All Forum Categories

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

All Forum Posts by: Eric Fernwood

Eric Fernwood has started 57 posts and replied 710 times.

Post: How to overcome economical downturn as landlord

Post: How to overcome economical downturn as landlord

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Nick Liu,

Great question. I will attempt to answer it from going through the 2008 crash in the Las Vegas market.

Buy the Right Properties to Start Off

During every market crash, some locations are hurt far worse than others. For example, the current drop in oil prices has hit North Dakota hard but has had little impact on Nevada. The same is true of business sectors within a metro area. Some sectors are hit far worse than others. However, it is hard to determine which are the affected by looking at the gross numbers provided by the news sources.

If you only looked at the unemployment rate and number of foreclosures in Las Vegas during the 2008 through 2014 period, you would expect all Las Vegas investors took a terrible beating. However, our clients reported that rents and time to rent did not change for class A and B properties. When one of our clients asked for specifics we dug into the data. In order to answer her question we analyzed MLS sales and rental data during the period from 2008 to 2014. One of the problems with most data is that it is too "averaged" to be truly useful. We decided to narrow our focus as follows:

• Single family

• 3 bedrooms

• 2 car garage

• 1,200 to 1,500 SqFt

We also restricted the geographical area to the region marked in green below.

Restricting the data to this property profile and area matched the majority of our investor's properties at that time, which are A or B class properties.

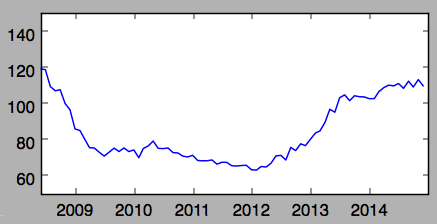

We started by exporting data from the MLS for conforming properties that sold or leased between 2008 and 2014. We then computed the average $/SqFt by month and plotted the results as shown in the graph below.

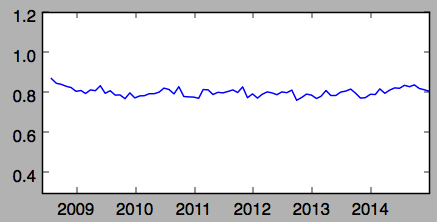

As you can see, the average $/SqFt sales price plunged by almost 50%. What happened to the average $/SqFt rental price? As you can see below, rental rates remained virtually unchanged.

The data showed what our clients were experiencing; A & B class investment properties saw little or no change in cash flow or time to rent during the 2008 to 2014 period. However, C class properties fared badly with vacancy rates exceeding 20% in some areas. We believe that the reason C class properties were disproportionately impacted by the crash has to do with the job sectors in which the different tenant pools worked.

Class C properties in Las Vegas generally rented in the range of $450/Mo. to $700/Mo. and were largely occupied by construction workers and hourly service workers. When construction virtually stopped in 2008, a great many of these people became unemployed and thus the high vacancy rate and falling rents. However, the tenant pool for Class A and B properties (largely casino workers), which generally rented in the range of $1000/Mo. to $1400/Mo., suffered income reductions but comparatively few became unemployed. Even those who lost their homes through foreclosure or short sales still needed a place to live and desired to stay in the same general areas so they became renters.

It is important to consider how the industry/business sectors which employ your target tenant pool are likely to perform during a downturn. We feel this is far more important than observing various purchase "rules" because it does not matter how little you paid for the property if there is no tenant paying the rent. Rental properties are only as good as the jobs in which the tenant pool works.

There is another factor that contributed to the class A and B rental stability in Las Vegas: eviction laws.

Eviction Laws

Incentives are strong determiners of how people will behave. A great example from history is the survival rate of prisoners transported to Australia during the 1860's. Originally, ship captains were paid a fee for every prisoner that walked onto a ship bound for Australia. Under this incentive program, only about 40% survived the transit. When the incentive changed to being paid for every prisoner that walked off the ship in Australia, the survival rate increased to about 98%.

In some states like California it can take up to one year to evict a non-paying tenant. So, if a tenant is undergoing financial stress, there is little incentive to pay the rent. As one client put it, "In California, tenants pay their bills in the following order: car payment, credit cards and, if they have leftover funds, the rent."

