All Forum Posts by: James Hamling

James Hamling has started 15 posts and replied 4597 times.

Post: Help Finding tenants

Post: Help Finding tenants

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Marcus Auerbach:

Quote from @Tim Swierczek:

Quote from @Marcus Auerbach:

Not a surprise, what you are offering is pretty beat up and you are asking top dollar. No amount of clever advertising or photoshopping pictures will get you over that.

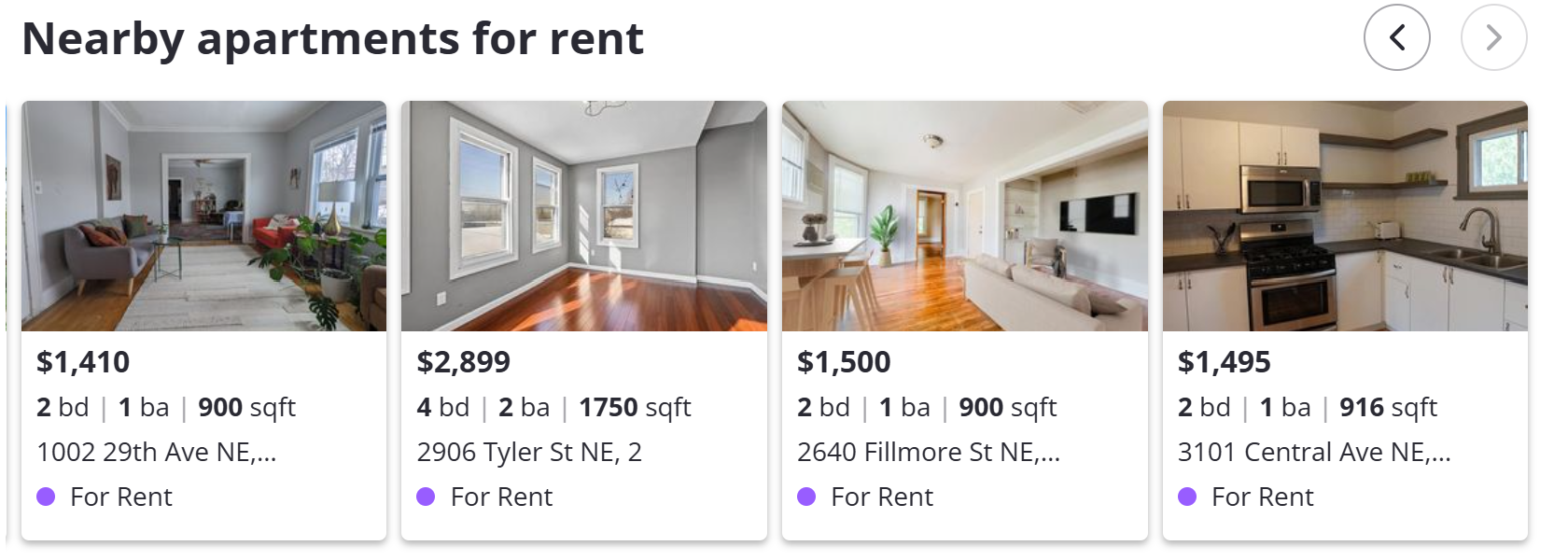

You need to do some mystery shopping and look at your competition. Ideally in person. Just scroll to the bottom of your listing link and you can see 4 places that are quite a bit nicer for under $1500.

You are offering small 900sqft with an original kitchen, only ONE bathroom that is dated and has no counter space, an interior that is a mix of finishes and colors, tile ceiling, super basic light fixtures, no garage and a totally overgrown yard - all of that screams total neglect. Who would rent that for top dollar?

Increasing your rent is horrible advice to begin with; and sweeping the parking lot, virtual staging and hiding the laundry area will certainly not close the obvious value gap!!

The rent amount may not be the issue, but what you are offering is pretty rough.

The other issue is that the only type of tenant you can attract with beat-up finishes are the ones who are on a budget and "don't care".

