All Forum Categories

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

All Forum Posts by: George Gammon

George Gammon has started 15 posts and replied 172 times.

Post: Dave Ramsey Is Misleading The Public

Post: Dave Ramsey Is Misleading The Public

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

I wanted to address this to educate people who have been mislead by the financial services industry...not just Dave Ramsey

Step 7 - Build wealth and give. This is where he want's you to "invest in mutual funds," and to be fair real estate (all cash and 5% of your investments). So let's assume the other 90-95% goes into mutual funds. Just go to his website and it's obvious he's drank the mutual fund koolaid. Again, not sure whether he knows how bad his advice is and is lying or is completely ignorant. My guess is it's the former because of the mental gymnastics required for articles like this from his blog.

And if you read the blog post it becomes obvious why I tend to believe he's blatantly lying to his audience and his whole schtick is a rouse. see below

Notice he brushes off the lost decade by saying you have to look at the bigger picture and you can't cherry pick time frames. But that's exactly what he does to make his claim about the 12% average returns. The whole basis for for the blog post and a big part of what he sells to his audience.

But it goes from a subtle white lie to blatant fraud when you look at how he's selling a "12%" return.

Meaning, most of his listeners are unsophisticated, they don't know a 12% drop one year and a 12% gain the next doesn't put you back at zero. They think that their money will just compound at a 12% clip annually. Let's look at reality.

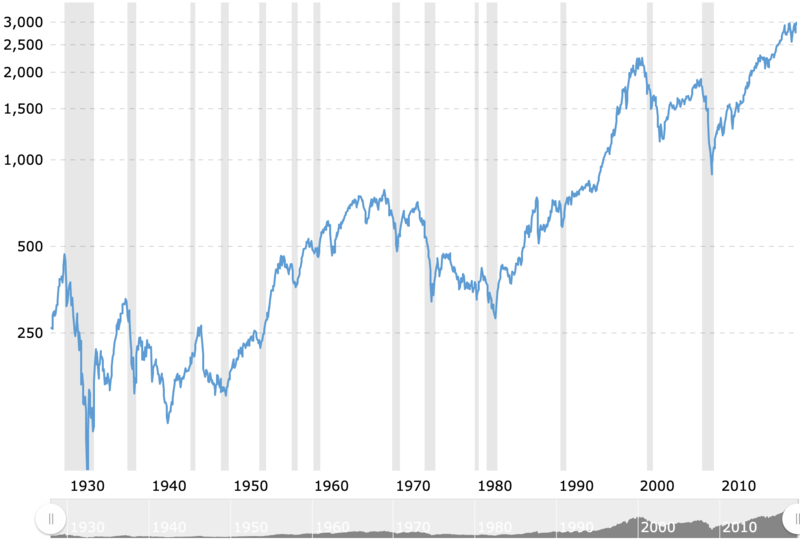

If we took what DR says at face value, the market goes up on average of 12% a year going back to 1923, we should be able to type the value of the 1923 S&P into a compound interest calculator, input 12%, and we should have roughly 3000 (where the S&P is today). I only have data from 1928 on, but I think you'll still get my point. The S&P was 17 in 1928. Let's see what happens...

If what DR says is true, the way he sells it to his audience, if S&P would have to be at 512,000 right now!!! It's at 3000!!!

And I'm not even adjusting for inflation. Adjusted for inflation (meaning 12% annual increases in purchasing power) the S&P would be at over 7,500,000!!! YES, 7.5 MILLION.

You maybe saying to yourself, "what George is saying can't be true" DR would never get away with that much of a lie. Here's why DR can get away with his claims. They're true in literal terms but they're wildly false in the way he presents it to his audience and how his audience perceives what he's saying.

DR presents this 12% claim as though, over the long haul, your money will grow by 12% a year. FALSE! Why? Because when a number is reduced by 10% and then increased by 10% you're not left with the same number...it's lower.

As an example. Take $1000 and decrease it by 50%, you now have $500. Increase that $500 the next year by 60% and you now have a total of $800. A $200 (20%) loss but a 5% average return (-50 + 60 = 10/2 = 5%).

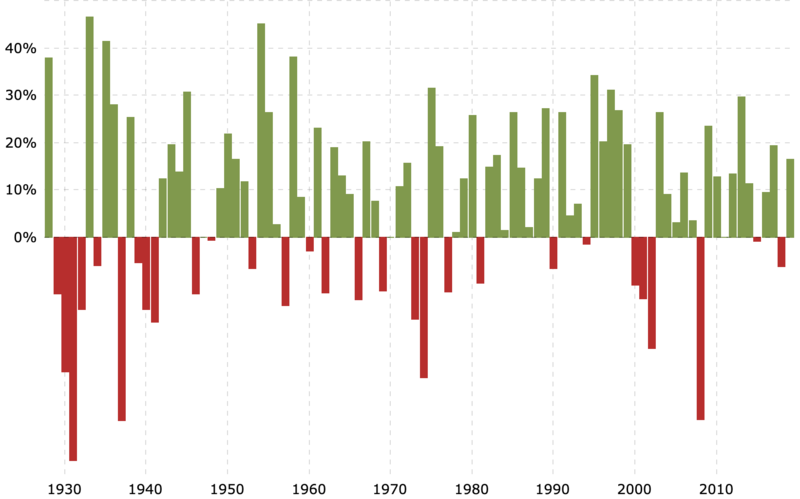

This becomes very clear when we look at graph of annual S&P returns.

Or better yet, look at an inflation adjusted chart. Please notice how much you'd make if you invested in 1928 and left your money in for 52 years, until 1980.

