All Forum Posts by: Jamie Parker

Jamie Parker has started 36 posts and replied 244 times.

Post: Whats more important: $100,000 or 10,000 calls?

Post: Whats more important: $100,000 or 10,000 calls?

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

@Joe Villeneuve the reinforcement is beautiful. "Don't give in to get deals". That's how I got the 5k. Also had a 30k deal fall apart. After being resuscitated twice, and 3 price changes. 8 months was just too long for one of the equity partners and bam. 35k isn't 100k but it looks better in a post than 5k.

Many of the leads from last year are still available so solving the problem and sticking with it could be the difference.

Post: Whats more important: $100,000 or 10,000 calls?

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

Quote from @Caleb Brown:

Love the consistency but others have made great points. To only close 1 deal after 19K calls is rough and there is something wrong in your process. It can be a variety but you need to look at every step to see where the fall off is. Are you not contacting good potential sellers? If you do contact is your script able to progress to the next step(offer or walk through)? If you do walk through is your presentation off or are you off on the numbers? If you do get under contract are you marketing these deals well enough? There is so many things to look at but you need to focus on more then just volume. You need to track other metrics to truly fine tune this or I'd do something else that's worth your time. A thought is to join up with a wholesaler(that's established) to learn the ropes, do their calls for them. You can earn money while learning what they do.

Consistency in the action of calling was the whole point of the conversation. However I like the feed back. Getting deals under contract has been tough. I posted in another form about my numbers. They dont work (65-75% ARV). Watching the market, seeing what is being rehabbed 80-85% ARV. Investors are simply paying more, and I doesnt make sense to me. On the development side, which is most of my prospecting, most of the sellers are simply not realistic about the asking price. 800k for 3 single builds lots when new construction is going for 550-750K in the same area. Maybe they want to sale but not as motivated, it's an interesting dynamic.

Never like to be the guy to blame the market, so the advice and concepts presented Ill take ownership of and measure accountability of that. Follow up with sellers may yield the fruit of last years initial, 2nd and 3rd contacts.

Post: Whats more important: $100,000 or 10,000 calls?

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

Quote from @Joe Villeneuve:

Quote from @Jamie Parker:

Quote from @Joe Villeneuve:

What happens when you make 10,000 calls, and get very little money out of it? The number of calls you make, are only important if you are guaranteed a specific dollar in return per call. Are you?

Dollars outweigh calls every day of the week.

To me, what appears to be the problem isn't setting the goals, or choosing the goals, but having a plan of how to get there. Simply making more calls doesn't guarantee money. That's the throwing you know what against the wall, and hop0e plan. Not a plan. What sticks is based on how you throw it, not how many you throw.

Your problem is probably your method of wholesaling.

Setting a goal doesn’t merely guarantee the outcome by course. The only way to ensure a goal is commitment to the input. I can’t make someone sell their property, some people will not be reduced to a dollar amount. Are my sales skills top notch, no. Do I have the instincts to overcome every objects, no. Have I missed some deals during this process, of course. But if, by whatever course of action, I am not committed to taking the necessary action the goal will never nothing more than a goal.

Just for numbers sake, there are some YouTubers doing 10,000 calls, 10s of thousands text messages and 10,000 mailers a month. I don’t have the budget to support but one lead source at a time. Networking at this time can only be done by phone. Fortunately, I have a few contacts to use. Of which I’ve done 1 deal with. I’m not looking to make a living making phone calls, but without a budget, you gotta start somewhere.

I sill tell you this, the reason why others that are successful might be doing 10,000 calls isn't because they are focusing on the number of calls. They do that many because they have a successful system that allows them to do that many. The number isn't a goal, it's a result.

So, what's you system?

First, where/how are you getting these numbers to call?

Second, when they answer the phone, what happens next,...from your end, not there's?

After 8 months of hacking at it, I have a real answer. Offers. Making more offers is the gap that I have to close. Taking the first "No" in conversation will result in speed running a list. Getting in the habit of overcoming "No" leaves room for more possibility.

In terms of systems. Being honest I dont have anything I would call a system at this time. Call, track and follow up is all I got for now. Within that simple framework, an additive measure is increasing opportunity to make offers.

Secondly, Networking and meeting with other investors in my area. That could help out also. I havent done much of either at this point. but thats what happens next.

I get my numbers skipped traced on Fiverr. I get the list from county records. When they answer the phone I ask have they considered or are considering selling their property. Thats all I got locked in so far.

Post: Whats more important: $100,000 or 10,000 calls?

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

Quote from @Chris Seveney:

Quote from @Jamie Parker:

With about 2 weeks to go in the year, Have you considered what your goals are for next year? Have you reached your goals for 2024? It has taken the last 6 months of the year to come to terms with an essentially game changing mindset:

"Track the input and let the effort determine the outcomes"

Initially I wanted reach a goal of $100,000 in a year wholesaling real estate. By May 2024, I realize the goal was crushing me. I found myself, trying to sell deals, not standing firm on the numbers. Ultimately I wasn't able to contract anything. Desperation begin to set in, almost like the opportunity was fleeing me. Even made 4 or 5 offers that were scoffed at initially, but ultimately sold at that price to another investor. I realized my confidence was lacking.

Around that time, I begin working with an accountability coach and establishing some small goals, embarrassingly small,...5 calls a week. I struggled to wrap my head around, 5 calls a week, at first. Then after a couple weeks the goal moved to 10 calls a week. By the end of June, I struggled to find 20 calls to make.