The single best thing you can do is personally tour some of your competitors close by. Pretend you are interested in renting. And then go back and look how you stack up.

Maybe, and I am not local, so I can only go by the data and could be wrong. But here is the thing: an adequate 3 bedroom unit has at least 1200 sqft. At only 900 these rooms must be glorified walk-in closets.

When you look at large data sets you find that there is a stronger correlation between rent and sqft than rent and number of bedrooms. That's why analysts like CoStar always measure daily asking rent/sqft.

Unless you are a family with a number of kids, bedroom count is not that important - the 3rd room is often just a guest room. So people will be happy to have it, but they don't need it.

After checking the location online, the two top questions everyone has when touring an apartment are:

1.) Is it nice?

2.) Is it spacious?

In this case, the answer to both questions is no. You can't change the size, but you can replace the kitchen, tough on the bathroom to fit a counter, because of the size, paint the rest, upgrade light fixtures, evaluate and update flooring, millwork as needed - no matter how cheap you do that, it's hard to make the numbers work.

Ultimately, the market will render the verdict. If you are not getting showings, you are not attractive. IDK what the benchmark is in your market. For our SF in the Milwaukee suburbs, I know if we don't get 10 inquiries per day in the first week, we have missed the mark. After phone screen and no-shows we usually end up with 12-15 in-person showings and we batch them over 2 days - a weekday night 6-7pm and a weekend day 1-2pm or so.

Maybe it's less for Minneapolis, but if you are getting the silent treatment from the market you have two choices: cut asking rent or take it off the market and call some contractors.

Not to throw gas on the fire here Tim but I gotta agree with Marcus on this one.

This place is pretty dang rough, to put it nicely.

Marketed as heart of NE, which it's not, Psycho Suzi's was really the beating heart of NE, and this place is a dang near in Columbia Heights. Anyone looking for "heart of NE" there looking for a specific experience and this sure ain't it.

Next, NE is like Northloop, TRENDY, right. Nothing about this place speaks to that, nothing at all. Colors, finishes, condition, nothing.

And a 900sqft basically is a 2br unit, that's how standard tenant's will view it when bedrooms are so dang small. Except for the bottom of the rung tenant demo which is now into attracting the opposite type of tenant the listing seems to be worded for.

The listing seems to be all kinds of opposites. The wording is of a great location, a great offering, but the property looks like a sec8 Broadway type property.

Sorry if it hurt's OP feelings but it's the brutal truth of it, the property is nowhere near the standard it's speaking to.

So if want that kind of tenant, it would require a hefty rent reduction, because your gonna have to bribe that tenant to deal with all the short comings. But on upside, that tenant will most likely fix the place up too. They'd paint it, probably do yard work, ask about updating things, so there is some merit and value to that hefty discount past a quality tenant.

But if just focusing on squeezing blood from the rock, your gonna get on of "those" tenants all but certainly.

A/C is a must have in MN for any even half way decent tenant, we know this.

The yard, what value is that? It's a shared space with another unit, there is limited value to that.

There is a lot wrong with this listing and yeah, I'd agree they gotta get down to $1,500 if they care about tenant quality at all.

What I lease in the area for $2k+ mnth is a heck of a lot more home then this.

New paint inside and out, updated kitchen and bath, updated fixtures, cleaned up and landscaped yard, yes, now you got a chance to reel in those tenants around that $2k mark, and with A/C. But as-is, yikes it's rough.

Honestly, as-is, might as well embrace it and just go sec8, seriously. Then put efforts to getting that diamond of a sec8 tenant, they exist. Upstairs unit makes it tougher, won't get the elderly/aged, and being 3br it will attract the wrong kind but that's where I'd say efforts are best placed, screening for the right sec8 tenant vs a hipster young couple/group.

Post: Structural engineer needed

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

@Jay Lee a lot more detail is going to be needed on your situation specifics, like why you need one, what your knowledge level is, what your specifically looking for the Engineer to do.

I've worked with several but I'm over 30yrs in housing industry with decades as a builder and multi-journey, so for me I just needed an Engineers stamp, had all prints and details done n set so they were just reviewing and, as said, stamping.