You would've made zero (adjusted for inflation). Dave Ramsey what happened to 12% per year??

What infuriates me the most is he targets people in the south and people who go to church, in other words people with traditional values who are more susceptible to his "be prudent, save money, no debt, invest in mutual fund" snake oil.

To be clear, 10% of what he says is spot on, have a rainy day fund and don't take on consumer debt, but the other 90% is so bad it's completely inexcusable.

If you're one of the millions of Americans, not just DR fans, who have drank the koolaid of the financial services industry and invested into the "safety" of mutual funds, I apologize, I don't relish being the bearer of bad news. But as I said in my first post on this thread, I feel a moral obligation to set the record straight.

Please note: I didn't even hit the tip of the iceberg of why mutual funds are quite possibly the worst investments on a risk/reward basis. I understand I exclusively focused on S&P and mutual funds typically contain bonds. I did this because interest rates have been driven down so low by the Fed, mutual funds no have to overweight equities because they can't get a return from bonds. This problem will be exacerbated if/when US bonds go into a negative yield like Europe and Japan.

I realize this is complex stuff. It's why DR can dupe so many, including maybe himself. I'd like to point out I learned none of the above in college. ;)

If you have any questions don't hesitate to reach out, all my contact info is on my profile.

Good luck,

Post: Student loans or investment property

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

Originally posted by @Mac F.:

@George Gammon, I read your profile. You are certainly someone with a lot of experience and a solid depth of knowledge.

You stated that you "feel a moral obligation" to show the light on Dave Ramsey, who has "destroyed more American minds than anyone else." If you could please do that in this thread, I'd appreciate it. I'm sure the 12 other people you tagged in your comment about DR would appreciate it too.

DR, to my knowledge, has never recommended fixed income investments. In the context of DR, a comparison of real estate investing to fixed income is an unfair straw man argument. DR mentions this often enough that I'm pretty certain most DR listeners know his position too.

DR recommends putting 15% of gross income into retirement in 'good growth stock mutual funds.' A fair argument would be to compare someone who followed DR's preferred method to your example. But even that would probably not be fair-- because nobody on this thread has advocated that. Maybe compare someone who uses that $200k to pay off their student debt, then saves a down payment and then invests in real estate?

Second, you keep bringing up that people here don't understand inflation. Could you please explain what you mean by that? I would think that a strong basic understanding of housing inflation is one of the things that attracts people to real estate investing, at least that's the impression I've gotten from reading the forums. It certainly seems to be a regular point of emphasis on the various BP podcasts.

Finally, why do you feel that net level of positive cash flow of $1500 a month on a 500k portfolio of properties with 40% down is reasonable, especially for novice investors? Please go into detail on this. One of the great things about BP is that there are so many experienced real estate investors, like yourself, here. That seems like a fantastic return, especially for novice investors, and I just don't have the confidence yet that that's reasonable. Maybe I'm confused, but I've listened to enough BP podcasts where I've been cautioned not to expect to make a strong return on my first real estate investment. As a novice real estate investor, I'd appreciate it. Oh, and feel free to be as technical and detailed as you want on this-- I need practice at calculating real estate investment returns.

Thanks.

Thank you for your post and questions. I'll respond by first outlining why Dave Ramsey's ideas are dangerous. Like a politician, he either knows the truth and is lying or he's an idiot.

Let's start by using DR "Financial Peace University" baby steps.

Step 1 - $1000 emergency fund. I can't argue with this.

Step 2 - Pay off all debt, using debt snowball. This is where he starts to go off the rails. Consumer debt is bad, granted, but all debt is not created equal. A 30 year fixed rate mortgage on a cash flow positive rental property is the opposite of consumer debt. There's no better way (risk adjusted) to build wealth in today's economic environment. Paying off fixed rate debt, that's paid by a 3rd party, is a terrible idea. And he's not talking about consumer debt exclusively, here's a pictograph from his website referring to real estate investing. See step #1

Also note: 5% of net worth. Another insane suggestion I could discuss for hours.

Step 3 - 6 months expenses in savings. Agreed.

Step 4 - Invest 15% of Household Income into Roth IRAs and Pre-Tax Retirement. Once again completely insane. I'll go into why this is incredibly high risk below when I discuss mutual funds. But if you want tax free way to build wealth real estate (starter homes in midwest purchased under the cost of construction) does that and is 100x less risky.

Step 5 - College fund. I disagree with the entire cultures obsession with sending kids to college (this isn't DR specific.) Do a simple cost/benefit analysis, 90% of degrees are a waste. If you want to be educated you have the internet, everything I know about macro, as an example, I learned from internet, audio books, and Youtube.

Also, I was a self made millionaire at the age of 34. Literally used nothing I learned in school past grade 3. Another example, a good friend is a small car dealer, his oldest son loves cars and just turned 18. My friend gave him the option of college or start out in family biz. Kid chose biz, is now making 70k a year and has a skill (flipping cars) he can use for the rest of his life to make 100k plus a year... no student debt and a much healthier liver.

The problem is the statistics on college are extremely misunderstood. They point to the fact college grads make more money, but they don't adjust for the skills required to graduate from college, such as self discipline, motivation and intellect.

My point is, it isn't necessarily the degree but the skillset and personality the kid had prior to college...college just gets all the credit, wrongfully so. The exceptions are skilled trades, doctor, lawyer, engineer etc. but there my argument would be most kids go into those fields for the money and you could make much more money flipping cars or 1000 other things by learning the trade instead of going to college and signing up for 200k in debt you can't unload in bankruptcy.

