All Forum Posts by: Eric Fernwood

Eric Fernwood has started 64 posts and replied 793 times.

Post: Investing in Las Vegas

Post: Investing in Las Vegas

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Rafal Soltysek,

There are good properties available, but they are not common - YoY appreciation for properties that conform to our target tenant pool: 27%. YoY rent increase, 18%. See the charts below. What do I call good properties? Below is how our clients' and our properties performed over the last 15 years:

- Average annual appreciation since 2013: >9%. More now since 2021 saw a large increase.

- 2008 crash - Zero decrease in rent, no vacancies. Property prices fell like every other property, but no decrease in rent.

- COVID - Out of +200 properties, about five tenants could not pay the rent and vacated, paying one to three months penalty for early lease termination. The properties were re-rented in one to two weeks for $100 to $300 per month more.

- The eviction moratorium had no impact on our clients. Total evictions in 15 years: 5.

- Average tenant stay: 5 years

- Average turn renovation cost: <$500

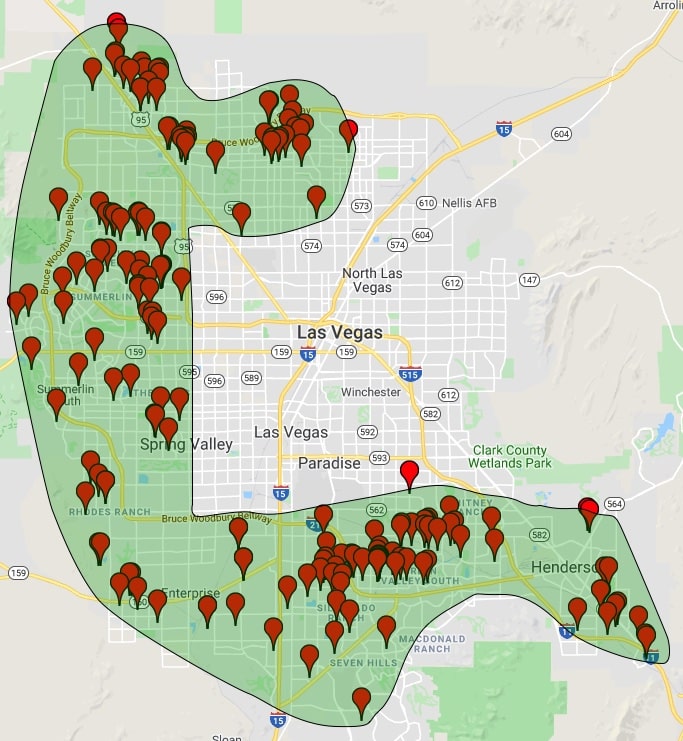

Where do we find most of our properties? Below is a map showing a sample of our client's properties and the general area where our software finds the most conforming properties. The green shaded area is where our software finds the most conforming properties. However, while the shaded area looks homogeneous, in reality, it looks more like Swiss cheese.

