Market Trends & Data

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated over 1 year ago on . Most recent reply

Mortgage rates can approach 5.5% in 2024, even if the Fed doesn't cut rates.

Happy 2024 BP Compatriots! Congrats, you made it 😉.

First post of the new year, where if you haven't read one of mine in the past, I do a brief, hopefully insightful, dive into real estate and financial markets. Plus something Nashville related, my home market :).

Today We’re Talkin:

- - Quick Data and News Items of the Week

- - Interest Rates: Is sub 5.5% in 2024 Possible? YES.

- - Consumer Update: rents disinflating but home sales down. Most homebuyers still on sidelines.

- - Tangent! What is the Federal Government Doing?

- - CNBC Special on Nashville: In case you missed it.

Today’s Interest Rate: 6.77%

(☝️ .16% from this time last week, 30-yr mortgage) 3 Curated Items: Data and News to Keep You Informed- 1 - Consumer remains resilient: Personal Income (+.4%) and spending (+.2%) increased in December (BEA)

- 2 - New Homes Sales Down, But a Rise Expected in ‘24 + Gains in residential construction spending and construction job openings (Homebuilders)

- 3 - Home Insurance will continue to rise faster than inflation + State Farm will raise rates 20% in CA starting March 15th, 2024. TX, FL also inflating rapidly. (SF Chronicle)

Interest Rates: Down Soon to ~5.5%?

Rates were up this week, but down on average these last 30 days. What will this do to home prices? 2023 ended up 4.8% YoY, the strongest annual gain seen in 2023, according to Case-Shiller. December numbers are still being tabulated nationwide but this number should hold relatively constant. In my home market of Nashville the data is out however, we were up 8.5% YoY. Interest rates are still too damn high but those able to buy are taking advantage.

