re fighting an uphill battle; pick right, and the market does half the work for you.

Never lose money. That’s rule number 1.

Rule number 2?

See rule number 1.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Andreas Mueller

Post: The Market Lives in the Future

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to my weekly BP Post! The Skeptical Investor, which I hope we all are :)

A frank, hopefully insightful, article from one investor to another.

Today, we’re talkin’ markets, and where they go from here. Is inflation at risk of reigniting or is the long-term downward trend still intact? Will there be a catalyst for housing activity like lower interest rates? Or will rates continue to stay high?

I found some interesting countertrends this week.

Let’s get into it.

The Weekly 3 in News:

The Weekly 3 in News:

- - 73.3% of U.S. mortgage borrowers have an interest rate under 5.0% (Lambert).

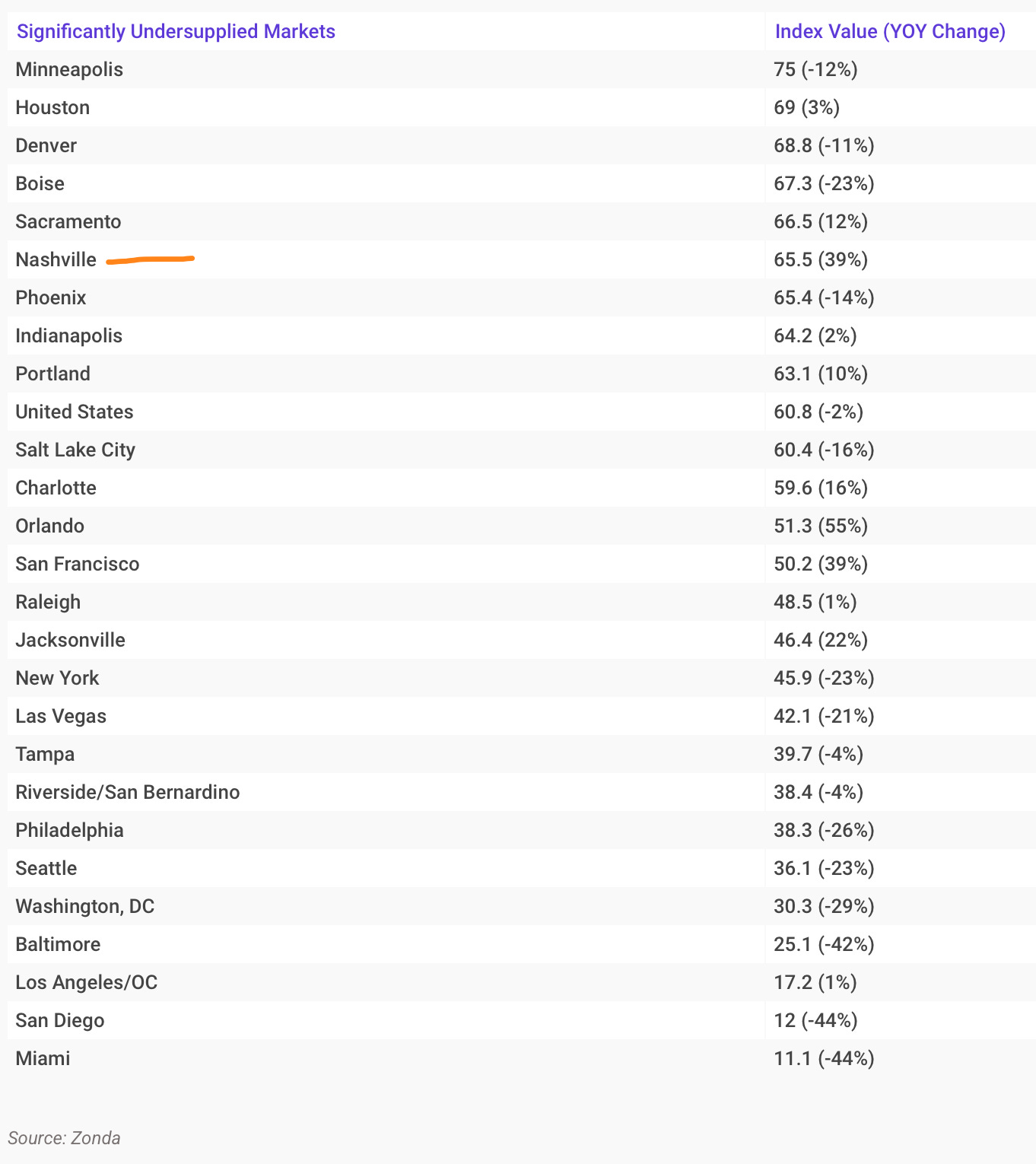

- - Most housing markets are significantly undersupplied for new lots to develop, including Nashville. We need more housing ()!