In Las Vegas, a typical eviction takes less than 30 days and costs less than $500. Tenants have a strong incentive to pay the full rent on time or they will be out on the street in less than 30 days. Due to Las Vegas eviction laws we believe that tenants in Las Vegas pay their bills in the following order: car payment, rent and, if they have leftover funds, credit cards.

What about the class C tenant pool? We feel that two factors made the crash very hard for class C property owners. First, if the tenant does not have a job, they can't pay the rent. When construction virtually ended in 2008, so did the related jobs. Second, in our experience, class C tenants tend to be cash based (class A and B tend to be credit based). Cash based tenants have little to fear from evictions and judgements because they carry no financial "history"; what they did in the past has little impact on their present or future. Such cash based tenants have little incentive to pay the full rent on schedule; they can always move to another property.

In Summary

• You need to buy properties where the tenant pool is credit based and their job pool is likely to be stable even in turbulent economic times.

• Tenants constantly pay rent only when there is a strong incentive to do so. Do local eviction laws incentivize paying the rent or do they have the opposite effect?

Post: Historians Perspective needed - RE crash of 2007 -2010

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Cory Mccarthy,

You posted an excellent question but one without a simple answer.

Investors were likely to be impacted by the 2008 crash in two different ways. First, if you sold the property during the crash under most conditions you would have lost money. However, if the property was still generating a positive cash flow during the crash few people would choose to sell so I will ignore this potential impact.

The main challenge for many investors was that they started losing money due to falling rents and rising vacancies. However, not every property in every location fared the same. Las Vegas was one of the hardest hit cities in the US during the 2008 market crash. And, if you only looked at the unemployment rate and number of foreclosures in Las Vegas, you would expect all Las Vegas investors took a terrible beating. However, our clients reported that rents and time to rent did not change. When one of our clients asked for specifics we dug into the data. In order to answer her question we analyzed sales and rentals during the 2008 to 2014 period ourselves.

One of the more common mistakes people made when doing such a study is to combine everything together and compute an average. Usually, the results of such averaging will be of little value. For example, would you be comfortable living in an environment with an average temperature of 70°F? Sounds pretty good? What if I told you that the day time temperature is 450°F and the night time temperature is -310°F? The average is 70°( (450 - 310)/2 = 70°).

In order to provide valid data we narrowed our research to the typical properties the majority of our clients purchased. The property profile we used is as follows:

• Single family

• 3 bedrooms

• 2 car garage

• 1,200 to 1,500 SqFt

We also restricted the geographical area to the region marked in green below.

Restricting the data to this property profile and area matched the majority of our investors at that time, which would be considered A or B class properties.

We started by exporting data from the MLS for conforming properties that sold and leased during the period between 2008 and 2014. We computed the average $/SqFt by month and plotted the results as shown in the graph below.

As you can see, the average $/SqFt sales price plunged by almost 50%. What happened to the average $/SqFt rental price? As you can see below, rental rates (and time to rent) remained virtually unchanged.

Our clients who purchased investment properties prior to 2008 saw little or no change in cash flow or time to rent. However, C class properties did not do well. Depending on the area, class C properties vacancy rate increased to over 20% and rents fell as well. Why did Class A and B properties do well while Class C properties did so badly?

Location and price range will primarily attract a specific tenant pool. In 2008, Class C properties, which generally rented in the range of $450/Mo. to $700/Mo., were largely occupied by construction workers and service workers. When construction virtually stopped in 2008, a great many of these people became unemployed and thus the high vacancy rate and falling rents. However, the tenant pool for Class A and B properties, which generally rented in the range of $1000/Mo. to $1400/Mo., suffered income reductions but comparatively few became unemployed compared to the tenant pool for Class C properties. So while the tenant pool for Class A & B typically had reduced income, they chose to prioritize paying the rent. Why? Based on our research we believe that the reason the rental market was so stable had to do with the eviction laws in Las Vegas, in addition to job stability.

In order for a tenant to consistently pay rent they have to have both the ability to pay and the willingness to pay. If the tenant pool remains employed, even at a reduced rate, they have the ability to pay because of the income requirements required by the property manager we work with. The willingness to use limited financial resources was largely due to our eviction laws.