Step 6 - Pay off home early. I completely disagree. Why? Because, in most cases, it's financially crazy to own a home.

Most people live in a home, that if it were a rental, would have an atrocious R/V ratio. So own rental starter homes in the midwest, under cost of construction, with 30 year fixed rate debt, that have good R/V ratios.

It's much better to rent a 1 million dollar house to live in and take the 1 million dollars and buy good rental props. Even if you don't pay cash it's most often cheaper to rent a nice house than to buy it when you consider the costs of owning. So rent where you live and buy things to rent to others.

Or house hack. Buy a triplex, live in one unit, and have your renters pay the mortgage (again, make sure it's 30 year fixed rate). This and BRRRR are by far the smartest suggestions on BP.

FYI, I'm 46 now, I've never owned where I lived.

Step 7 - Build wealth and give. This is where he want's you to "invest in mutual funds," and to be fair real estate (all cash and 5% of your investments). So let's assume the other 90-95% goes into mutual funds. Just go to his website and it's obvious he's drank the mutual fund koolaid. Again, not sure whether he knows how bad his advice is and is lying or is completely ignorant. My guess is it's the former because of the mental gymnastics required for articles like this from his blog.

And if you read the blog post it becomes obvious why I tend to believe he's blatantly lying to his audience and his whole schtick is a rouse. see below

Notice he brushes off the lost decade by saying you have to look at the bigger picture and you can't cherry pick time frames. But that's exactly what he does to make his claim about the 12% average returns. The whole basis for for the blog post and a big part of what he sells to his audience.

But it goes from a subtle white lie to blatant fraud when you look at how he's selling a "12%" return.

Meaning, most of his listeners are unsophisticated, they don't know a 12% drop one year and a 12% gain the next doesn't put you back at zero. They think that their money will just compound at a 12% clip annually. Let's look at reality.

If we took what DR says at face value, the market goes up on average of 12% a year going back to 1923, we should be able to type the value of the 1923 S&P into a compound interest calculator, input 12%, and we should have roughly 3000 (where the S&P is today). I only have data from 1928 on, but I think you'll still get my point. The S&P was 17 in 1928. Let's see what happens...

If what DR says is true, the way he sells it to his audience, if S&P would have to be at 512,000 right now!!! It's at 3000!!!

And I'm not even adjusting for inflation. Adjusted for inflation (meaning 12% annual increases in purchasing power) the S&P would be at over 7,500,000!!! YES, 7.5 MILLION.

You maybe saying to yourself, "what George is saying can't be true" DR would never get away with that much of a lie. Here's why DR can get away with his claims. They're true in literal terms but they're wildly false in the way he presents it to his audience and how his audience perceives what he's saying.

DR presents this 12% claim as though, over the long haul, your money will grow by 12% a year. FALSE! Why? Because when a number is reduced by 10% and then increased by 10% you're not left with the same number...it's lower.

As an example. Take $1000 and decrease it by 50%, you now have $500. Increase that $500 the next year by 60% and you now have a total of $800. A $200 (20%) loss but a 5% average return (-50 + 60 = 10/2 = 5%).

This becomes very clear when we look at graph of annual S&P returns.

Or better yet, look at an inflation adjusted chart. Please notice how much you'd make if you invested in 1928 and left your money in for 52 years, until 1980.

You would've made zero (adjusted for inflation). Dave Ramsey what happened to 12% per year??

What infuriates me the most is he targets people in the south and people who go to church, in other words people with traditional values who are more susceptible to his "be prudent, save money, no debt, invest in mutual fund" snake oil.

To be clear, 10% of what he says is spot on, have a rainy day fund and don't take on consumer debt, but the other 90% is so bad it's completely inexcusable.

If you're one of the millions of Americans, not just DR fans, who have drank the koolaid of the financial services industry and invested into the "safety" of mutual funds, I apologize, I don't relish being the bearer of bad news. But as I said in my first post on this thread, I feel a moral obligation to set the record straight.

Please note: I didn't even hit the tip of the iceberg of why mutual funds are quite possibly the worst investments on a risk/reward basis. I understand I exclusively focused on S&P and mutual funds typically contain bonds. I did this because interest rates have been driven down so low by the Fed, mutual funds no have to overweight equities because they can't get a return from bonds. This problem will be exacerbated if/when US bonds go into a negative yield like Europe and Japan.

I realize this is complex stuff. It's why DR can dupe so many, including maybe himself. I'd like to point out I learned none of the above in college. ;)

If you have any questions don't hesitate to reach out, all my contact info is on my profile.

Good luck,

Post: HELOC Share your thoughts and experiences.

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

@Luis Escudero Smart move Luis. I'm not sure why anyone would suggest doing a refi first because you'll be under increased pressure to put the money to work? In other words, you'll be making payments before you find a deal.

What's nice about an LOC is you don't make payments until you use it, so you can take your time and find a good deal, then start making payments.

My guess is you'll want to buy a rental prop? If this is the case, I'd strongly suggest terming out the debt once the the property is purchased you want to keep long term. Why? Better interest rate, but far more importantly you can transition the debt into 30 year fixed rate and lock in an artificially low rate.

I purposely used the word "artificially" because very few Americans realize 30 year fixed rate mortgages would not exist in a free market. Meaning the banks would never issue that loan because it most likely loses money, due to inflation, over the long term.

You're paying the bank back with cheaper dollars than you borrowed. This creates a transfer of wealth from the lender (bank) to the debtor (you). So why to banks do the loans? Before the inks dry the sell the paper to fannie and freddie.

In other words 30 year fixed rate mortgages are subsidized by the tax payer.

