All Forum Posts by: Eric Fernwood

Eric Fernwood has started 64 posts and replied 782 times.

Post: Getting into investing in Florida

Post: Getting into investing in Florida

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Derek Green,

If you plan to fix and flip houses, you can ignore this post. If you plan to fix and rent, please read on.

The goal of real estate investing is financial independence. Where you invest is therefore the most important decision. The city determines all long-term income characteristics, including:

- Whether rents of existing homes increase faster than inflation. This is crucial for maintaining financial independence—if you invest in a city where rents don't outpace inflation, your purchasing power will decline and you will have to go back to work to supplement your income.

- Operating costs. Every dollar you lose to operating costs is less for you to live on. Below, I compare the overhead expenses of three states with no state income tax.

- Whether you or the government controls your business, you need a pro-business and pro-landlord legislative environment.

- Crime - High crime levels and long-term economic growth do not go together.

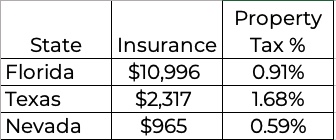

Operating costs vary tremendously by state. Below is a comparison between Nevada, Texas, and Florida.

- State average property tax source.

- Texas and Nevada average insurance source.

- Florida's average insurance cost source

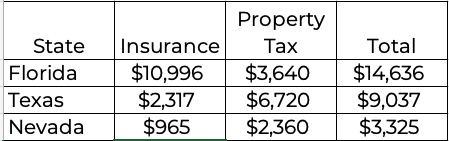

To put this in perspective, below is an estimate of annual operating costs for a $400,000 property.

Compared to a property in Nevada, properties in other states require additional cash flow to compensate for their higher operating costs.

- Florida: +$11,311 ($14,636 - $3,325)

- Texas: +$5,712 ($9,037 - $3,325)

The takeaway is that operating costs can have a huge impact on financial independence.

Remote Investing

Live where you like, but invest where you can achieve and sustain financial independence.

Most investors don't live in cities that meet all the requirements for financial independence. Therefore, the real question isn't whether to invest remotely—it's where and how to do it safely.

Once you've selected a city that meets the requirements, you'll need an experienced local investment team to minimize risk. While books, seminars, podcasts, and websites offer valuable general knowledge, ultimately you're investing in a specific property in a specific city. This requires deep local expertise. Only an experienced local team can provide the local market knowledge and resources essential for success.

Post: New Builds are Actually Good Deals Right Now...?

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Jake Andronico,

Whether new construction is a good option depends entirely on your target tenant segment. In investment real estate, everything depends on having reliable tenants occupy your property. Reliable tenants pay rent on schedule, stay for many years, and take care of the property. Reliable tenants are the exception, not the norm. However, there are tenant segments with a higher concentration of reliable people than others. Success depends on buying properties that attract this segment.

So, reverse the approach. Instead of focusing solely on the property and hoping it attracts reliable tenants. Start by identifying a tenant segment with a high concentration of trustworthy people. You identify this segment by interviewing property managers. Once you know what and where this segment rents today, buy similar properties. This approach dramatically reduces the dependence on luck and opinions.

This approach mirrors how national retail chains select stores and localized offerings. They don’t pick a store location and hope customers will come. Instead, they identify their target customers and open stores near them. They also adapt to local preferences. For instance, McDonald’s offers spam and poi in Hawaii and wine in France.

Does new construction make sense? It depends on the tenant segment you want to attract. We've focused on the same tenant segment in Las Vegas for over 17 years. New single-family homes in desirable areas start at $550,000, but our target tenants can only afford to rent properties priced between $350,000 and $475,000 today. While new construction might seem appealing with its lower maintenance costs and move-in-ready condition, these properties typically attract tenants who stay just one to two years. In contrast, our target tenant segment stays an average of over five years. So, new construction is not a viable option in Las Vegas.

Post: Out of State investing does not work. With very few exceptions.

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Marcus Auerbach,

I agree that OOS investing is very difficult, unless you work with an experienced local investment team. So far, we have delivered over 550 properties to about 180 clients worldwide. Of the 180 clients we've worked with, only 9 or 10 were local. Our repeat business rate is over 90%, and our largest source of new business is existing clients.

My point is that OOS investing works, but only when you partner with an experienced investment team. It simply cannot succeed if you try to do everything yourself.

Investment City Requirements

The location is critical because it defines all long term income performance. If your goal is financial independence, the city where you invest must meet the following:

- Significant and sustained population growth.

- A metro population > 1M.

- Rapid and sustained existing home appreciation.

- Low operating costs.

- Low risk of natural disaster.

- Pro-business and pro-landlord legislative environment.

What are the odds that you happen to live in a location that meets all the city requirements listed above?

Live where you want, but invest where you can build an income stream that enables lifelong financial freedom.

Another Consideration

Everything you learn from books, podcasts, seminars, and websites is general information. You will buy a specific property in a specific location and will need multiple local resources. The only source for what you need is an experienced local investment team. This is true even if you invest locally.

Commenting on the specific issues you stated:

- Renovation: We have long standing relationships with a number of service providers. For example, our preferred renovation company has completed over 440 renovations. So far, their prices are usually $3,000 to $10,000 less than any others. Before we established relationships with specific service providers, it was difficult for me to get any contractor interested in renovations under $25,000. With the relationships we've established, they now know they must take all our deals (large and small) to receive any of our referral business.

- I completely agree with you on "deals in the hood." The fundamental problem is that no property ever paid rent—the tenant pays the rent. So, we focus on a highly reliable tenant segment. Our tenant's average stay is over 5 years, with only 7 evictions in 17+ years out of a tenant population exceeding 1,000. We experienced no vacancies or rent decreases during the 2008 financial crash. We achieved this by identifying the right tenant segment and buying properties similar to what they were renting.

