All Forum Posts by: Adam Macias

Adam Macias has started 62 posts and replied 233 times.

Post: First time Flipper (Starting with $13,000 in reserves)

Post: First time Flipper (Starting with $13,000 in reserves)

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

Quote from @Evan Alexakos:

I've been interested in real estate for the last couple of years and just graduated from college. I'm taking a gap year before heading off to law school and desperately want to get started. As of now, I have $13,000 and a dream to get into real estate. FHA loans, househacking, and BRRRR are other possible starts, but I am in a situation where they are either not possible or not preferred. Is it possible to get into flipping with $13,000 of my own cash? Can I target trailers as a viable option? Should I look into family and friends who I know are willing to invest in the first property?

I'd prefer to do it without having to borrow money, but I can also borrow. If anybody has an interest in sharing tips with a newbie and future real estate investor, I'd very much appreciate a conversation.

Think in terms of master and apprentice.

That helped me immensely.

You have a good amount of marketing money, and that's all that money should be focused on.

Totally just my opinion, but you must master finding deals.

That's where all the money is in this business is the lead generation.

Without leads for flips, you have no business.

Because you can just partner with an investor who has more experience than you.

That's why I did 10 years ago with a really good friend of mine now.

Instead of wholesaling, I just brought him leads, we agreed on a 20% cut for

me on the total profits of the finished sale.

Which meant zero risk for me anyway because all I did was spend a little money

on marketing. There's tons of investors that'll do this with you.

No guru needed, no wholesaling needed, totally doable.

Just make sure you have the proper agreements in place to people are honest and the numbers are clear.

Post: Who determines the price of a house?

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

Quote from @V.G Jason:

The first party in the transaction usually dictates the price. That's usually the seller via the realtor.

The seller has the right to list at whatever price they want. The market may not respond to it, but that's the market. Not the price.

Speaking past theory, and in the real world 99% of buyers have no idea what the price is and the realtor's abilities to seize the emotional disarray is what actually makes it sell. Right now, the banks are the actual stopping point-- less approvals, less closings, stricter terms.

I spoke with a seller in probate today who listed with a Realtor two months ago for $525k, it didn't sell, they did two price drops, had 50+ people come look at it..

The Realtor and PR BOTH listed it for what they dictated..

AND IT DIDN'T SELL.

Why?

Post: Atlanta Realtor | Helping Investors Find Cash Flow Deals in North GA

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

Quote from @Tripti Jindal:

"Hey, I'm Tripti Jindal, a Realtor® with Keller Williams / Mangla Realty Group in North Atlanta. I focus on helping investors analyze deals in Cumming, Suwanee, Duluth, and Alpharetta — especially rental ROI and cash-flow properties. If you're ever looking at this market, happy to share numbers or recent comps. Always glad to connect with fellow investors!"

Welcome to the BiggerPockets Community Tripti!