A couple times I was doing something jazzy that I dreamt up myself so there was some interaction about my hair-brained idea, but process was pretty much the same that I had all prints and details completed and it was just review and approvals.

So my experiences have all been very good. But I'm an industry insider basically talking shop.

If a person has little to no experience or knowledge, has little to no idea of what there doing and calls an engineer out expecting them to be quick, cheap or to act like a GC, it's probably going to be a painful experience I'd guess.

Post: Has anyone here successfully navigated this situation?

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

@Frank Pyle there is regulations in your market for how such a property get's designated, and what one has to do to get the designation changed.

For example, in MN the property has to be permanently affixed to a foundation structure, and there is assorted options and details from on concrete slab, pilons with anchoring straps, etc etc..

From there, in MN, an inspection must be completed showing compliance, the manufactured home title which is held by DMV is surrendered to county with paperwork and shazam it's a SFH.

In your scenario it would appear the first one did that process, and the second hadn't.

Get with your local building and zoning authority to find out the details of how to get-r-dun.

Post: What is the most common loan size you see from investors?

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

I am really confused here @Kyle Vogeler.

Your talking multi-family, which intones size. And value-add which ad's complexity. And your looking to do this in a way that sure as heck sounds like syndication, but not following sec rules & reg's until having done some......

And all of this with just $10k from LP's......

This sounds like a recipe for all kinds of bad outcome potentials.

What am I not getting here?

Post: If you had $10M, how would you invest it?

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Austin Fowler:

Quote from @V.G Jason:

Quote from @Austin Fowler:

Quote from @V.G Jason:

Quote from @Gregory Schwartz:

Take $20M, pick up 50 single-family homes at ~$400k each. Rent them at $3k, net about $2k per door. That’s $100k/month in cash flow, plus appreciation. Low-maintenance properties, low-drama tenants, simple portfolio. It’s not flashy, but it’s clean, seats enough to self mange (for the REPS tax benefits), and lets you live well without headaches

$3k at $400k is hard, but possible. Have some higher, some lower, but mainly higher. You'll still have tenant issues, maintenance, etc. To think it'll be all roses is just naive. Fortunately have PMs, AI agents, etc.

With $10 mil continue to be focused on properties in Austin, and Phoenix. Doesn't change for me on the personal portfolio.

$1mil folks worry about protecting their wealth. $10mil folks focus on growing their wealth. But to get to the latter, you usually have to go through the former. Majority of this board shouldn't be focused on this problem though. Think it's just to sniff out potential investors for OPs fund.

Hi V.G., the goal is to encourage actual real estate experts, actual people that operate at this scale, to share techniques that work at this scale and help educate people to head in that direction as well. If you anyone wants to operate at this scale, they need to focus on learning techniques that work at this scale. When it comes to building wealth, you can waste decades of your life learning labor intensive techniques and building a portfolio that simply doesn't scale.

I "operate" with more "scale" than 99% of BP.

And I'm telling you 99% needs to stop being obsessed with scale. And start being obsessed with diligence.

You're getting it right from the horse's mouth, yet still want to push this point. It's missing the forest for the trees. You're trying to scale by acquiring outside capital, I get it. Go do that in a proper form.

Totally agree with a need for everyone to be obsessed with due diligence. For example, when I acquire an asset, it is a month+ long process involving hundreds of people doing group due diligence trying to find holes in the deal and learning more about it before anyone invests. It's an approach anyone can use. I disagree with the philosophy that there are some special people that use special techniques that are amazing and can't even be explained, and then a majority of average people that should stick with average techniques that don't scale. There are good investment techniques that anyone can use that are scalable. One example of such a technique is doing extensive group due diligence on passive multifamily. Another is simply cash or an index fund, neither of which chew up your time and scale arbitrarily. This thread is all about identifying scalable techniques that anyone can use. Or just interesting techniques that people have used at scale. Working together as a community to educate each other.