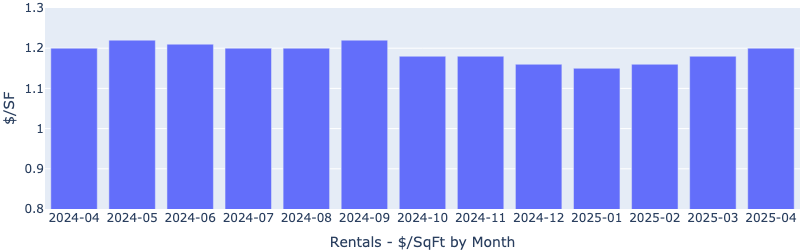

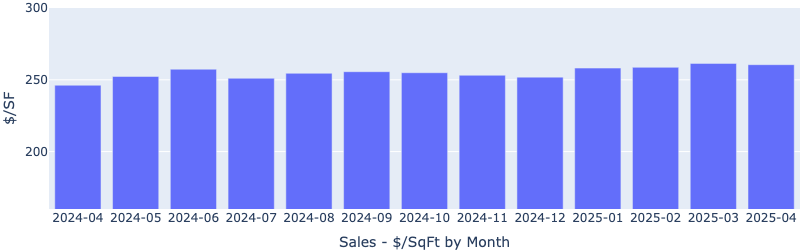

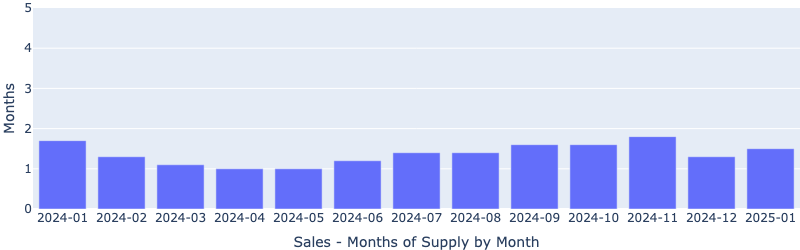

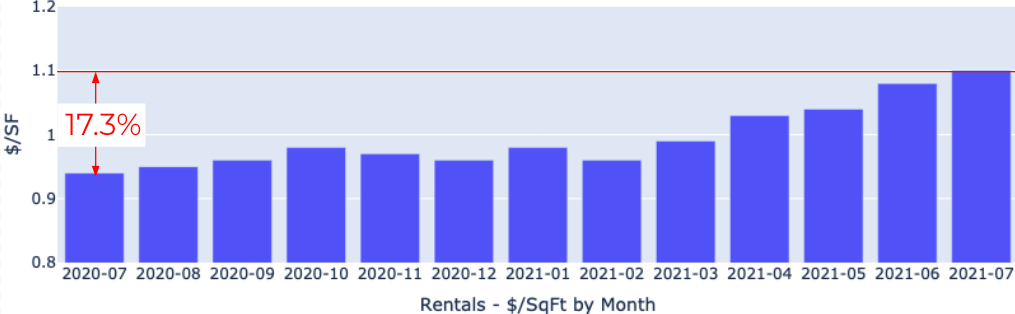

What is the current market situation for conforming properties? Below are trailing 13 month statistics:

Rentals - Median $/SF by Month

Rent is up 18% YoY.

Sales - Median $/SF by Month

Prices are up 27% YoY

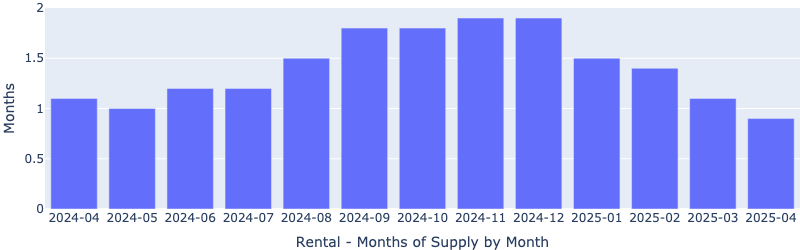

Sales - Months of Supply

This is no bubble. There is only 0.5 or 0.6 month of supply since March 2021. Demand is far greater than supply.

Why Will Las Vegas Continue to Perform?

The two big factors driving demand are increasing population and tens of thousands of new jobs.

- California - People and companies continue to flee California and a percentage choose Las Vegas.

- >$20B in new construction under development and several billion more announced. This will create tens of thousands of good jobs bringing more people to Las Vegas.

- No state income tax.

- Property tax average is 0.55%

- Landlord insurance on a $420,000 property is $550/Yr.

Conditions for Success:

- The right tenant pool - Not all tenant pool perform equally well. Vacancy cost being the biggest cost difference.

- The right local investment team - You cannot learn all you need to know and find all the resources you need on your own. And, working with an investment team costs you nothing. Failing to work with a good investment team will cost you time, money and risk.

- The right property - You must select properties that attract the right tenant pool and have low maintenance costs.

Summary

There are good properties available today. The conditions increasing demand are real and driven by new jobs and people fleeing California. We see no reason for this to change for the foreseeable future.

Post: New investor - Advice on Brrr’ing in Las Vegas Market

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Kevonna Ahmad,

We have clients (and we) use the BRRRR method. However, buying a property significantly below market value, renovate, refinance and repeat will probably not work. Demand is outstripping supply significantly, so few (good) properties are to be had at a discount. However, due to rapid appreciation (27% YoY) you can refinance them fairly quickly. Below are two charts showing how properties that conform to our property profile performed over the last 13 months.

Sales - Median $/SF by Month

27% YoY appreciation.

Sales - Months of Supply

Six months of supply is considered a balanced market. Currently, conforming properties are at about 0.6 months of supply. The limited supply of properties is what makes finding properties at a discount unlikely. Also, the limited supply is a clear indication that this is not a bubble. While we may not see 27% annual appreciation rates in the future (I hope not), I believe prices will continue to rise rapidly, which works well for BRRRR. Let me know if you would like a BRRRR case study.

Rentals - Median $/SF by Month

Rents are also rising rapidly. YoY increase of 18%! This means that even with the rapid price increase, you will still receive a good initial return and expect your return to growing as rents increase.

I hope the above helps.

Post: Buying Rentals Out Of State Without Turnkey Companies

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

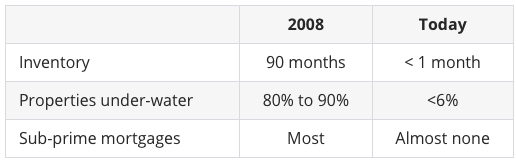

The advantage "experts" have is that they are always right somewhere at some time. However, they are rarely correct in any specific location at any given time. Las Vegas is just such a location. Below is a comparison between 2008 and today, what we are seeing, and what will continue to drive the Las Vegas market for the foreseeable future.

