All Forum Posts by: Dan H.

Dan H. has started 30 posts and replied 6359 times.

Post: Why markets with low appreciation grow your net worth twice as fast

Post: Why markets with low appreciation grow your net worth twice as fast

- Investor

- Poway, CA

- Posts 6,484

- Votes 7,543

Quote from @Sean Martin:

Dan brought this up earlier about a Dave Meyer thing… There has been this fallacy that lower appreciation markets have not appreciated anywhere near higher appreciation markets in the last few years.

From my personal experience, a property in Fayetteville NC I’ve owned since 2021 has appreciated 65 percent. Appraisal was just done. And there was no value add on this one. Only thing I did was add gutters and some cleaning at first!

Not saying this will continue in the future but even lower appreciation markets have seen some big moves since Covid!

The post I referenced had many historical low appreciation markets out performing many historical high appreciation markets. I forgot what the duration was but am almost sure it was more than a few years (i believe it was at least 5 years duration).

The issue is that when you span out in duration, the numbers depict the appreciation reality. events like significant wars, GFC, COVID, Great Depression each affect the markets slightly differently. These large events are not that rare and can have large effects on the appreciation if you use a short duration window such as 5 years or even in some cases 10 years.

Neighborhoodscout has Fayetteville NC has 9 of 10 over the last 2 last years (10.42%/year, total 21.92%) If you have 65% appreciation in 3 years you have far exceeded the market. Do you understand why?

However the appreciation over the last 10 years Fayetteville NC scores 5 of 10 (6.58%,not bad, not good). Over 10 years, Fayetteville NC scores 3 of 10 on appreciation, 3.38%/year which is poor.

This near term good appreciation may continue or it can be a transitory appreciation rate, only time will tell. If it continues, Fayetteville NC could become a high appreciation market.

https://www.neighborhoodscout.com/nc/fayetteville/real-estat...

San Francisco’s appreciation rate over the last 10 years is 1out of 10. The work from home bartered their appreciation. Are they now a low appreciation market.

https://www.neighborhoodscout.com/ca/san-francisco/real-esta...

My view is 5 years is definitely too short and 10 years, if it has a huge event such as Covid, GFC, etc, can be too short. I believe 10 years from now, San Francisco will have good appreciation over those 10 years but time will tell if my forecast is accurate.

Good luck

Post: Why markets with low appreciation grow your net worth twice as fast

- Investor

- Poway, CA

- Posts 6,484

- Votes 7,543

Quote from @James Hamling:

Quote from @James Hamling:

Quote from @Dan H.:

Quote from @James Hamling:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Quote from @Mike D.:

Quote from @Dan H.:

Case Shiller used to publish a list with total residential return for this century. The top of the list was all high appreciation markets. The bottom of the list was comprised of high initial cash flow properties. What the list showed was a strong correlation between appreciation and cash flow over a long hold. The list showed a poor correlation between long term cash flow and initial cash flow.

I invite you to run your numbers at 80% LTV using that extra down payment to deal with any initial negative cash flow. Use the appreciation and rent growth for this century on each city. Basically the case shiller data without the effort of determining local property tax, maintenance, PM rates, etc..

In have been investing in my San Diego market for many years. I have purchased with poor timing and great timing. My worse appreciating property has appreciated $2700/month over its hold ($47k down and closing). My best appreciating properties have appreciated over $10k/month over their hold. I suspect that virtually all residential RE in my market will have numbers between my best and worse case.

Knowing the San Diego appreciation rate (almost 6%/year for this century per neighborhoodscout) how do you think the rent growth has been?

With time the market with the higher rent growth will always have higher cash flow than the higher initial cash flow market that has lower rent growth. It is basic math,

So the high appreciation market has historically produced both better appreciation numbers and better long term cash flow than the low value markets. This is easy to verify and I believe most experienced investors ecognize this. I recognize past history is not necessarily an indicator of future performance but the metrics on my San Diego market still look promising.

My view is the low cost markets are best served by local RE investors who know the nuances of the area.

Best wishes

Okay, running the numbers at 80% LTV sounds interesting. If you do it for Austin, leaving all the other numbers from the initial example the same, you'd have a $2129 monthly payment on a 30 year loan with 7% interest, so -$14,296 negative cashflow. Since you are capturing the full appreciation on the property with a lower down payment, $80k, and since you now have larger principal paydown ($3251 in the first year), your return is now: cashflow -$14,296, principal paydown $3251, appreciation $28,000 = $16,955/$80,000 = 21.2% return. So far it looks good. So far.

And yes, you could now stick a very large amount of money in reserves to deal with the negative cashflow. Not sure what kind of rent growth you're proposing but let's say 5%. I used a spreadsheet that I had whipped up previously to figure out how much total you're going to need in reserves before the property starts cashflowing and was surprised to find that it still wouldn't be cashflowing after 20 years (!) and over those 20 years it would incur negative cashflow of more than $217k. The rest of the down payment you were going to put away in my example is only $145k, but that money grows at some kind of rate over the years so I suppose it would end up being enough to make up for all the negative cashflow this property would ever incur.

Even so, several large issues:

- The opportunity cost on the $145k is major. Since this is your reserve fund, you definitely have to keep it invested in something safe which will probably barely beat inflation. Let's be generous and say you make 5% on it. So, dealing only with the first year of doing this, you make $16,955 from the house and $7,250 from your reserves, or a total gain of $24,205 on a total investment of $225,000 or 10.8% return. Again, that's making several generous assumptions, and the return continues dropping year over year, which leads to the second problem.

- By the time your cashflow is inching closer to $0, your return on equity is bad, like below 10%.

- You are burdening yourself with negative cashflow for years when you could be in a different market with a higher return making cashflow which you can actually use to go to the grocery store and eat.

- Returns from appreciation are more volatile than cashflow in general and after going through this torture for years it is possible you could see very little payoff.

So, I don't see why someone would do this. I don't have access to the Case Shiller data you mentioned so I made some other assumptions that might be different. I'd also be interested in hearing if I misinterpreted something about what your idea was.

I agree with the thesis that high appreciation markets will eventually produce "better" (at least higher) long term cashflow because rent grows faster as well, but it takes a very long time and comes at the cost of low return on equity, to the point that you'd be better off selling out and going into other investments such as a stock/bond portfolio. You also have to consider the opportunity cost in the years when you're waiting for the cashflow to materialize.

I do not know if you switched numbers from your OP or if your calculation on time span to positive cash flow is off.

You show a negative $328/month on $2200 rent.

Without compounding (with compounding it would be better and take less time to achieve positive cash flow) using your rent growth percentage

1.05 ** years * $2200 - $2200 is the rent

at 5 years

1.05 ** 5 * $2200 - $2200 = $607.82 which is likely enough greater $328 to compensate for expenses other than P&i having risen (basically inflation on the non fixed costs).

>Since this is your reserve fund, you definitely have to keep it invested in something safe which will probably barely beat inflation. Let's be generous and say you make 5% on it. So, dealing only with the first year of doing this, you make $16,955 from the house and $7,250 from your reserves, or a total gain of $24,205 on a total investment of $225,000 or 10.8% return. Again, that's making several generous assumptions, and the return continues dropping year over year, which leads to the second problem.

There are many ways to manage risk. I believe high diversification reduces risk. I think only a very conservative investor would have more than a year of safe, liquid reserves (money market, etc). So your reserve scenario does not match most investor’s approach. I do agree that the reserves should not all be in one asset class; that is too risky. But an investor has a year or so liquid and substantial other investment in other classes besides RE, they have a more robust plan than someone relying solely on cash flow.

>By the time your cashflow is inching closer to $0, your return on equity is bad, like below 10%.

what ends up typically occurring is money is extracted before is gets to a 50% LTV to leverage the capital elsewhere reverting the cash flow. I virtually always have used 30 year fixed loans once stabilized for their safety but I have yet to hold a loan 10 years. With the rate increases that started q2 2022, there is a chance that I will finally hold one of these loans over 10 years.

