Welcome to my weekly Investor Newsletter. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Today We’re Talkin:

- - The Weekly 3 - News, Data and Education.

- - All the “whys” for High Home Prices

- - Home Prices, it’s more than just supply and demand.

- - Generation Toolbelt. LFG!

- - Bring Back Home Ec!

- - My Skeptical Take.

Fuel for the Day: Greens! I actually make my own greens smoothy / drink often but when I am on a writing heater and don’t want to pause, I grab some AG1. Good stuff, really good. Gets my brain firing.

The Weekly 3: News, Data and Education to Keep You Informed

- - Folks are Skipping Till to Spring to Buy. Rates are coming down in a few months, and buyers know it (, ).

- - Refinancing is starting back up again. But you ain’t seen nothing yet (ResiClub).

- - Book Recommendation: Bubble in the Sun: The Florida Boom of the 1920s and How It Brought on the Great Depression. The 1920s in Florida was a time of excess, immense wealth, and precipitous collapse. It was the largest human migration in American history, far exceeding that of the West. And it was real estate speculation here that helped cause the Great Depression. This is a must for your library, something to re-read again and again (Knowlton).

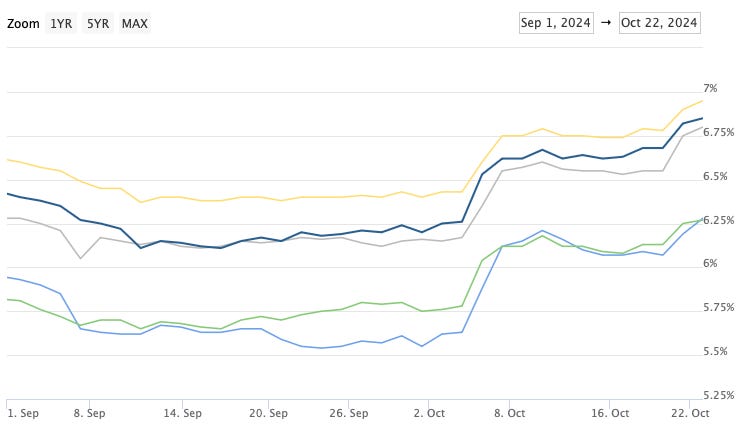

Today’s Interest Rate: 6.25%

(☝️.06, from this time last week, 30-yr mortgage)

Guten Morgan investors. It’s a lovely day to talk real estate. Let’s get into it.

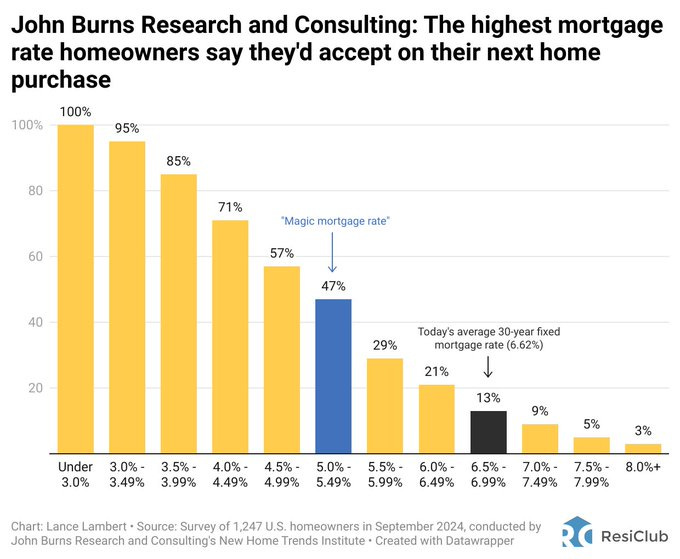

Last week was all about rate cuts. But it’s going to be a while for mortgage rates to come down (as I’ve written about), so for now let’s put that on the back burner and talk about something poignant.

Home Prices.

Why are Home Prices

This High?

The primary reason for the price of anything is simple supply and demand. (And we will get into significant secondary reasons below, keep reading!)