I'm not a big fan of it, but if it's there, I'm going to use it, and I suggest everyone do the same. It's free money and it's the only asset (I consider it an asset) in the US that's currently cheap. Real estate prices are sky high, if you have to buy, buy with cheap debt. You'll definitely make money on the debt, so it hedges your downside on the property, and if the prop goes up in value it's a double win.

Hope that helps,

Post: Newbie Investor - How to Invest $60000

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

@Misty Evans the great news is you're in a perfect market to start. I love the linear midwest markets because of the reduced macro risk.

Now let me give you some advice no one has ever heard on BP. This takes out of the box to a whole new level.

But if you keep an open mind, I'm confident it'll make sense.

First what are the main skills you'll need, or need to develop, to be successful, whether you're remodeling to rent or flip?

1. Ability to manage people

2. High level problem solving

3. You have to have systems and processes in place

4. Mastery of comps and negotiation (you make money on the buy side)

5. Ability to create something the market wants

The above list is probably not too controversial...

Heres where it's going to get WAY outside the box! ;)

In a past life one thing I did as a "side hustle" was I flipped trucks. Specifically 1995-2002 Fords. The process is literally identical to flipping houses but you're investing 7k...not 700k. I'd find low mile trucks that were beat up, I'd have the interior redone, fix every mechanical issue, give it a brand new paint job, and flip it.

On a strictly cash on cash ROI basis the returns are much higher than house flipping. I'd very often double my money in a month. Unfortunately, it's impossible to put more than 100k to work. But it's a fantastic way to make 100k-300k a year.

So the best advice I can give you, and I'm completely serious, is to start by flipping a couple trucks/cars to get a feel for the process and what can go right and wrong.

If you want to start flipping homes, as an example, buy/remodel/flip a couple trucks first. Once you've worked out all the kinks and implemented the processes, take the model and do the same with houses.

1. You'll get the needed experience I outlined above, with a fraction of the risk.

2. You'll make some good money to put towards your first flip.

What's not to like?

I'd actually suggest this learning tool to any newbie wanting to get into the RE remodeling/flipping/rental game.

I've seen so many investors lose their shirts on the first few flip attempts. There are countless things that can go wrong and they never know what they don't know. So why not learn the exact process with 1k of downside and 10k of upside, instead of 100k of downside and 50k of upside??

Like I said at the beginning, it's outside the box, but it makes a ton of sense and I'd encourage you, and all other newbie's, to consider it.

Good luck,

P.S If anyone has any further questions please don't hesitate to contact me directly, all my contact info is on my profile page.

Post: Student loans or investment property

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

Originally posted by @Christian Rojmar:

“So what it then boils down to is measuring the actually risk of taking 200k and paying off student loans opposed to investing in positive cash flow rentals with 30 year fixed rate debt at sub 4%, because it makes them feel good.”

I think you are missing the point people are making about “do what ever is going to make her feel best.”

The problem I see with your argument that it “boils down to measuring the [actual] risk of taking 200k and paying off student loans opposed to investing in positive cash flow rentals. . . because it makes them feel good” is that it is all about the financials. People simply value things differently. You assume that just because a person will be better of in the future based on math, that person will feel better down the road. Financially, yes, but happiness, enjoyment of life, etc. maybe not. I did not see her asking what makes most sense financially (but maybe that was inherent in her question) but more general, "what should I do?". For example, while working 15-hour days and not seeing my family, and living in a 500 sf apartment is the financially right decision, it is the wrong decision for me because I value time spent with my family way more than I value money. Same can hold true for stress/piece of mind.

“In the prior post we established they'd lose around 800k...I think that qualifies as risk.”

Frankly, I do not think we have established that they would lose 800k unless we make some extremely irrational assumptions that favor investing in RE. And don’t take me wrong, everyone on this site want to invest and believe investing in RE is the way to get out of the rat race but the numbers are not reality. For example:

- You assume that they actually have $200,000 to invest right away;

- You assume a first-time investor will find properties that will generate $1,500 monthly true cash flow on a $200,000 investment;

- You assume that they will pay no tax on the cashflows from the investment;

- You assume they will pay no capital tax on the sale of properties in future;

- You do not factor in the risks of investing in RE rather than paying off debt;

- You assume that they will pay off the debt completely rather than put at least some of the $200,000 in market which should conservatively generate 5% annually (which can be leveraged significantly just like RE). Even just $100k in market will generate ~$165,000 pre-tax in 20 years.

“What makes 2019 10x more dangerous than 2009? In 2009 the private sector was bailed out by governments, in the next recession who bails out the governments?”

While I certainly agree that a recession will happen eventually (probably sooner than later), you are talking about an event that will change the way we live today... I would probably buy gold if I believed this would happen. If you are thinking of a “normal” recession, then market will come back just like it did after 08-09, similarly to how the RE market came back.

2. And this is by far the most important topic you brought up. Can rents increase if wages are flat

This was very informative, helpful, and appreciated – but I am not sure it answered my concern? I am not talking about fixed debt v. rent but real rent v. real wages. If rent is going up by 5% per year, inflation by 5% and wages by 2%, real rent is staying flat while real wages is going down by 3%. The discrepancy between real wages and real rent is increasing rapidly – less people can afford housing. Same is true for home values.

Help me understand how “at some point people can’t afford the sky high rents” and “but remember those are inflation adjusted numbers and debt is nominal” have anything to do with my concern that real rent is increasing more rapidly than real wages?