2008 vs. Today

I see no similarity, despite the fear mongers in the press. Of course, fear sells, no one buys good news.

What We Are Seeing

Below is 13 month trailing statistics on all single family properties that conform to our property profile. Our property profile defines properties that our target tenant pool is willing and able to rent.

$/SF Rental Rate

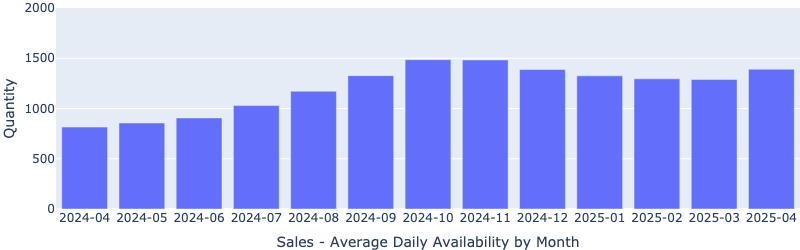

Rental Monthly Inventory

Around 3 months of inventory is typical for this time of the year. Today, it is 0.4 months.

$/SF Sales

Sales Inventory by Month

I think you will agree that there is little to indicate a crash. The question is, will it continue? In my opinion, yes. Perhaps (hopefully) not at the current fevered pitch.

What I Expect in the Foreseeable Future

Demand is what drives prices. So, what is driving demand in the Las Vegas metro area?

- Jobs - Today, there is about $20B in new construction, and another $5B to $7B has been announced. This new construction will create tens of thousands of additional jobs, which will result in more people moving to Las Vegas. More people will increase demand, which will increase prices and rents.

- California Exodus - Almost every day, I read another article about companies and people fleeing California. A percentage of the people fleeing California come to Las Vegas. This is especially true with the digital nomads. As more Californians flee, demand will continue to increase, which will increase prices and rents.

- Pro Business Environment - Nevada has no state income taxes, low property tax, low-cost property insurance, reasonable traffic, reasonable property prices, lower cost of just about everything. Las Vegas is investor-friendly. Evictions take less than 30 days and cost about $500. For our target tenant pool, we've had five evictions in the last 15 years. California commercial energy rate: $.2275/kWh. Nevada: $.1114/kWh. California is just over twice as expensive.

I could continue, but I think you can see that Las Vegas is a desirable place to live, especially when compared to California.

Risks

- Water - Today, between 70% and 80% of all water consumption is wasted on grass. It makes no sense to grow grass in the desert. If the situation becomes dire, implement a progressive water charge. Lawns will disappear rapidly. Alternatively, Las Vegas is about 300 miles away from a major source of water in northern Nevada. Almost all the land between Las Vegas and the water sources is federal, so minimal cost. The Keystone pipeline was 1,200 miles and crossed several states, and was mostly on private or reservation land, and is projected to cost $5.7B. The most recent casino to open cost over $7B. The last estimate I heard for building the Las Vegas water pipeline was $2B. However, whether the cost is $2B, $10B, or $20B does not matter. Las Vegas is not going to be shut down due to water.

- Californication - This is a valid concern. People flee California due to regulations, and costs and then want to implement the same disastrous conditions in Nevada. Fortunately, it seems that after about a year, they lose the "California" mindset. So, this may not be a valid concern.

My Opinion

Las Vegas is doing well today and is very likely to do well into the foreseeable future. What am I personally doing? I am adding more properties to my portfolio.

Post: Is Las Vegas a good place to invest in real estate in 2022?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Jalen De Leon,

Is Las Vegas a good place to invest in 2022?

It depends on your goals. If you were looking for a highly reliable long-term income stream, Las Vegas is one of the best places in the US. In this post, I will look at what's happening today and provide some insight into what is likely to happen in the foreseeable future.

What's Happening Today?

2008 vs. 2021I see no similarity, despite the fear mongers in the press. Of course, fear sells, no one buys good news.

Where Is the Market Today?Below is 13 month trailing statistics on all single family properties that conform to our property profile. Our property profile defines properties that our target tenant pool is willing and able to rent.

$/SF Rental Rate

Rental Monthly Inventory

Around 3 months of inventory is typical for this time of the year. Today, it is 0.4 months.

I can show more stats but I think you will agree that there is little to indicate a crash. The question is, will it continue?

What I Expect in the Foreseeable Future

Demand is what drives prices. When there is more demand than supply, prices rise until supply equals demand. So, what is driving demand in the Las Vegas metro area?

- Jobs - Today, there is about $20B in new construction, and another $5B to $7B has been announced. This new construction will create tens of thousands of additional jobs, which will result in more people moving to Las Vegas. More people will increase demand, which will increase prices and rents.

- California Exodus - Almost every day, I read another article about companies and people fleeing California. A percentage of the people fleeing California come to Las Vegas. This is especially true with the digital nomads. As more Californians flee, demand will continue to increase, which will increase prices and rents.

