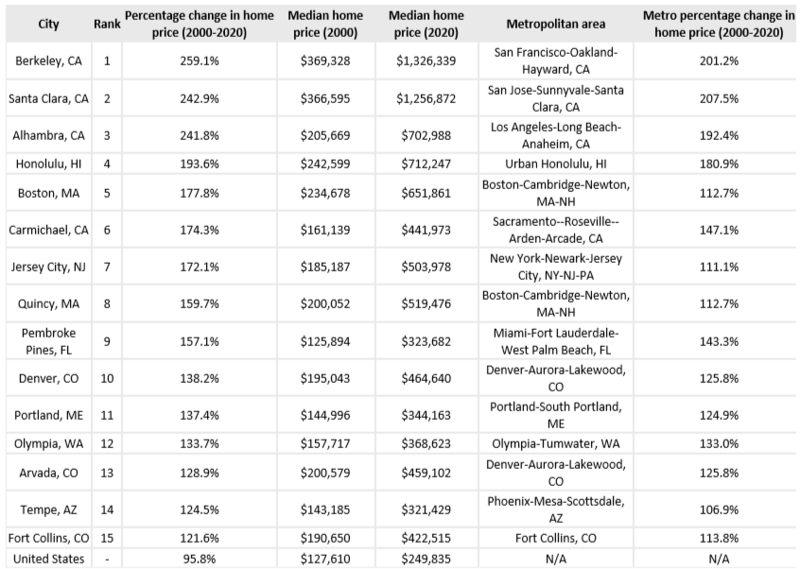

The best and most recent example of local government action that demonstrates the risks of rental property ownership in the East Bay (Berkeley and Oakland) is the City of Oakland's sneaky removal of exemptions from rent and eviction controls for duplex and triplex owner-occupants.

A voter-approved measure effective in January 2019:

- removed exemptions for owner-occupied duplexes and triplexes; and

- allowed the city council to add limitations to the law without an election.

Owner-occupied duplexes and triplexes were previously completely exempt from BOTH rent control AND eviction control. Those exemptions made 2-3 unit properties in Oakland attractive for investors.

The voter measure removed the exemption from eviction control for small property owners. That was somewhat of an inconsequential loss because at the time, there was no restriction on rent increases. So, if you had a tenant living under your roof that was a lot more work than normal, you could simply reset the rent to an appropriate level since rent control did not apply.

But notice the second provision in the voter-approved measure. When the voters ceded their right to approve future changes, they gave away the farm.

The Oakland City Council promptly adopted a moratorium on rent increases. They did so without any opportunity for public input. They then proceeded to conduct a rulemaking to impose rent control on duplex and triplex owners. That rulemaking concluded about a month ago. So now, owner-occupied duplexes and triplexes (except for units that are exempt as new construction, as defined by Costa-Hawkins) are fully regulated instead of fully exempt from rent and eviction controls. Most homeowners that were aware of the City's plans to adopt rent control expected to have some time before their exemption were fully revoked. But the city's strategy was to revoke those exemptions before the homeowners could make any adjustments.

There are likely thousands of owner-occupied duplex and triplex owners in Oakland who probably still do not know about this - i.e., that they have TOTALLY lost what previously was full control over who gets to remain under their roof, how long they get to stay, and what rent they will pay now and in the future. Very few of the affected homeowners recognized that the new rules would lock their rents at existing low levels and that the tenants they currently had might become permanent. Those who failed to act are less likely to be able to cover long term costs.

The clever maneuver by the Oakland City Council locked existing below market rents in place but did so in a way that most certainly will prevent many homeowners from making a fair return on their investments and will cause others to lose money on their investments. So, investors should keep an eye on any court actions resulting from the rules slipped into place by the Oakland City Council.

In Oakland, the annual CPI rate for rent increases effective July 1, 2019 through June 30, 2020, is 3.5%. This not as bad compared to Berkeley, where the annual increase for more than a decade has been 2% or less.

Since duplex and triplex homeowners are much more likely than apartment building owners to rent at below market rates, the new city rules in Oakland seem clearly to have been designed to intentionally punish those homeowners who had been renting at the most affordable rates. Ironic? The City of Oakland also recently won a Superior Court ruling in Owens v City of Oakland that validates the city's regulation of room rentals in owner-occupied single family homes.

Because so few professionals and homeowners understand what just happened in Oakland, I think the pricing in Oakland does not reflect the horrendous nature of the new policies on 1-3 unit properties.

I would tend to agree that Oakland and Berkeley are no fly zones for real estate investors. I intend to invest in small multi-family properties (2-4 units), but will add a layer of "regulatory armor" around any local investments based on what applies now and what the tea leaves tell me will apply in the future. Key word: future.

I have owned real estate for over 25 years and multifamily properties for 20 years. I still feel like new real estate investor. I am most interested in developing a system or joining a team to identify and invest in off-market small multifamily opportunities.