Scalability is easily and readily available for the vast majority, scalability is not the issue for most.

The issue for most is how limited their investment capitol is, the massive return expectations being sought, over an exceptionally short time-span.

Many seeking parabolic, unrealistic, compounding returns. Which are not really returns, as so many are actually seeking full income replacement via the "investing".

To boot, adding in the riders of things such as "passive", "low risk" and "certain"......

To be fair Austin, you as a syndicator are hacking the scalability via syndication, O.P.M.. Most are not capable, willing or interested in raising O.P.M. to scale and thus a natural limiter of there investible capitol.

Remove your LP capitol, you would not be at the size you are, correct? No syndicator would. So it's not fair to pretend it's the deals that make scalability alone. It is possible but it is very rare, exceptional and non-ordinary for such.

For the vast majority who are measuring their investible capitol in the tens of thousands, while balancing a FT career, a family, life in general, yes it is rare skills and talents to find, analyze and execute on profitable investments at any kind of regularized interval. And in those early steps, the outlay of capitol far outstrips the returns for years or decades limiting any reasonable expectation of scalability.

In my experience the primary focus for most is not on scalability but on certainty to achieve financial freedom. Which is often defined as a passive income about matching to current active income levels.

For most the only scalability that matters is how to get to their ends. I often see a correlation that this is meet for most between 20-40 SFR's.

For many, scaling beyond that is just added work, and no longer "freedom" as was the entire intent from start, financial freedom, not an occupation change.

Post: Federal Layoffs Effect? - 1,633 New Listings In D.C. Area Last Week

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Russell Brazil:

Quote from @James Hamling:

Quote from @Ken M.:

Quote from @Ken M.:

Feb 21 2025

This is just a marker to see if Federal Layoffs actually affect the real estate in the D.C. Area

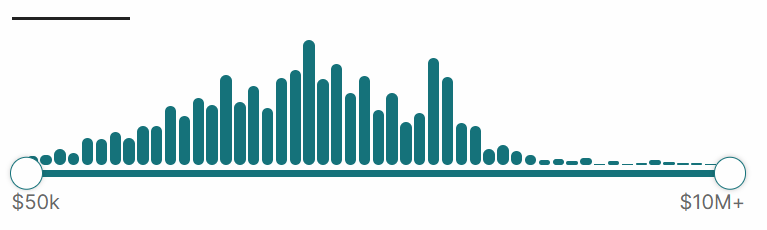

Redfin lists 1,463 New Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

Redfin lists 5,888 Total Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

And here is the price distribution

.

Aug 28 2025

Now the map is

Redfin lists 2,035 New Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

Now Redfin lists 10,548 Total Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

And here is the price distribution

Now, I'm not a mathematician, but I think the number of properties went up.

From 5,888 Total Listings to 10,548 Total Listings

or about 79.14 %

Maybe those federal layoffs have had an effect? Nah, couldn't be, must be the slowing rotation of the earth, climate change, co2 emissions or something. I don't think the full story has been written yet.

When D.C. is no longer the nations capitol, home to a rotating door of lobbyists, special interests, consulate adjacent things, that's when I will have some concerns.

Until then everything else is just a selling opportunity, a buying opportunity, or a leasing opportunity.

Let's not forget DC also has the infrastructure of the entire east coast pipelines of the internet, and thus giving them the 2nd largest tech sector workforce barely less than the Bay area. It also has the largest private sector legal sector. All the major. Major pharmaceutical companies, major hospitality companies all headquartered here.

And at risk of letting my nerd-flag fly..... all the museums, it's the "Intellectuals Vegas".

I could spend a week in D.C. and probably not get my fill of things to do and see. Not a fan of the oysters though, I gave em a fair shot, still think it tastes like sea-weed snot, lol.

Post: Federal Layoffs Effect? - 1,633 New Listings In D.C. Area Last Week

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Ken M.:

Quote from @Ken M.:

Feb 21 2025

This is just a marker to see if Federal Layoffs actually affect the real estate in the D.C. Area

Redfin lists 1,463 New Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

Redfin lists 5,888 Total Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

And here is the price distribution

.