- Pro Business Environment - Nevada has no state income taxes, low property tax, low-cost property insurance, reasonable traffic, reasonable property prices, lower cost of just about everything. Las Vegas is investor-friendly. Evictions take less than 30 days and cost about $500. For our target tenant pool, we've had five evictions in the last 15 years. California commercial energy rate: $.2275/kWh. Nevada: $.1114/kWh. California is just over twice as expensive.

I could continue, but I think you can see that Las Vegas is a desirable place to live, especially when compared to California.

Risks

What do I see that could possibly slow down growth?

- California becomes the place for low cost business operations, personal freedom, and reasonable cost real estate. Not happening.

- Major terrorist event. There are much better places to make a statement against the US than Las Vegas. Very unlikely.

Concerns That I Hear

- Water - Today, between 70% and 80% of all water consumption is wasted on grass. It makes no sense to grow grass in the desert. If the situation becomes dire, implement a progressive water charge. Lawns will disappear rapidly. Alternatively, Las Vegas is about 300 miles away from a major source of water in northern Nevada. Almost all the land between Las Vegas and the water sources is federal, so minimal cost. The Keystone pipeline was 1,200 miles and crossed several states, and was mostly on private or reservation land, and is projected to cost $5.7B. The most recent casino to open cost over $7B. The last estimate I heard for building the Las Vegas water pipeline was $2B. However, whether the cost is $2B, $10B, or $20B does not matter. Las Vegas is not going to be shut down due to water.

- Californication - This is a valid concern. People flee California due to regulations, and costs and then want to implement the same disastrous conditions in Nevada. Fortunately, it seems that after about a year, they lose the "California" mindset. So, this may not be a valid concern.

My Opinion

Las Vegas is doing well today and is very likely to do well into the foreseeable future. What am I personally doing? I am adding more properties to my portfolio.

Post: Buying Rentals Out Of State Without Turnkey Companies

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

There are some great comments on this thread. So, I decided to put in my $0.02.

Out of the +200 clients we've worked with over the years, only 10 to 15 are local. All the rest reside in other states or countries. Our repeat business rate is over 90% so far so we know that our process works. So, my contribution to this thread is to outline the process we recommend. The basic process is illustrated below.

To keep this post in a reasonable length I will focus only on the first 5 steps, which if done well will make the remaining steps minimal effort on you.

Define Your Goals and Resources

Without defining your goals, it will be hard to know where to start the journey and to see whether you can reach your goals. The least you need to know includes:

- Your starting point - How much capital and credit do you have or expect to have in a reasonable time frame? Unless you plan to pay cash for your properties, get pre-qualified for an investor loan, so you will know how much credit you will have access to.

- The end goal - This is usually something like $10,000/Mo. income, in present value dollars.

- Time frame - The shorter your time frame to reach your goal, the more initial capital and credit you will need.

Your plan does not need to be complex or in any specific structure. Simply writing it down and making adjustments as you progress is all you need to do.

Get Your Finances in Order

It takes money to make money. Despite what you read ("Nothing down to independently wealthy in 6 months", etc.), you need cash and credit to invest. In Las Vegas, long-term investment-grade properties cost between $300,000 and $400,000. By the time you buy a property, renovate it and bring it to market, you will need about 30% of the purchase price in cash (assuming a 25% down investment loan). So, at $300,000, you will need about $90,000. There are cheaper investment locations, but you cannot afford them.

Location

As long as you buy in a good location, appreciation, inflation, and rent increases will correct all but the worst mistakes. However, if you buy in a bad location, you can do little to turn things around after the fact. Below are three key location selection factors.

- Appreciation - The number one criteria in location selection is that prices and rents are rising faster than the rate of inflation. If you buy in a location where prices and rents are not increasing above the inflation rate, your income will be eroded over time by inflation.

- Population Size - Greater than 1 million. Small towns may rely too much on a single business or market segment. For example, a lot of experts recommended buying rental properties in areas where fracking was big. Today, I suspect a lot of people are seriously regretting following that advice.

- Population Growth - If people are moving into a location, many things have to be right. I would not invest in any location where the population is stagnant or declining.

You will not find any cheap properties in locations that meet the above location requirements. The price of properties is driven by demand; no demand, low prices, little or no appreciation.

Once you select a location, the next most important decision is the tenant pool.

Tenant Pool

To make money, the property must be continuously occupied by what I call a good tenant.

Good tenants are the exception, not the norm. Vacancy cost can be the largest expense after debt service or almost negligible, depending on the tenant pool. (Let me know if you would like to know more about selecting tenant pools). Once you identify a target tenant pool, you only buy properties that this tenant pool is willing and able to rent.

Investment Team

It takes a lot of skills to be successful in investment real estate. Either provide all these skills yourself (you can't) or work with an investment team that already has the skills. Below is a list of the necessary skills and the primary source for each skill (click on the image to enlarge).