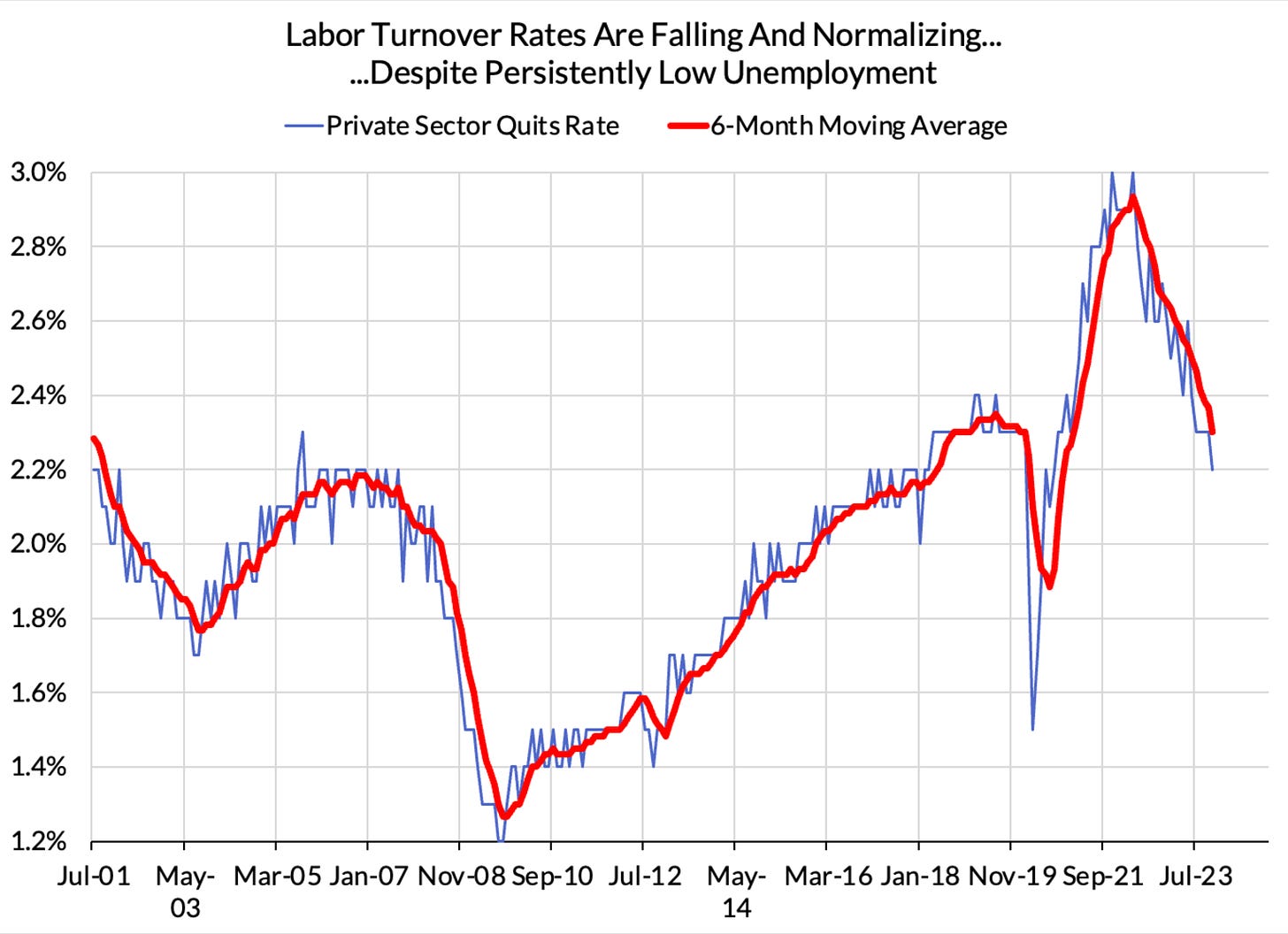

What’s next for interest rates? The 40,000+ employees at the Federal Reserve (still an insane number to me) are probably watching labor markets most closely for signs of cooling. Fortunately, we did see this week some Jack Frost, which should keep the Fed on its course to stepping down rates in 2024: we are now at a pre-COVID job quits.

Look out Lower Mortgage Rates - Is sub 5.5% in 2024 Possible? YES.

Economists will also be watching the bond market, most notably the 10-year Treasury yield. 30-yr mortgage rates track the 10-year and the spread between the two is still historically high. The current difference (“spread”) between the two is 287 basis points (or 2.78%). The historic average “normal” spread is ~175 bps. So if mortgage spreads “normalized,” regressing to the historic mean, and the Fed did nothing from today to lower interest rates, the 30-yr mortgage would be 5.65%. In other words, if the bond market cooperates and the economy doesn’t overinflated, rates should be close to 5.65% in 2024 even without the Fed cutting.

Today’s rates: 10-yr Treasury Yield - 3.90%, 30-yr Mortgage Rate - 6.77%.

My Thoughts10-yr / 30yr spread can go up from here of course. The current spread of 287 is down since spring 2023 where it hit a whopping 330 bps. IMO, spreads will go lower in 2024, but we do need to observe a cooling labor market (and continued lower inflation).

We are emerging out of a real estate recession and so far the data show slowing key indicators, good news for rates. As long as we don’t see a spike in unemployment above 5% and inflation doesn’t tick up above 3% by Q3, the 2024 environment should bring back demand for homes. Again, the Fed says it’s cutting 3 times, the market says it will cut 6 times. IMO 2024 should bring rates somewhere in the 4.75% - 5.5% range.

This insight is HUGE. But keep a watchful eye. (and keep reading my posts 🙂)

The Consumer - MixedSome thoughts/data on the consumer.

Consumer sentiment was way up (14%) in December, reversing all declines from the previous four months. “These trends are rooted in substantial improvements in how consumers view the trajectory of inflation” and likely due to dropping mortgage rates, IMO.