My worse appreciating property has appreciated $2700/month over its hold. It never had negative cash flow but even if it did, it could not impact the return significantly. I purchased for $47k out of pocket including closing costs. My best appreciating properties have appreciated over $10k/month over their hold. One of these did have initial negative cash flow at purchase (quite large negative cash flow), but in less than 3 years it had positive cash flow. The negative cash flow was always inconsequential compared to the value increase.

I do believe the low cost markets are appropriate for local investors. Long distance investors should seek higher quality assets.

Good luck

Hey Dan, so when you say the cashflow goes positive in the fifth year, something is off there. You must not be using the new P+I for 80% LTV--it's $2129 and there's more than $14k negative cashflow in the first year. So, an extra $608 a month doesn't come close to smoothing that out. Some wires got crossed somewhere.

It seems that a sophisticated, very wealthy operator could possibly implement your strategy--say they had some stream of cash from something else that they didn't need and could funnel into this, removing the need to keep reserves--but for the average person, even the average millionaire, it would be insane. You suggested keeping reserves, but I suspect that if you yourself use this strategy you are doing something different.

I guess I should have said my strategy is not for billionaires!

>Some wires got crossed somewhere.

possibly. In the original post you indicated -$328 cash flow under Austin. Was this not correct? Was it a subset of the cash flow? Maybe there was a typo. It is the number I used.

In San Diego it is common to see projected rent to selling price ratios of ~0.5%. However, these are not typically what is being purchased by investors or if they are it is because they plan on doing a rehab and significantly raising the rent (a value add). The purchases that have those ratios without the value add and a projected rent increase are virtually all OO purchases. I suspect this is the case in virtually all lower cash flow markets. I have never purchased in my market without at least a projected 0.7% stabilized monthly rent ratio, including the cost of value add in the property cost. Since the rates increase, my underwriting shows 0.7% ratio is cash flow negative at high LTV in my market (while being far superior to the rent ratios that would occur on OO purchases).

I question if your large negative cash flow is mostly derived using stats that include OO purchases. I know if this was done on my San Diego market, it would depict a far worse cash flow than the already bad cash flow that investors are obtaining. I find it unlikely that Austin investors are regularly purchasing investment properties that project negative $1,167/month cash flow (even though my last purchase my underwriting showed a little worse than this per unit (4 units), but it had value add and positive cash flow was achieved in less than 3 years).

Do you believe Austin RE investors are buying at a projected negative $1,167/month? I think it is unlikely.

I will also point out that if I purchased in my market a property that was negative $1,167, my worse monthly appreciation property is $2700/month. $2700 - $1167 =$1,533.00 monthly return not including equity paydown and that is my worse monthly appreciating property. My best is up ~$1m in 3.5 years. $1m/40 is $25k/month (by the way it is the same property that had the horrendous cash flow at purchase that I mentioned earlier in this post). Tough to make $25k/month in cash flow with less than 5 units.

by the way my underwriting does not show those cheap markets to have cash flow anywhere near the projections of those investing there. In general the investors grossly under estimate maintenance/cap ex, do not depict anything for PM and sometimes grossly under represent vacancy/uncollected rent. I saw a post recently that showed $86/month maintenance/cap ex and a vacancy rate of one quarter the city’s vacancy rate. The $86 was 10% of rent and is at least a factor of 3 low for sustaining maintenance/cap ex on that unit. I asked where he got the number and got an initial reply that he had calculated it via cost and lifetime. It was clear he used 10%. I called him on it and did not get a response. I asked how he justified using vacancy of 25% of the city’s vacancy rate and got a reply that he was in the suburbs with lower vacancy. I believe he could have lower vacancy, but 75% lower seems unlikely. Certainly it seems to be very aggressive underwriting. I pointed out he had no entry for uncollected rent so his 5% vacancy was covering both. This is the quality of the underwriting I see regularly in low rent markets. This under writing is unlikely to be sustainable over any reasonable length hold.

There are challenges in RE everywhere and I believe those in low cost markets should start there (but in the upper half of the price range of that market). I do not believe these markets are likely to produce the returns that OOS investors seek.

Good luck

Hey Dan, I found the mistake here--the $328 is the *annual* cashflow for Austin. Everything I've written is with that in mind.

I understand that basically what you're saying is that an investor in Austin is unlikely to buy a single family home in that price range. I don't know about the logic of other investors--I've seen people on the board buying houses like that--but that would be my logic as well. So if you want to redo both examples using small multifamily, that's fair, but I think you'll find the same principle applies. Comparing apples to apples, the small multifamily property in Memphis is going to have a much higher rent to selling price ratio than the one in Austin, and I don't think the scale of the return of the Austin property to the Memphis one would change much.

I know that your underwriting shows that investing in cheap markets is very unprofitable--we've discussed that before. On my actual investments, which are small multifamily in the Midwest, I get about $100 a month per unit in maintenance and capex, so a duplex would have about $200 a month. The $86 seems low to me but it's not wildly off. I'm basing this on actual records I keep for my own investments using several years of data. I'm not sure about the way that most people invest because the way most people invest is probably irresponsible, honestly. There are plenty of people who buy junk turnkey properties from lying, cheating providers and lose their shirts.

My point about the investment that's -$1167 a month is this. It's not suitable for most people. If they have to keep reserves, like I said before, it creates way too much idle cash and the overall return on the reserves + the property itself is low, making the investment unattractive. If they have an income stream say from a company that they want to funnel into that to deal with the negative cashflow, okay, sure, that person is at a level where what I'm saying no longer applies.

>Memphis is going to have a much higher rent to selling price ratio than the one in Austin, and I don't think the scale of the return of the Austin property to the Memphis one would change much.

On day 1 yes. The case Shiller data showed over long holds the cash flow to purchase cost was highest in the highest appreciating markets. The BP released data that was much shorter in duration (i believe it was an 8 year span) was showing the trend. For example in the 8 years San Diego went from a poor cash flow at purchase to having a total cash flow somewhere near the middle. The cash flow in those 8 years was near the middle. The appreciation was near the top. A longer time span on that BP data would have shown continuing improvement of the San Diego cash flow. The math shows the higher rent growth market will have the better cash flow with time.

>my actual investments, which are small multifamily in the Midwest, I get about $100 a month per unit in maintenance and capex, so a duplex would have about $200 a month.

Using actuals does not accurately reflect future cap/ex. Large cap ex have long lifespans. How many sewers have you needed to replumb? Kitchens replaced? Roofs replaced? Fences replaced? Etc. Even the electrical and hardscape have a lifespan. I guarantee you did not get this $100/month using lifespan and replacement costs on all items associated with the property (true sustained maintenance/cap ex costs). $86/month (and your $100/month) is way too low if allocating sustained costs. I invite you to create a spreadsheet to determine your sustained costs. In my market we have more costly water heaters (low NOX) and high labor costs. It is $1600 to replace at reasonable cost (some plumbers charge a lot more) which I suspect t is quite a bit more than your market. 1600/10 (my expected lifespan in years)/12 (months in a year). The cap ex on the water heater is $13.34/month in my market. Note including the maintenance it is a little higher as pilot lighting, thermostat coupler replacement, occasionally replace a burner under warranty, an anode replacement, etc. do this on all items including the supplied appliances and yard and you will see $100 is way too low even if that is based on your current actuals.

I believe your cash flow projected numbers are very incorrect because I believe you included all the OO purchases in your average purchase price and only the rentals in your rent points. OO in general are larger and more costly by a wide margin than the average rental. If these OO properties were actually rented, it would drive up the average/median rent. So question is how did you determine the average cost of RE purchase? Am. I correct that it includes all the OO? Then recognize the volume of OO versus investor purchases and OO would skew the numbers further. I suspect virtually no Austin RE investor is purchasing projecting a stabilized $1167/month negative. As indicated, I recently purchased a property that at purchase had large negative cash flow. My stabilized cash flow was slightly positive if rents were flat. I just finished stabilization ~6 months ago. My stabalized rent on my underwriting without any rent growth was just over $15k. With rent growth $17.4k and increasing with each tenant renewal.

