All Forum Posts by: Joshua Aycock

Joshua Aycock has started 5 posts and replied 18 times.

Post: Article: A thought experiment - Real Estate vs S&P500

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

Quote from @Allan C.:

@Joshua Aycock the most important thing to recognize about a free market is the efficiency. Returns are proportional to risk, effort and other quantifiable and unquantifiable factors that all the other investors in your market have already defined for you.

Unless you have established a true competitive advantage, you only realize higher returns as you trade off something else. Only you can determine if the higher yield is worth the trade off.

Yep, love this thought @Allan C. The effort and management required of RE is definitely something to consider in the process, and absolutey a factor. I don't believe I have a distinct competitive advantage (yet) but agree that the risks/effort matrices are different between the two investment options. Thanks for reading & responding!

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

Quote from @Tony Kim:

Quote from @Joshua Aycock:

AND imagine the real estate is NOT cash flow positive. Consider the ‘negative cash flow’ as simply additional reinvestment…just like the S&P.

I am all about building cash flow over time through real estate. However, I’m early early early on in my journey.

I am wrapping up construction on my ‘house-hack’ 3 bed / 3 bath single family home in Minnesota. Once it’s done, I’ll bring on two roommates, and effectively cut my living expenses by $1,500–2,000.

I’m just beginning in the journey and contemplating the two main paths I see before me (on this and the next deal).

I can go after a ‘pure’ tried-and-true-investment-20%down-property. One that cash flows right out of the box with minimal capital expenditure or reinvestment. Or, I can go for another rehab, to capitalize on forced appreciation and net worth impact.

As I consider the options before me, I create thought experiments. I’d like to include you in one today.

The problem with Forced Appreciation (Net Worth Impact) Properties:

Debt costs become too high for excellent cash flow.

Unless you find a gem that really doesn’t need much but looks like it does. If you undertake a total renovation, or “flip”, you’ll have pretty significant reconstruction costs. If you can get a cosmetic fixer-upper, the options open up on the cash flow side.

Construction costs on my current (and first) property have run over $130k. I bought it at $250k in a neighborhood that can support $600k+ property values. Houses that are just blocks from me go for 3/4 of a million dollars. My equity impact will be fine. But the cashflow return may not be.

Cashflow Assumptions

If I tried to rent the house as an entire unit, I could probably get $2,500–2,750. Let’s assume all utilities/trash/etc. are paid by the tenant. This means I don’t have additional cash expense outside of fixed debt payments. We’ll use $2,500 as a conservative estimate for the purposes of this thought experiment.

All-in (mortgage + construction loan payment), my fixed debt costs per month will be ~$2,400. That leaves only $100 of cash flow, BEFORE non-cash and deferred-cash expenses.

Non-cash expense includes an implied 5% vacancy, for example. This is not something that will actually hit the bank account but will impact cashflow at some point. Deferred-cash expenses are depreciation, reinvestment, capital expenditures, and maintenance. When estimating ~15% of rents for expenses like these, monthly noncash and deferred-cash expenses add $375/mo. They represent expenses that will be realized at some point (you just don’t know when).

Therefore, my net cashflow on the high-equity-impact house is negative ($275) per month. That means I’ll have to contribute/invest an extra $275 of my own personal cash per month to maintain the property.

Opportunity Costs

I’ll highlight why this isn’t such a huge deal to me, by using an economics concept called Opportunity Cost.

For those unfamiliar, Opportunity Cost is the implied cost of doing something because it also means you’re NOT doing something else. Essentially what you do is valued against what else you could have done instead.

By having to ‘invest’ an extra $275/month in the ‘non-cashflowing-equity-impact’ house, I can’t allocate that ‘investment’ elsewhere…like the S&P500.