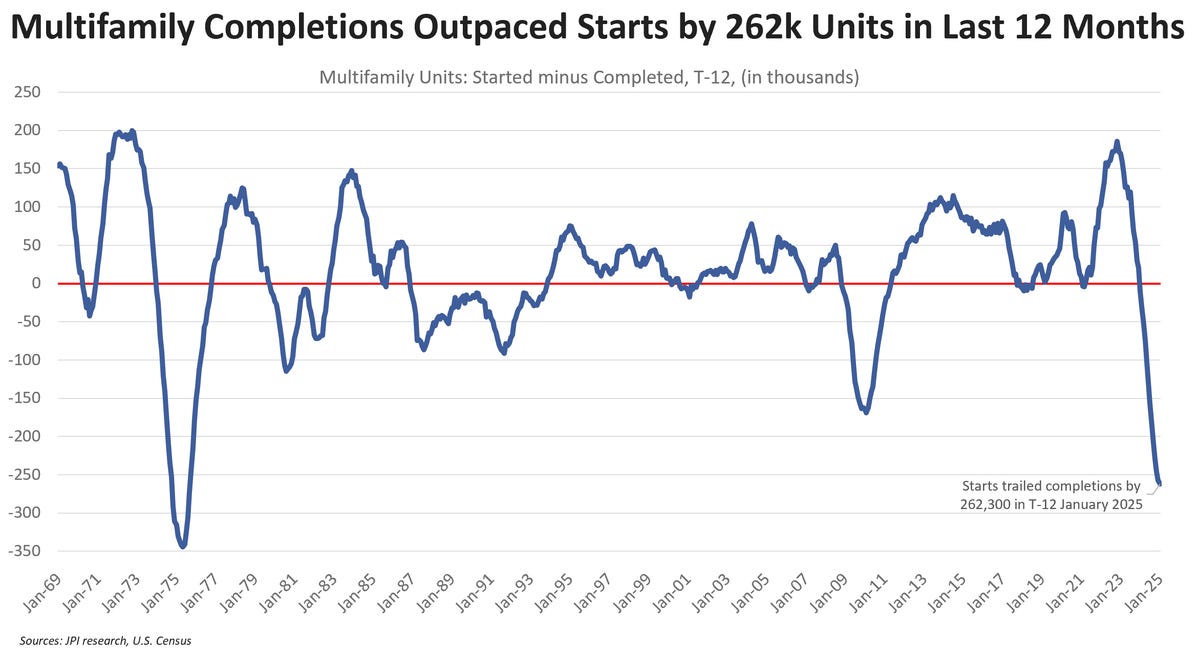

- - New apartment construction continues to plummet. Apartment development starts are trailing completions by the most since the 1970s. We are entering into a severely undersupplied housing moment as interest rates weigh on development (Parsons).

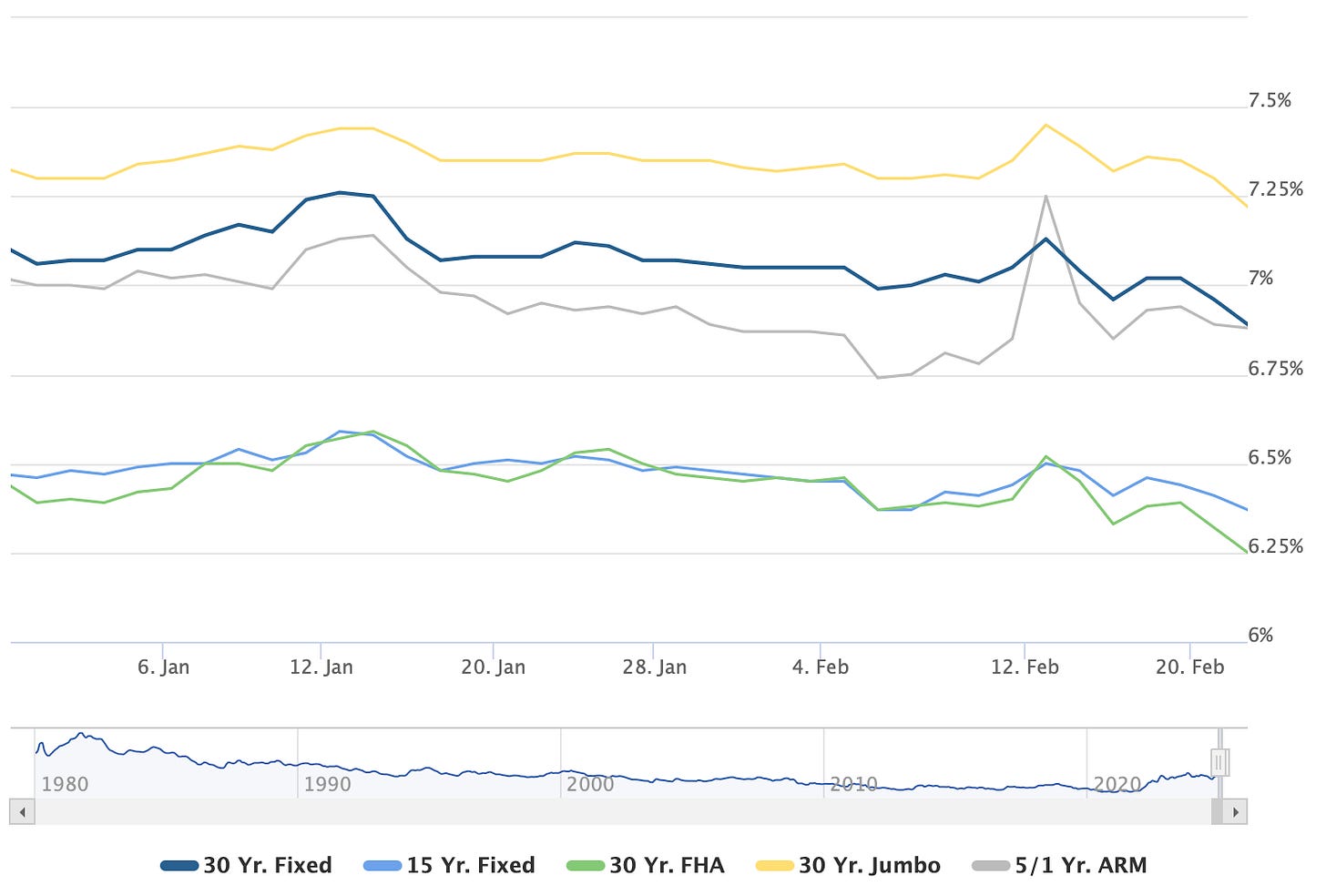

Today’s Interest Rate: 6.87%

(👇.09% from this time last week, 30-yr mortgage)Inflation has been trending higher