In the case of housing: we have ample demand (and more on the sidelines waiting to jump in once rates tick down) and not enough supply. Not even close.

Supply is currently short 1.5 million housing units of what is needed to keep up with demand.

Increasing Supply Works!

Case in point, in 2017-2019 while facing a severe housing shortage, Minneapolis enacted its 2040 Plan, becoming, “the first major U.S. city to end single-family exclusive zoning, opening the door for developers to build multifamily buildings on lots where a single-family home used to be (NBC).”

The result? Supply UP!

A Pew Research report found that between 2017 and 2022 - the beginning of the Minneapolis 2040 plan - “housing stock grew by 12% in the city, compared to 4% statewide. An NBC News measure of home buying difficulty shows that Hennepin County, where Minneapolis is located, is the second-easiest county to buy a home in compared to the seven counties adjacent to it — even though Hennepin is the most populous county in the state.”

Great damn job Minneapolis!!!!

What Else is Contributing to Home Prices?

Supply and demand this is not the whole story. Home prices are higher than they normally would be even in these tight market conditions.

Tell me why!

Well, I don’t mind if I do.

Home prices have been amplified because of the increased costs for builders to actually build a home in the US, mainly:

- Inflation (materials and labor).

- Regulatory burdens.

Let’s look at both:

Inflation

Prices for everything necessary to build a home - including building materials and hourly labor - are much much more expensive. These higher prices are likely permanent, as prices rarely deflate (and that can cause a whole other set of economic problems).

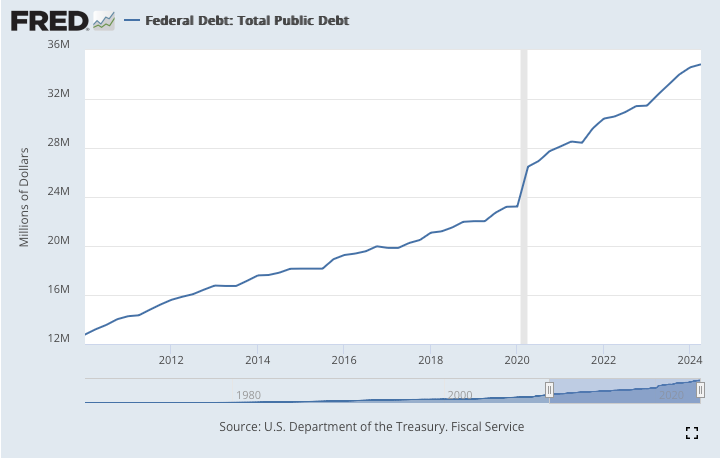

I have written at length about the case and effects of inflation. In short, inflation is caused by policies and spending (not consumers or businesses). And over the last few years, we went on quite the money printing spree.

More than $10 Trillion!

You can read all about what the US did in my previous article on the subject here.

It’s a doozy.

For now, just know we had a few years of much higher than normal inflation and it caused permanent damage in the form of higher input prices to build a home.

Regulations

The second cost of a home is regulatory policy. Especially for large development (ie apartment and condo buildings), where many of our housing units come from.

Building housing is subject to a significant array of regulatory costs, including a broad range of fees, permits, reviews, and other requirements imposed at different stages of the development and the construction process, with both a direct cost and a time/delay cost.

In fact, according to a recent study, regulation “imposed by all levels of government accounts for an average of 40.6 % of development costs (NAHB, O’Leary).”

Apartment developers in particular are subject to a variety of regulations across all levels of government. They include: zoning requirements, building codes, impact fees, permitting requirements, design standards, public land requirements, and federal Occupational Safety and Health Administration regulations and other labor requirements. Unfortunately, many regulations, such as design standards, go far beyond important safety concerns, and impose costly mandates on developers that drive housing costs higher. Others are duplicative and require resources to confirm compliance with multiple regulators with overlapping jurisdictions.

Further, the study noted that “[Three quarters (74.5%) of housing developers said they encountered “Not In My Backyard” (NIMBY) opposition to a proposed development, adding ~ 5.6% to total development costs and an additional 7.4 month delay.]”