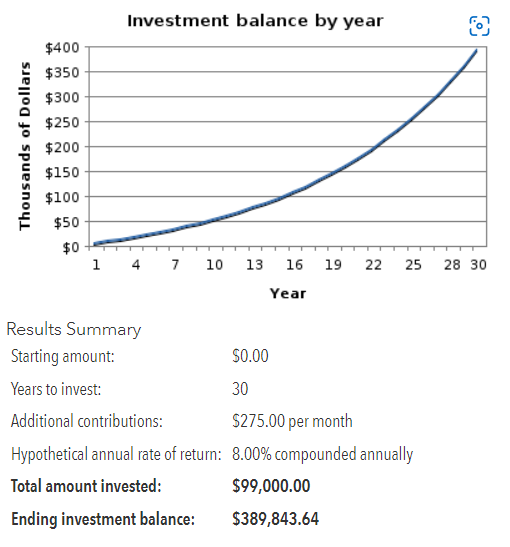

This is what my $275/month investment would look like in the S&P500 over 30 years (the length of my mortgage) at a long-term annual Rate of Return of 8%.

Calculator & visualization courtesy of KJE Computer Solutions via American Funds

Calculator & visualization courtesy of KJE Computer Solutions via American Funds

My $99k investment over 30 years turns into $389,843. Not bad! 394% total return over that timeframe.

Now, let’s discount that number back to today’s dollars to get a Present Value (PV). PV represents a lump sum today of what future cash flows are worth. Because the $275 is invested over 30 years, the $389k cumulative asset is actually worth $38,741 if I had it as a lump sum today. I do this, because the cash flows of real estate and S&P500 transactions aren’t the same. By bringing it back down to an PV level, I can compare apples to apples today, so to speak.

PV of S&P500 investment over 30 years = $38,741.

Real Estate Additional $275 ‘Investment’

Similar to the S&P500 investment, over 30 years, I’ll accumulate $99k of additional investment dollars in the house project. However, this doesn’t have the same future value as the S&P500 because the house underpins the future value.

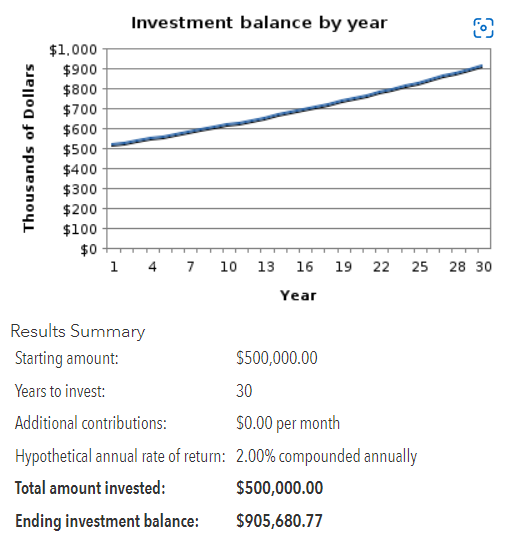

Here is what the property value will look like over 30 years.

Calculator & visualization courtesy of KJE Computer Solutions via American Funds

Calculator & visualization courtesy of KJE Computer Solutions via American Funds

The property appreciates to $906k, assuming 2% annual return, starting from current value of $500k. Zero additional contribution is appropriate for the house calculation, since there are no positive realized cash flows from the property.

The key, though, is that over the 30-year period, the mortage and construction costs have been paid down by the monthly rents. Even though the monthly rents didn’t cover ALL of the expenses, the debts still got paid down over time, and I have a free-and-clear asset worth $906k in 30 years.

To find the PV of the real estate transaction, I need to maintain the 8% Rate of Return (since that’s my opportunity cost to invest in the S&P500).

The Present Value (value today) of the $906k house in 30 years = $90,089. That’s 2.3x the return of the S&P500 when measured in dollars today.

The Comparison

Would you rather have $38k today or $90k today?

Seems like an obvious answer, right?

I’ll take the $90k.

The house only appreciates at 2%. The S&P is at 8%. The house still wins.

What’s the difference? For one, the house is starting with a value higher than the S&P500 investment. However, if you remove the starting value of the house from the future value, the house still yields $406k ($906k-500k). That’s still higher than the $389k S&P500 future value, although not by as much.

How is it possible to have such a large difference!? It’s mainly in how the investments change in value.