But…

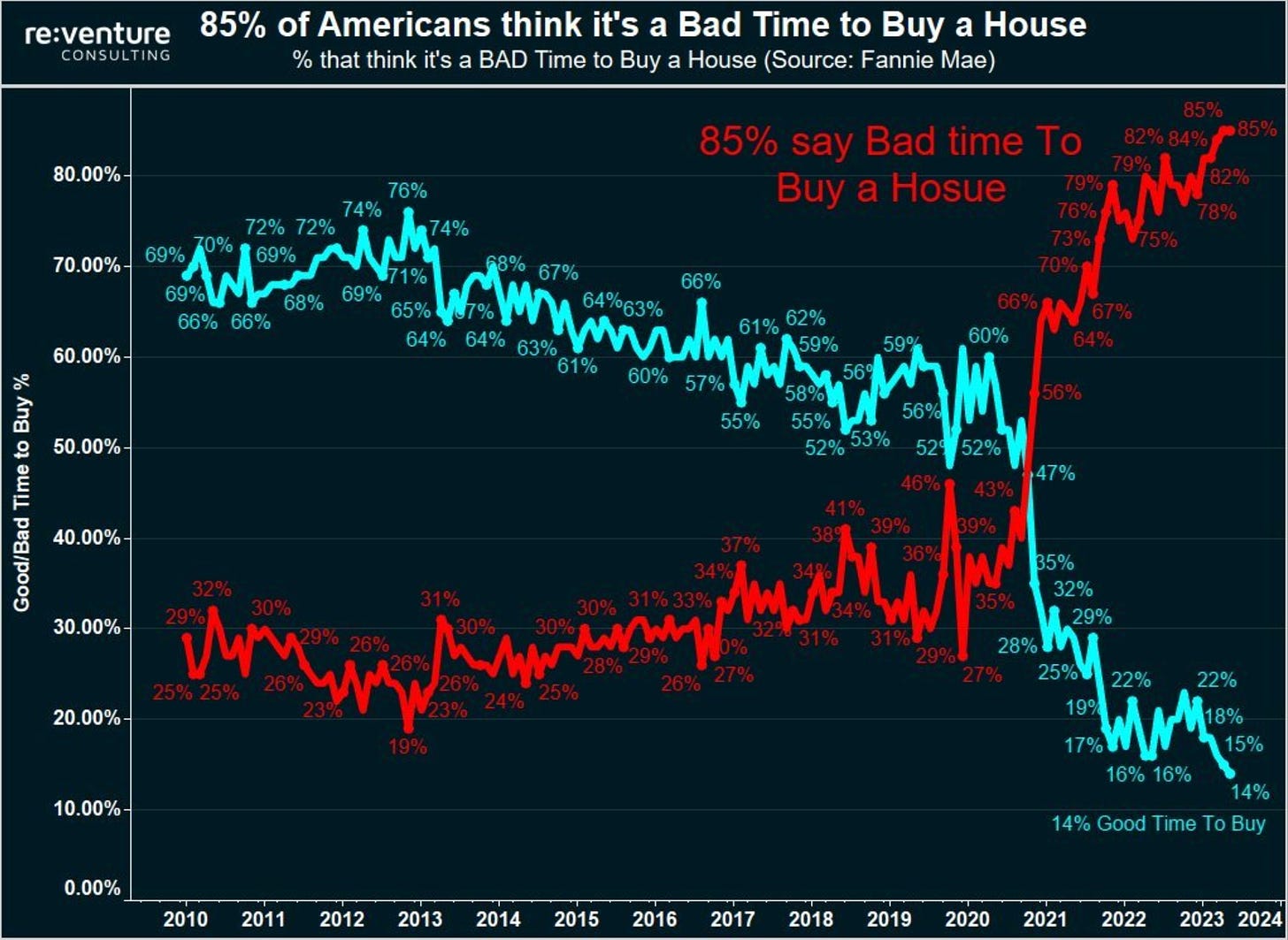

A record 85% of Americans now say it's a bad time to buy a house, according to Reventure. Two years ago, 30% of Americans thought it was a bad time to buy a home. Even in 2008, during the worst housing crisis of all time, this metric did not top 85%.

Millennials (ages 26 to 42), the largest potential buyer of homes, are still on the sidelines. Damn I’m technically a millennial? Although I Identify as a latchkey Gen X-er 😁. I digress….

Millennials, have been hit hard financially and are facing a housing market with high interest rates and low inventory. Many are choosing to rent, and rents are showing signs of disinflation. In fact, median U.S. “asking rent fell 2% year over year in November to $1,967—the biggest decline since 02/2020.” (Redfin)

My Quick Take: Redfin cited a building boom as the culprit but that hasn’t been my experience in Nashville, despite having the most apartments under construction in the country. Rents are still rising, but are disinflating. (I’m referring to single family and small multifamily homes. Now apartments/condos, which I don’t track as closely).