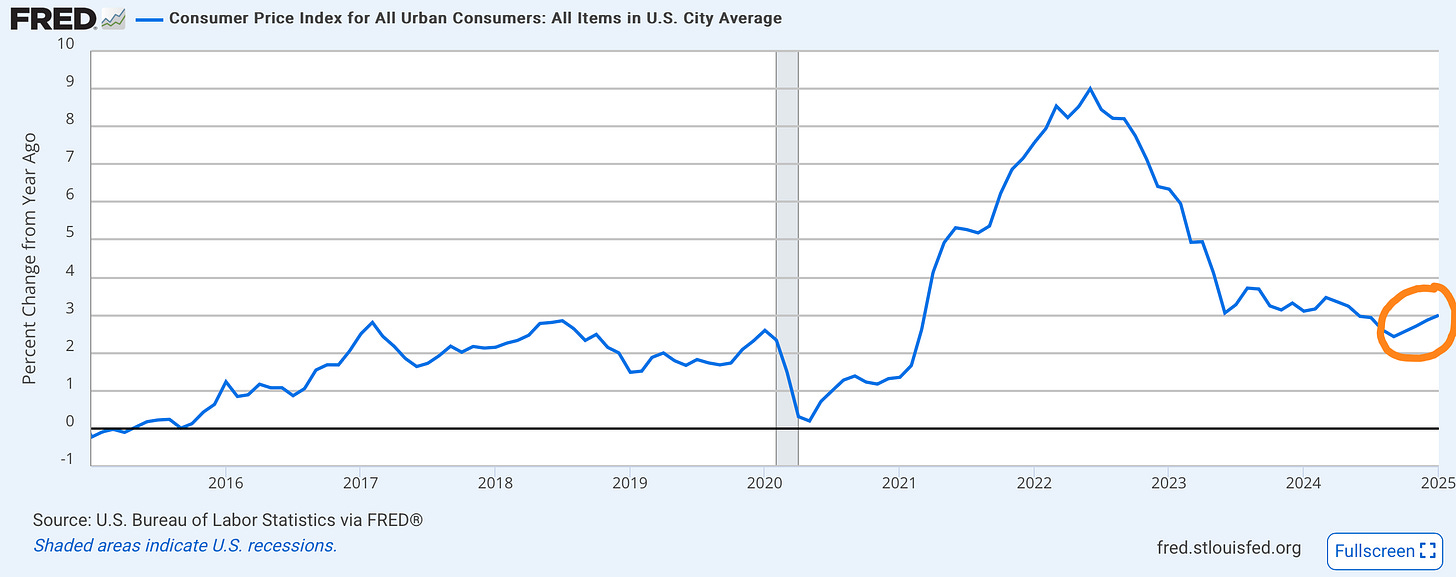

Inflation has come down significantly since its peak. A few years ago prices were going up 9%, and now we have settled ~ 3% price growth. But this ain’t good enough, and is still 50% higher than the Fed’s 2% target.

And to his credit, Federal Reserve Chair Jerome Powell seems in no rush to cut rates with inflation above target level. During his congressional testimony last week, Powell said, “If the economy remains strong, and inflation does not continue to move sustainably toward 2 percent, we can maintain policy restraint for longer.” And that “the Fed would not lower its policy rate until there is “greater confidence that inflation is moving sustainably down toward 2 percent.” This is a welcome, cautious approach prioritizing inflation data over premature rate reductions.

However…. it appears that inflation may instead be reversing course.

It’s been four straight months of price increases.

- October - 2.57%

- November - 2.71%

- December - 2.87%

- January - 3%

Four, a trend does make.

And oddly, Fed Chair Powell seemingly brushed this off in his testimony, saying “A couple of months doesn’t make a trend.” This is not accurate. I couldn’t believe it.

This is a big deal, and it seems nobody is talking about it. A not so fun fact, we have not had more than 2 consecutive months of inflation growth since the end of 2021.

Until now.

I’m getting PTSD from when the Fed and former Treasury Secretary Yellen insisted for months and months that inflation was not a worry, it was “transitory..”

How did that play out y’all?

So count me extremely skeptical. Inflation has a real risk to the upside here.

Where do interest rates go from here?

Now, here is where it starts to get interesting.

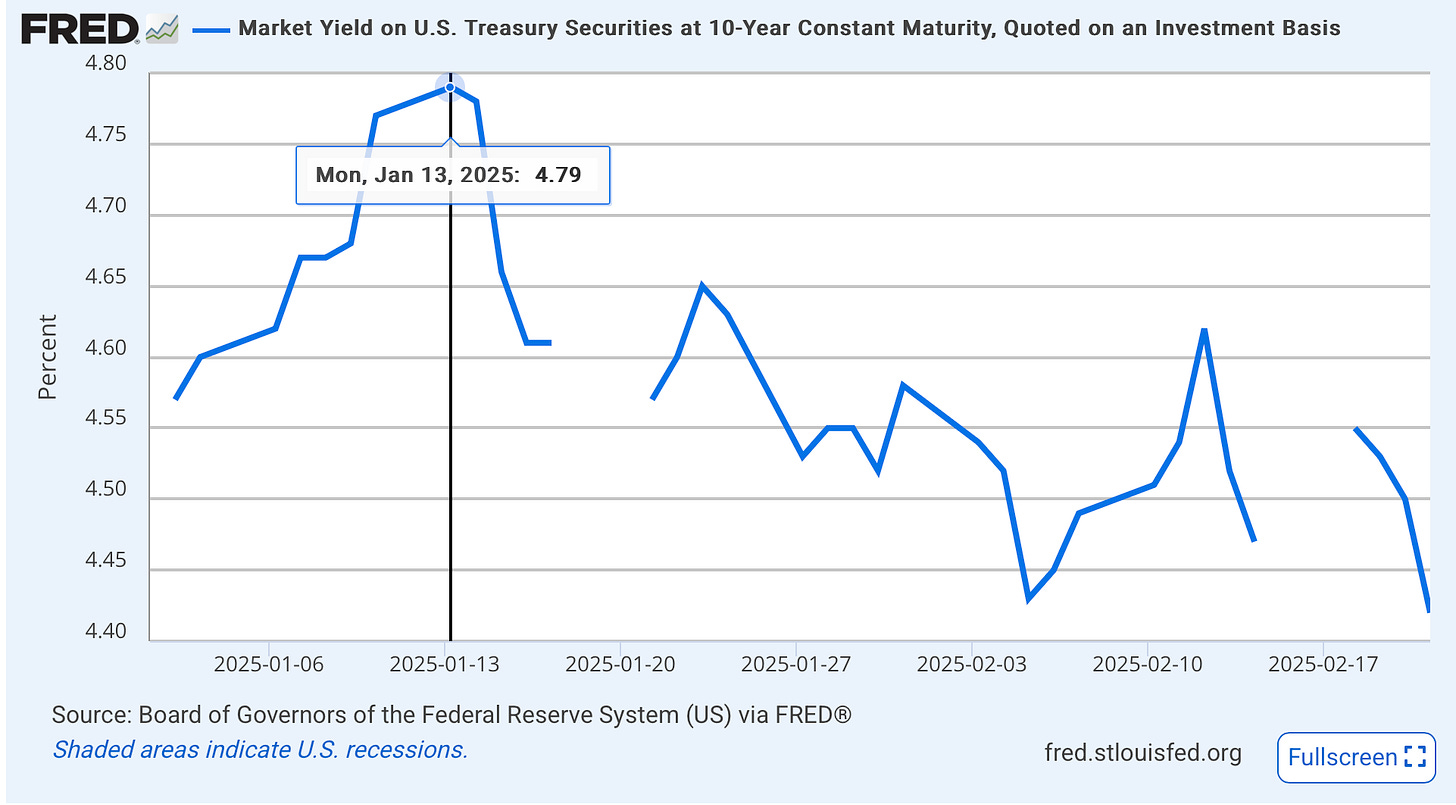

After having a bit of a tantrum to start the year, where the 10-yr treasury spiked to ~4.8%…

…bond vigilantes have been feeling better about inflation’s prospects these last few weeks (the breaks above are holidays).