I do not believe anyone is using your reserve model (including those without income stream to supplement the negative cash flow) but I will admit some (maybe many) are using a reserve model that may be aggressive. I keep less than 1% of my networth liquid. However I am diversified into 3 very Different asset classes and the stock asset class is diversified within stocks. I have little liquid compared to my RE holdings. I guarantee that I am better able to survive a GFC type event than a very large percentage of RE investors. I recognize not everyone can diversify into 3 different investment categories to diversify risk but they are not keeping liquid reserves that cover all negative cash flow until they achieve positive cash flow. My belief is if they have diversified reserves (not necessarily liquid) to cover no income for a year, they are far better prepared to weather a GFC like event than most RE investments.

The historic data is clear that the high appreciation markets have out performed the cheap markets (the case Shiller data clearly showed this, the BP data was on its way to showing this) . It is why you are getting such push back from experienced investors. The question is what will occur going forward. No one knows but I believe in general the high appreciating markets will continue to out perform the cheap markets.

good luck

Let me get started with a key point that this discussion has been helping me to formulate: it can be said that high appreciation markets outperform less expensive ones based purely on appreciation and rent growth, but it's a moot point. The key thing this does not consider is use of leverage. A small investor can generate a higher total return in low appreciation, high cashflow markets by using leverage.

Now I'm going to go off topic. I've had this discussion (about my capex and maintenance numbers) before on the board with others. Again, OFF TOPIC. I like discussing things like this so I will do it but it does not affect my examples either way. Nobody said my capex and expenses were low in the examples, because I used higher numbers that I know are more typical.

My accounting isn't sloppy. I've had this pushback from several people, so I'm starting to understand that my numbers are unusual. $200 a month (actually I'm at a hair more) is not fake or wrong. I'm confident this can be replicated, at least doing things the way I do it. And yes, just to see if I'd had an exceptional run of years, I have separated out the capex, assumed everything is going to break on the typical schedule, plugged in the prices I pay for those things, and it comes out the same. So what it comes down to is I'm paying less for that stuff than what is typical. I rarely do any maintenance now, but at one time I did all of it so I know how to do stuff. I use people from Taskrabbit, who are extremely affordable, as well as people I know, and I don't let my management company do a single thing. I have systems for checking everything they do and making sure it's up to standards. So, I will come right out and say I get that these numbers are not *typical* but they are *possible*, because I am getting them right now. If you are laid back and a little sloppy then maybe it's double? I don't know. That's all I can say about it. Again, before somebody jumps down my throat, this is *not relevant* to the concept at hand. OFF TOPIC OFF TOPIC OFF TOPIC. Nobody said my examples were wrong because I didn't use my numbers but ones that are more typical. We are not talking about the larger concept. Okay, that's over.

So again, for sure, the high appreciating markets *will* have the higher cashflow over time, but with lower total return. Then why stay there?

Honestly, I don't say people can't use appreciation markets to power their purchases of cash flow properties. I'm sure that's worked for many people. But the fact is that, given you can get a higher return on your equity in low appreciation markets, all other things being equal, you'd might as well do everything there. I mean do you want an 11% return or a 23% return? Take the 23% return, don't spend the cashflow and use *that* to buy more cashflow. It may be an unusual way to do it but nobody has shown that it won't work. Why not think outside the box a little? I definitely wanted to hear from experienced investors and that's why I posted this. What I'm generally hearing is a few assumptions need to be tweaked but I think the majority of people have said, if grudgingly, that the concept seems valid. Believe me, my sincere intent is ultimately to learn. This is me forming my own investment approach, and if I can find a way to do it better, or if someone corrects me, I'll change direction. I don't mean just "you are so misguided you are a fool you are an xyz"--I don't care about that if there's nothing to back it up. I care about investing well.

My theory about where a lot of the pushback is coming from? This isn't how institutions do it. So everybody looks to the level above them thinking they should be doing it that way, without realizing maybe they *shouldn't* be doing it that way. Institutions have swayed markets and set cap rates to their standards, but small investors with leverage can go to markets they don't go to and make money. Ultimately the proof will be in the pudding. I am using this approach--it's been working fine---and I plan to keep using it. I thought about buying some property in Phoenix or Nashville or somewhere and rejected the idea for the exact reasons here. The return on investment/equity is just lower with the amounts you'd have to invest to cashflow, and I don't want to take on negative cashflow. So why go there?

I think that what you are edging around saying is maybe the biggest possible objection to this approach and the best argument in favor of high appreciation markets. If you do *value add* there, they can take you somewhere. So I will agree, for someone who is reasonable and not just a crowd-follower and actually looking at their numbers, they'll realize they *shouldn't* buy the house in Austin that I used in my example, like you've been saying, and they'll do a value add project in Austin instead. There is absolutely no reason for a passive investor to buy that house. Or, all other things being equal, anything in Austin at all.

Yeah, so now I see you're saying that you wouldn't actually use reserves in that way. Agree with the approach to reserves.

> it can be said that high appreciation markets outperform less expensive ones based purely on appreciation and rent growth, but it's a moot point. The key thing this does not consider is use of leverage. A small investor can generate a higher total return in low appreciation, high cashflow markets by using leverage.

I am 100% missing what you say here. I can get the same LTV in both markets (excluding the real cheap stuff that is hard to finance). I can more easily get equity line of credit on high value assets. My cost to extract (closing costs) is lower as a percentage on high value assets. I cannot think of one way that low value assets are easier to leverage. I cannot think of a few ways high value assets are easier to leverage.

> I have separated out the capex, assumed everything is going to break on the typical schedule, plugged in the prices I pay for those things, and it comes out the same. So what it comes down to is I'm paying less for that stuff than what is typical. I rarely do any maintenance now, but at one time I did all of it so I know how to do stuff. I use people from Taskrabbit …

I invite you to post your lifespan and costs on these cap ex items into this thread. A tad over $200/month is not including all sustained expense. The most recent I did was interior only (condo). It was a new market to market to me, I ran my numbers by @Pete Appezzato (with STS/Exp) and incorporated his feed back. My interior only number was significantly higher than your total cost. In my market I have dedicated maintenance staff and my small attached unit maintenance/cap ex cost is $300/month. Detached is higher.

>The return on investment/equity is just lower with the amounts you'd have to invest to cashflow, and I don't want to take on negative cashflow. So why go there?

I think the market is much more challenging than prior to q2 2022. I agree with you comment at purchase. Historically your statement valid in high appreciation markets in incorrect as the hold length increases. In general it takes active value add, patience, a sophisticated value add, alternative financing, or a far below value purchase. I understand high appreciation markets not being ideal for everyone.

>fact is that, given you can get a higher return on your equity in low appreciation markets, all other things being equal, you'd might as well do everything there.

Historically the cheap markets has not produced a better return on equity. Case Shiller showed this. Unless you have as reputable source that shows otherwise I view it we know what has done better historically. We do not know what will do better going forward. I view it similar to growth versus income stocks. Note if I purchased Amazon circa 2000 it was losing money but its valuation was far above Barnes and noble, many if not all of the large car manufactures. Why? Growth potential. One needs to evaluate ROE, but not primarily against its cash fliw (doing so would be compare to an income stocks but it is more akin to a growth stock) but against its overall projected returns just as you old do for a growth stock.

>Ultimately the proof will be in the pudding. I am using this approach--it's been working fine---and I plan to keep using it

I think you can do fine anywhere. However you indicated build your net worth twice as fast as an appreciating market. I will offer you to pick any one of my San Diego area purchases from my profile or either of the two acquisitions I made in Dec 2021 that are not in my profile. I will provide price, down, current value, current rent. I will include appreciation per month of hold. It will give you something to view what I have obtained in my high appreciation market. I have already indicated my appreciation on hold varies from a low of $2700/month (total out of pocket including closing costs was $47k) to almost $25k/month. This is what is possible in high appreciation markets.