My point, and again I may just be missing what you are saying, is that while $1 in real wages (accounted for inflation) was worth $1 in real rent in 1960, in 2014, $1 in wages is only worth $0.73 (if I am doing the math correctly – 120%/165%-1). Real income is not keeping up with real rent and something will have to give regardless of whether debt stays the same.

I totally get what you're saying about real wages vs. real rents. These are high level topics both of us are trying to tackle via text, which is hard. I don't think I'm doing a good job explaining my point on inflation. There's an obvious mis communication. Regardless, I sincerely appreciate the dialogue.

I'd like to strongly encourage everyone reading this thread to start thinking about how macro can and will affect you investments, job, retirement, and overall quality of life. And please dedicate time to mastering the concept of inflation...you'll thank me in 20 years. ;)

P.S. If anyone would like to communicate directly with me, regarding the topics I've outlined in this thread or anything else, all my contact info is on my profile page.

Post: Student loans or investment property

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

Originally posted by @Derrick E.:

@George Gammon Respectfully, you are not taking in to account DSCR/DTI with those student loan payments hanging over your head. I am paying off some of my student loans to open up more buying power down the road.

Derrick, thanks for your response. Even with a 100% cash purchase, assuming 200k in student loans and 200k cash, they're much better off in 20 years financially. They'd still have all the cash flow from inflation, the original 200k, the nominal/real appreciation of the asset, depreciation, and zero student loan debt.

George

Post: Student loans or investment property

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

Originally posted by @Christian Rojmar:

@George Gammon Great examples and certainly not feeling disrespected.

1) I respect that you are looking at it 100% from the financial side of things and I am not disagreeing with your math other than that you will have to pay capital gains tax at some point reducing that number depending on 1031 etc. However, I know many people that cannot function when debt is hanging over their head and while it may not be the best financial decision, paying of the debt sooner rather than later will give them piece of mind which is more valuable to them.

2) As for inflation and its effect on rental values, I am personally very concerned about the growing discrepancy between rents and income and something is going to have to give - i.e. is it reasonable for rent to continue growing with inflation or more while income is staying flat (in what seems to be best case scenario). I cannot see that scenario pan out... I would say the same for property values and how rapidly they are increasing compared to income. I would love to hear your thoughts on this because it worries me.

3) I have student loans that I pay absolute minimum on while investing in market which is providing compounded growth.

4) Reading back my poorly written comment,while it may sound like it, I am not saying that they should pay off debt ASAP unless it will give them piece of mind, and I am certainly not arguing that they should put any income into a savings account or an interest bearing note and let it sit. However, if debt is a concern, which it clearly is for this person, investing in the market with a return of 7-8% annually may be the better option due to the liquidity and not having to take on more debt (and you can leverage your position there as well if you want).

Christian, thanks for the well written and thought out response. You bring up a couple things I think are extremely important to address.

1. Some people can't function with debt over their heads. In other words, it makes some people feel good to not have any debt, because they feel like they're taking less risk, and if taking less risk makes someone feel good or sleep well at night than it's worth it.

If humans were rational this would hold merit because most would instinctively know probabilities/risk. Unfortunately, humans are the opposite. We are terrible at analyzing risk and probabilities.

As an example some people have a fear of flying but they'll drive 2 hrs a day in traffic, often without a seat belt. Or ask someone if they're more afraid of terrorists or catching a cold? Mass shootings or falling off a ladder? Hopefully these examples are rhetorical.

Bottom line people really really suck at accessing risk. And often, what makes us feel good, is actually far more risky.

Many on this thread have suggested the original poster do what ever is going to make her feel best. But isn't doing things that are uncomfortable because of cost/benefit part of what defines adult behavior? Going to the gym, working extra hours, studying in college, waking up at 6am, admitting mistakes, personal discipline, etc. If we never did anything uncomfortable because of a greater benefit in the future we'd all be 3 year olds.

And then take this to its logical conclusion. I'm sure everyone would admit there is a level of risk that exceeds the benefit of feeling good. Would you tell a friend to eat a cheesecake everyday or smoke because it makes them feel good? Of course not.

So what it then boils down to is measuring the actually risk of taking 200k and paying off student loans opposed to investing in positive cash flow rentals with 30 year fixed rate debt at sub 4%, because it makes them feel good.

In the prior post we established they'd lose around 800k...I think that qualifies as risk. Next, by paying off the student loans the poster will be 100% reliant on a job and traditional retirement plan, call it social security and 401k. (I'm assuming the poster never invests because of a continued irrational fear of debt). So they're totally at the mercy of an employer, the stock and bond market, and the US economy.

Remember how people are really bad at accessing risk. Get a good job, 401k, no debt...what most would consider low risk, is actually extremely high risk. Why?

The US is 23 trillion in debt (on balance sheet), we are the largest debtor nation in the history of the world, the US has a wildly inflated standard of living because of the USD status as world reserve currency, the stock market is at nose bleed levels, and the bond market has 15 trillion in NEGATIVE yielding debt. Additionally, the US is 11 years into an economic expansion, the longest in history. The next recession will come. When? We don't know, but based on history, sooner than later.

In 2009 the world economy nearly imploded because of debt bubble. Is debt lower or higher now? Much higher. The consumer debt bubble was merely transferred to a sovereign debt bubble. What makes 2019 10x more dangerous than 2009? In 2009 the private sector was bailed out by governments, in the next recession who bails out the governments?

I could go on and on, but the bottom line is there's a very good chance a good paying job might not always be there. There's a good chance a 401k won't be there. There's a 100% mathematical certainty social security will not be there. And there's also a good chance that rental property, in a linear market, in a good neighborhood, purchased with 30 year fixed rate debt, will be there...