This has translated into (slightly) lower mortgage rates.

Since peaking on Jan 13th (matching the 10-yr Treasury peak) at 7.26% the 30-yr mortgage rate has been down each week since (with some volatility last week).

Very interesting.

And, ironically, this could continue.

In an interview this past Friday, Treasury Secretary Bessent told Bloomberg that the Fed may stop selling Treasuries off their balance sheet, which the Fed has been doing while lowering interest rates. These two actions were working against each other, so if they do stop Treasures rolling off, this will make it easier (with lower supply) for the Treasury to issue/sell 10yr bonds and potentially lead to lower long-duration bond rates, and thus mortgage rates.

The Fed doesn’t control mortgage rates, but they do own mortgage bondsIt is often said, including by yours truly, that the Fed doesn’t control the long end of the yield curve. Ie, when the Fed cuts it’s short-term Fed Funds Rate that does not have a direct affect on 10-yr Treasury rates, or 30-yr mortgage rates.

True. But…

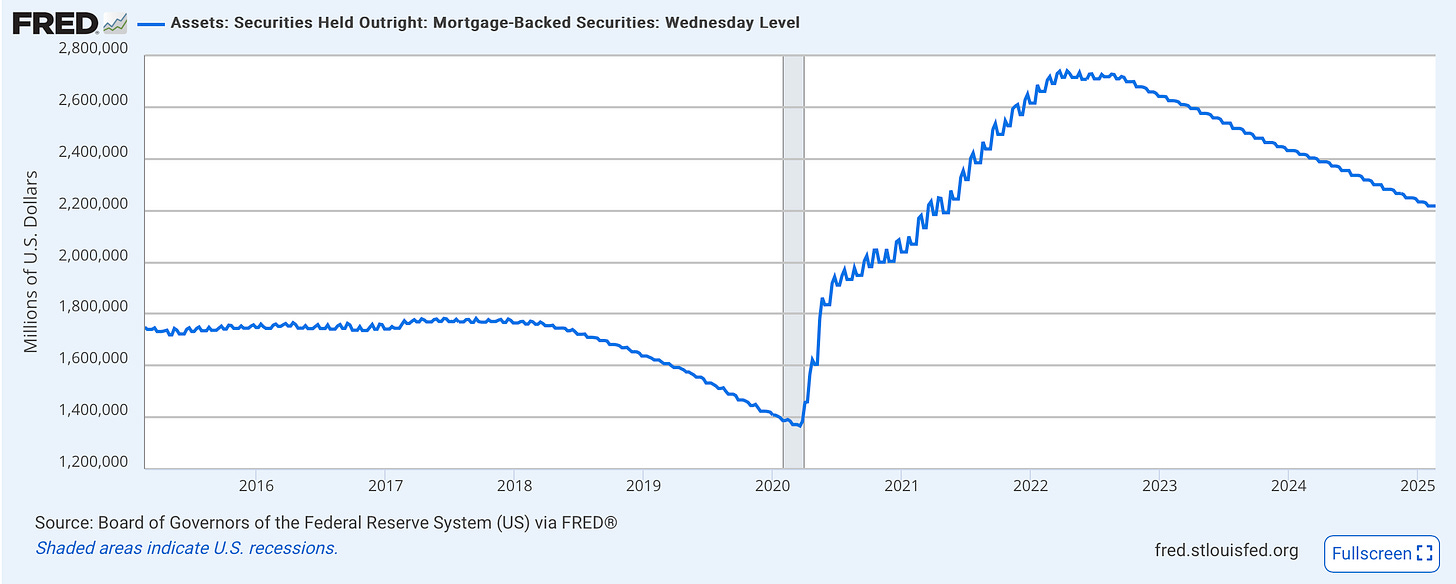

The Fed does buy mortgage bonds (mortgage-backed securities). Currently $2.2 trillion worth, in fact. This is called Quantitative Easing (QE) and it very much affects interest rates. Treasury bonds are long-term debt securities issued by the government to finance its spending. When the central bank engages in QE and buys treasury bonds, it increases the demand for these bonds. Higher demand for treasury bonds leads to an increase in their prices. Bond prices and yields are inversely related: when bond prices rise, yields fall. Therefore, QE lowers treasury bond yields. And since the 30-yr mortgage follows the 10-yr Treasury rate (put simply: they are competing investment tools) the Fed very much can affect mortgage rates.

This QE mortgage rate manipulation became a policy tool in 2009, following the Great Financial Crisis. And it will remain so, until the Fed mortgage bond portfolio drops to zero. So when the Fed buys mortgage bonds they can manipulate mortgage rates down by introducing additional demand. This contributes to a higher-than-usual premium in the spread between the 10-year Treasury and 30-yr mortgage rates i.e. higher mortgage rates.

The complication today is that since buying a hell of a lot of these bonds from 2020-2022 they have been steadily selling them back into the market or allowing them to roll off/expire.

This does put upward pressure on mortgage rates.

The Market Lives in the FutureBeyond directly lowering treasury yields, QE increases the overall money supply in the economy. This influx of money can lead to lower interest rates across various financial markets, including mortgage rates. The signaling effect of QE also plays a role. When the central bank engages in QE, it signals its commitment to keeping interest rates low for an extended period. This influences market expectations and reinforces the downward pressure on mortgage rates.

Labor market softening could further help with ratesIn his testimony, Powell also remarked that the labor market has "cooled from its formerly overheated state" but remains "solid." He continued, saying “[the Fed can] "ease policy if the labor market unexpectedly weakens or inflation falls more quickly than expected." This shows that the Fed is prepared to lower interest rates if the job market suddenly deteriorates or if inflation drops faster than anticipated.

Welcome reassurance to the market.

Additionally, Powell noted that the Fed is in the midst of a framework review, evaluating its monetary policy and communication strategies. This should wrap up by late summer 2025 and could provide a pivot point for Fed policy.

My Skeptical Take:

The 4-month inflationary trend should be extremely concerning. I am skeptical that the Fed will be able to cut rates by the conclusion of its framework review this late summer.

Last month I made a call on mortgage rates for 2025.

And I’m sticking by it.

So, if the Fed won’t do it, how could mortgage rates drop?

I still think we can get to sub-6% this year on the 30-yr mortgage. But it won’t be because of the Fed cutting rates. It will be because these 3 things happen:

- - The labor market continues to normalize (aka cool), wage inflation slows but not alarmingly, and the bond market can stop fighting the Fed. Once bond market vigilantes believe that future inflation is under control, interest rates - and thus mortgage rates - will tick down (Long-term bonds will be more valuable and investors will buy them). Mortgage rates go down with Treasuries.