>someone who is reasonable and not just a crowd-follower and actually looking at their numbers, they'll realize they *shouldn't* buy the house in Austin that I used in my example, like you've been saying, and they'll do a value add project in Austin instead.

even though I have requested it, you have not provided how you obtained the value of the investor purchase in Austin or elsewhere. I believe you included all the OO purchases in your property value and that your calculations regarding initial cash flow are very inaccurate. I hope you can see how this would skew the numbers. If I am correct that you used all the OO purchases in property purchase price it would explain how your calculations on cash flow are so absurd. People seldom purchase the highest priced homes as rentals. The properties investors purchase have to make sense as investments. Virtually no investor would purchase your Austin example property, suggesting that is what investors are purchasing to make your case is faulty.

a lot of successful investors have indicated their experience is your hypothesis has historically been false (also indicated by the Case Shiller data and the BP data was going in that direction).

This does not Imply what the future will hold. It certainly does not imply that you cannot do well being a smart investor in a high initial cash flow market. I personally think most RE investors are best served by investing in a market close to them which is what you have done.

I question if at this point you still believe your hypothesis. I really do not see how someone with an open mind would still be pushing that hypothesis.

Good luck

Hey Dan. Yeah, I believe this, lol.

Anyway, my first paragraph is referring to the return on equity being better in less expensive markets. I know you go into major negative cashflow in order to capture appreciation that is (or at least has been) high in San Diego, and I don't dispute that this can be done profitably, if you can stomach it, though the volatility is very great and it's not for everybody. Part of my premise was that you wouldn't go into negative cashflow. So, assuming you put down enough to cashflow in say San Diego and also in Memphis, the amount is much larger in San Diego, right? Not only is it larger, it's a larger *percentage* of the property's value. Now, assuming modest appreciation, calculate the total return on that down payment, including cashflow, principal accumulation, and appreciation. Unless you go into negative cashflow, and I understand that you personally do do that, the return as a percentage is always greater in the less expensive, higher cap rate markets. It doesn't matter that the appreciation is less. That's basically just me restating my first post.

Now, we're going off topic again, but I'll go there. I'm just marking this paragraph off again. This does not have to do with my main point and has to do with Dan's questions about my capex numbers. Let's get a rough cost per unit on major capex items for a duplex in the Midwest. A roof lasts say 25 years, right? I expect to spend around $9k for a roof and that covers two units so that's $180/unit/year. A water heater might last 12.5 years and I can get one for $1000. $80/unit/year. Furnaces last maybe 17.5 years and I can get one for $2k. $114/unit/year. Appliances, I do end up replacing them a lot. That probably averages $100/unit/year. Windows? Honestly I have seen windows last 100 years and I rarely replace them. I have never had to do any foundation work. Although flooring, paint, kitchen and bathroom items are technically capex I factor them into turns and I gave those expenses separately. So, adding up all the capex expenses I just gave, we're at $474/unit/year, so just under $1k for a duplex. I don't have time right now to do this in totally granular detail but that will give you a rough idea of where this number comes from. Again, I am a major cost cutter and this cannot be achieved without effort. If you just call some contractor you could easily pay double or more for all this stuff. I'm buying used appliances, I have an affordable HVAC guy, etc. I have the feeling that most people invest in what to me is a very lazy way. With a few phone calls, and also by building relationships over time, these numbers are possible in the Midwest.

I would like to see the Case Shiller information you are mentioning. I think it must be showing returns assuming that everything was purchased in cash. Of course appreciation rates are higher in low cap rate markets and they've been valued the way they have because institutions purchase them with low or no leverage. Are they really showing return on equity using leverage? I'd be really surprised if they're doing that and showing high appreciation markets come out ahead. The math shows they don't, and anybody can duplicate that math. Why wouldn't it be fair to include cashflow in ROE?

Yes, sure, I'd like to see the numbers for a San Diego purchase. Is this a passive investment? Because if we're talking value add, that's outside what I'm talking about. I'm sure you can do well if you are actively involved. But that's a different ballgame.

How did I obtain the value of the investor purchase in Austin? By looking at the MLS in Austin and seeing what a modest single family home costs. I think my projections of revenue are close to reality, however this is a market that I don't invest in so I don't claim it's perfect. It can be confirmed by going on realtor.com, looking up some modest single family homes on the MLS, and then looking up rental listings for the same. I think you will find my example is reasonable.

Again, no doubt appreciation and rent growth is higher in Sun Belt markets, but if you can't capture that gain without putting down tons and tons of money, your overall return as a percentage is lower. And who doesn't want the higher percentage? All other things being equal.

>Part of my premise was that you wouldn't go into negative cashflow. So, assuming you put down enough to cashflow in say San Diego and also in Memphis, the amount is much larger in San Diego, right? Not only is it larger, it's a larger *percentage* of the property's value.

I now understand what you were saying. However, I am unsure even at the lower leverage point that historically the higher appreciation markets still have not out performed the lower appreciation market. Let's for example use San Diego (5.74%) versus Detroit (1.98%) or Cleveland (2.45%) for this century (source neighborhoodscout). If I put double percentage down so 60% LTV versus 80 LTV my gain as a percentage from appreciation has still out produced them and my cash flow due to higher rent growth has out produced them. So thinking the ROE is worse even with less leverage is certainly not universally true.

However the mathematics of using a lower LTV to increase initial cash flow is poor in higher appreciation markets. This does not stop people from suggesting it and maybe some less experienced investors choosing it without a full understanding of the numbers.

Your cap ex items is missing a lot of items such as kitchens, bathrooms. Also my market only has windows close to 100 years if the property is classified historic. Those old windows need a lot of maintenance and would be cheaper if they had been replaced by vinyl. Fencing, landscaping. Sewer. Electrical. Knob and tube. Fused breaker boxes. Virtually everything on a property has a lifespan.

All cash purchase would reduce the appreciation benefit. It would hurt the high appreciation markets more than the low appreciation markets. The case Shiller data used high investor leverage in the calcs but it did not matter as the 3 top cities were all near the top in cash flow since the start of the century (they would have been real high on the list based on their rent growth) and near the top for appreciation. San Fran was the top city at the last data I saw but its appreciation took a hit when work from home increased (so I do not believe they would be the top today).

Here is an example of why the appreciation markets have outstanding cash flow if there has been no extraction of value. San Francisco's average rent in year 2000 was $977 (not sure of number of BR). Apartments.com lists current 2 br average apartment as $4218. Note SFH are mush higher.

$4218 - 977 =$3,241.00 month increase of rent

$3241/25 =$129.64 average annual increase. In reality it started with lower than this average and has been higher than this average recently.

Clearly a 2 br apartment unit purchased in San Francisco in the year 2000 would have produced crazy cash flow without any extraction of value SFH would be far greater cash flow. You could do this with any of the cities with high appreciation numbers for this century and you would see the same thing It is because there is a tight coupling of long term cash flow and appreciation. There is not a strong coupling of long term cash flow and initial cash flow.

>Yes, sure, I'd like to see the numbers for a San Diego purchase. Is this a passive investment?

I have one property that had no upgrade value add (I do not consider residential RE passive but this has been about as passive as it gets, one unit has turned twice, 3 units have original tenants).

Purchase in Dec 2020 for $640k including bird dog fee ($625k + $15k birddog fee). I used 80% LTV at 2.75% (I wish this was still available), 30 year but including bird dog fee would be a little lower than 80% LTV. Quad in Escondido. Worth ~$1.5m today (look at current quad values in Escondido, over 3700'). PITI $2982. Market rent $8725. Using 40% expense ratio w/o principle, cash flow $3,395. including principle pay down $4,468/month. Gain from appreciation $1.5m - $640k = $860k. $860k/55= $15.6k/month of appreciation. note rents are not high enough to achieve this return via cash flow even if 0% LTV. Note my birddog fee and down together was $148k. I do not remember the closing costs but I did not pay any points to get that loan.