In 2022, millennials were the largest generation of homebuyers, accounting for 43% of all purchases. But that number fell to 28% in 2023. (Business Insider)

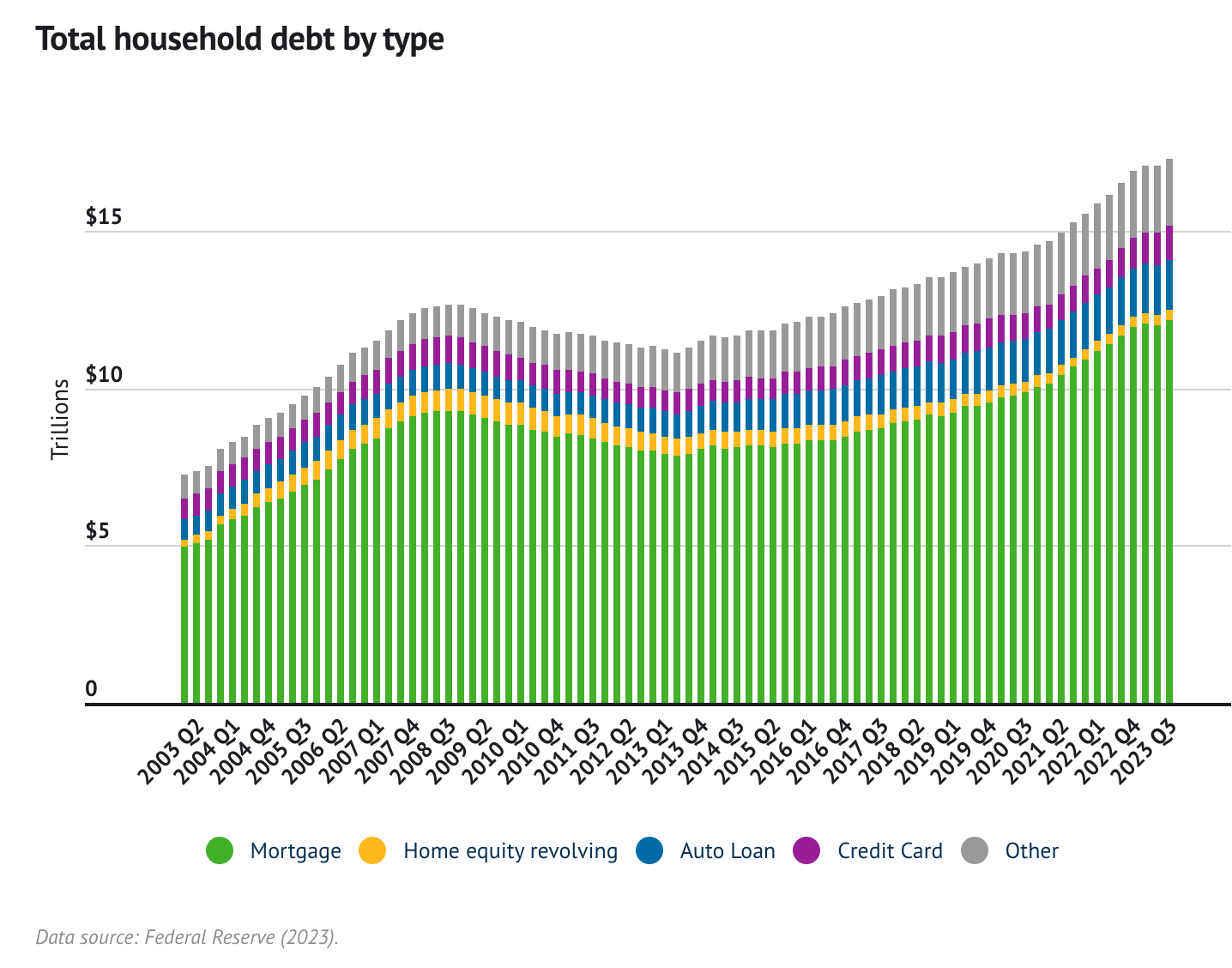

Additionally, total household debt is rising higher.

As are credit card defaults. Although still at historical lows.

So all considering, the consumer is looking in decent shape.