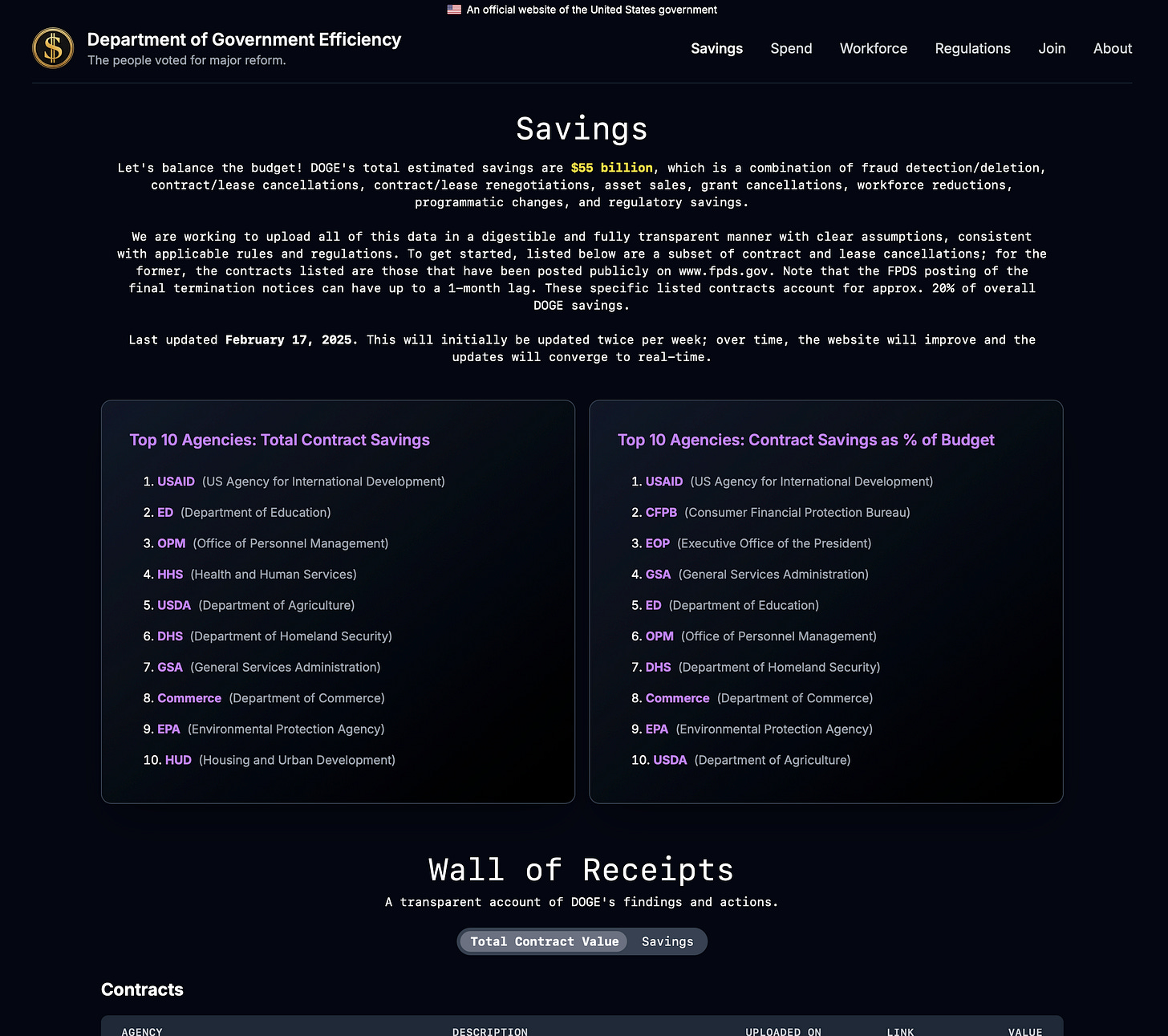

- - Government spending is being slashed (hopefully). If it becomes clear that the DOGE White House effort is working, long-term Treasury bill yields will fall even faster. Hell, DOGE says they have saved $55 billion in taxpayer dollars so far, according to the Administration’s new “transparency” website. This may be “inflated” (pardon the pun) and the effort has received criticism BUT if they can achieve even a fraction of the $2 trillion they intend to cut it will be enough of a signal.

Remember, it’s been just 30 days since they started.

- - The Fed can use its balance sheet to affect mortgage rates. The Fed doesn’t need to start buying mortgage bonds again (ie quantitative easing) but it can stop selling/rolling mortgage bonds off its balance sheet. It has $2.2 trillion of these babies and continuing to release them back into the market is likely putting upward pressure on rates. And if the housing market stays in correction territory (by # of transactions) then they may even consider adding to their treasure trove of Treasuries (say that 5 times fast).

So, will we get to 5.xx% mortgage rates this year?

Yes we can.

All the market needs is confidence that inflation and federal spending are starting to tick down, with a cool, yet steady, labor market.

Remember, the market lives in the future.

I’m not assuming anything of course. And I recommend you do the same.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Andreas Mueller

Post: Off Market Hermitage Flip in a GREAT Neighborhood!

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

DM me for email

Post: Off Market Hermitage Flip in a GREAT Neighborhood!

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

add me to your email list. These don't work for my clients BUT i have 12 investors looking. anything small multi or that has a 2nd living space

Post: Fannie and Freddie: Is it time to end Government Control?

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Post: Fannie and Freddie: Is it time to end Government Control?

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Welcome to my weekly BP Post!

Today, we’re talkin’ Fannie Mae and Freddie Mac, the mortgage giants still under government conservatorship 17 years later. In the coming months, they may be released from their government overlords. There are a lot of thorny issues associated with this transition back to independence.

Let’s get into it.

The Weekly 3 in News:- - Redfin is laying off 450 employees from its rental division, this, after agreeing to a $100 million deal making Zillow the exclusive provider of multifamily rental listings on Redfin (NewsWire).

- - Women are buying more homes. In 1985, 75% of first-time buyers were married; that share is just 50% today. Single women first-time buyers grew from 11% in 1985 to 24% in 2024. In the most recent data, single men rose from 9% in 1985 to 11% in 2024 (NAR).