So which is more risky? Paying off the student loans or buying the investment property? At the very least it's a toss up. ;)

I would argue it's much more risky to pay off the student loans, especially when you consider the loans maybe forgiven, therefore advising to pay them off because it would feel good, is similar to advising someone to smoke because it feels good.

2. And this is by far the most important topic you brought up. Can rents increase if wages are flat? I think you said you don't see this happening? Again, this illustrates how little most understand inflation. And I'm sorry to pick on you but it's imperative everyone gets this.

You're comparing 2 completely different things. Real (adjusted for inflation numbers) and Nominal (just numbers without an inflation adjustment.) 30 year fixed rate debt never changes, your first payment is the same as the last payment, it's a nominal number. When you compare your debt payment to your income stream (rent) you have to compare apples to apples. In other words, nominal numbers with nominal numbers.

What you're doing in your chart above is showing real (inflation adjusted numbers.)

I know this get's really confusing, really fast, so let's use an example using your chart above. According to your chart rents are 160% higher than they were in 1960 (in real terms.) Wages are 120% higher (in real terms.) A delta of 40%, which to your point, seem unsustainable at best, how could rents possibly go up? At some point people can't afford the sky high rents.

But remember those are inflation adjusted numbers and the debt is nominal. In other words real rents could come down while nominal rents could sky rocket. How? If the rate of inflation exceeds the rate of rents going up. In other words, if rents are going up by 2% per year and inflation is 3% per year, real rents are going down while nominal rents are going up.

Question: Will a dollar buy more or less in 20 years? If your answer is less, that's all that matters, rent's will be higher but the debt payments will be the same.

Let's go back to your chart one more time. Look at rents from 1970 to 1980. Didn't go up that much right? But when you run the numbers through and inflation calculator rent's more than doubled in nominal terms.

Your chart uses inflation adjusted numbers but the debt doesn't adjust with inflation. When you use nominal rents, with nominal debt, over 20 years, rent's will 100% of the time be higher.

The bottom line:

1. Paying off student loans is NOT less risky than investing, in the way I outlined, and IMHO it is irresponsible to advise someone to do it anyway because it feels good.

2. When analyzing any investment make sure to compare real (inflation adjusted) numbers with real numbers and nominal numbers with nominal numbers...debt is nominal, so it must be compared with nominal rents, which over time, will always go up.

Thanks again for your response, I hope I was able to shed some light on, at very least, how inflation works with debt. It's crucial to making good investment decisions over the long term.

George

Post: Student loans or investment property

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

@Joel Johnson @Armin Nazarinia @Christian Rojmar @Tiffany Faulknor @Derrick E. @Mac F. @Alpesh Parmar @Nate Bell @Alonso Escalante @Marcus Johnson @Ashley Gish @Jonathon Weber @Shahene Nili @Derek Joyner

I'm really concerned with the lack of understanding on BP in general, especially on this thread.

I want to say upfront that I mean absolutely no disrespect to anyone on this thread, but I feel a moral obligation to try to "show the light" to as many people as possible. For many years I thought Paul Krugman had destroyed more American minds than anyone else...I'm now thoroughly convinced it's Dave Ramsey.

(We'll assume there's not a 30% chance the student loans will be forgiven.)

First, the number one issue I see on this thread is people conflating rental property with a bond, annuity, or any fixed income instrument. Meaning, you take money from your bank account, buy the fixed income instrument, you get a fixed monthly payment, and in the end you get your principle back along with the interest.

The reason people make this mental error is they don't consider/understand inflation. In other words, over the long term, rents go up, the debt payments stay the same. See chart

As an example, lets say there's a 2.5% annual rate of inflation. You buy a 20 year, interest only, fixed income asset for 100k, with annual 10% interest. At the end of the 20 years you have 300k (200k interest + 100k principle.)

THAT IS NOT HOW RENTAL PROPERTIES WORK.

If you buy a 100k rental property, with a yield of 10%, and there's 2.5% inflation, at the end of the 20 years you have approx 363k. Why is there a 63k difference? Because inflation increased yield by 2.5% per year. In first example, inflation had no effect on yield because the rate of return is fixed.

Just to drive this home let's use a different example.

Many on this thread have suggested @Ashley Gish would need a higher rate of return on the investment than the rate of return on her student loans. Again making the mistake of assuming a 100k rental property is the same as having 100k in the bank.

Obviously the 100k in the bank would need to have a higher interest rate than the rate on the student loans, or if both rates were the same it would be a wash, or if the rate on the bank account was lower, it would be better to pay off the loans.

But what if the interest rate on the 100k in the bank increased by 2.5% per year? (interest rate x .025 not plus 2.5). Assuming both the cash in the bank and the student loans started with the same rate, will the cash in the bank make more than the amount of interest paid on the student loans? YES!

So that's how the cash flow works, now we'll discuss the price of the fixed rate asset vs. a rental property. In other words, the capital gains.

Again assuming 2.5% annual inflation, and assuming you put 100k in a bank account, at the end of 20 years what would the value of your original 100k be? Answer: 100k.

Under these same conditions, what would the value of your 100k rental property be? Answer: 163k.

Next, remember the renter is paying the mortgage. We haven't even discussed how debt increases returns. But I'll skip that for now, and go straight into a final example which will undoubtedly put an end to the Dave Ramsey insanity once and for all.

In this hypothetical let's say you have 200k in student loans and 200k in cash. Option #1 is paying off the debt so you would have zero cash and zero debt. Option #2 is putting 200k down on 500k in rental properties, using 30 year fixed rate debt at 5%, and keeping the 200k in student loan debt.

