Originally posted by @Mac F.:

@George Gammon, how is Dave Ramsey duping people regarding stock market returns? First of all, the investment he's talking about when he uses the 12% number is the Investment Company of America fund-- it's returned 11.96% since it's inception in 1934 and is one of the ten largest mutual funds by assets under management.

https://www.americanfunds.com/...

https://www.forbes.com/sites/r...

Second, your calculations on S&P returns leave out dividends and dividend reinvestment-- that's one of the major reasons that S&P returns are not a good proxy for mutual fund investments (full disclosure-- I'm a former stockbroker). Third, please stop with the bonds. Dave Ramsey, to my knowledge has never recommended fixed income investments, or mutual funds with bonds in them. The only fixed income you'll find in the funds Dave recommends will be cash equivalents (like T-bills and overnights)-- generally because the fund is holding the cash while trying to find an investment opportunity. If you want to do a comparison of your preferred method compared to the 8-10% annualized mutual fund return, go for it.

You're a talented copywriter, but if you're going to say someone's 'lying or completely ignorant,' you might want to get your facts right.

Mac what numbers do I have incorrect? I'm not sure you understand my point. My point is NOT that xyz mutual fund doesn't have a 12% average return going back to 1934. My point is the way Dave Ramsey, and the entire financial services industry, make it seem as if you put $100 into a mutual fund, and that mutual fund has an average return of 12%, your $100 will grow at 12% annually.

That's unequivocally false.

The market goes up and it goes down. A 12% loss and a 12% gain the following year is a loss to your capital but it's a 0% annual return. Let's go over my original example once again.

You start with $1000. The mutual fund goes down by 50%. You now have $500. The following year the mutual fund goes up by 60%. You now have a 60% gain from your balance of $500, giving you a total of $800. You are down $200 from your original investment of $1000. But the mutual fund has an average return of 5%.

If a mutual fund told you it had an average annual return of 5% would you expect it to make money or lose money?

That's my point. A mutual fund (S&P, Dow, anything) can have a positive average return and the fund can still lose money. Just because you're in a fund that has a 12% average return, it doesn't mean your money will grow at 12% per year.

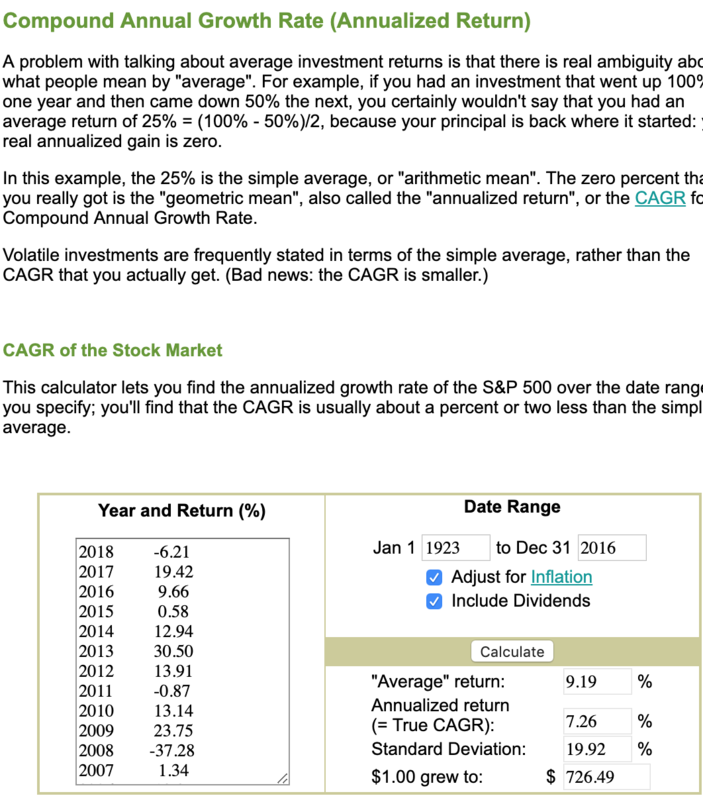

Here's a chart from the link in your post.

Notice, it includes dividend reinvestments. Also, it's over 20 years, 19 of which have been parts of the largest/longest bull market in US history (in other words, the numbers only get worse if you go back to 1934). According to this very chart, from their own website, $10,000 invested with them in 1999 would now be worth $35,000, including dividend reinvestment.

$10,000 compounded at 6.5% is $35,000. Notice: 6.5% NOT 12%. And thats not adjusted for inflation. Adjusted for inflation $35,000 in 2019 is actually only about $23,000 in 1999 dollars.

Adjusted for inflation, $10,000 invested in the very fund you sent me the link too, compounded at a rate of about 4.2%. A far cry from 12%.

And remember this 20 year time frame includes 19 years of the greatest bull market in history. Yes, we had a 50% draw down, but thats what happens in a stock market. It goes up, and it goes down. And it's cyclical, and we're 11 years in to a the longest bull market in history, and interest rates have been declining for 40 years, and the S&P was lower (adjusted for inflation) in 1980 than it was in 1928...52 years with a negative real return.

I'm sorry for anyone invested in a mutual fund assuming an average rate of return is the rate at which your money should grow...that's simply not true.

The good news is you can take your money out of a mutual fund without penalty, and put it into cash flowing real estate, bought under the cost of construction in linear markets with 30 year fixed rate debt...Unless of course you took Dave Ramsey's advice and your money is in a 401k or IRA. ;)

George