- - Nashville hotel industry is expanding rapidly, 2nd only to New York City in its growth. The Music City is set to add 2,849 hotel rooms (current total is 58,959), according todata. Over the last decade, Nashville has grown its hotel room supply by 52%, opening 20,000 rooms. Of the 2,849 rooms set to open this year, most fall in the upper-scale classes. Nashville has been growing luxury offerings with the openings of hotels like the Four Seasons Hotel Nashville, SoHo House Nashville and 1 Hotel Nashville and restaurants like Craig’s, Sushi Bar, Joe Muer Seafood, Harper’s and more (CoStar).

Today’s Interest Rate: 7.02%

(👇.03% from this time last week, 30-yr mortgage)Fannie and Freddie: What are they?

First, a super quick refresher.

Fannie Mae (the Federal National Mortgage Association) and Freddie Mac (the Federal Home Loan Mortgage Corporation) are two government-sponsored enterprises (GSEs), established in 1938 and 1970, respectively. GSEs are entities established but not operated or owned by the Federal government to (oftentimes) enhance credit availability, in sectors that have some sort of public good connection like agriculture or housing. GSEs, once established, operate as private corporations, with shareholders, and are sometimes even listed on stock exchanges. Fannie Mac is a publically traded company, ticker FNMA (more later).

These GSE’s were created to to promote homeownership by providing liquidity to the secondary mortgage market.

These are GIANT housing players, and this is hard to understate. For example: Fannie Mae backs 25% of all single-family mortgage loans, including 1.4 million in 2024 alone and 21% of outstanding multifamily apartment mortgage debt (Fannie).

What do Fannie and Freddie even do?

Mortgage rates tend to fall as the supply of funds in the mortgage market increases, making homeownership more affordable. So, put simply, Fannie and Freddie facilitate financing/liquidity to this market, focusing predominately on single-family mortgages and multifamily construction. For it’s part, Fannie Mae historically has focused more on purchasing mortgages from larger financial institutions, while Freddie Mac was originally designed to support smaller/regional/thrift institutions. However, this distinction has completely blurred over time. Even their mortgage products and target audiences have morphed to be both strategically and technically similar

Here you can compare Fannie and Freddie. But I’ll save you the click. If you drew a vendiagram, they would be largely overlapping.

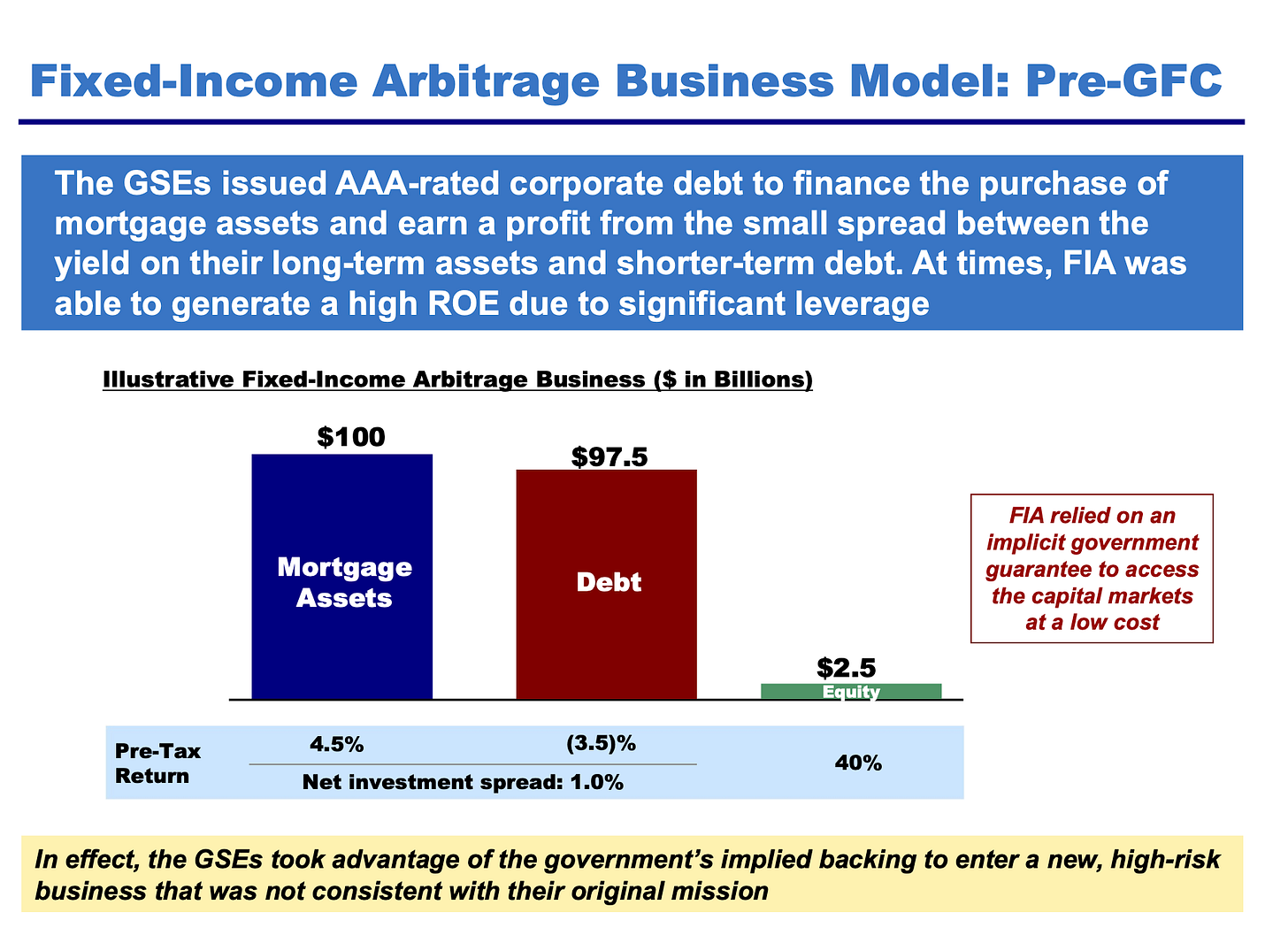

What is Conservatorship?In 2008, the Great Financial Crisis (GFC) smashed these two but good. And because they were so intertwined in our ecoomy, they needed a bailout. However, their failure was much their doing. They were totally overlevered, undercapatilaized, and were taking risks like a large hedge fund.

Taxpayers to the rescue.