For example, in California it can take up to one year to evict a non-paying tenant. So, if the tenant has limited financial resources, they know that they can skip paying the rent for months with little risk of being evicted. In Las Vegas, a typical eviction takes less than 30 days and costs less than $500. Tenants know this so they prioritize paying the rent because they know that they will be quickly evicted.

In summary, we came to the following conclusions:

• Not all jobs were affected equally in the 2008 crash. Metro averages do not provide a reliable indication for any specific tenant pool.

• Some business sectors/occupations were hurt less than others. You need to consider how the business sectors which employ your target tenant pool are likely to perform in a downturn.

• Tenants pay rent when they have the ability and willingness to pay the rent. Local eviction laws can play a significant role in ensuring the rent is paid on schedule.

• The typical hold time for real estate is 10+ years. What can be a great investment today can become a financial disaster if the market changes. You need to look at both the return today and what it is likely to be in the foreseeable future.

• Careful selection of properties which the tenant pool found highly desirable enabled properties to still rent quickly during this turbulent period.

I hope this helps, Cory. Best of luck to your success.

Post: Las Vegas Investment Properties 2016 Outlook

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Allan Maerina,

Thank you for your kind words. Are there any topics that you would like me to cover in the future?

Best Wishes,

Eric

Post: Las Vegas Investment Properties 2016 Outlook

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Wrote the following for our clients in mid December 2015. Would welcome comments from fellow BP members.

National Economy

We think that a quote from Business Wire summarizes the national economy fairly well.

Las Vegas Housing Market

For the general Las Vegas housing market, the Las Vegas Review-Journal summarized the 2016 outlook as follows:

What We Are Anticipating in 2016

Our predictions are based on the following assumptions:

• Interest rates will rise in 2016 but at a modest rate. "Interest rates are headed up, but at a fairly mild pace." Forbes - Interest Rate Forecast 2015 - 2016

• China's economy will continue to slow down and there will be less cash property purchases in 2016. "China's Economy: More Volatility Ahead in 2016?" Bloomberg Business

• There will be no significant world events that will create volatility in the world economy.

Assuming the above, we predict the following for class A and B investment properties in Las Vegas:

• Sales Volume - The sales volume in 2016 will remain about the same as it was in 2015. If interest rates rise more than expected towards the end of 2016, we will see the sales volume trending down.

• $/SqFt - With sales volume declining, $/SqFt growth has flattened in recent months. We see $/SqFt as stable at least through the first half of 2016.

• Rents - Single family rents have steadily increased starting in mid 2015. Las Vegas has very little remaining develop-able land that is desirable. Because of this and continued economic growth in Las Vegas, we expect the trend to continue in 2016. For example, "Faraday chose the (North Las Vegas) site over locations in Georgia and Illinois that offered usable auto plants and better relocation incentives because it likes the business environment Nevada offered." Las Vegas Review-Journal. It is predicted that Faraday will employ 4,500 direct employees and approximately 9,000 indirect employees. We are seeing other businesses relocating from California and other states with less business-friendly laws and high taxes.

• Cash vs. Financed Purchases - With the Chinese economy slowing, we expect further declines in cash purchases. A year ago the percentage of cash sales was close to 50% and now it is down to 23%. The large number of cash buyers was making it difficult to get financed offers accepted through the first half of 2015.

In Summary

We do not see any significant overall change in the market if interest rates do not increase significantly. Las Vegas remains one of the few large metro areas with:

• Positive cash flow with 20% down financing

• Business friendly environment

• No state income tax

• Low property taxes (~0.86%)

• Low landlord insurance (~$500/Yr)

• Timely and cost effective evictions (28 days / $500)

• Almost zero urban sprawl since Las Vegas has little develop-able residential land in desirable areas

• Steadily growing population.

• Steady economic growth.

Post: Out of State Newbie

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Sean Autry,

I've been in Las Vegas for about 9 years. I was living in NYC and when I decided to change careers (in my last life I traveled internationally 200+ days/year), I chose real estate because there was little or no viable software for selecting good properties. I considered many locations in the US and Asia but decided on Las Vegas due to its unique characteristics. So far, the market has not disappointed me.