I am not claiming this was an average purchase. If you look in my profile, I think I referred to its rent ratio as a unicorn find for San Diego. A CA law that I knew about at purchase but was not yet reflected in pricing also allowed this unit to have appreciation far above the average even for San Diego. However, in general I have done BRRRRs. This is my non BRRRR purchase. It was my "passive" RE investment.

>How did I obtain the value of the investor purchase in Austin? By looking at the MLS in Austin and seeing what a modest single family home costs. I think my projections of revenue are close to reality, however this is a market that I don't invest in so I don't claim it's perfect. It can be confirmed by going on realtor.com, looking up some modest single family homes on the MLS, and then looking up rental listings for the same. I think you will find my example is reasonable.

I do not find that method as reasonable. It is heavily factoring in OO purchases (what percentage of SFH do you think are OO purchases versus what percentage are not OO purchase?). I think this method would provide a misleading number in every market, but especially high priced markets. You use a property price that includes OO, but the rent is only of rentals. In general, the OO properties cost a lot more than what RE investors would pay and in general are nicer OO properties would rent for more than the average rent driving up the average rent. it is, however, what I believed you had done and why your negative cash flow estimate was as large as it was and likely worse than any investor would tolerate.

>no doubt appreciation and rent growth is higher in Sun Belt markets, but if you can't capture that gain without putting down tons and tons of money, your overall return as a percentage is lower.

If an RE investor chooses to use a lower LTV, it will impact their return. Even with the lower LTV, some high appreciation markets would still out produce some (many?) low appreciation markets as my examples showed. More importantly it is the investor's choice. Maybe they sleep better knowing rents cover all expenses. My last purchase I went max LTV even though using my numbers showed ~$5k/month negative (I had no problem sleeping). This was a value add and I knew that the negative cash flow would not last long. It now (3.5 years later) has decent cash flow (rent $17.6k, P&i ~$6.9k, piti ~$9.5k). It is also up in value almost $1m above purchase and value add costs. This was a value add, so not passive.

Good luck

Hey Dan, I went into this math in detail in my first post, but I doubt that 60% LTV is going to be enough to cashflow in San Diego. It certainly would not be enough in most cases today and I doubt it would have been in the past either. I have played around with these numbers quite a bit and believe that what I said in my first post is sound. It gives the example of a high cashflow, low appreciation market vs a low cashflow, high appreciation one and shows how return on equity is greater in the first, when both markets are paid down enough to casfhlow a tiny amount. Yes, the mathematics of using a lower LTV to increase initial cashflow is bad, so if you're going to do it, you have to go all in and deal with insane negative cashflow. Apparently you do this. I understand it can be done, but if you are setting aside enormous amounts of reserves for this you need to consider how much money you're keeping idle. The opportunity cost is extreme. On the other hand, if you are fortunate enough to be in a position where you have a lot of cashflow you don't spend or need for anything, by all means do this.

I included the items you mentioned--kitchens, bathroom--in turns. A turn is technically pretty much capex, except for cleaning and trash out, but all this does is shift numbers from one column to the other. The ultimate return doesn't change. I think we're kind of quibbling over small stuff now. I don't believe there are any large holes in my numbers.

Yes, I know high appreciation markets can have great cashflow if you let them sit for years and years because they have high rent growth. But go ahead and calculate the return on equity in those situations. You have so much idle money sitting there that the return as a percentage is probably not beating the stock market. James had an example like this of a class A property that he's getting good ROI on, but not good ROE. Part of what I'm pointing out here is the importance of return on equity. If your return on the equity you currently have in a property at any given point in time is not beating the stock market, that would be a pretty strong indication that you might want to pull that money out and do something else with it. I guarantee by the time you have crossed the line into great cashflow in a high appreciation market that your return on equity is low. I would not be motivated to invest in this way. Owning a property is a big administrative burden at the least. Even if it sits there and cashflows and appreciates, if your money is making 5-10%, why would you want to do that? I know there are many people who do.

About your Escondido property, you must have gotten an incredibly smoking deal on the purchase price and it wasn't natural market appreciation which as far as I know in Escondido was nowhere near that. The numbers you mentioned would mean 20% market appreciation if that's where the gain came from. However it was achieved, here's the problem, that's looking back into the past. You told me yourself you're currently underwriting with flat appreciation over the next few years, but let's say it's 2% and calculate the return on equity now. The monthly appreciation would be $2,500 and you said cashflow and principal paydown together are $4,468 a month. That's a total of $6,968 a month or $83,616 a year. Given that your equity is around $900k, that's a 9.3% return on equity. Have you calculated that and are you happy with it? Then by all means proceed. But what my post was about was that far greater gain than that can be gotten in high cashflow, low appreciation markets.

Prior to q2 2022 it was fairly easy to find cash flow positive purchases in San Diego. They did not have day 1 cash flow comparable to the cheap markets because investment markets are efficient and build in items like expected appreciation, expected rent growth, risks including tenant risks, but they had positive cash flow. I have only purchased one property that projected negative cash flow at purchase. Its value is up ~$1m in 3.5 years and has modest cash flow.

No smart investor handles the negative cash flow by having cash reserves that get them to the cash neutral state. I keep saying this but you keep acting like this is how investors handle this risk. It is as absurd as the subject of this post.

Your calculation for return on equity is not one that anyone uses. IRR, COC, etc projections all use the future projected returns and not solely the initial returns. So your ROE calculation is very flawed and why you have a mistaken belief on which market has historically produced the better ROE. What do you call your ROE calculation that does not use any projection of future returns? An IRR calculation going back in time on pretty much any decent length calculation will show the high appreciation markets have out performed the low appreciation markets. Guess what! this is the same calculation as ROE at that time except is the actual return on the equity from that time (not a projection).

you replace kitchen on tenant flips? You replace bathrooms on tenant flips? You do new electrical on tenant flips? New roofs on tenant flips? I offered to look at your spreadsheet of lifespan and costs. I claim $200/unit is not near enough if allocating for sustained maintenance/cap ex on all items. Show me a spreadsheet with the costs and lifespan of all items that depict this. The last one I did was interior only on an away market (so not using my staff) and it was ~$300/month and I incorporated the inputs from an agent in that market. Low rent markets have a higher expense ratio than higher rent markets. Your maintenance/cap ex is higher as a function of rent.

you keep going back to cash flow as though it is the only source of return. I have positive cash flow on all my properties and all but one (maybe 2) always projected positive cash flow but it does not matter. I could have had negative $1k/month of cash flow over the hold and my irr if I exited would be outstanding. This is because my lowest appreciating property is $2700/month. If I subtracted $1k/month off it would be $1700/month return on an initial investment of $47k. Note this is my worse. I have at least 3 properties with over $10k/month of appreciation over their hold. Not sure you concentration on cash flow as the source of return. The reality however is the high appreciation istion markets historically have the higher cash flow because of the tight coupling of appreciation and rent growth. Look at the San Francisco rents I posted. $3200/montn of rent growth this century ensures that San Francisco has experience better cash flow than any low appreciation market that you can find. I challenge you to find one. And if you thing San Fran is an outlier, look at San Diego, NYC, LA, Boston, etc. they all had better cash flow for this century than the best low appreciation market you can find assuming no cash extracted.

>About your Escondido property, you must have gotten an incredibly smoking deal on the purchase price and it wasn't natural market appreciation which as far as I know in Escondido was nowhere near that. The numbers you mentioned would mean 20% market appreciation if that's where the gain came from. However it was achieved, here's the problem, that's looking back into the past. You told me yourself you're currently underwriting with flat appreciation over the next few years, but let's say it's 2% and calculate the return on equity now.

I got a good deal, but there was a state law that had already been signed but that was not yet reflected in pricing that also contributed to this properties appreciation.