Aug 28 2025

Now the map is

Redfin lists 2,035 New Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

Now Redfin lists 10,548 Total Listings In D.C. Area Last Week from Manassas Park to Bowie (why those points? Because that's what fits on my screen) ;-) There is no regard to type of listing and new construction is not included

And here is the price distribution

Now, I'm not a mathematician, but I think the number of properties went up.

From 5,888 Total Listings to 10,548 Total Listings

or about 79.14 %

Maybe those federal layoffs have had an effect? Nah, couldn't be, must be the slowing rotation of the earth, climate change, co2 emissions or something. I don't think the full story has been written yet.

When D.C. is no longer the nations capitol, home to a rotating door of lobbyists, special interests, consulate adjacent things, that's when I will have some concerns.

Until then everything else is just a selling opportunity, a buying opportunity, or a leasing opportunity.

Post: If you had $1M, how would you invest it?

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Austin Fowler:

Quote from @James Hamling:

Quote from @Joe S.:

Quote from @James Hamling:

Ok @Austin Fowler you really want to know what I'd do if dropped $1m liquid in my hands and I gotta utilize it in Real Estate, even though all of 7 people on BP will comprehend it......

About $5k into website, 2 VA's and system.

From there 1 VA calls on active buyers agents in designated markets presenting pitch to fill my calendly.

From there I pitch my C4D program for "nearly financed" buyers. When the buyers agent get's leads, works em, and finds there buyers are oh-so-close to approval but not there, they can still earn that commission via my C4D program.

Everything would revolve around "median" world of things.

Required minimum down payment is 20%. No exceptions. Everything else, there would be guidelines but just that, guidelines and negotiable whereas down has 0-flex.

All app's via website. Va#2 process's per training.

Buyers get a pre-qual budget. Buyers agent then helps them shop for such. When they find the right one, buyers enter agreement and post held escrowed down with me. Buyers agent submits PA, myself as buyer.

At end of day, it's infinite investing, because when closing is done and all $ has cleared I am personally $0 into any property, that $1m was simply used to launch the biz and then to leverage to landing the PA's.

The tenant-buyers financed the purchase via there down, which I utilize to unlock financing on the purchase. I would be using portfolio lending on DSCR underwriting, cross securitized by, you got it, the giant pile of cash sitting in an account spinning round n round.

Now being C4D buyers there is 2 spreads. First is on purchase price, second is interest rate.

I only have to capitalize risk exposure, overhead and profits because I have $0 invested capitol. Thus a small spread can equal sizable returns.

Now if you understand the math here, buyers doing 20% down on a buy price that has a profitable margin built in, then you understand how it would be more then 20% on my actual purchase. Probably more-so 30%.

In summary, I wouldn't deploy 90% of the $1m, I would leverage the lions share of the $1m to unlock infinite returns via OPM.

And I am now well liquid to cover any potential default issues if such were to occur. But being "median" focused and with C4D buyers who put 20%+ down aka significant skin into it, well one would have to chop off there own preverbal legs to give me a bloody nose. And I'd be well liquid to more then amply take care of any bloody-nose.

My risk exposure would be less then that of standard landlording, as the tenants would have far more securitization. So risk wise, it's a low-risk strategy in real estate.

And end of day, everybody is winning, the agents win, the end buyers win, and I win.

The trick to it all is setting and keeping good fences.

100% of C4D's I have seen blow-up have all had the common component of neglect on behalf of the investor. Selling to persons they shouldn't have, under securitizing, not keeping strong fences.

There ya-go Austin, that's what I'd do. And I'd dedicate as-much-as 20hrs a week to it. I'd fund my va's for 90 days and from there forward I'd require the venture to self-fund all operations from revenues. And that would be my "stop-loss". The moment it stops self-operating, I'd end it, regardless of a causation.

Thus preserving my capitol.

Hey James, you do not have to wait to get $1 million to do one or two of deals as a test run…IMO

I think that is a very thought out plan. A couple of thoughts though. From my observation, it is harder to get a substantial down payment and a higher than market interest rate at the same time. (Maybe your market is different.)