Post: Out of State Newbie

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Sean Autry,

Welcome to BiggerPockets. I am a realtor in Las Vegas and most of my clients live in other states or countries so I frequently have discussions with potential clients concerning how I would determine where to invest.

So we are on the same page, I believe all investment properties must meet three criteria:

The overall process I would follow to meet all three criteria is illustrated below.

Below is a description of each level.

Metro Level Considerations

I would only consider metro areas with:

Location Level Considerations

Once you have filtered prospective locations through the above criteria you will likely have a relatively small number of potential metro areas to consider. Now you can focus deeper into each one remaining. To do this you need detailed location level information. Where can you get such information? Local property managers. Every day property managers deal with marketing properties, maintenance, tenants issues, rehab, local regulations, finding and screening tenants and many other rental property related issues. Local property managers know what works and what will not work. Google the name of the city plus the words "property management" and you should get a number of hits. Go through their web sites and look for mid sized property managers. Select 3 or 4 and call them. The minimum you need to know is:

Have a list of well formed questions before you call and take notes. (I created a list of property manager interview questions. If anyone would like a copy, send me an email.) If you hear the same information from multiple property managers, then it is probably true. When you finish your property manager interviews you should have a reasonable guess to the answers to each of the following:

Once you combine answers to the above questions you will have what I call a property profile.

Detailed Location Investigation Considerations

With the property profile you should know exactly what you are looking for. The next step is to contact a local Realtor. Provide them with your selection criteria (where, type, configuration and purchase price range) and they will send you conforming properties and you can do further analysis. If everything still looks good it is time to go see the location yourself and start to assemble your investment team.

Your Investment Team

It is imperative that you have a trusted local team. At the minimum you need a (good) property manager and a Realtor. For more details on the investment team check out this BP post.

Sean, I hope I answered your questions. If not, please post them. You can find out more about real estate investing through the links on my profile page.

I wish you success.

Post: Current Henderson Market?

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Antony S.,

Profitable flipping is extremely difficult in the current market. Several factors must line up in order to make flipping a profitable business. It was great in 2005 but not at this time. Please see A Process for Increasing Your Odds of Profitably Flipping Properties (BP Editor's Choice Award) for more on flipping.

On formulating a multi-year plan, we do this with our clients. You need to determine your destination before you can choose a path. Some of the questions I ask my clients include:

• Goals - Appreciation, cash flow, balanced cash flow and appreciation?

• Available funds

• Time frame - When do you need what?

• Risk tolerance

• Credit - Leverage is highly desirable in real estate investing

In terms of the Las Vegas investment market, as @Phillip Dwyer stated, good investments are hard to find (the same is true for everywhere). However, we spent years developing and tuning software for selecting good properties. Today prices are higher but so is the rent. We are constantly finding properties with a real return (including all recurring costs) in the 5% to 7% range (single family). However, these properties represent only 0.01% to 0.1% of the available properties on the MLS so we can only do this because of our proprietary software.

Antony, I have never seen a "60 day subject to financing" clause. You need to line up your financing before you make any offers. You need to know all your costs (including financing) before you consider any purchase.

Best of luck.

Post: Do you have a system for investing out of state?

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Tyler Brown,

You asked an excellent question but not one with a simple answer. I will tell you the process I would follow and some of the concerns I would have.

So we are on the same page, I believe all investment properties must meet three criteria:

• Sustained profitability - The property must generate a positive cash flow today and into the foreseeable future (10+ years).

• Likely to appreciate over time - You would never buy a property just for appreciation but appreciation is very desirable. And, rents usually rise along with appreciation because appreciation is the result of increased demand.

• Investor friendly state/county/city regulations - Evictions, rent control, code compliance requirements, etc. This is a critical factor. In some states it can take more than a year and cost thousands to evict a non-paying tenant while your mortgage payments and costs continue. Few investors could handle such a loss. If you think eviction regulations and landlord rights are not critical, you have not seen the movie Pacific Heights.

While it is relatively easy to satisfy one or two of the above criteria today you need to satisfy all three for the foreseeable future (10+ years). Too many new investors only consider how the property will perform today using metrics like ROI. However, ROI tells you nothing about how the property is likely to perform in the future.

The overall process I would follow to meet all three criteria is illustrated below.