Now let's assume the positive cash flow collected from the properties is the exact amount as the monthly student loan payments. And the total rent and total student loan payment were both $1500 a month.

With a average inflation rate of 2.5% over 20 years, at the end of 20 years this is how the 2 options would play out.

Option #1 - 0 cash and 0 debt

Option #2 - 114k in cash, 673k in equity, and 0 debt

Which would you choose? It's literally the difference between being completely broke and almost being a millionaire.

So how did I get those numbers? Remember the 2.5% inflation rate. If rent increased by 2.5% per year for 20 years it would go from $1500 to $2457. Of course $1500 goes to student loan payments but the difference, over 240 months (20 years) of rent payments is approx 114k.

How about the equity? You start with 200k in equity, the renters pay off 154k of the original loan amount, and the 500k in rental properties goes up each year with inflation (2.5%) so at the end of the 20 years the value of the properties is 819k, a 319k difference. So 200k + 154k + 319k = 673k

In all seriousness arguing to pay off the student loans now is akin to arguing for the flat earth theory...it's truly that level of irrational thinking.

And I want to stress this is not my opinion, this is math, plain and simple. If you dispute the conclusion you're not disagreeing with me, you're disagreeing with math.

I want to reiterate that I mean NO disrespect to anyone on this thread. I'm in no way doing this to be negative, or heckle people, I'm only doing this because I want everyone on BP to understand how inflation affects real estate investing. And how dangerous the ideas of Dave Ramsey are to real estate investors.

Debt for consumption is bad...absolutely 100%!

Debt for productive investment is very good...100%!

I leave you with food for though. If debt on net balance is negative, how and why does the world have fractional reserve banking? And what would the world wide standard of living be without fractional reserve banking? Or simply compare the standard of living in countries that have a developed credit/banking system and those that don't.

George

Post: Student loans or investment property

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

@Ashley Gish Great, question. I'm sure many can relate so thanks for the post.

Let me start by saying...Don't even think about paying off your student loans. That is the mother load of bad ideas! The Hindenburg was a better idea.

There is no rational reason to pay them off, especially if they're fixed rates. And if they're not fixed rate re fi them asap with a fixed rate.

Several on the thread have given you some good advice, don't pay off student debt and buy a rental prop(s) to have tenants pay off you loans and build equity for you. But I don't think they went far enough to explain why.

First let's go over the numbers so we can do a thorough analysis.

I don't know exactly how much you have to use for investments or debt reduction but I'll assume you have 200k because that's the amount of your loans and you're talking about paying them off. This is enough where you could make all your student loan payments with the positive cash flow from the rental props if you invested the 200k.

(I'd suggest markets in the Midwest and south where you can get a higher R/V ratio. If you're set on investing in Oregon, maybe you could check out Corvallis, Eugene, Hood River, etc. a smaller metro area that may have better R/V ratios.)

Now let's look at the rate of inflation.

I've gone over this in great detail on other posts more pertaining to this topic so I won't get into the inflation details here. That said, look at a chart of historic rates of inflation (far right column)

2001-2018

1967-1983

The reason I wanted to show 67-83 is it was a time of higher inflation. I think the probability of the US going through substantial rates of inflation over the couple decades is very high (again, that's a different post) but we'll just use the numbers from the past 18 years. On average about 2.5% per annum.

For the sake of ease I'll say the positive cash flow coming in from the properties is $1000. Initially this will all go to cover your monthly student loan payment. But what happens when rents go up? And not even in real terms, just with the rate of inflation?

After 5 years you'll have an additional $131 monthly in rent above and beyond your student loan payments.

After 10 years you'll have an additional $280.08 per month.

After 15 years you'll have an additional $448.30 monthly.

And after 20 years you'll have an additional $638.62 monthly. Using the mean number ($280) times the 240 months of the 20 year term of the student loan, you get about $67,000 in additional cash flow assuming rents go up at the rate of inflation and assuming inflation stays ridiculously low (which is possible but unlikely, and obviously this is a very crude number, but I don't have time to do the exact math)

What if the US averages 5% inflation over the next 20 years? Totally possible, again look at 1967-1983.

Please notice the ending 20 year number at 2.5% ($1638) compared to 5% ($2653).

It becomes glaringly obvious how you make money off inflation because the debt payments stay the same. But that's just the cash flow, now let's look at the appreciation.

Notice: Over the long run homes don't appreciate, they merely go up with the rate of inflation.

But that doesn't mean you don't increase your purchasing power via inflation. (Assuming you're using 30 year fixed rate debt, which is the second smartest thing you can do after not paying your student loans.)

Assume you have 200k in equity, but the combined value of the homes on you balance sheet is 500k. If inflation increases by 10% the value of your assets goes to 550K, an increase of 50k. But 50k is not a 10% increase of 200k, which is your investment. It's 25%. You've increased your purchasing power (made money) and your asset didn't appreciate it just went up with inflation.

Here's what it looks like in the calculator.

Your asset went up in price by 319k but your investment was only 200k, so again, you increased your purchasing power or you made money. Let's look at what happens with a 5% rate of inflation.

The numbers get big very fast. ;)

And remember your renters have been paying down the balance of your mortgages so you've got more equity as well.

After 20 years you'll have a balance of 146k, in other words, your renters paid you another 154k.

But wait there's more!

You'll have the depreciation of the assets to use to offset part of your income.

Finally, lets add everything up to get an apples to apples comparison.