There is no cost to work with an investment team and every advantage. If you try to do everything yourself, it will cost you more, and the odds of being successful are much lower. Do not make this mistake.

Good investment teams are hard to find. But with the right team, you will be able to execute the remainder of the process with minimal hassle. The place to start is with an investment Realtor. Know that even in a large metro area, there is likely only one or at most two investment Realtors. If you would like a process for finding an investment Realtor, let me know.

In Conclusion

Long answer, but I hope this will provide a process for buying properties remotely without buying from a turnkey provider.

Post: Investing in Vegas - best neighborhoods?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Account Closed,

Your experience is far different than ours. I believe the difference has to do with the tenant pool your properties target, the management company, and your service contacts.

Our clients and we own over 200 properties. They all target the same tenant pool. Our results over the last 15 years:

- Average tenant stay: 5 years.

- Average annual maintenance: about $350 plus the occasional water heater or air compressor.

- Average turn cost, less than $500. The low cost reflects our property selection process, the tenant pool we target, how we renovate a property, and the Nevada lease agreement. Regulations in Nevada, specifically the Las Vegas metro area, enable you to put a lot of the cost onto the tenant. For example, if any glass is broken in the house, the tenant is responsible. It doesn't matter how or why the glass was broken. When they move out, they have to return the property in a similar condition, except for reasonable wear and tear. They do have to have the carpets professionally cleaned, touch up paint, and many other tasks. So, the turn cost to the owner is very low.

- Evictions: 5 in 15 years

- 2008 crash - our clients had no (zero) decrease in rent and no vacancies. Property prices fell, as did all properties, but the income stream was unchanged.

- COVID - of the 200+ properties our clients and we own, five tenants had to move out due to job loss and such. To the best of my knowledge, all five paid 1 to 3 months penalty for early termination of their lease. And, the property was rerented in about a week at $100 to $300 more a month more. So, COVID and the eviction moratorium had little to no impact on our target tenant pool.

- YoY rent increase: 18% (July 2021)

- YoY appreciation: 19.3%. (July 2021)

- Time to rent in the current (crazy) time, <1 week. Under normal conditions, 2 to 3 weeks.

On property managers, we feel your pain. There are VERY few good property managers. We select one, work with them for a few years, they go bad, and we have to find another. (If you would like to read our paper on finding the right property manager, let me know.) Finding a good property manager takes interviewing dozens of property managers and a lot of research and time. (Hint: You cannot afford a property manager with a good yelp review.)

Our management costs are low - 8% of collected rent plus a $500 lease-up fee. Since our average tenant stay is 5 years, this is not a major cost. We also get reduced rates because of our volume. Some critical property manager characteristics:

- The property manager must be exceptional at selecting good tenants from your target tenant-pool or find another property manager. Tenant selection is a very difficult skill to master.

- Never work with a property manager with an in-house maintenance staff. Maintenance departments are a cash cow for property managers. I do not want my repairs to be a cash cow for the property manager. Also, I want the original invoice for all work and no markup.

- We specify which tradespeople the property manager will use. This greatly reduces our costs and increases quality.

- We have a detailed specification for the renovation company to follow. So far, the company had done well. They've probably renovated over 90 properties for us. We are about 80% of their total business, so if we need them working on Sunday, the only question we get is, "What time should I be there?".

Another frustration I believe you've experienced is managing your properties remotely. It isn't easy to find, qualify, renovate and manage properties remotely. You need a local investment team. However, there is rarely more than one such team in any metro area, and sometimes there is none. With a good investment team, remote investing is lower cost, easy and safe.

Of the 200+ clients we've worked with, only 10 to 15 live in Las Vegas. All our other clients live in other states or countries. We've never met half of our clients, and 1/3 have never been to Las Vegas. So, remote investing works, as long as you have a good local investment team.

Jack, I doubt any of this helped your situation but I hope it will help others.

Post: Investing in Vegas - best neighborhoods?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Sorry Laurie, I did not address your question on the best neighborhoods.

First, it depends on what you want to optimize; cash flow, appreciation, or a balanced investment. Most of our clients are interested in appreciation because they are building a future income replacement. Initially, optimizing appreciation may seem counterintuitive, but property values will rise faster than you can accumulate income in a rapidly appreciating market.

On specific neighborhoods, hard to give a simple answer. Every property targets a specific tenant pool. We selected a tenant pool many years ago and continue to buy properties that our target tenant pool is willing and able to rent. Below is a map showing where some of our client's properties are located. The green shaded area is where our data mining software finds over 90% of the properties.

On our target tenant pool performance:

- During the 2008 crash, our clients had zero decreases in rent and zero vacancies. The market value of their properties declined, but their rental income was unchanged. The crash was a time for our clients to load up on properties.