The S&P investment derives most of its value through appreciation alone. Yes, there will be dividends…but over the long-term, the lion’s share of value comes from appreciation of equities.

The house, on the other hand gains value through BOTH appreciation AND debt paydown (aka equity improvement). By leveraging debt, I wrangled myself into an asset worth $500k as a starting point, versus starting at $0, as is the case in the S&P investment. The value improves so much more because while the house is appreciating, I am simultaneously gaining equity in the asset as it gets paid down.

To highlight the importance of this even further, we can segment the value of the house into two camps: appreciation and debt paydown (equity improvement). After 2 years, the house only appreciates to ~$520k. However, over that same time, I’ll accrue ~$10k in equity from debt paydowns (using other peoples’ money, IE: rents). Combined, that’s $30k of value, compared to the S&P investment of only $7,100(24 monthly payments of $275 = $6,600 + $510 interest). The equity paydown alone eclipses the value of the alternative investment within 2 years.

This is the power of leveraged appreciation and equity improvement through real estate.

Summary / Consolidation / Conclusion

I am definitely over-simplifying what it means to hold a real estate investment property for 30 years. There’s a lot that goes into it, that just doesn’t matter if you throw the same $275/month into an S&P index. There is management, deferred maintenance, updates, and tenants to deal with.

Perhaps that’s exactly why the returns are so different.

There is an implied opportunity cost of time, that I haven’t mentioned to this point. The simplicity and plug-and-play value in the S&P really works if you’re not into managing rental property. However, the difference in value could indicate the implied worth of property management work over time.

The other thing I didn’t mention in the calculation is that after the 30-year mortgage is up, the house cash flows the full rent, less non-cash and deferred-cash expenses. After all the debt is paid off, that’s effectively $2,225 per month of straight cash flow. Let that hit your bottom line & see what happens.

Stay frosty, friends.

Technical Finance Note: Some of you might have noticed that I used PV of the future cashflow, instead of NPV, which would have included discounts on each of the $275/mo (or $3,300/yr) investment installments. Some others might notice that I didn’t include the cost to purchase and rehab the property in either calculation. I essentially used ‘finished house, renters in place’ as Time-0 in both calcs. This was all done intentionally to keep the calculations relatively simple. If I were to add those to a true NPV calculation, it would yield a similar result, albeit with lower NPV values than PV values. The PV is still an effective method to compare apples to apples of the relative asset values after 30 years. The $99k ‘investment’ over time is the same, regardless of the NPV/PV calculation convention.

How much are you putting down to acquire the 500K property? 100K? How are you accounting for the future value difference between a monthly 275 payment vs putting down a lump sum 100K payment? That's a pretty huge Opportunity Cost delta between those two scenarios. If you put 100K into the S&P for 30 years with an annual return of 8%, you would end up with 1,006,265.69 all without lifting a single finger.

Of course, at this point you'd be subject to 900K in LTCG which is a substantial tax liability. That's where RE and its like-kind exchange option helps to even out the gap.

Also, in real life, a good property would also be providing you with a good amount of income for those 30 years.

Yeah, @Tony Kim, I BRRRR'd this deal. So I got into it for $12,500 down on $250k original purchase price. The $500k is on the after-rehab value.

But you bring up a good point in the size of a lump sum versus time in the market.

The point I was trying to illustrate is that IF I have to pay an extra $275/mo...IF that was going somewhere, it would still make sense for it to be into the property, despite not being CF positive.

Great point though! Throwing a big chunk into S&P would yield a lot more down-the-line...so could RE though, so neither are bad options IMO...just tradeoffs.

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

and thank you, @JD Martin, appreciate the encouragement

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

Quote from @Steve Vaughan:

REI and indexes each have their place.

A househack is a no brainer. Reducing costs like living expenses, buying below market value and adding value at huge multiples are the main advantages of RE.

I would not net positive living in my house without RE or househacking. But my passivity is determined sometimes by things outside of my control like weather and tenants.

But RE takes work and someitmes indigestion.

There should be balance sheet investments as well as cash-flow. Both RE and S&P take buy and homework vs blind buy and hold or buy and hope.