Choice #1, the Dave Ramsey (Hindenburg) option leaves you with:

- 0 dollars in 20 years and 0 student loan debt in 20 years

Choice #2, the rational option leaves you with: (nominal dollars)

- 67k from cash flow

- 319k from appreciation (inflation)

- 154k from renters paying your mortgage

- 200k from your original equity

- ?? from tax deductions in the form of depreciation

- And 0 in student loan debt

For specific numbers please adjust for inflation but you get my point. Not paying your student loans, taking the money and investing in cash flowing rental props with 30 year fixed rate debt, is the absolute no brainers of all time no brainers.

Good luck Ashley, I sincerely hoped that helped.

George

Post: Is "Stupid" Money Chasing Millennials in Your Market?

- Flipper/Rehabber

- Las Vegas, NV

- Posts 174

- Votes 251

Originally posted by @Alan Grobmeier:

@George Gammon, great info & great post.

However, with 21T in debt, state & local pensions defaulting, can our government afford anything other than ZIRP without causing another Great Recession?

I see low interest rates ‘forever’ on the horizon. How can they do anything else without causing chaos?

Alan, great question.

Can our government afford anything other than ZIRP? Short answer: No, they can't even afford ZIRP. In fact they can't afford the debt with NIRP.

The US government has to default on it's debt. Let me say that again, the US GOVERNMENT HAS TO DEFAULT ON IT'S DEBT.

Question is will they default the old fashioned way by renegotiating the debt or not paying, or will they default by paying the creditors back with dollars worth less than the dollars the government borrowed?

My guess is they'll pay with cheaper dollars. In other words, they'll have to create inflation.

This gets at the heart of your point about interest rates being low forever. Sure the short end of the curve can be low forever but the Fed doesn't have total control of the long end (10 year, 30 year.) Central banks have suppressed the long end of the curve by buying those bonds but they have to "print money" in order to buy the bonds.

This is highly inflationary because you're dramatically increasing the money supply. See chart of US

So why hasn't the world (US) seen more inflation? It has. It just hasn't shown up in the CPI but it's shown up in asset prices.

The point is, inflation is the only thing that can save the US from its fiscal issues, while at the same time, it's the catalyst that will most likely crush the US economy.

If/when inflation, the Fed's doing everything in its power to create, gets out of control, the US economy will be in serious trouble. Let's think it through. Artificially low interest rates create mal investment (investments that wouldn't have been financially viable under normal market conditions/rates. Remember fed funds rate average about 5%+. See chart)

If fed funds rate is 5% and we have a steepening of the yield curve, where does that put the 10 year, or mortgage rates? Maybe 7.5%? How about commercial loans on all these multifamily complexes being built? Maybe 8.5%? Think about how many investments have been made since the GFC and ZIRP...how many would be able to service their debt if they had to roll it over at 8.5%?

If that were to happen the Fed would most likely do more QE to bail out the economy but that creates more money, which adds fuel to the inflationary fire. The only solution then is Volcker style crushing inflation with 20% interest rates. Unfortunately, this time around that won't be possible because of the US couldn't afford the interest payments on the 23 trillion in on balance sheet debt. Compare our current debt to gdp ratio to 1980. See chart

The US currently pays about 500 billion a year in interest, and at a 2% interest rate. At a 10% it would be 2.3 trillion, and let's not think about 20%. ;)

How would the gov pay for the massive deficits? By issuing more bonds, but more bonds increase the money supply putting more upward pressure on rates. You can see the vicious cycle.

So the short answer to your question is the Fed doesn't have total control of the long end of the curve. The long answer in the next decade, the Fed might not have control of the any part of the curve.

Most peoples rebuttal is the US will be Japan, interest rates will be low forever.

What I preach till I'm blue in the face on BP is you have to look at probabilities NOT possibilities. Is it possible the US turns into Japan? Sure, but is it probable? And let's not forget, US becoming Japan is our BEST CASE SCENARIO. In other words, the most optimistic outcome is a 30 year depression.

Those who make the Japan rationalization, are usually people who'd be crushed by higher rates, and rarely have studied the similarities (other than they had a big crash too) or the differences. I could go on and on about the differences, but lets look at one major metric.

Japan has been the largest creditor nation in the world 28 years running. The US is the largest debtor nation in the history of the world. Let that sink in...

How can Japan have a 230% debt to gdp and be the largest creditor nation? Their public debt is owned by the central bank and other various institutions. So they own a lot of other countries assets and owe very little to other countries (even though they owe a staggering amount to themselves.)

The US is the opposite, it owns almost no foreign assets and owes foreign countries more than any nation in the history of the world.

This means all those dollar assets held be foreigners can be sold fast if the conditions are right, creating the velocity needed to create inflation when combined with the massive expansion in our money supply. Foreigners don't own any Japanese assets to it would be much harder to create a rush of selling needed to increase velocity and/or inflation.

And this is just one difference between Japan and the US.

Please don't get me wrong. Japan has got problems, HUGE problems, but problems are significantly different than the US.

Which takes us back to probabilities. There's a 100% chance of 1 of 3 outcomes over the next decade.

1. Inflation (1970's)

2. Deflation (Japan)

3. Nothing (US stays locked in this moment in time forever)

Let's just assume there's a 33.3% chance of each outcome. That means there's a 33.3% chance many on this thread go bust. And a 66.6% chance things get really bad, BTW what happens to pension funds if the US turns into Japan for the next 10 years? Answer...they go bust.

Bottom line is investing in the US right now is extremely dangerous, especially for those whistling past the grave yard needing ZIRP forever to stay in business. If your business model requires ZIRP, you are part of the mal investment. Don't build your investment framework around ZIRP. ;)

George