Below is a description of each level.

Metro Level Considerations

I would only consider metro areas with:

• Reasonable access (flight/drive) from where you live. Sooner or later you will want (or need to) inspect your properties.

• A city where you would like to spend time. One of the many advantages of investment real estate is that travel expenses to inspect your properties are deductible. I live in Las Vegas and many of my clients (especially the ones in Canada) "inspect" their properties between January and March.

• A population exceeding 1M will have sufficient historical data so you can evaluate trends. Also, larger cities have more stability than smaller cities because they tend not to be a one-employer economy.

• Financially stable - Cities that are in bankruptcy or near bankruptcy are not good places to invest. If you look at inflation adjusted $/SqFt prices in such cities you will find that property prices have fallen as well as rents. And, they are likely to continue to fall because the business environment that caused the fall is not likely to change. For more information see, "Investing in Declining Markets" on my profile page.

• Metro areas which do not experience hard freezes or significant moisture. Ongoing maintenance costs are significantly higher in areas with hard freezes and moisture.

• No or limited urban sprawl - In every metro area I've seen there are areas that were once prime areas and over time become distressed areas. The reason is that people with money will tend to move to newer areas with newer floor plans, etc. You do not want to buy in areas that are trending down.

• Stable or increasing job quantity and quality - The value of a property is no better than the jobs around it. In many parts of the US, manufacturing and similar jobs are going away and what remains are service sector jobs. Service sector jobs tend to pay much less than manufacturing jobs so the families of these workers have less disposable income. Less disposable income means that they cannot afford to pay the level of rent they did in the past so property prices and rental rates fall.

Location Level Considerations

If you selected a number of potential metro areas and filtered them through the metro level considerations you will likely have a relatively small number of potential metro areas to consider. Now you need to focus deeper into each one remaining. To do this you need detailed location level information. Where can you get such information? Local property managers. Every day property managers deal with marketing properties, maintenance, tenants issues, rehab, local regulations, finding and screening tenants and many other rental property related issues. Local property managers know what works and what will not work. Google the name of the city plus the words "property management" and you should get a number of hits. Go through the web sites and look for a mid sized property manager. Select 3 or 4 and call them. The minimum you need to know is:

• Where - Specific location within the metro area that rents the best.

• Type - Condo, multi-family, single family, etc.

• Configuration - Singe story, two story, number of bedrooms, etc.

• Rent range - If the most desirable tenant pool can only afford to pay between $800/Mo. and $1,000/Mo. you should only be looking at properties that you can purchase, rehab and profitably rent within that rent range.

• Regulations - The most important will be the time and cost to evict.

• Typical rehab costs and issues to avoid.

• Typical time a tenant stays in such properties and typical turn costs.

Have a list of well formed questions before you call and take notes. (I created a list of property manager interview questions. If anyone would like a copy, send me an email.) If you hear the same information from multiple property managers, then it is probably true. When you finish your property manager interviews you should have a reasonable guess to the answers to each of the following:

• Where

• Type

• Configuration

• Rent range

• Regulations (like eviction cost)

• Typical rehab costs

• Typical time a tenant stays

• Typical turn cost

• Insurance cost

• Property tax rate

• Probable property manager you would like to work with

• Probable ongoing maintenance costs

• Probable recurring costs

• Purchase price range - When you know where, type and configuration, you can easily determine the sales price range using Zillow or a similar site.

Time to dig deeper.

Detailed Location Investigation Considerations

With the property profile you created during Location Level Considerations, you should know what you want. The next step is to contact a local Realtor. Provide them with your selection criteria (where, type, configuration and purchase price range). They will send you conforming properties and you can do further analysis. If everything still looks good it's time to go see the location yourself and start to assemble your investment team.

Your Investment Team

It is imperative that you have a trusted local team. At the minimum you need a (good) property manager and a Realtor. For more details on the investment team check out this BP post.

Tyler, my response ended up being much longer than I originally intended. However, you asked an excellent question and I believe the answer will be of importance to many BPers.

Post: Las Vegas, NV

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Jeff Workman,

Welcome to Biggerpockets.

As I understand your questions:

• Do you need an real estate attorney?

• Do you need an accountant if you own investment real estate?