In Texas contract for deeds are not smiled upon at least that's the word on the street. I have a number of DSCR Loans that I am nervous to wrap if I could do the C4D like you're speaking over here I would definitely consider doing it.✅

I have a friend of sorts that has wrapped some DSCR loans with no problems. I'm just a bit nervous to do so…

All very valid points Joe.

In my experience there is no shortage of person who want to buy on C4D, but those correctly capitalized, yes they are the diamonds in the rough.

And that is the entire point of C4D, in my eyes at least, it's not for everyone. C4D is "a" tool in the tool-box. It has a specific purpose, and best use. When used wrong, like a pipe wrench to pound a nail, well let's just say "results may vary" is an understatement.

My most ideal C4D buyers are self-employed, often in first years, especially when in a service industry. Think Electricians, Plumbers etc.. Where they have great enduring incomes, and immense write-off potentials. They commonly run into the problem of being told they need to take 2 years of hit's on the paperwork, use less write-off's, to more accurately show income to achieve the financing approval looking for.

I don't use C4D for buyers seeking to gain what they can't actually afford, on faith and hope that someday in the future they will.

In my experience about 95% of people first are not so welcoming or interested in C4D, and for good reason, it's lessor known and has been used and abused by nefarious persons way too often. If I get 10 minutes to discuss it, 95% become accepting. It's about doing it legally and thoroughly. I always have full closings and R.E. Attorney on every one. I encourage inspections and appraisals. Sunlight is the best disinfectant, right.

I say DSCR just for simplicity of the paperwork. Key is more on using portfolio lending. When have such a relationship with a bank, and repetition, it breeds comprehension and security. To be more exact I'd, at whatever point, utelize a commercial financing "product", but as said portfolio, with a LOC. We would close via the LOC, then they complete paperwork to then roll that next purchase into the entire whole of the financing, and replenish that LOC. The actual account with the capitol would just sit in it's account, used just as eye-candy for the PA's, and warm-fuzzy feeling for the bank I'm working with.

One may wonder "but what about when you get ____ properties in there?". Keep scale in mind, there C4D's, they ideally finance out in 3-5yrs, so there is a natural churn to it all. And a person is going to do what, as-many-as 10 a year, maybe. 50 SFH's worth isn't really all that much $ in commercial finance terms.

If your concern on wrapping DSCR is on a what-if revenues get interrupted, I'd remind that by wrapping in a grouping you lower your risk exposure. 10 SFR's on a mortgage is much safer than 1, because loss of any 1's revenue is only a loss of 10% revenues, not 100%. Same way insurance works on risk exposure.

As for not needing the $1m, I know, I do these now, and have for years, hence why I can rattle on about them, because I actually do them and am speaking from experience not theory.

Well..... except for scaling, that is theory, I am not at-scale on it, not at all, haven't tried to scale but have thought on it a few times. I don't market it at all, 100% word of mouth....

What scale has your current word of mouth approach got you to?

I'm not sure how to answer this question....

In your segment of the industry my nickname is "oz". If know of me, let's just leave it at that and not get into shop talk here as much in that space carried NDA's to them.

If talking specific to just C4D scale from word-of-mouth........ I don't have that exact # off top of head but shooting from the hip, in the range of 40/50'ish completed in last few years. Since covid.

It's kinda funny how memory bench-marks certain events, like "since covid" or post GFC etc., but that's how I readily recall things, in which "era" they were.

Post: If you had $1M, how would you invest it?

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Austin Fowler:

Quote from @James Hamling:

Quote from @Austin Fowler:

Quote from @Remington Lyman:

Quote from @Austin Fowler:

Very interested in hearing people's investment strategies in real estate. What do you do? What are you passionate about? What kind of returns do you target when investing? How hands-on are you? How scalable is your investment approach? If you won or inherited or otherwise suddenly had $1M in cash, how would you use it to expand your portfolio? Or accelerate your wealth creation?