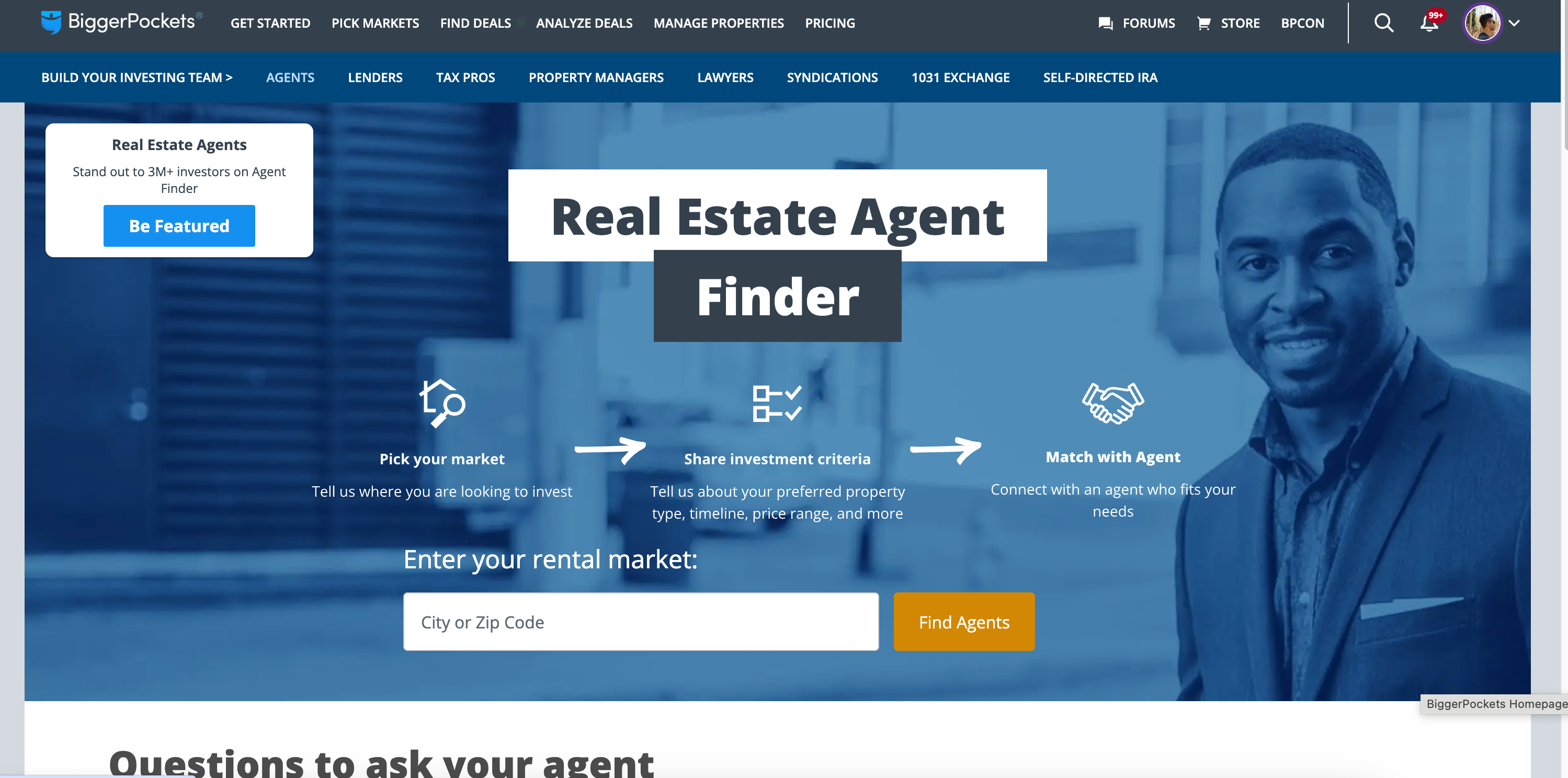

Post: BiggerPockets is looking for real estate agents in Denver!

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

Quote from @Benjamin Louie:

@Adam Macias

Hey Adam, thanks for sharing! This sounds like a great opportunity for agents in Denver to connect with active investors. I’m curious what does the process look like for qualifying leads and ensuring they’re ready to work with an agent? Would love to learn more.

Hi Benjamin! I'll send you a DM!

Post: I did a test asking agents on Zillow one simple question..

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

I did a test asking agents on Zillow one simple question:

"Morning Crystal! It's Adam Macias. What type of buyers do you typically work with in Denver?"

It was three different variations of just asking this simple question.

I think it was about a 75% reply rate of saying "STOP"

or "Not Interested".

Now what's the major problem here with this whole situation?

Because I've been to meetups and asked agents that and didn't

get a "OPT OUT" reply lol you know how weird that'll be?

It's actually Zillow itself.

Zillow doesn't protect your information because it's just a

massive directory exposing all your contact information.

So, the number on Zillow is your "Zillow number", trust

and same with the email.

"leads@ yourwebsite" is an obvious filtering mechanism.

me as an avid marketer I know what you're doing and you're systems lol

So it's not the message, it's the avenue itself.

Luckily for Featured Agents, clients come through a filter

first so we know they are serious, we have two factor

authentication to ensure this even further to reduce spam.

And only THEN can a buyer client select an agent to work with

based on the information they see in how an agent can help

them and their specific situation.

Much higher quality lead means a much higher conversation

rate and overall long term relationship with that client

to get repeat business.

The difference is one offers the ability for you to spend

too much time sifting and sorting and getting distracted,

and one avenue, (us at BiggerPockets), let's you focus

with intent only with those who are serious and want to

speak with YOU specifically because they need your help

in buying a property TODAY.

Post: I read a study that showed 64% of Americans

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

I read a study that showed 64% of Americans from Ramsey

find buying food being their number one stressor.

That's wild to me.

It wasn't even housing or a car payment anymore.

So it's telling me people have realized they are STUCK

in there current position so it makes no sense to worry

about moving, buying a house, or luxury like vacations.

Food is the biggest stressor because money is taken up

elsewhere.

But how I take it is people have made the conscious

decision to stay put and make the most of their current

living situation.