• Why real estate as opposed to other investments like stocks.

• Is Las Vegas the right location?

All good questions which I will answer below:

Do You Need An Real Estate Attorney?

We have many investor clients and to the best of my knowledge none has engaged a real estate attorney. The contracts and process for buying residential (non-commercial) real estate are highly standardized. Everyone uses the same purchase contract and the actual purchase is executed by a third party called a title company. Commercial is a totally different situation.

Do You Need an Accountant?

None of our clients specifically engaged an accountant for the real estate portion of their portfolio. The property manager handles all the day-to-day activities and at the end of the year provides the needed tax forms. Again, this is on the residential side. Commercial real estate is different.

Why Real Estate?

Traditional investment concept (stocks, bonds, CDs, 401Ks, etc.) is to accumulate enough capital so you can later draw-down (withdraw) funds over a period of time. Simplistically, to determine how much you need to accumulate you need to know: the amount you will withdraw per month, how long you will live and what inflation will be during these years. For example, suppose you plan to withdraw $5,000 a month for 30 years and there is zero inflation, zero transaction fees, zero taxes and zero capital appreciation. If that is the case, then the math is easy:

30 Years x 12 Months/Year x $5,000 = $1,800,000

However, if inflation exceeds capital appreciation you will need to accumulate more before you start to with draw money. For example, if you expect 3% net inflation during the draw-down period you would need approximately $3,000,000 to draw down $5,000 (present value) over 30 years. Also, what if you or your spouse live longer than planned?

With real estate, the concept is to accumulate sufficient income streams over time such that the aggregated income streams meet your income needs today and into the future. For example, suppose each property you buy generates a net cash flow of $250/Mo. If this is true, then you need to accumulate $5,000/$250 or 20 properties.

How much would it cost to purchase each property? As in the previous example, we will ignore inflation and appreciation. Assuming each property costs $180,000 and you obtained 30-year financing with 20% down at 5% interest, you will need about $36,000 plus another $12,000 to cover closing costs, rehab, etc. or $50,000/property. Simplistically, 20 x $50,000 = $1,000,000 is what you need to establish a $5,000/Mo income stream. When the mortgages are paid off the cash flow will significantly increase but we will ignore this for the present example. And, since rents historically track inflation while your recurring costs remain relatively constant, your return will increase as inflation increases.

Is Las Vegas the Right Location?

Most of my clients live in other states or countries. One of their first questions is, "Why should I invest in Las Vegas?" My response is,"What are your goals?" It is important for me to know what they are seeking because Las Vegas will not meet everyone's goals. I will briefly discuss where I think Las Vegas is strong and where I think it is not as strong (Here is a BP post with more details). Note that I will focus on single family properties, the multi-family and commercial market is quite different.

Las Vegas' advantages:

Short term:

• You get to keep more of the rent the property generates. This is due to the low property tax rate, zero state income tax, low insurance, and low maintenance costs.

• Low business risks due to landlord friendly laws. In Las Vegas an eviction takes 28 days or less and costs about $500 (compared to ~1 year in California as an example).

Long term:

Metrics like ROI are only a snapshot in time; how the property is likely to perform today. ROI tells you nothing about how the property is likely to perform in the foreseeable future. Simplistically stated, if there is continued demand for a item the price will rise or stay the same. The key demand factors for real estate are:

• Population - If people are moving out of a area, housing prices and rental rates in that area are likely to fall. If people are moving into an area, housing prices and rental rates in that area are likely to rise. Depending on which study you choose to believe, Las Vegas' population is projected to increase by 1% to 2% per year for the foreseeable future.

• Urban sprawl - Urban sprawl can be an absolute value killer. People with money will tend to move to newer areas and the people with lower incomes are left behind. The result is falling property prices and falling rental rates. Las Vegas is a virtual island, it is surrounded by federal land. There is almost no expansion room in desirable areas so urban sprawl is almost non-existent in Las Vegas.

• Job quantity and quality - The value of a property is no better than the jobs around it. In many parts of the US, manufacturing and similar jobs are going away and what remains are service sector jobs. Service sector jobs tend to pay less than manufacturing jobs so the families of these workers have less disposable income. Less disposable income means that they cannot afford to pay the level of rent they did in the past. Inflation adjusted income in Las Vegas have been slowly increasing (except during the 2008 to 2011 crash) and projections are that the increases will continue according to a Federal Reserve Bank study.