Wow.

This is why both presidential candidates are talking about the need to reform housing regulations on the campaign trail.

Construction Innovation: A Call to Action

It seems that innovation in the construction technology space, and thus labor productivity, is an area for significant improvement.

Productivity in virtually all industries is accelerating over time, leaving construction in the stone ages.

Logan Mohtashami

We don't really build homes that differently than we did 100 years ago.

Why?

We need investment in construction technology and government needs to green-light it asap.

It’s just too expensive to build a home!

Gen Z is Gettin Handy

One glimmer of hope is the new Generation Z folks are getting interested in the trades. Gen Z is becoming known as Generation Toolbelt.

Love it!

A fantastic Wall Street Journal article reviews the renewed interest in vocational training, manufacturing and hands-on labor fields.

From the article:

“Demand for trade apprenticeships, which let students combine work experience with a course of study often paid for by employers, has boomed. In a survey of high school and college-age people by software firm Jobber last year, 75 percent said they would be interested in vocational schools offering paid, on-the-job training (WSJ).”

And this idea of blue collar career interest was recently discussed on the All In Podcast, which includes a group of prominent Venture Capitalists. They make a great point about the “premium of human service.” This is something that won’t be disrupted by AI; in fact, it could be a catalyst.

There is a role for government and investors here. We need more startups, funding and pro-business policies in traditionally blue-collar industries!

And I’ll go a step further.

What Happened to Home Ec?

Frankly, it’s a shame we don’t have Home Ec anymore. Teaching personal finance, woodshop, home repair, car repair (the mechanical part) and cooking should be required at every high school. A full yearlong class. And it often is not on the top of lists for parents to pass on to their kids anymore. Young folks just aren’t handy anymore. I took apart my TV (a few times, and the toaster) when I was 11 and after a little parental lecture, they encouraged it (this time with Goodwill appliances). We should all be teaching our kids (and other little family members aka nieces and nephews) this stuff too. It’s about thinking through problems, being resourceful, critical thinking etc… not necessarily that you will be a contractor (but it could be).

So I say, bring back Home EC!

My Skeptical Take:

The US economy seems to be chugging along well, at least for now. GDP is up 3% YOY, unemployment is historically low at 4% (and even better here in Nashville at 2.9%). Inflation is ticking down and is likely at the Fed’s 2% target, which we will see in hindsight. Prices for staples are down a bit from their high and their inflation has slowed considerably, particularly in gas and many groceries. It is true that home prices have never been higher, but this also means most homeowners have more equity in their homes than ever. An average of $300,000 in equity in fact.

Rates are on the way down, meaning Spring will likely bring a new wave of demand to the market and folks will look to refinance their home, taking cash out to pay for life needs, and also likely to splurge on new toys. This point should be emphasized. Fortunate homeowners will very much be flush with future cash. Equity in homes is multiple Trillions that people will tap in the next 12-18 months. This money will be spent throughout the economy.

I am Skeptical that the US economy will have a Goldilocks recovery in the next 18 months. Specifically, I am concerned that the relatively positive state of the current economy may be a lingering result of the stimulative drugs Uncle Sam slipped in our martini. Consumer spending is 2/3 of the economy and it’s hard to ignore the sheer volume of free dollars the federal government pumped, and is continuing to pump, into the economy. $10 Trillion dollars worth. Folks will spend those dollars. In addition to my point above on tapping trillions in home equity.

When the drugs stop, or at least abate, it will be time for the come-down.

Keep a Skeptical eye out. And it could be something international that sparks it. It is unfortunately a tumultuous time in many parts of the world.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-Andreas

Please Share this Article!

It takes several hours to write this weekly article, and they will always remain free. All I ask is that you share it with 1 friend. Just 1. If you do, you will get two gifts: free education for one of your friends, and good karma for helping to grow a community of folks trying to figure out a way to create wealth for their family.

* I write this myself and get it out for you all on the same day. Apologize in advance for the likely errata. Don’t have a team of editors, yet.

** The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and do not constitute financial advice.