Pivot into opportunities as they present themselves. I moved a lot from RE into the S&P mid June. RE has high transaction costs and long lead times. Buy and homework.

@Steve Vaughan I like how you say that "RE takes work and sometimes indigestion"...it's been true up to this point. I like the passivity of S&P, but at this point in my career, I think I want to scale using RE equity jumps, then move into more passive, "plug and play" options like S&P down the line. Thanks for commenting!

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

Thanks for the further feedback, Joe. I've addressed some of your comments below. I'll think more on how I can describe what I'm trying to do in the future.

Quote from @Joe Villeneuve:

Your next section describes a property that is negative CF just waiting to happen ($100/m CF). If it has a NCF of $275/month ($3300/yr), that means after 5 years you will have paid an additional $16,500 for that property...and will have made no money.

What I'm trying to argue is that even without perfectly CFing the property, I'd still end up ahead from an EQUITY perspective. The asset appreciation and principal paydown (using someone else's money) provide a Net Worth Impact regardless of whether I had to contribute additional money over that timeframe.

Your definition of "opportunity cost" is incorrectly applied here. The alternative investment in the SM. at only 8%, is a linear return. REI gives you an exponential return. The "opportunity loss) over that same 30 year period, would include so many zeros, it wouldn't fit on the page. Comparing the SM to REI, is far from an "apples to apples" comparison.

That's basically my point...that over 30 years, I'd still end up ahead, even if the property required consistent cash re-infusion. I'm just trying to bring that future value back to a number today.

Thanks again for making me think harder on what I'm trying to communicate!

all the best

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

@Joe Villeneuve, thanks for your response. I'm just starting out and appreciate you checking my thinking! Would you tell me more about what you saw that you don't think is prudent? Or what bad assumptions do I make? Would love to understand more of your thoughts.

I was trying to approach it to show the power of REI versus alternative investments. Where did I miss, in your opinion?

Post: Article: Shelter is a Game...not just a living expense

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

You’re a player no matter what your situation is…you’re in the Real Estate game. It’s just a matter of what position you play. This is a philosophy I heard first on the BP Podcasts featuring Bryce Stewart. His episodes, specifically, have been incredibly influential on me.

Money is a game. There are rules, objectives, strategies, and outcomes that people strive for, just like football or soccer or pickleball. I view real estate in the same way: as a game.

For most people (I think), real estate is simply a means of living. Most people are faced with the problem of having a place to live and make one of two decisions: 1) buy a house, or 2) rent. However, if you want to play the game of real estate, your options open up.

Before We Begin — The Risks

Playing the game comes with risk, just like playing any game. There is risk of loss or “injury”. There is risk of failure or “losing”. There is reputation risk, mental-emotional-social risk. There are legal risks or “penalties” for doing things the wrong way.

I’ll acknowledge that playing certain positions in the game isn’t for everyone. Some of the role-specific risks are too great for some people to take on. Unfortunately, many people haven’t been taught/given/provided the tools/strategies/bandwidth/resources to get involved in certain positions.

Not all roles are created equal. Not all outcomes are equitable. Not all resources are evenly distributed. There are winners and losers in the real estate (and any) game.

“Playing” certain roles/positions in real estate requires that you have capital, know-how, resources, and connections to do so. The position you “get to” play requires different types of mindsets, too.

The Players

“Playing” the real estate game goes beyond just buying a house to live in. I’ll divide “the Game” into four categories of players:

- The Renters — people who don’t own the property they use for shelter.

- The Homeowners — the people who buy a property for shelter.

- The Investors — the people who buy a property for other people’s shelter (renters).

- The Supporters — the people who make the investors’ deals happen (real estate agents, loan officers, title companies, contractors etc.)

- The Financiers — the banks that lend to Homeowners and Investors

There is a high barrier to entry to play certain positions

Participating as a Homeowner or Investor requires capital in the form of financial reserves, down payments, and closing costs. Even after purchase, there are significant capital expenditures required to keep the house maintained and functional.

Participating as a Supporter requires professional experience. To become a real estate agent requires licensing. Becoming an appraiser, mortgage loan officer, or banker requires professional accreditation and experience.