Where is Las Vegas relatively weak? The entry price point for class A town homes is about $125,000. There are locations in the US where you can buy similar properties for less than $50,000. However, I question the long term implications of buying in declining markets like the mid-west where service sector jobs are replacing high paying manufacturing jobs.

Jeff, I hope I answered some of your questions. For more Las Vegas specific real estate investment information please see my profile.

If you or other BP members would like to learn more about real estate investing you are welcome to join me as I check out investment properties for clients. Almost all of our clients live in other states or countries and I usually check out properties alone and I welcome the company.

Best wishes,

Post: If and when the sky "IS" falling, will it crash on Turnkeys too?

- Realtor

- Las Vegas, NV

- Posts 737

- Votes 1,510

Hello @Account Closed,

You asked a very good question and on the surface it seems like a simple question to answer but it isn't. I will start by stating that the purchase vehicle (turnkey or direct purchase) makes no difference when it comes to how a property is likely to perform in times of economic instability. In my opinion, the only difference might be that since you will pay more for a turnkey property you will likely see a lower return but that is not a factor of economic stability.

Rental stability is totally dependent on the jobs your tenants have. If the tenant's jobs go away, they cannot pay the rent. So, when you are considering a property, consider the major employers where your tenant pool is likely to work. How did these employers and their market segment fare in the last crash? A more likely future risk is how the location is trending. Are property prices increasing or decreasing? Are the quantity and quality (earning power) of jobs increasing or decreasing? You need to consider these factors because ROI and similar metrics are only a snapshot of the market as it is today. ROI tells you nothing about how the property is likely to perform in the future and typical hold times for investment real estate is 10+ years. Also, in times of economic instability there are no "safe" regions or safe metro areas. "Average properties" in "regions" don't exist. You buy a specific property in a specific location and whether your property stays rented (performs) depends on whether the tenant pool stays employed. There is another layer to be considered.

There are a range of rental prices available for any given area. You might have properties renting from $300/Mo. to $10,000/Mo. The occupations of the people who live in a $300/Mo. property are likely very different than people who live in a $10,000/Mo. rental. Because they have different types of jobs they likely have different employment sectors and thus have different vulnerabilities. For example, assume that the primary pool of tenants for $10,000/Mo. rentals are doctors. If the federal government decides that all doctors incomes are capped at $100,000/Year, the tenant pool for $10,000/Mo. is going to vanish. Would a cap on doctor incomes significantly impact properties renting for $300/Mo.? Probably not at all. How does my (silly) example play out in the real world?

Las Vegas was one of the hardest hit metro areas in the US during the last crash. Unemployment exceeded 10% during the 2008 to 2014 market crash. However, like in all crashes, not all income levels were equally affected. We did a study of how single family home rental rates for properties renting in the $1,000/Mo. to $1,300/mo. range in the area shown on the map below fared during this period.

As we all know and reflected in the chart below, the property $/SqFt prices fell sharply during this period.

With the high unemployment rate, falling property prices and large numbers of foreclosed homes coming onto the market you would expect that rental rates would also fall. They didn't. Below is a chart showing $/SqFt rental rates for conforming properties during this period. As the graph shows, rental rates were virtually unaffected by the market crash.

The reason there was virtually no change in rental rates is that the tenant pool for these properties continued to be employed and thus continued to pay the rent. However, if you owned properties and the tenant pool was largely connected to the construction industry the results were very different. Construction virtually stopped in Las Vegas at the beginning of this period and time to rent and rental rates for rental properties catering to this pool of tenants did not perform well at all.

In Summary

• The method you choose for purchasing the property (turnkey or direct purchase) is not a significant factor when it comes to how the property will perform during times of economic turmoil.

• "Average properties" in "regions" don't exist. You buy a specific property in a specific location and whether your property stays rented (performs) depends on whether the tenant pool for that specific stays employed.

• Within the same general location, different economic pools of tenants are subject to different job risks during times of economic turmoil.

Doyle, you asked a great question and I hope I answered it. If not, post another question.