** TANGET Alert!

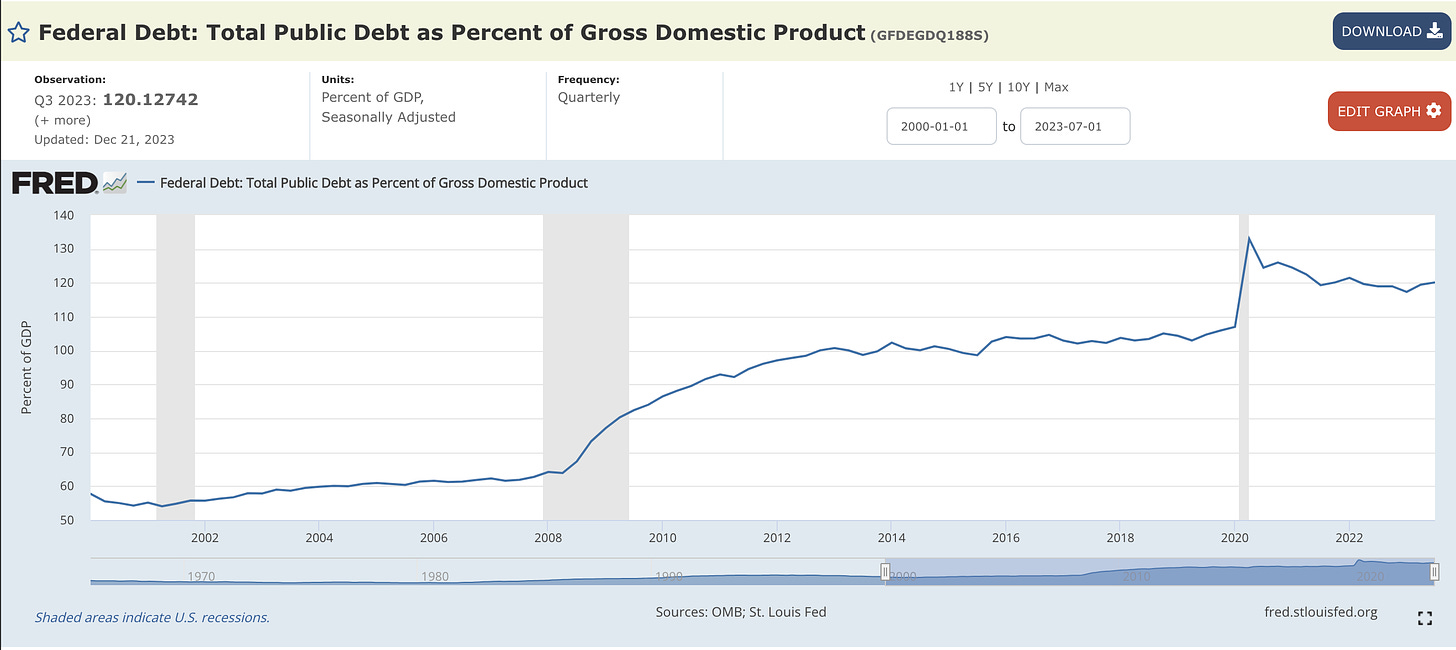

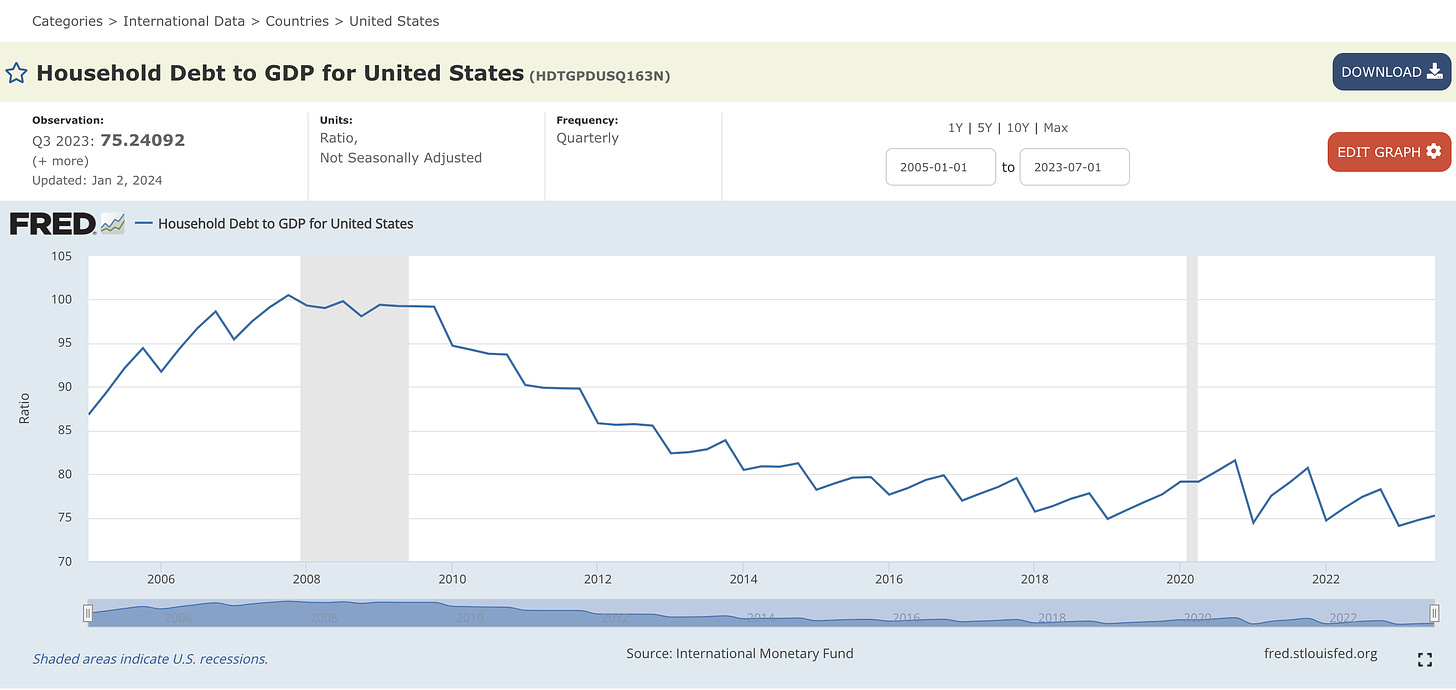

BUT, compared to the Federal Government’s books… well. Take a look at Household Debt to GDP and Federal Debt to GDP. Who looks like they are in more trouble?

Now look at Household Debt to GDP. Lower.

Looks like the Consumer learned their lesson after 2008 (and in fairness banks/congress did do some good here to put credit rules in place, like the Qualified Mortgage). The US National Debt is now past $34 Trillion! Up a whopping $ 29 Trillion since 2000. Insane….

But I digress…

One silver lining: it looks like this largest investment-aged demo is at least putting their money to work, even if they can’t invest in a home. The number of Americans who own stocks is at an all time high; 58% of households, according to the Federal Reserve, as reported by