The Investor-players seek opportunities to bring value to Renters in exchange for monthly income. The Renters exchange their monthly income for shelter. Investors, theoretically, are incentivized to maximize value in their property, to maximize the return from their investments.

The Financiers back the Homeowners and Investors by providing debt instruments. They expect to be repaid over time for taking the risk on the players purchasing their respective shelters.

The players of the game interact with each other to find each of their own best-outcomes.

In the Real Estate Game ecosystem, everyone is dependent on each other. The Renters provide income to the Investors. The Supporters, very practically, make the deals happen. The Homeowners rely on the Supporters’ expertise to secure their shelter as well.

What it’s like to be a ____ player

There are, of course pros and cons to being certain types of players.

Renters have the flexibility of choice. Within the boundaries of their affordability, Renters dictate to Investors what they want. If there is enough demand driving certain amenities, more Investors will include those features in their value offering. Similarly, if Renters decide they don’t value something as much anymore, Investors will have to pivot their capital to more attractive options. If enough Renters leave a city center during a pandemic for beaches and farms and rural areas, Investors will eventually decrease capital investment in cities and find new short term rental opportunities in more rural areas (ahem, AirBNB and VRBO), for example.

Homeowners might have it toughest. They have the highest volume of regular costs with only their income to repay their shelter expense. People who buy their home for shelter alone are likely not paying for it from rents on other shelters they provide to Renters. Homeowners not only expense monthly debt payments, they also incur capital expenditures, updating costs, and taxes and insurance. Owning your shelter may not be ideal if you’re in an area with exceptionally high property values. Or, you may value the flexibility of being able to move locations every few years…owning your shelter may not be ideal in this instance either.

Supporters come in all sizes and shapes. They’re the ones that keep the business going. They do the cold calls to get Grandma and Grandpa thinking about cashing in on the equity they’ve accumulated over 40 years. They do the property searches and legal process work. They execute on the Homeowners and Investors plans.

The Investors are the most flexible group. They commit capital, much like homeowners, but their repayment structure isn’t reliant on their own income. Investors pay for their properties using other peoples’ money. Very literally, Investors use Renters’ rent for capital expenses, updates, reinvestment, and a risk-adjusted return. Investors are the ones that make coin from real estate, because they are the ones bearing the greatest risk of loss. Homeowners bear risk of loss too, but only to the level of their one property and their ability (or inability) to maintain it. Renters bear no liability because they don’t own the property and are not obligated to update or maintain it. Supporters are more or less hands-off once the deal is done. The Financiers are happy as long as their debt payments are being made.

Consolidation & Conclusion

I consider myself a player in two camps: Investor and Homeowner.

I bought my first shelter as a Homeowner, with the intention of it being my first investment. I’m playing the game like an Investor. I’m not planning on just spending 30 years here, making the monthly mortgage payments. I’m going to get roommates to offset my income. From that extra (offset) income, I’ll then reinvest in the next property. Then the next one. Then the next one.

I don’t consider my shelter as just another living expense. I run my house like it’s a business itself. My house is only an asset if it’s generating a return. It doesn’t generate a return if I’m only playing as a Homeowner and living in it by myself.

There’s flexibility between players, and it’s important to remember the co-dependence between all of them. None can exist without the others.

I hope to provide some level of support/education through documenting my own process. I hope that my story is relatable enough to show others what’s possible.

Post: Article: A thought experiment - Real Estate vs S&P500

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

AND imagine the real estate is NOT cash flow positive. Consider the ‘negative cash flow’ as simply additional reinvestment…just like the S&P.

I am all about building cash flow over time through real estate. However, I’m early early early on in my journey.

I am wrapping up construction on my ‘house-hack’ 3 bed / 3 bath single family home in Minnesota. Once it’s done, I’ll bring on two roommates, and effectively cut my living expenses by $1,500–2,000.

I’m just beginning in the journey and contemplating the two main paths I see before me (on this and the next deal).