- During COVID, out of >230 properties, five to ten tenants had problems paying the rent and voluntarily vacated and paid a penalty to get out of the remainder of their lease. The properties were re-rented in days, usually at a substantially higher rent. The eviction moratorium had zero impact on our tenant pool. And, YoY rent is up 18%, and property prices increased 19.3% YoY.

- Average tenant stay is about five years.

- We've had five evictions in the last 15 years.

- Average turn cost is about $500. This is also a function of the landlord-friendly lease agreements that seem unique to Las Vegas.

I cannot provide a list of "good" subdivisions because it is more complex than just any house in a given subdivision. Some examples:

- Some floorplans in a subdivision that otherwise rents well may not do well at all. An example is split levels.

- Depending on the condition of the property, the renovation cost may be too much. Also, just because the property looks good to you does not mean it will attract your target tenant pool.

- Some streets within subdivisions do not rent well. In most cases, we do not know why; we have the data that proves this. We have identified 2,065 streets as of today that rent poorly.

- The location within the subdivision can be any issue. For example, targeting young families and the house near the subdivision entrance takes longer to rent and rents for less.

- If any dimension of the master bedroom is less than 12', the time to rent increases. For example, a property with a 18x11.5' bedroom will take longer to rent than a 12x12' master bedroom.

I could continue, but I hope you understand that there is not an easy answer to the good subdivision question.

A frequent question is what database we are using. There is no public (paid or free) database with the property and tenant pool level data needed to evaluate properties. We've been accumulating our data over at least ten years. And, we continue to learn more about the market as we continue to collect more information.

If I had to give a simplistic answer, I would generally describe "good" investment properties as:

- Property prices between $300,000 and $425,000

- 3 or 4 bedrooms

- Bathrooms vs bathroom must be: bathrooms >= bedrooms - 1

- No pools or in-ground spas.

- Only tile roofs

- Probably built since 1990

- 2+ car garage

- Reasonable HOAs are very desirable and typically get higher rents.

- Do not buy three-story or split-level properties.

I hope this helped.

Post: Investing in Vegas - best neighborhoods?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Bill B.,

Another great post. Thank you!

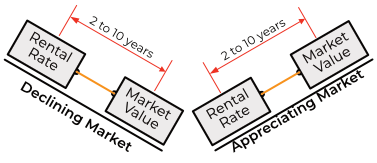

I agree with your assessment on rent increases not matching prices in the short term. According to the research I've read, there is a strong correlation between rent and property prices. Depending on the market, rent lags property prices by 2 to 10 years. So, rents will catch up to price increases, but it will take time. The same is true for declining markets. See the image below.

In declining markets, any market where appreciation and rent increase slower than the inflation rate, the rent today reflects property prices from 2 to 10 years ago. That is why declining markets tend to have a higher initial return than appreciating markets.

However, along with higher initial rent comes a guaranteed long-term decline in inflation-adjusted dollars. I've had questions on this, so I will use an example.

A couple of years ago, a client did a 1031 Exchange from a popular mid-western investment location. He was pleased with the performance of his property but felt the area was getting rough and would not continue to do as well in the future. Below is what he originally paid for the property and what he sold the property for.

He was happy the rent and the price both increased by 10% over the hold period. But what actually happened? Before I continue, a little about money and the effects of inflation.

Money in and of itself is of no value. The value of money comes from the goods and services you can buy with money. Inflation is the decreasing amount of goods and services the same amount of money will buy over time. Below is a chart showing how much money it would require today to buy the same basket of goods you bought in 1990 for $50.

Back to the mid west property. What actually happened is that he lost money on both the rent and the sale price, if you correct for inflation or buying power. If I assume 3% inflation, here is what happened:

- $900/Mo. in 2009 dollars has the same buying power as $1,174 in 2018 dollars. So, the $1,000/Mo rent he was receiving was actually a 17.4% decrease.

- $100,000 in 2009 dollars has the same as $130,477 in 2018. So, a sale price of $110,000, was actually a 15.7% loss.

My point is that you need to think of buying power and not just the number of dollars. If property prices and rents are not rising faster than the inflation rate, your income is declining over time, guaranteed.

How Are Things in Las Vegas?

For the narrow segment of properties we target, YoY rent increased by 18% and prices increased by 19.3%. See the charts below.

Rentals - Median $/SF by Month

Sales - Median $/SF by Month

So, things are going very well for our clients. And, we are seeing excellent returns from the properties we close each month.

The Eviction Moratorium is...Maybe Not Over?

The "experts" are predicting an eviction apocalypse. One of the advantages "experts" enjoy is that any prediction is probably right somewhere at some time. Just not in Las Vegas at this time. I will explain.

How the (eventual) end of the eviction moratorium impacts the rental market depends on the tenant pool. In Las Vegas, we have three primary tenant pools:

- Transient - This tenant pool is primarily low-skilled hourly workers making little more than minimum wage. Whenever there is economic turbulence, they are the first to be laid off and the last to be rehired. When you hear about tenants not paying rent during the moratorium, this is the tenant pool segment. These are the primary tenants for C and most -B Class properties, of which we do not target.