So if you're not hounding and pushing to find qualified

buyers, this is why you'll have a listing sit on the market

for 76 days and then go, "idk why".

Well I know why, it's not 2020 ANYMORE FOR THE LAST TIME.

2020 messed up a lot of people in the head in thinking

what a normal market is.

Think of all the scenarios and situations we were in,

and y'all think that's a normal market? lol

Times change.

Policy changes.

People seldom do.

Post: I just can't imagine a Real Estate Agent not taking advantage of this.

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

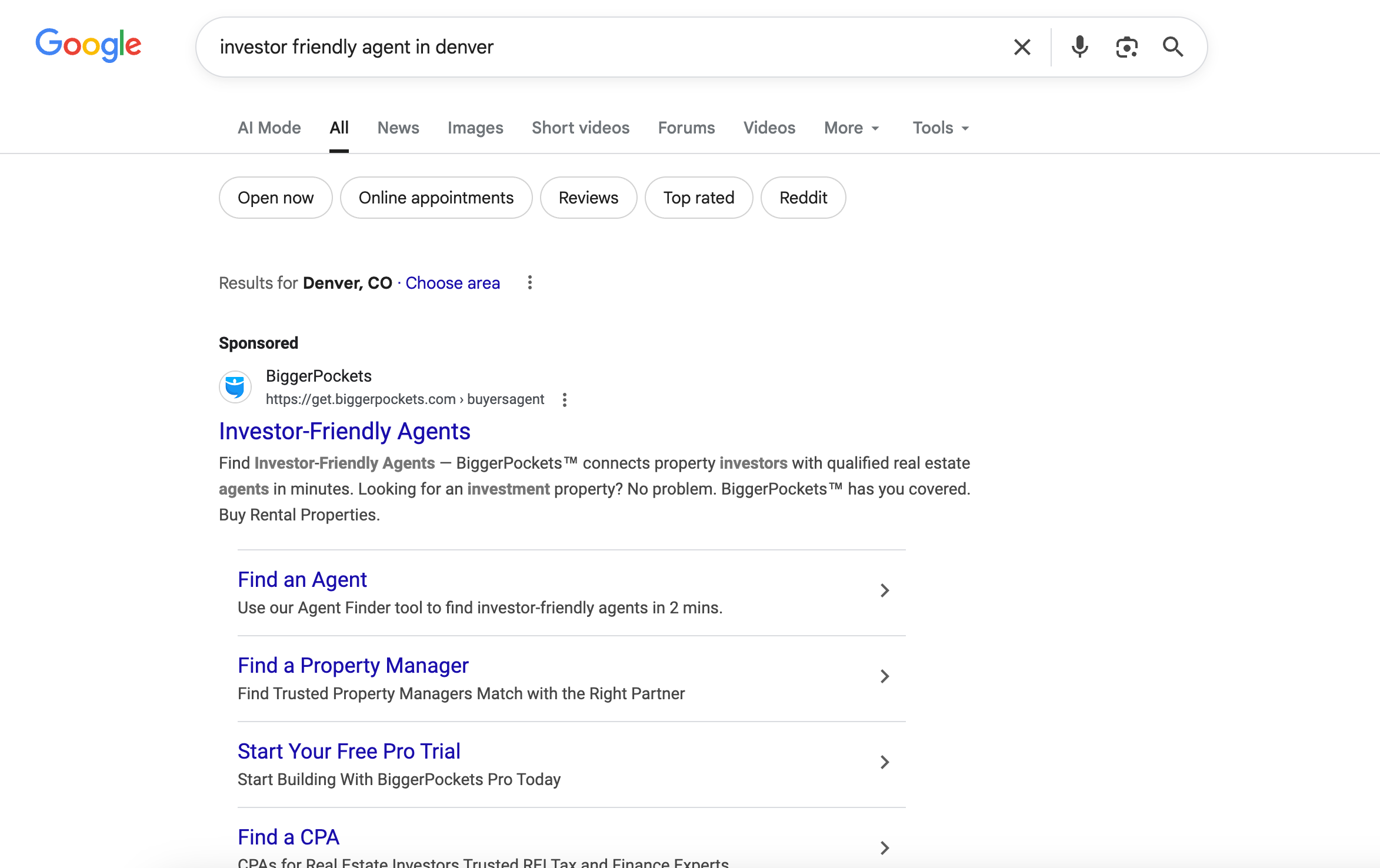

We dominate investor + agent keywords on Google.

This is on the paid and SEO side combined too.

I saw the data, THOUSANDS of investors every month

search keywords like "investor friendly agent" and others

all over the country and we at BiggerPockets show up at

the top every time.