So Congress passed, and President Bush signed (wow, kinda forgot about Bush until now), the Housing and Economic Recovery Act of 2008 (HERA), which established a new agency (we love creating new federal agencies in this country): the Federal Housing Finance Agency, giving it authority to place regulated entities into conservatorship or receivership. This is what they did with Fannie and Freddie.

Side Note: I was working as a staffer in Congress at the time, what a wild year. We thought the sky and the heavens were falling. Truth is we didn’t yet know how bad the crisis was and how finaical markets had been allowed to run amok. It was chaotic.

Conservatorship allowed these entities to conserve their assets in order to preserve their solvency and ultimately stabilize the housing finance market. FNMA took total control over these entities. As stated on their gov website: “FHFA is responsible for the overall management of Fannie Mae and Freddie Mac and has informed the Enterprises which decision-making functions should be performed by the Enterprises' boards of directors and/or management teams. The boards and management teams must consult with FHFA and obtain conservator approval as FHFA directs. Overall, the conservator has ultimate authority over all operations of the Enterprises.”

In exchange, the US Treasury injected up to $200 billion each in capital and owns stock (technically warrants and senior preferred) in FHFA, upwards of 80% of it. And, since 2012, after FHFA was back on its feet, the Treasury has been paid an ongoing dividend on the earnings of FHFA. ie the government / taxpayers are making money on Fannie and Freddie, for bailing them out (more on this later).

Afraid of secondary effects, both Fannie and Freddie remain in conservatorship today.

What specifically did they do wrong?

According to Warren Buffet, Fannie and Freddie really failed because of high-leverage risk-taking in the fixed income arbitrage space, saying:

“The portfolios are what really got them into the trouble…the managements of Freddie and Fannie tried to juice up the earnings, basically, because the insurance guaranteed that they were given that mortgage. I always thought that made a lot of sense. But the portfolio operations enabled both of those entities to use, in effect, government-related borrowing costs and sort of unlimited credit, to set up the biggest hedge fund in the world...So the portfolios are poison. They aren’t really needed to carry out the function of Freddie and Fannie.” - Warren Buffett, 9/8/2008

Fannie and Freddie no longer do fixed-income arbitrage, as it served no credible purpose for the mortgage market. IMO: It looks like regulators were asleep at the wheel here, just like they were concering the big banks and derivative providers like AIG.

Whew, ok background done…. (yes some of this is oversimplified, hold the comments keyboard warriors).

Is it time to end the government conservatorship?

Just the other day, incoming Treasury Secretary Scott Bessant was asked about ending conservatorship, saying “[concerning a Fannie and Freddie release,] …anything that is done around a safe and sound release is going to hinge on the effect of long-term mortgage rates.” In other words, the government is concerned about an immediate affect on mortgage rates, because rates are so high today, and will be cautious in their approach.

What could happen to financial markets?So what’s the big deal? They have been operating effectively since ~2012, so why take the government's thumb off the scale?

Could a return to independence help lower mortgage rates, or have other positive effects?

Yes! There are some potential material benefits to GSE independence. But…

If you haven’t noticed, we have been in a bit of a precarious situation these last few years. Interest/mortgage rates are at historical highs, crashing new home construction and existing home sales to the lowest level in 30 years. And while the government wants to be rid of responsibility for Fannie and Freddie, they have to be careful. Ending conservatorship would have significant implications for the mortgage finance system, broader financial markets, and economy writ large.

Key conservatorship issues to considerAny plan to exit Fannie and Freddie's conservatorship should promote market liquidity, and thus, access to mortgage credit. Treasury, HUD, and market participants/investors will have to carefully navigate many thorny issues, including:

- - Increased Market Competition: Fannie and Freddie will compete more aggressively for mortgage business, which will lead to innovation but also potentially higher risk-taking. Adequate capital requirements and clear guardrails should be implemented to mitigate risk. Much of this has already been done, as a result of Dodd-Frank and other landmark laws following the GFC.

- - Portfolio Caps: Fannie and Freddie’s tight lending portfolio caps will likely be removed. But, if overly onerous capital requirements and regulatory restrictions are put into place, this would likely limit efficiency gains from independence, which is the whole point. They should also be subject to federal stress testing.

- - Mortgage Rates and Government Support: If Fannie Mae and Freddie Mac were to operate without explicit government support, mortgage rates might increase due to higher perceived risk. Therefore, implicit government backing, as they did in 2008, may need to be part of their return to independence, albeit it with limitations to prevent moral hazard risk. We also should be prepared for temporary bond market volatility in the short term, as the GSEs reenter the market. This is natural. To minimize this government must be fully transparent, and not surprise the market.

- - Liquidity: These entities are a colossal source of liquidity for the mortgage market. Their exit from conservatorship must be clearly telegraphed to avoid liquidity issues. This is extremely important.

- - What’s the difference between me and you? Fannie and Freddie have molded themselves into a uni-blob. Returning to independence should reestablish differentiation and creativity between Fannie and Freddie. For example: Treasury may want to incentivize Freddie to refocus on regional, small lending products to reinvigorate smaller homebuilders/developers. New home and existing home renovation/construction in the pipeline has fallen off a cliff, especially in the current high interest environment. An independent Fannie and Freddie has the power to incentivize/create lending products necessary to boost the future housing stock.

- Taxpayer benefit: Exiting conservatorship will be a significant revenue event for taxpayers, providing the US Treasury with more than $300 billion, for their ownership interest.