I like buying properties and having my tenants pay off the debt with their rent. I am passionate about making money. I do not do a good job calculating returns; I just try to buy good deals. I am pretty hands on. It is pretty scalable. I would put it in a money market account and buy properties as I come accross them

What is your definition of cash flow? Rent - management - vacancy - maintenance - taxes - insurance - mortgate? Can you give an example of something available today that would cash flow? Without cashflow, how would you scale?

Your asking the wrong question Austin. You should be asking at what annual rate is the scalability.

One can scale buying and doing standard rentals. But scaling will be measured in years and decades. The rate of capitol return is simply not something that lends to any significant self-scaling metric. Period, full-stop. Those who say there C/D can scale so fast blah blah blah, there full of sh#t, or too new or clueless.

The only "hack" is some form of hacking, as in house hacking, something of that nature and in that the scalability is created by the buy and build, not the operation itself. Because these strategies literally create equity. Equity that speeds up capitol recapture, so one has the capitol to scale.

Scaling requires capitol. When talking real estate, it means sizable capitol. There is no passive or passive-like monetization of real estate that generates the kind of capitol required for any note worthy pace of acquisition.

Cash-flow is generally measured in hundreds. Acquisition costs are generally measured in tens of thousands. The former does not lend to any rapid scaling of the later.

100%.

But therein lies the crux of it all.

The novices are lulled by promises of cash-flow, to then be crushed on the capex rocks, because they chased a false promise.

They used a feeling of scale, vs an accuracy of complete numbers and reality. Because the desire to get-in, scarcity of viable opportunities, FOMO, leads them into capitol drains vs capitol contributors.

In my experience most thought/felt what they were doing would make $, and scale, only to experience a very different reality. Very few intentionally, knowingly and willingly enter as an equity investment. I have many of the later as clients, I have helped many of the former. The later are a much more rare breed.

Post: If you had $1M, how would you invest it?

- Real Estate Broker

- Minneapolis, MN

- Posts 4,772

- Votes 6,268

Quote from @Joe S.:

Quote from @James Hamling:

Ok @Austin Fowler you really want to know what I'd do if dropped $1m liquid in my hands and I gotta utilize it in Real Estate, even though all of 7 people on BP will comprehend it......

About $5k into website, 2 VA's and system.

From there 1 VA calls on active buyers agents in designated markets presenting pitch to fill my calendly.

From there I pitch my C4D program for "nearly financed" buyers. When the buyers agent get's leads, works em, and finds there buyers are oh-so-close to approval but not there, they can still earn that commission via my C4D program.

Everything would revolve around "median" world of things.

Required minimum down payment is 20%. No exceptions. Everything else, there would be guidelines but just that, guidelines and negotiable whereas down has 0-flex.

All app's via website. Va#2 process's per training.

Buyers get a pre-qual budget. Buyers agent then helps them shop for such. When they find the right one, buyers enter agreement and post held escrowed down with me. Buyers agent submits PA, myself as buyer.

At end of day, it's infinite investing, because when closing is done and all $ has cleared I am personally $0 into any property, that $1m was simply used to launch the biz and then to leverage to landing the PA's.

The tenant-buyers financed the purchase via there down, which I utilize to unlock financing on the purchase. I would be using portfolio lending on DSCR underwriting, cross securitized by, you got it, the giant pile of cash sitting in an account spinning round n round.

Now being C4D buyers there is 2 spreads. First is on purchase price, second is interest rate.

I only have to capitalize risk exposure, overhead and profits because I have $0 invested capitol. Thus a small spread can equal sizable returns.

Now if you understand the math here, buyers doing 20% down on a buy price that has a profitable margin built in, then you understand how it would be more then 20% on my actual purchase. Probably more-so 30%.

In summary, I wouldn't deploy 90% of the $1m, I would leverage the lions share of the $1m to unlock infinite returns via OPM.