By July 2024, I decided to try a different approach. I built a list and skip traced 750 addresses. That lead to 20 calls a day, then 50, then over a 100 a day. After a month, my first contracted deal in over 5 years as a wholesaler (own 2 properties 2023/2024). For the next month, I tried to find a rhythm but struggled find consistency in effort. After the first deal closed, something changed.

"Track the input and let the effort determine the outcomes"

This mindset took the pressures of outcome, off the table. This has been my biggest discovery, in life.

¡¡NOW I HAVE A GOAL!!!

10,000 Calls Made

Where I started 2024 and where I am finishing, two difference places. My mindset is absolutely stronger because it only reflects my ability to do the work. Life can be many things, can take us many places. If you do the work. For those that may be wondering, No, I DID NOT make $100,000 in real estate in 2024. More importantly, I can start off 2025 with a realistic foundation. In this situation 10,000 calls has been more important that making $100,000 in 2024. But, next year....

You need leading and lagging goals/indicators. 10,000 calls may be a great goal but if the lagging indicator is that brings in $10,000 where as going to five REIA events is a goal and brings in $10,000 which is better? You need to work backwards (EOS is a great way to do this) where you start with your lagging goal of where you want to be, but then you need to understand what it is that gets you there and break it down by quarterly milestones then tasks to get to that milestone (for example if its making 2500 calls a quarter and you do not have phone system or software, that would be a task to keep you moving).

That makes sense, EOS breaks down the year into quarters then the quarters into quarters to maintain goal orientation. set a 90 day goal, then track inputs to reach that goal. Tweak and peak if goals is missed or duplicate if goal was reached.

Post: Whats more important: $100,000 or 10,000 calls?

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

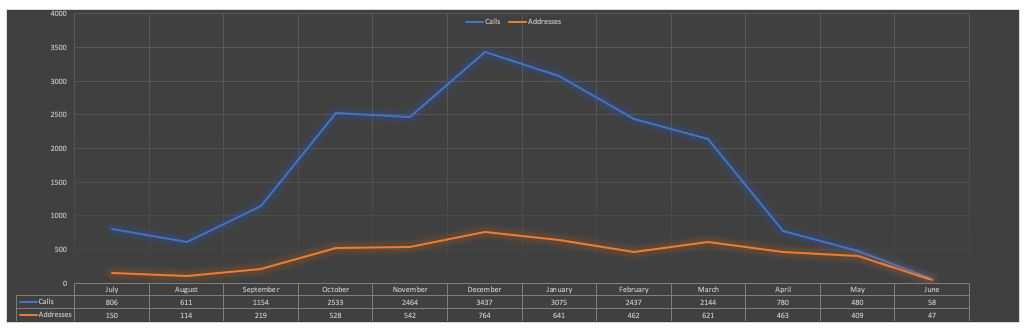

Update:

At the 6 month point of starting, I was riding high on momentum. By the 1 year mark, July 2025, everything came to a screeching halt.

Year 1 Totals

Calls: 19979

Addresses: 4960

Deals: 1

1 year of calling for $5,000. Such a letdown, and there is no way to brush it under the rug. A lot of effort and not a lot to show for it.

Takeaway 1:

What is the system used to make calls?

Before getting into applications and tools,

What are the steps:

- Initial contant

- Filter between "Call again" and "Don't Call Again"

- "New List"

- Follow up with "Call Again" in "Follow Up List"

If they aren't ready yet (not qualified sellers)

- Mix in with "New List"

- "New List" "Call Again" Mixed together for "Follow Up" List

Repeat.

One part that not fully exercised was prospecting buyers!!

Networking with buyers is a part of the game that I did not fully capitalize on.

Realizing this late May and Early June, I was wrong in this approach and decided to pause and reallocate prospecting time to develop buyer relationships with greater intention.

Day 2 of year 2, this year will be exciting.

Post: Looking to Connect with Wholesalers in Memphis

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

Quote from @Thomas Scott:

Hi,

I am an out of state investor based in New York. I am a Builder and a Firefighter so I do not have time to source deals. I am looking to connect with wholesalers in Memphis only.

Thanks,

Tommy

Hello Tommy,

I was Navy Fire Fighter for 7 years. I would like to know more about what type of projects you are looking for. New construction, Buy and Hold? I agree with Jordan MIG and Facebook. My facebook was hacked 4 years ago so I am on here and linkedIn. IF you would like to hop on a call, feel free.

Post: Failed BRR in Memphis TN

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

@Jaycee Greene@Sean Dempsey hopefully they do the right thing.

Post: Just Closed My 200th Deal in Louisiana – Ask Me Anything

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

@Stephen Keighery that's great advice. What was the time frame, from starting a new market and stabilizing the market to prepare for the next market?

Post: Just Closed My 200th Deal in Louisiana – Ask Me Anything

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

Hey@Stephen Keighery congratulations on 200!!

When did you know that it was time to expand from the first market into the second and third ones?

Post: How are you analyzing Fix and Flips in 2025 (Mines Not Working)

- Real Estate Investor

- Memphis, TN

- Posts 274

- Votes 89

Anyone want to do a walk through with me in Clarksville, TN? If you are a flipper its your deal, I am looking to get some pointers on walk throughs as far as estimating repairs goes.

Dm me.