I can go after a ‘pure’ tried-and-true-investment-20%down-property. One that cash flows right out of the box with minimal capital expenditure or reinvestment. Or, I can go for another rehab, to capitalize on forced appreciation and net worth impact.

As I consider the options before me, I create thought experiments. I’d like to include you in one today.

The problem with Forced Appreciation (Net Worth Impact) Properties:

Debt costs become too high for excellent cash flow.

Unless you find a gem that really doesn’t need much but looks like it does. If you undertake a total renovation, or “flip”, you’ll have pretty significant reconstruction costs. If you can get a cosmetic fixer-upper, the options open up on the cash flow side.

Construction costs on my current (and first) property have run over $130k. I bought it at $250k in a neighborhood that can support $600k+ property values. Houses that are just blocks from me go for 3/4 of a million dollars. My equity impact will be fine. But the cashflow return may not be.

Cashflow Assumptions

If I tried to rent the house as an entire unit, I could probably get $2,500–2,750. Let’s assume all utilities/trash/etc. are paid by the tenant. This means I don’t have additional cash expense outside of fixed debt payments. We’ll use $2,500 as a conservative estimate for the purposes of this thought experiment.

All-in (mortgage + construction loan payment), my fixed debt costs per month will be ~$2,400. That leaves only $100 of cash flow, BEFORE non-cash and deferred-cash expenses.

Non-cash expense includes an implied 5% vacancy, for example. This is not something that will actually hit the bank account but will impact cashflow at some point. Deferred-cash expenses are depreciation, reinvestment, capital expenditures, and maintenance. When estimating ~15% of rents for expenses like these, monthly noncash and deferred-cash expenses add $375/mo. They represent expenses that will be realized at some point (you just don’t know when).

Therefore, my net cashflow on the high-equity-impact house is negative ($275) per month. That means I’ll have to contribute/invest an extra $275 of my own personal cash per month to maintain the property.

Opportunity Costs

I’ll highlight why this isn’t such a huge deal to me, by using an economics concept called Opportunity Cost.

For those unfamiliar, Opportunity Cost is the implied cost of doing something because it also means you’re NOT doing something else. Essentially what you do is valued against what else you could have done instead.

By having to ‘invest’ an extra $275/month in the ‘non-cashflowing-equity-impact’ house, I can’t allocate that ‘investment’ elsewhere…like the S&P500.

This is what my $275/month investment would look like in the S&P500 over 30 years (the length of my mortgage) at a long-term annual Rate of Return of 8%.

Calculator & visualization courtesy of KJE Computer Solutions via American Funds

My $99k investment over 30 years turns into $389,843. Not bad! 394% total return over that timeframe.

Now, let’s discount that number back to today’s dollars to get a Present Value (PV). PV represents a lump sum today of what future cash flows are worth. Because the $275 is invested over 30 years, the $389k cumulative asset is actually worth $38,741 if I had it as a lump sum today. I do this, because the cash flows of real estate and S&P500 transactions aren’t the same. By bringing it back down to an PV level, I can compare apples to apples today, so to speak.

PV of S&P500 investment over 30 years = $38,741.

Real Estate Additional $275 ‘Investment’

Similar to the S&P500 investment, over 30 years, I’ll accumulate $99k of additional investment dollars in the house project. However, this doesn’t have the same future value as the S&P500 because the house underpins the future value.

Here is what the property value will look like over 30 years.

Calculator & visualization courtesy of KJE Computer Solutions via American Funds

The property appreciates to $906k, assuming 2% annual return, starting from current value of $500k. Zero additional contribution is appropriate for the house calculation, since there are no positive realized cash flows from the property.

The key, though, is that over the 30-year period, the mortage and construction costs have been paid down by the monthly rents. Even though the monthly rents didn’t cover ALL of the expenses, the debts still got paid down over time, and I have a free-and-clear asset worth $906k in 30 years.

To find the PV of the real estate transaction, I need to maintain the 8% Rate of Return (since that’s my opportunity cost to invest in the S&P500).

The Present Value (value today) of the $906k house in 30 years = $90,089. That’s 2.3x the return of the S&P500 when measured in dollars today.