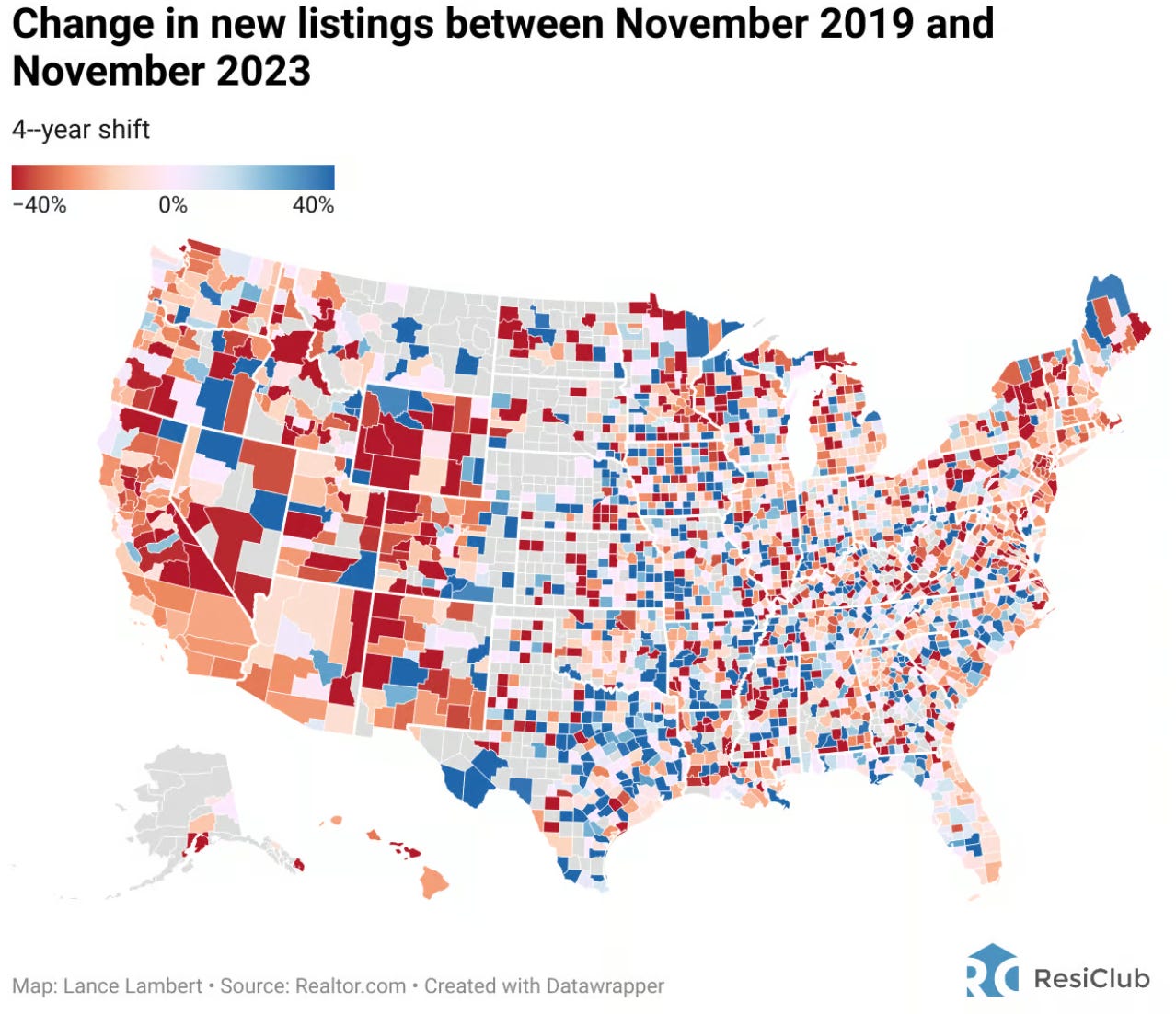

Unusual Whales (a great Twitter follow). Especially if you are in California, where only 15% of Californians can afford a home. As a result, home sales are at a 16 year low. Homebuyers are leaving Los Angeles more than any other metro area in the country, however, the total migration out of cites has slowed considerably, driven by COVID policies.

Probably not used to seeing California colored red :)

In case you missed it: Nashville CNBC SpecialJust in case you missed last week’s newsletter. This is a great series, and they started with my home of Nashville! More of these to come around the country. Stay tuned.

Cities of Success: Nashville. A CNBC Exclusive on the growing city. (TV subscription needed, but should be available soon widely).

Bottom Line

2024 will likely be a banner year for real estate, if you have the dry powder. Start saving / setting aside / raising that money now. We should see 3-6 rate cuts, and housing demand / home sales should tick up. But be careful of building into your numbers debt service and mortgage rates that are too bullish. Keep those numbers skeptical.

To quote the late giant Sam Zell, “Real estate isn’t just about buildings as inanimate objects. It often reflects the pulse of the nation.” Pay attention to what’s happening in your local market and in the economy around you. Talk to business owners, waiters, bartenders, subcontractors. 2024 may be a volatile year, protect your downside.

Most Interesting Tweet of the WeekYuck. Hey @nerdwallet, I know your business is based on ads from lenders/banks/credit card companies that pay for your crappy site that has more pop-ups/ads than a porn site, but…maybe don’t promote stuff like this? It’s predatory and reeks of 2008.

That’s it for this week. If you are interested in digging deeper into these ideas or talkin’ real estate investing - which I always love doing - don’t hesitate to reach out. You can message me directly right here on BP!

Stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

- Andreas Mueller