- Permanent - This is the tenant pool we target. Very few were laid off during the 2008 crash, and the same is true doing COVID. So, this tenant pool was largely unaffected by either event. Also, the driving factor for this tenant pool segment is not an eviction (having to move); it is the credit impact. They know that if they have a late payment, let alone an eviction, they will not be able to rent an A-Class property again. Their only option will likely be moving to a C Class property with unsafe and terrible schools in a bad area. In my opinion, this tenant pool will rob gas stations to pay the rent. So moratorium or not, this tenant pool performs.

- Transitional - This tenant pool has a high enough income that they are typically home buyers. They typically only rent if there is a major negative event in their lives. Once they sort out the problem, they will buy a home. The 2008 crash seriously impacted this tenant pool and some were hurt during COVID. We do not target this tenant pool.

Transient tenants are the primary tenant pool that have not been paying rent. However, even with Transient tenants, I disagree with the “experts” that there will be a tenant apocalypse. The “experts” forgot that all Transient tenants will need a place to live and all landlords will need tenants. So, some shuffling around will occur but not a lot more.

Will the landlords of C and most B class properties ever get paid for the back rent? In my opinion, most will not. When I was working with property managers handling C-Class properties, I heard many times that most of this tenant pool have multiple evictions and skips in their past. So, the threat that they might get evicted again is not an issue. And, why should this tenant pool bother filling out paper to get rental assistance money to give to someone else when another eviction has no impact on them at all? I think many landlords of properties targeting C and B class properties are unlikely to get past rent. This is another example of why C Class properties do not measure up to the paper returns.

So much for today and my prognostications!

Post: Out of State Investing for Cash Flow

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Michael Castillo,

Great that you are doing your due diligence on an investment location. Instead of listing cities that might be good investment locations, below are some considerations that will help you evaluate locations. Remember that you will hold the property for many years so look beyond initial return.

ROI is a Snapshot in Time

Return metrics, like ROI, are only a snapshot in time. ROI estimates how the property is likely to perform on day one of a lifetime hold. ROI tells you nothing about how the property will perform in the future.

For example, suppose you are considering two properties in different markets with the same initial ROI. Property A is in a market where rents are increasing above the rate of inflation. Property B is in a market where rents are increasing below the rate of inflation. Over time, Property A's inflation-adjusted cash flow will increase while Property B's cash flow will decrease.

Another example, suppose Property A has a lower initial rate of return than Property B. If you based your decision only on the initial return, you would choose Property B. As you can see, Property A is a much better long term hold.

My point is that you must look beyond the initial return; you will be holding the property for many years, and you need the inflation-adjusted income to increase over time. After all, your living expenses will be increasing.

Location Considerations

Below are some of the more important considerations I recommend when evaluating locations.

Population SizeI would only consider metro areas with a population greater than 1 million. You want a stable economic environment, and small towns may be too dependent on a single company or commodity. Here is a list of metro areas ranked by population.

AppreciationAppreciation is an excellent economic health indicator. When properties appreciate, demand is increasing. Demand will only increase if new jobs are being created, people are moving into the location, the government is not oppressive, and many other things have to be right. However, I would never consider any location where rents and prices are not increasing above the rate of inflation.

CrimeWhile crime is everywhere, crimes occur in some locations much more frequently. Properties in cities with high rates of crime are unlikely to do well over time. Few people would choose to move to such a location and people with sufficient income will move away to a safer location. Median income in the area will fall as well rents and property prices. Also, Employers are unlikely to open new operations in high-crime areas either. Here is one list of high crime cities. I would not invest in any city that appears on this list.

Population ChangePopulation change tells you a lot about a location. If the population is increasing, many things have to be going well. Also, with a growing population comes rising demand which will result in increased property prices and rent.

If the population is decreasing, there are serious issues. Moving to a different state or city is an expensive proposition, both in terms of stress and expense. Things have to be pretty bad to motivate a significant number of people to move away from a location. I would not consider any location without a rising population. Here is a list of metro population changes between 2010 and 2019.

JobsA property is no better than the jobs around it. However, it is not just the jobs your tenant pool has today. Except for government and utilities, the average lifespan of a company is about ten years. Even companies listed on the S&P 500 only have an average lifespan of 18 years, and it is declining. So the jobs your tenants have today will vanish in the next 10 to 15 years. The location will only stay economically viable if new companies are moving into the location, creating new jobs requiring similar skills and paying a similar wage.

The best way I know to quickly assess the economic health of a location is median household income. If the median household income, adjusted for inflation, is not increasing, the location is in decline. The St Louis Federal Reserve is my go-to source for such information. As an example, here is a link to median household income for Las Vegas (Clark County).