I just can't imagine a Real Estate Agent not taking advantage of this.

All it takes is a message to me here on BP to learn how

to get repeat business like Craig Curelop, and many others have.

Just Google Craig's name, he even wrote a book for us.

That's how powerful leveraging our platform is.

Not only do you get solid buyer clients to work with,

it expands your network 100x.

Cheers!

Post: Who determines the price of a house?

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

Quote from @Ken M.:

Quote from @Adam Macias:

Quote from @Ken M.:

Quote from @Adam Macias:

Who determines the price of a house?

It's always the buyers.

Always. Always.

It's not the Realtor.

It's not the Seller.

It's not the Appraiser.

It's not Zillow.

It's not the News.

Only the buyer.

Doesn't matter if it's 70% of it's ARV.

Or if it's $100k over asking.

So having the right buyers is the

most vital piece of a successful RE career.

.

Well, half right. If that is changed to "Cash Buyers". Few and far between in this market. A seller is not required to sell though, which means if he disagrees on the offer, the house can sit for an indeterminate amount of time at an indeterminate value.

Buyers can't get financing if the appraiser doesn't give the value necessary to support the financing, no matter what the asking price or offer price is.

Sellers can't sell for less than what is owed to the bank, if the bank won't do a short sale and reduce the amount owed to what new financing will allow.

A lender will pull back the loan if a defect in the property makes the property uninhabitable.

There are a lot of reasons a sale will fail.

"A house is worth what a willing seller will sell for, to a willing buyer who has the ability (money) to close." Isosceles circa 1306

Actually, this proves my point entirely. It's still all about the buyers you have regardless of the scenario. If you only have "cash" buyers well then there's no room for retail homes.

If you only have retail buyers, you miss out of the fixer upper opportunities.

Your buyers determine how well you do in this market.

A buyers list of a variety of clients determines the ability to go out and shop for what they're looking for.

Actually, you goal determines the type of buyer you will accept.

That's only ONE buyer in a sea of buyers. I remember having a house I was wholesaling in Aurora, one buyer wanted it $30k below, one wanted it at asking, one wanting it $10k above. It's all about how strong of a buyers list you have.

Post: BiggerPockets is looking for real estate agents in Denver!

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

My name is Adam, and I work with the BiggerPockets Featured Agent Program!

We’re looking for a few real estate agents in Denver to fill openings in our Featured Agent Program, so if you’re an agent I’d love to talk with you about receiving what I personally think are some of the best leads on the market!

Think of it this way - there are millions of Biggerpockets members, podcast listeners, and Youtube subscribers who are actively investing - BUT THEY DON’T HAVE A REAL ESTATE LICENSE LIKE YOU DO.

That’s where you come in - we need rockstar agents like you to connect these leads that are ready to go and want to work with you specifically.

If you’re interested in learning more about receiving leads from BiggerPockets or know someone who’s interested, just send me a message and we can start a conversation to see if it would be a fit for you.

Or, just message me if you want to talk more about it.

Happy Investing!

Post: Who determines the price of a house?

- Real Estate Consultant

- Fort Collins, CO

- Posts 247

- Votes 151

Quote from @Ken M.:

Quote from @Adam Macias:

Who determines the price of a house?

It's always the buyers.

Always. Always.

It's not the Realtor.

It's not the Seller.

It's not the Appraiser.

It's not Zillow.

It's not the News.

Only the buyer.

Doesn't matter if it's 70% of it's ARV.

Or if it's $100k over asking.

So having the right buyers is the

most vital piece of a successful RE career.

.

Well, half right. If that is changed to "Cash Buyers". Few and far between in this market. A seller is not required to sell though, which means if he disagrees on the offer, the house can sit for an indeterminate amount of time at an indeterminate value.

Buyers can't get financing if the appraiser doesn't give the value necessary to support the financing, no matter what the asking price or offer price is.

Sellers can't sell for less than what is owed to the bank, if the bank won't do a short sale and reduce the amount owed to what new financing will allow.

A lender will pull back the loan if a defect in the property makes the property uninhabitable.

There are a lot of reasons a sale will fail.

"A house is worth what a willing seller will sell for, to a willing buyer who has the ability (money) to close." Isosceles circa 1306

Actually, this proves my point entirely. It's still all about the buyers you have regardless of the scenario. If you only have "cash" buyers well then there's no room for retail homes.

If you only have retail buyers, you miss out of the fixer upper opportunities.

Your buyers determine how well you do in this market.

A buyers list of a variety of clients determines the ability to go out and shop for what they're looking for.