>The monthly appreciation would be $2,500 and you said cashflow and principal paydown together are $4,468 a month. That's a total of $6,968 a month or $83,616 a year. Given that your equity is around $900k, that's a 9.3% return on equity

your calculation on roe is not a standard calculation as roe project the future projections. The roe calculation is correctly done as though you purchased the property today with the existing financing at the current LTV (meaning LTV today) . It includes the expected appreciation and expected rent growth (ideally with conservative numbers). You are correct for the last few years I have been using 0% appreciation for 5 years due to my desire to be conservative and my near term uncertainty. I have been using 5% at year 6 onwards in my market which is 0.75% lower than my market appreciation. I have been doing rent growth also conservatively ay 3% annually even though 5% is close to historical for this century in my market. However, my ROE is calculated at 10 year, 15 years, and 20 year exits. Even with my hopefully conservative underwriting my ROE calculations are far above 10%. I would not choose RE investing if I was only projecting 10% return. That is virtually the same as the lifetime s&p500 which is much more passive. The return from REI must compensate for the work and risks. 10% (or 9.3%) is not nearly sufficient. In general I have achieve infinite ROI on my investment properties (all but 2). I demand my ROE be far higher than the S&P 500. On that Escondido quad it is far over twice as high (I recently ran numbers on this property for ROI and IRR was in the 70% a year if I exit in 10 years. It would be higher per year if I exited today implying the next 10 years are below 70% per year).

Good luck

I thought we were getting close to an understanding but there are some major misunderstandings of what I'm saying here.

I see that you want to use this San Diego example plugging in its increase in value as if it were market appreciation, but that's a false premise. You got a good deal and did something with this property that you haven't fully described to get its value to increase. If you don't want to calculate ROE based on a projection, then you can go back one year and we can assume that your value add was completed by then and you were then benefiting from pure market appreciation. As far as I can see, property values depreciated slightly over the past year in Escondido. There was no appreciation. We'll say somehow your place didn't depreciate, so zero gain from appreciation, I don't know what your cashflow was but I assume it's grown a bit so maybe $3000 average monthly, principal paydown should have averaged $1025 a month over the past year, that is all the gain you had and the equity was $900k. That gives you a return of $48,300 a year or 5.4% ROE. Imagine if you were calculating ROE, then your projection of no appreciation would have led you exactly to this number and you could have chosen to extract your capital sooner. Or were you happy to invest at 5.4% for the past year? If you were, good.

I'm sure your value add play, whatever it was, was good, but as a passive investment this doesn't seem that good to me and certainly does not rival what's available in other markets. I will make your argument for you more cleanly: you can get good returns in high appreciation markets through value add plays, and they can rival those available to passive investors in high cashflow markets. That's all you have to say, not try to use your value add gain as appreciation. It is very, very appropriate to calculate your return on equity at such time as your value add stuff is done. You could then sell that property and invest it in something else and that is a very important number that can show you when it would be advisable to do that.

I'll repeat that. If you are done with your value add or whatever you were doing and are now holding a passive investment, it is absolutely appropriate and even crucial to evaluate what its return as a passive investment will be using ROE. If the return sucks, sell it and either recycle your capital into another value add project or put it into a better passive investment. To be direct, I think you held this place too long and should get rid of it now. Of course, you're the one in charge of your own money and I'm sure overall you've done well. It's also not the case that you don't have blind spots, and you're being very direct with me, so I'm doing the same.

It doesn't bother me in the slightest if other people (that you know) don't do it like that. Dan, do you know that in kindergarten I insisted on holding my pencil in a way different than what they tried to teach and purposely wrote in all caps with many of the letters backward just because I wanted to? I knew exactly how I was expected to do it, read above my grade level and chose to do things that way because I wanted to. This is just the way I do things and I'm not an idiot like some people are trying to make me out to be. This type of thing has been going on a long time and I know people are threatened by people who do things differently and especially those who don't change when everybody makes a big fuss about it but I'm no fool and I'm doing this stuff this way for a good reason. It's very important for some here to think I have no experience at this and either don't have any actual investments or I'm going to go bankrupt tomorrow or a I'm an enormous fool. All that is false.

Several posts ago, you absolutely suggested using reserves to cover the negative cashflow on a high LTV investment in an expensive market. I think you realized after I laid the numbers out that that doesn't work. But go back and look at your post. I have never exactly been sure what you're proposing doing instead of reserves. You vaguely described diversifying in other ways. You haven't said how exactly, but there is surely an opportunity cost attached to what you are doing and I am interested in finding out what it is and if the return really is that good when those opportunity costs are taken into account. The return is also incredibly volatile and the volatility itself will lower the percent return in addition to simply not putting money in your pocket as reliably as cashflow.

I don't know why we're still going around and around about my capex numbers. I have enough properties and enough years on record that a kitchen is not going to implode tomorrow in a way I haven't accounted for. That is factored into turns. I gave you a list of major items and showed my numbers for them. If that isn't enough, then sadly that's how it's going to have to stay. I'm confident in my numbers and going deeper into them is going to be very time consuming and serve only to prove to you that they're right. They are right, and I'm sorry, I don't have the time to do it. If you want to think they're wrong, you can think so.

I do not assume cashflow is the only source of return and the fact that you're saying that at this point makes me think that a lot of what I'm saying is being missed. To repeat, factor in cashflow, appreciation, and principal buildup. Assume you're not going to take on negative cashflow and you're using enough leverage to barely cashflow. Calculate your return on equity (highly advise you start doing so now) in high appreciation and low appreciation markets. The latter will win.

To repeat, and it's not the first repetition, I know rent growth and appreciation are higher in high appreciation markets. This basic fact is not being disputed by anybody. Investors using leverage can gain higher percentage returns on their money in markets with better cashflow, simply because they can cashflow with less equity and therefore earn a much higher return on equity. It doesn't matter that cashflow and appreciation are better in NY, LA, Boston, etc., etc. Not unless you buy all properties in cash because you're an institution or someone with $100 million.

>You got a good deal and did something with this property that you haven't fully described to get its value to increase

I thought I explained it. I did nothing to the property. I knew a law had passed that would increase the value of this property. No effort, no value added by me (the value was added by the state legislature). My first protege recently had land values in its current use at ~$1m. He knew about a city law that made the property much more valuable with a different usage. He sold the land with a different use at $1.5m to someone that would use the land for its highest value. The city just (in the last month) changed the law to prevent what they legally were allowing and encouraging. He did nothing to improve the property.

In both cases we believed the value would increase due to laws passed. It is little different than a new NP is established by congress. You buy a little cabin just outside the park with the belief that the park will raise the value more than other areas. You could be wrong and would possibly lose transaction costs at worse case. If you right and the property outside the park appreciates double the rate it would have without the NP, you made a good investment.

I refer to these as sophisticated value adds meaning they are more about knowledge than work involved.

You are a little high on my principle paydown possibly because you included birddog fee into the loan but it was not) but a little low on my cash flow (but remember my expense estimate is far more conservative than you use). Oberall you are ~$300 low. Also remember I used 0% appreciation for last year in my ROE calculations before it was flattish in appreciation (my projection was fairly accurate). Not sure of your source showing it went down as most sources I see are slightly up, but flattish is fair. Even with that projection of zero appreciation last year, my ROE shows great (I do not calculate for anything less than 10 years). This is in part because my actual rent increase $395/month last year and because I show 5% appreciation starting in the future until end of time (until selling it). As indicated my lowest IRR was above 70%/year.

>Several posts ago, you absolutely suggested using reserves to cover the negative cashflow on a high LTV investment in an expensive market. I think you realized after I laid the numbers out that that doesn't work.