And I am now well liquid to cover any potential default issues if such were to occur. But being "median" focused and with C4D buyers who put 20%+ down aka significant skin into it, well one would have to chop off there own preverbal legs to give me a bloody nose. And I'd be well liquid to more then amply take care of any bloody-nose.

My risk exposure would be less then that of standard landlording, as the tenants would have far more securitization. So risk wise, it's a low-risk strategy in real estate.

And end of day, everybody is winning, the agents win, the end buyers win, and I win.

The trick to it all is setting and keeping good fences.

100% of C4D's I have seen blow-up have all had the common component of neglect on behalf of the investor. Selling to persons they shouldn't have, under securitizing, not keeping strong fences.

There ya-go Austin, that's what I'd do. And I'd dedicate as-much-as 20hrs a week to it. I'd fund my va's for 90 days and from there forward I'd require the venture to self-fund all operations from revenues. And that would be my "stop-loss". The moment it stops self-operating, I'd end it, regardless of a causation.

Thus preserving my capitol.

Hey James, you do not have to wait to get $1 million to do one or two of deals as a test run…IMO

I think that is a very thought out plan. A couple of thoughts though. From my observation, it is harder to get a substantial down payment and a higher than market interest rate at the same time. (Maybe your market is different.)

In Texas contract for deeds are not smiled upon at least that's the word on the street. I have a number of DSCR Loans that I am nervous to wrap if I could do the C4D like you're speaking over here I would definitely consider doing it.✅

I have a friend of sorts that has wrapped some DSCR loans with no problems. I'm just a bit nervous to do so…

All very valid points Joe.

In my experience there is no shortage of person who want to buy on C4D, but those correctly capitalized, yes they are the diamonds in the rough.

And that is the entire point of C4D, in my eyes at least, it's not for everyone. C4D is "a" tool in the tool-box. It has a specific purpose, and best use. When used wrong, like a pipe wrench to pound a nail, well let's just say "results may vary" is an understatement.

My most ideal C4D buyers are self-employed, often in first years, especially when in a service industry. Think Electricians, Plumbers etc.. Where they have great enduring incomes, and immense write-off potentials. They commonly run into the problem of being told they need to take 2 years of hit's on the paperwork, use less write-off's, to more accurately show income to achieve the financing approval looking for.

I don't use C4D for buyers seeking to gain what they can't actually afford, on faith and hope that someday in the future they will.

In my experience about 95% of people first are not so welcoming or interested in C4D, and for good reason, it's lessor known and has been used and abused by nefarious persons way too often. If I get 10 minutes to discuss it, 95% become accepting. It's about doing it legally and thoroughly. I always have full closings and R.E. Attorney on every one. I encourage inspections and appraisals. Sunlight is the best disinfectant, right.

I say DSCR just for simplicity of the paperwork. Key is more on using portfolio lending. When have such a relationship with a bank, and repetition, it breeds comprehension and security. To be more exact I'd, at whatever point, utelize a commercial financing "product", but as said portfolio, with a LOC. We would close via the LOC, then they complete paperwork to then roll that next purchase into the entire whole of the financing, and replenish that LOC. The actual account with the capitol would just sit in it's account, used just as eye-candy for the PA's, and warm-fuzzy feeling for the bank I'm working with.

One may wonder "but what about when you get ____ properties in there?". Keep scale in mind, there C4D's, they ideally finance out in 3-5yrs, so there is a natural churn to it all. And a person is going to do what, as-many-as 10 a year, maybe. 50 SFH's worth isn't really all that much $ in commercial finance terms.

If your concern on wrapping DSCR is on a what-if revenues get interrupted, I'd remind that by wrapping in a grouping you lower your risk exposure. 10 SFR's on a mortgage is much safer than 1, because loss of any 1's revenue is only a loss of 10% revenues, not 100%. Same way insurance works on risk exposure.

As for not needing the $1m, I know, I do these now, and have for years, hence why I can rattle on about them, because I actually do them and am speaking from experience not theory.

Well..... except for scaling, that is theory, I am not at-scale on it, not at all, haven't tried to scale but have thought on it a few times. I don't market it at all, 100% word of mouth....