TaxesState taxes (income and property) are a good metric of the cost of doing business. The so-called "Blue" states are examples of where the cost of living and doing business is unreasonable. The high cost of living is why so many people are leaving these states. I would never invest in states with high income (or property) taxes.

Michael, I hope the above will help you to evaluate potential investment locations.

Post: Las Vegas Bound! Neighborhoods?!

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Da'Mario Hughley,

As @Michael Robbins said, it depends on your investment goals. I will share ours so you can use it as a starting point for what you are seeking.

I believe every investment property must meet the following three criteria.

- Sustained profitability - The property must generate a positive cash flow today and into the foreseeable future, in good times and bad.

- Appreciating - Appreciating at or above the inflation rate. The properties we target had a YOY increase in rent of 14.3% and appreciated 18% (May 2021).

- Low Operating Cost - In a location where operating costs are low and regulations favor investors.

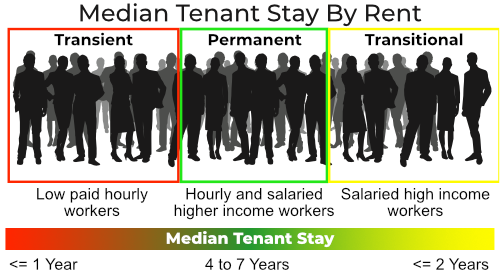

When I first moved to Las Vegas (about 16 years ago), I did a lot of research concerning tenant pools. I started with defining the characteristics of what I call a "good" tenant. Next, I researched which tenant pool segment had the highest concentration of good tenants. I then translated this tenant pool's needs and wants into physical property characteristics. These are the properties we target. Below is a high-level view of what I learned about the three major tenant segments.

Tenant Pool Segments

While segment generalizations may not apply to any specific individual, generalizations are useful when evaluating segments because most members share common behaviors. As an example, I will focus on the frequency of tenant turns by tenant pool segment.

In my research, I've found that tenant stay has a strong correlation with income, as shown below.

Comments on the three tenant pool segments:

- Transient - This tenant pool is primarily low-skilled hourly workers making little more than minimum wage. The typical renovation cost per turn is $1,500. The average tenant stay is one year. The average rent is $850/Mo. The average time to rent is eight weeks. When you hear about tenants not paying the rent due to Covid, this is the tenant pool they are talking about.

- Permanent - This tenant pool could be hourly or salaried, but they earn well above minimum wage. The typical renovation cost per turn is $500. The average tenant stay is five years. Typical rent $1,500/Mo. Typical time to rent, two to four weeks. This is the tenant pool that we target.

- Transitional - This tenant pool has a high enough income that they are typically home buyers. They typically only rent if there is a major negative event in their lives. For example, a divorce, the death of a spouse, etc. Once they sort out the problem, they will buy a home. The typical tenant stay is two years. The typical renovation cost per turn is $2,000. Typical rent $2,500/Mo. The typical time to rent is eight weeks.

How has the "Permanent" tenant pool performed for us?

- Average tenant stay: 5 years

- Number of evictions in the last 16 years: 5

- Average turn cost: <$500

- 2008 crash performance: zero decrease in rent, zero vacancies

- COVID performance: Out of >200 properties, 5 tenants had trouble paying and moved out.

Properties That Attract Our Target Tenant Pool

The majority of our properties are single-family and a select set of townhomes. We've investigated condos in the past, but they have multiple limitations, including an average tenant stay of about two years, financing restrictions, and the high HOA fees limit profitability. Below is a map showing the areas in which we find most of the properties (green) and the location of some of our client's properties. Note that while the green area appears homogeneous, in actuality, it looks more like Swiss cheese.

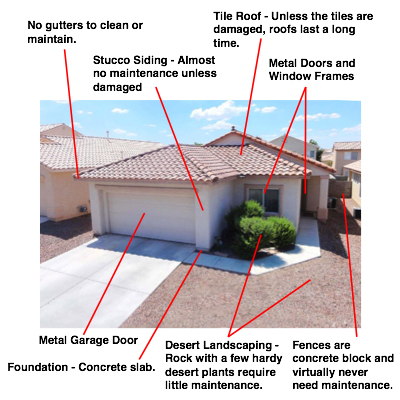

Many new clients ask about condos because they have concerns about high maintenance costs. Due to the properties we target, construction, and our process for selecting properties, our average maintenance cost is between $300 and $400 per year, plus an occasional water heater or AC compressor replacement. This is similar to maintenance costs for condos. Below is a typical property that we target. As you can see, there is not a lot to maintain.

Some thoughts for your consideration:

- Select your target tenant pool first and then buy properties that this tenant pool is willing and able to rent.

- Find a good investment team. If you would like information on selecting an investment Realtor, let me know, and I will post it.

- I would not pre-judge the type of property to buy. I would buy properties that generate the highest net return today and continue to do so into the foreseeable future.