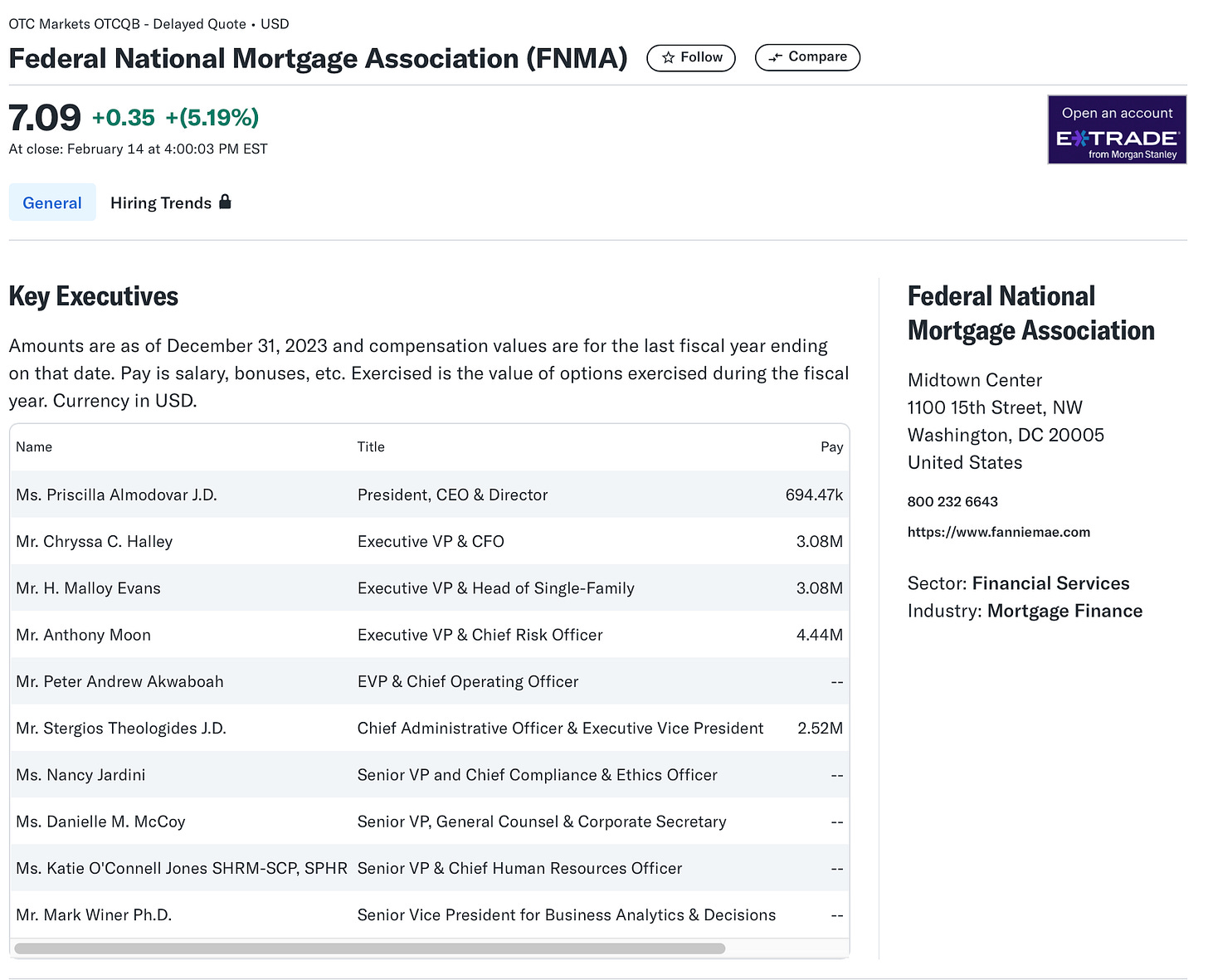

FNMA is still publicly-traded

Remember, the FNMA stock still trades today. And on the news of potentially ending conservatorship, it has gone gangbusters. Up 433% since the election. Chart on:

Think that’s a bid number? Well hold my beer.

What the hell is up with the salaries over there?! They are still in government conservatorship but folks are making wild money. For example:

- - Executive VP, Mr. Anthony Moon is making $4.4 million / year.

- - President, David Benson $4.5 million

- - Executive VP, Chryssa Halley, $3 million

I should have gotten into government mortgage buying….

But I digress….

My Skeptical Take:

The conservatorship of Fannie Mae and Freddie Mac represents a unique intervention. The federal government took control to prevent collapse, manage through crisis (and their mismanagement), and potentially reform these institutions for improved stability in the U.S. housing market.

Government “owned” Fannie and Freddie have successfully provided liquidity to the US mortgage and multifamily construction market for more than 15 years. So as we transition out of conservatorship we obviously need careful planning to mitigate disruptions.

That being said, we have to end it, private markets can do a better job. IMO. Ending conservatorship presents an opportunity to improve market liquidity, access to mortgage credit and, perhaps most importantly, boost home and apartment construction.

Investor Bill Ackman has a fantastic in-depth presentation on why we should end the conservatorship, which is a must-watch. But if you don’t have time, in summary, he argues that Fannie and Freddie took excessive risk to juice profits, which had nothing to do with supporting the mortgage market. This was the single reason for their failure and could have been prevented, even during the GFC. Unfortunately, many financial institution were doing the same, and regulators were asleep at the wheel.

for ending conservatorship are:

- - Maintain the availability / affordability of the 30-year, fixed-rate,

prepayable mortgage.

- - Protect taxpayers from bearing the cost of a housing downturn.

- - Minimize government involvement in the housing finance system.

- - Maximize probability of successful private capital raise.

- - Maximize taxpayers’ profits on Treasury’s investment in the GSEs.

Ackman’s key steps to ending conservatorship are:

- - Set appropriate capital requirements.

- - Limit government-granted benefits.

- - Develop market-based compensation and governance policies.

- - Clarify the nature of ongoing government backstop (implicit and/or explicit).

We have time, likely 12-24 months, IMO. Ending conservatorship may be a lower priority endeavor for the Administration, but they want to do it. As I wrote about last week, lowering mortgage rates via the bond market are their priority. That and continuing the current tax cuts. I think they wait until rates are lower to end conservatorship so they aren’t potentially blamed just in case ending it has a temporary affect on long-term interest rates.

BUT, the time to START acting is likely now. Which may bring some market volatility, and us Skeptical Investors should be aware.

Why?

- - Unemployment remains near record lows.

- - GDP growth trending at approximately 3%.

- - National home prices have surpassed the 2006 peak.

- - Major stock market indices at or near all-time highs.

- - Housing construction, supply and existing home sales are all at recessionary levels.

In other words, things are good. The economy is functioning well. This is often the best time to take action.

HUD Secretary Scott Turner will function as the “quarterback” of this effort (apropos as he played in the NFL). He has said publicly that he plans to act. And it’s important to know that ending conservatorship was set to happen earlier, but was upended by COVID. On October 28, 2019, FHFA announced a strategic plan to prepare Fannie and Freddie for their eventual exit from conservatorship. And FHFA is currently drafting a recommended approach to the termination of the conservatorship, for Treasury review, which they began before this Administration took power.

A return to independence for Fannie and Freddie could promote a healthier mortgage market and lower costs for consumers.

Just be aware of the potential ramifications and market volatility.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

Andreas Mueller

Post: Renting Primary Residence & Job Relocation

- Real Estate Agent

- Nashville, TN

- Posts 223

- Votes 110

Don't forget 5) principle paydown and 6) leveraged returns, among others.

Owning real assets in this inflationary environment is key to growing wealth, and real estate is the best asset available (in my biased opinion) :) .