I did not. I did state to run the numbers using 80% LTV and using the money not placed into he property to cover any negative cash flow. 1) I did not state where this money would be held. 2) I certainly did not mean to keep all of it liquid. The numbers do work. I showed you in the last post even if I was $1k/month negative over the hold, my worse appreciating property still would have made $1700/month ($2700 - $1000) not including principle pay down or any tax benefits. My down and closing was $47k on this property. I did not need cash flow for it to have produced a great return. I have had decent cash flow on the property (and would have had good cash flow but equity was extracted twice from this property), but even with negative $1k cash flows month this return would beat many/most low appreciation markets.

>I have never exactly been sure what you're proposing doing instead of reserves. You vaguely described diversifying in other ways. You haven't said how exactly, but there is surely an opportunity cost attached to what you are doing and I am interested in finding out what it is and if the return really is that good when those opportunity costs are taken into account.

As long as the reserves are not placed in RE, you have diversified and reduced risks. there are literally infinite options, but having more than 6 months liquid reserves are very conservative and certainly not my recommendation. I did real well with mineral rights before I did well in real estate. Again it was a knowledge play as fracking was starting to be heavily incorporated but people were selling on valuations that did not include the production increases that could result. I went all in (except for home, job, and 401k, everything I had liquid and could borrow unsecured) but I had much lower amount as my all in back then. I believe their time has passed so this is not a recommendation to diversify into. Stocks, bonds, anything that is likely over time to beat money market. Money market is fine for near term reserves (I would not do more than 6 months, but different people have different risk tolerances).

>Calculate your return on equity (highly advise you start doing so now) in high appreciation and low appreciation markets. The latter will win

It has not and it does not. The historical data already shows the high appreciation iatiin markets have produced the far better return. You act like this data does not exist or you ignore it. I will admit past performance does not necessarily match future performance

We agree to disagreee on your maintenance/cap ex. I do have a question: are any of your units on the 2nd or more replacement of any large cap ex items such as roof, kitchen remodel, HVAC, etc?. This tells me if you have gone full lifetime on sustained costs.

>I do not assume cashflow is the only source of retur

You only used cash flow in all your ROE calculations. Your calculation method is not any industry standard that I ever heard of. Calculation of ROE still calculates into the return the growth (rent and appreciation) until the projected exit. You even did it when you calculated the ROE from my Escondido quad. It is not how roe is calculated. It was interesting the return without any growth it is almost 10%. That is crazy good. With growth, obviously that return is a lot better.

>Investors using leverage can gain higher percentage returns on their money in markets with better cashflow, simply because they can cashflow with less equity and therefore earn a much higher return on equity.

historically this has shown to not typically be the case. The data is there that shows this. When case Shiller used to publish their residential return for this century it showed the high appreciation markets in general fad the higher cash flow. And of course they had the higher appreciation. The BP data on residential return was much shorter in duration (I believe it was only 8 years) also was on its way to showing this as poor at purchase cash flow cities in 8 years had moved near the middle. By the way, for CA cities the BP data had a large mistake related to property tax that under calculated the cash flow.

>It doesn't matter that cashflow and appreciation are better in NY, LA, Boston, etc., etc. Not unless you buy all properties in cash because you're an institution or someone with $100 million..

I do not understand this statement at all. If you buy all cash the appreciation does not benefit from leverage. The leveraged investors benefit the most from appreciation and rent growth.

Where does it make more sense to purchase all cash, the low appreciation markets or the high appreciation markets? In the high appreciation markets they want to maximize the benefit from appreciation. This requires leverage. In the low appreciation markets, cash flow is the primary source of return. Cash flow is higher with less leverage.

By the way this is my last response in this thread. You keep bringing up items that I have already addressed. You have demonstrated you do not understand ROE or how to calculate it. My responses are sufficient to educate someone receptive to the concepts.

By the way I suggest virtually all REI to invest in a market they are intimate with regardless of if it is a high appreciation or a low appreciation market. This is usually their home market.

good luck

I'm exhausted of this circle-jerk and gonna put a nail in this coffin.....

Here is the facts of the math of things. What appreciation low, and high looks like, by the #'s.

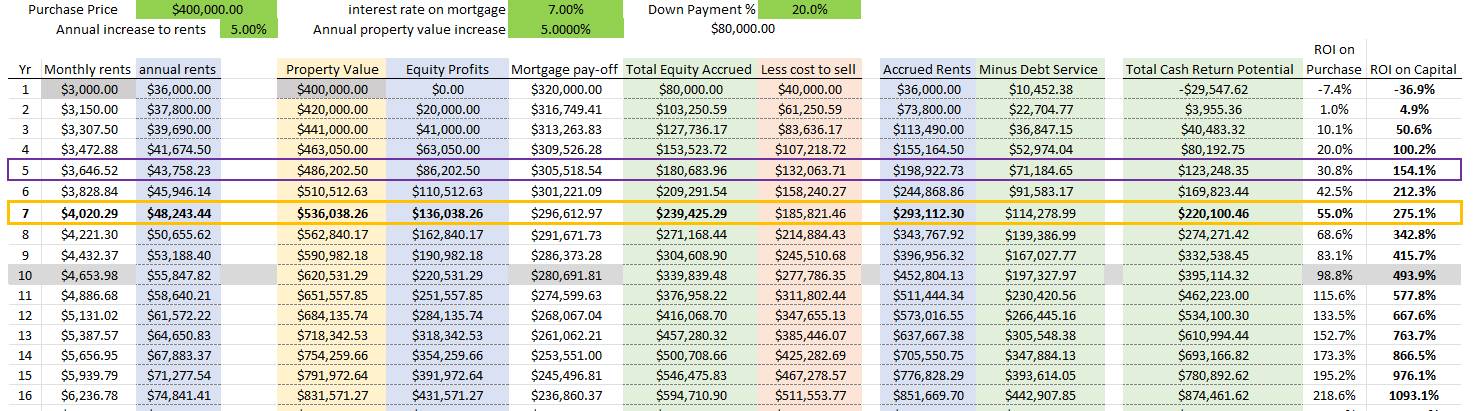

$300k property, appreciation at 2%. And let's keep in fantasy vein and say it's a 1% deal to start, rent's at $3k mnth.

Yr 6 your at an aggregate 200% ROI. Of course this is with 0 cap-x/maintenance but hey, it's fantasy land.

Now, vs appreciation which as Mike wants to compare, a HIGH appreciation market......

Same $300k buy, same interest rate, BUT were gonna drop rents to starting at $2,500 vs $3k and increase appreciation rate to a HIGH rate, 7%.

Now yes, I am more then well aware of the countless markets who've had 12 - 24%+ annual appreciation but let's see what just 7% as a "high appreciation" rate does......

Again, keep in mind we nerfd DOWN rents $500mnth (- 17%) in this.

Results???????

The high appreciating property is a 320% ROI in yr 6, that is a 1.5X return too the "cash-flow" property.

Yr 6 gross rents $42k.

Yr 6 gross rents of the "cash-flow" property are $39,746........

Yup, MATH, compounding returns, that's how math works.......

The appreciation property over-take the "cash-flow" property, as the cash-flow LEADER in yr6.

And after yr6 the appreciation property just keeps expanding and exaggerating that lead on producing MORE cash-flow then the "cash-flow" property........

So how is Mike so backwards on his assumptions? Simple, a person with experience of 1-4yrs would feel, FEEL as if their low-appreciating property is winning out, they just haven't realized yet.

Now the big X-factor vs the 2 asset types is if and when there is a major inflation event. As those of us IN the industry experienced with the covid-inflation, the well positioned properties caught the biggest impact of that inflation. I had properties that paced 20%+ annual rent increases for 3 years consecutively. It was bonkers.

The low grade assets, yes, they had big increases too but nowhere close to 20%, roughly half. Same goes for property values, they didn't catch those same gains.

Which is why Mike is buying those properties today at "cheap" prices and feeling, emphasis on FEELING, like he's a genius beating everyone else.

Those properties are "cheap" for a reason........ Mike just hasn't figured that part out yet. He will, in time, nobody can beat the realities of time.