The Comparison

Would you rather have $38k today or $90k today?

Seems like an obvious answer, right?

I’ll take the $90k.

The house only appreciates at 2%. The S&P is at 8%. The house still wins.

What’s the difference? For one, the house is starting with a value higher than the S&P500 investment. However, if you remove the starting value of the house from the future value, the house still yields $406k ($906k-500k). That’s still higher than the $389k S&P500 future value, although not by as much.

How is it possible to have such a large difference!? It’s mainly in how the investments change in value.

The S&P investment derives most of its value through appreciation alone. Yes, there will be dividends…but over the long-term, the lion’s share of value comes from appreciation of equities.

The house, on the other hand gains value through BOTH appreciation AND debt paydown (aka equity improvement). By leveraging debt, I wrangled myself into an asset worth $500k as a starting point, versus starting at $0, as is the case in the S&P investment. The value improves so much more because while the house is appreciating, I am simultaneously gaining equity in the asset as it gets paid down.

To highlight the importance of this even further, we can segment the value of the house into two camps: appreciation and debt paydown (equity improvement). After 2 years, the house only appreciates to ~$520k. However, over that same time, I’ll accrue ~$10k in equity from debt paydowns (using other peoples’ money, IE: rents). Combined, that’s $30k of value, compared to the S&P investment of only $7,100(24 monthly payments of $275 = $6,600 + $510 interest). The equity paydown alone eclipses the value of the alternative investment within 2 years.

This is the power of leveraged appreciation and equity improvement through real estate.

Summary / Consolidation / Conclusion

I am definitely over-simplifying what it means to hold a real estate investment property for 30 years. There’s a lot that goes into it, that just doesn’t matter if you throw the same $275/month into an S&P index. There is management, deferred maintenance, updates, and tenants to deal with.

Perhaps that’s exactly why the returns are so different.

There is an implied opportunity cost of time, that I haven’t mentioned to this point. The simplicity and plug-and-play value in the S&P really works if you’re not into managing rental property. However, the difference in value could indicate the implied worth of property management work over time.

The other thing I didn’t mention in the calculation is that after the 30-year mortgage is up, the house cash flows the full rent, less non-cash and deferred-cash expenses. After all the debt is paid off, that’s effectively $2,225 per month of straight cash flow. Let that hit your bottom line & see what happens.

Stay frosty, friends.

Technical Finance Note: Some of you might have noticed that I used PV of the future cashflow, instead of NPV, which would have included discounts on each of the $275/mo (or $3,300/yr) investment installments. Some others might notice that I didn’t include the cost to purchase and rehab the property in either calculation. I essentially used ‘finished house, renters in place’ as Time-0 in both calcs. This was all done intentionally to keep the calculations relatively simple. If I were to add those to a true NPV calculation, it would yield a similar result, albeit with lower NPV values than PV values. The PV is still an effective method to compare apples to apples of the relative asset values after 30 years. The $99k ‘investment’ over time is the same, regardless of the NPV/PV calculation convention.

Post: Tax Implications for Seller in Seller-Financed Deal?

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

@Steve Vaughan Thank you for the response and sharing your experience on the Seller side! What qualities have you looked for in prospective buyers to ensure they hold their end of the deal? I want to approach this in the best way possible.

The property is owned by a personal trust registered to an address here in the same town. Any recommendations on how to approach them? The property is not currently on the market...I will approach them cold.

Post: Tax Implications for Seller in Seller-Financed Deal?

- Investor

- Stillwater, MN

- Posts 18

- Votes 7

@Ashish Acharya and @Michael Plaks thank you both for your input! Michael, especially the advice about not giving tax advice to the sellers, great reminder there. I should focus the proposal more on the potential interest opportunity vs the tax implications.

That older thread was a good resource too! Got really technical, but I think it highlighted why I should stay away from using cap gains deferral as a core selling point.

Michael, it's an Investment property registered to a personal trust. I'm assuming that how it is taxable would depend on the basis, current value, and value of the note, correct? Any other recommendations/tips for approaching based on the ownership vehicle being a trust?