It's the simple SIMPLE math of compounding returns. The one who compounds at a faster/bigger rate, will beat out the lower EVERY TIME. That's how compounding works.

---- More ? -----

Ok, let's say vs 2 "cheap" $200k low-appreciating properties, at 1%, vs an "expensive" $400k well appreciating:

The "cheap" returns $206k at yr 7.

The "Expensive" returns $296k at yr 7, starting with rents 75% that of the "cheap"......

That's a $90k difference in just 7yrs, $90k MORE one makes with the LOW cash-flow day 1 via higher appreciation.

What's $90k over 7 yrs? That's over $1,071 per month.......

Really want you mind blown.....

How about an answer on how to 10X your investment capitol, and this is at just 5% appreciation rate (keep in mind where fed rate has been around, nearly 5% right.....)

also keep in mind this is starting at a rent of just $3k on a $400k property, that IS cheap, very very cheap in my markets. Stupid crazy cheap to be honest.

With S&P compounding at a 12% annual rate your $80k would turn into $248,467.86 over 10 years.

Via "poor cash flow day 1" high quality Real Estate assets in well appreciating markets averaging just 5%..... $395,114.32 yr 10......

I don't know about you but averaging 5% annual appreciation is VERY attainable where I am positioned. Last few years have been double digits annually meaning things could sit flat, dead flat, for years, and still hit that 5% annual average. Do you seriously think well positioned properties will appreciate 0% over next 5 years? Of course not, right.

Cash-flow keeps the lights on, and appreciation will make you WEALTHY. FACTS......

Well positioned, quality, strategic investment real estate BEATS S&P, beats "cheap cash-flow" properties, beats most every investment vehicle in existence.

Once risk adjusted it DOES beat everything.

I agree with your sentiment but am unaware of any market that has long term appreciation as high as 7%. I am using since 2000 which includes the GFC. Many markets may have over 7% if starting after that. Using since the year 2000 (source neighborhoodscout), San Fran may have been above 7% before the work from home batted its appreciation. LA is over 6%. My market San Diego is near 6%. No market that I have looked at is over 7% going back to the year 2000 and only a few I have seen is over 6% since the year 2000.

The 1% or even 2% appreciation lower (I consider markets over 5% since the year 2000 to be high appreciation markets) adds a bit of time to hit cash neutral but on a leveraged purchase the appreciation alone whoops the low inflation total return. At 20% LTV, 5% appreciation is a 25% return on initial equity (I do realize there are transaction costs, but that is true in both markets). On your $300k example, 80% LTV means initial equity of $60k. 5% appreciation is $15k. The appreciation is $1,250/month. if I subtract the -$500 month cash flow in your example, that is $750/month return in year 1 without including equity pay down and tax benefits which are comparable in both markets. Note the appreciation and rent growth are compounding functions meaning year 1 is the worst year. Anyone other than Mike think he can generate $750/month return after expenses on a $300k purchase in the cheap markets on a high leverage purchase? If they do they likely need some lessons in underwriting.

the math going backwards is clear. However near term some of those traditional low appreciation markets have experienced appreciation comparable to many of the traditional higher appreciation markets. @Dave Meyer I believe did a post on this a few months ago. I am sure it can be found easily. The time span was too short to indicate much other than the traditional cheap markets have been competive in appreciation recently with traditional high appreciation markets. If it continues, the line is blurred between high appreciation and low appreciation markets. Can Detroit be a high appreciation market? Time will tell. @James Hamling I have seen at least one of your posts indicate, paraphrasing, that the goal is not to purchase the markets that have experienced the high appreciation but the markets that are going to experience the high appreciation. That certainly is the goal, but much easier said than done. I look at my market dynamics/metrics and it looks likely to continue to have high appreciation but it is not guaranteed.

Fortunately my primary market has had very good appreciation and rent growth since my purchases. But there is a reason I have not purchased in 3 years in my market (I have put out only a few offers in my market in those 3 years). There are challenges to purchase properties that meet my lofty return expectations. Getting an infinite return that does not bleed cash after a high LTV value extract is near impossible (a unicorn find). I historically was able to find these. I do not invest in RE as the primary for a 20% IRR (possible exception for a vacation home). I would be very happy with 20%/year as LP where the investment is passive. I am spoiled by a different time (2010 to 2022 had a lot of opportunity in RE, the present is more challenging).

best wishes

I suggest first stripping out any "exceptional" data segments if want to get any chance of accuracy in analysis. For me that means I look pre-GFC, and post GFC - COVID.

GFC was a once in 100+ yr thing, so it's gonna skew data. Same with covid. So one has to separate out such things, keep them in their own window of perspectives.

Next, keep in mind I said an average appreciation rate. If you get 10%, 2%, 4.5%, 12%, 1%, in the context of investing which means over a duration of time, we don't get hyper fixated on any 1 years results and instead we focus on how 5, 10, 20etc years of things comes out.

Much of what I do is a 7yr window. Given this cycle of economy, achieving an averaged 5% appreciation on asset's looks to be a rather non-special bar to achieve. We are in the age of inflation, keep that in mind. Inflation via many many mechanisms. What Bessent has presented for future plans is an inflationary action. What POTUS presents is also inflationary. The demands of national debt presents inflationary resolves. All directions point to inflation.

Inflation realized in real estate is appreciation.

Diminishing ability to buy/own a home vs rent, increasing tenant pool and tenant demand is an inflationary action.

Look, leverage or no leverage is a completely different conversation. What Mike put forward, besides being a complete violation of mathematics, is just bizarre. it's not different, it's saying 1+1= Llama. It's bizarre.

The front facing math alone proves appreciation wins. Add in depreciation, 1031, pyramiding, tenant quality, impact on operational expenses, this all just widens the victory gap appreciation holds into a grand canyon.

It's actually similar to the all-cash vs with leverage debate.

If one understands the math, leverage doesn't just beat out all-cash, it crushes it. But the math is not always readily understood.

And those debates also are lead via feelings vs facts. That holding all-cash "feels" safer.

Feelings vs facts.

There is a reason why when we invest it's a question of what do the #'s say, not how does it feel.

Interestingly enough Dan, when I stripped out the outlier data and took the longest data segment i could to peg "normalcy" for an average appreciation rate, what I got was:

Rents: 3.89%

Property: 2.9395%

Yes, this data includes a lot of post GFC data, because one has to, you can't just cut off 10yrs so it is arguably nerf'd down a bit. But I like to consider things conservatively and be surprised positively.

So looking forward, a 5% appreciation market is not really anything all that special. It's saying that the inflation cycle will be only 2pts more then "cheap money" past.

Post WWII debt deleverage says something very different than 2pts.

Now to those who say housing can only go up so far..... I say how do you cap out the price of lumber, wire, nails, Electricians, Plumbers, concrete, excavators, water 7 sewer...... As long as the cost of everything that goes into making housing is not capped, housing itself will not be a capped price.

The volume of sales, the % of person who can buy xyz housing, that will change but in an inflationary cycle, the cost of housing will increase.

This is why we see housing getting smaller and smaller again.

Now also remember, every person priced out of ability to buy is an added tenant. Hence the long standing prediction of tenants becoming 60% vs the historical 40%. Or more.

Again, inflationary.

All signals are inflationary. A deflation would lower US exports, strain US imports, strain domestic economy. Big $ doesn't want that. Big $ and Big Power uniformly agrees inflation is far-far better than deflation.

So my bet is on inflation vs deflation.

>So looking forward, a 5% appreciation market is not really anything all that special. It's saying that the inflation cycle will be only 2pts more then "cheap money" past

Looking at it as a 2 pt difference is one way to look at it, but to me the more appropriate way to look at it is 5% is over 67% higher than the average appreciation rate. Note my market is almost 100% higher than your just less than 3% number. LA is over 100% higher than your listed national appreciation.

2 points added to 100 is a lot different (2% increase) than 2 points added to less 3 (over 67% increase).