In summary, out-of-state investing is necessary to achieve financial independence, unless you happen to live in a city that meets all the requirements I listed above.

Post: Current SFH landlord, new to trying to expand and do a 1031 exchange

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Michael Fluder,

Whether a location makes sense depends on your goals. If your goal is to buy a property, almost any place will do. If your goal is financial independence, there are specific investment city requirements.

Before I continue, understand that no property ever paid rent. The tenant who occupies the property pays the rent. The property is simply a vessel that a tenant pays to occupy. Therefore, you need to focus on the entity that pays the rent and the long-term income requirements. There are three income requirements to achieve and maintain financial independence, which are determined by the city where you buy.

- (Historic) Rents must rise faster than inflation. If you doubt the importance of rents outpacing inflation, just try buying the same basket of groceries today that you bought a year ago—at last year's prices.

- The income must last throughout your lifetime. Income persistence depends on your tenants' employment, meaning new companies must continuously establish operations in the city and create replacement jobs. This is essential because the average lifespan of a company is ten to eighteen years. Every non-government job your tenants have will disappear in the foreseeable future. So, job creation is critical. A good indicator is rapid and sustained population growth.

- You must be able to acquire multiple properties with minimal total capital. This requires a city where existing properties appreciate rapidly.

If the city where you choose to invest meets all the above (financial independence) requirements, you're ready to proceed. If not, I recommend searching for a location that does.

The other city selection consideration is an experienced investment team. Everything you learn from books, podcasts, seminars, and websites provides only general information. You won't buy a general property—you'll buy a specific property in a specific location, and you'll need specific local resources. The only source for what you need is an experienced local investment team.

Michael, how you feel about a city or property doesn't matter. What matters is how the city/property performs over the rest of your life.

Post: Recession-Resistant Property Types Worth Considering:

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Mohamed Youssef,

Most people focus on property types—single-family homes, condos, commercial buildings, etc.—and hope for the best. I took a different approach: I focus on reliable tenants and buy what they are willing and able to rent.

My ResultsTo give you an idea of how effective this approach is, here are my 17+ year results:

- Delivered over 550 residential rental properties.

- Maintained a vacancy rate of less than 2%.

- Average tenant stays over five years.

- Zero decline in rent or vacancies during the 2008 crash.

- Almost no impact from COVID and the eviction moratorium.

Properties don't pay rent; tenants do. A property is simply a container that people pay to occupy. To have a reliable income, you need properties that attract reliable tenants. A reliable tenant:

- Stays many years.

- Pays rent on time.

- Has stable employment, even during economic downturns (e.g., government or business-critical jobs).

Instead of picking a property and hoping it attracts good tenants, I reversed the process. I started by identifying a target tenant segment, then researched what and where they are renting. From this, I created a property profile with four key elements:

- Location: Where does the target tenant segment already rent?

- Property type: What type of properties do they prefer (e.g., condos, single-family homes, etc.)?

- Rent range: What can they afford?

- Configuration: What are their specific housing requirements (e.g., number of bedrooms, garage size, yard, etc.)?

For example, in Las Vegas, I found that tenants earning $60,000–$85,000 with elementary school children are the best performers. They have secure jobs, are unlikely to buy homes due to high property prices, and tend to be long-term renters.

Why I Avoid Commercial PropertiesWhile some investors prefer commercial properties, I find them less reliable. Here’s why:

- Easy to duplicate: For example, when I moved to my current home about 11 years ago, there were two self-storage facilities within about 5 miles. Today there are over 18. The population has not increased 9 times, so I assume these 18 storage facilities are essentially splitting the same amount of business that the two were splitting 11 years ago. This explains all their signs offering "X months free" promotions.

- Economic sensitivity: Mobile home parks often cater to lower-income tenants, who are the most likely to be laid off during economic downturns.

- Declining demand: Offices of any kind can be problematic. Nationwide, office buildings are suffering from low occupancy rates and declining rents.

Residential properties offer several advantages over commercial properties:

- Demand-driven pricing: Residential property values and rents are driven by supply and demand. In cities with significant and sustained population growth, prices and rents rise rapidly.

- Better financing: Residential loans typically offer 30-year fixed rates, while commercial loans require refinancing every 3–7 years, exposing you to interest rate risk and additional expenses.

- Faster depreciation: Residential properties depreciate over 27.5 years, compared to 39 years for commercial properties, offering better tax benefits.

That said, not all residential properties perform equally. In Las Vegas, only a narrow segment of properties meets my performance criteria.

Income ReliabilityDon't just choose a type of property and hope it performs during the next economic downturn. Instead, focus on properties that attract reliable tenants.

Post: What Are Your Real Estate Buying Criteria When Looking to Purchase a Rental?

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Allen Zhu,

You asked excellent questions, and I agree with Kevin that they call for long answers. I will do my best to be helpful and keep my post reasonable in length.

Selecting a good investment city and property is straightforward. I will explain the process below. Reach out if you have questions.

Let me first share my key assumptions:

- Tenants, not properties, pay rent. A reliable tenant is invaluable—they stay many years, pay the rent on schedule, and care for the property.

- Renters are diverse. Each tenant segment has specific housing requirements and will not rent properties that don't meet those requirements.

- Real estate investing is about long-term financial freedom. Your rental income must outpace inflation, last your lifetime, replace your current income, and continue even when the economy dips.

If we agree on that, here’s how I approach location and property selection:

Location is King

Where you invest dictates your long-term income potential. Look for cities with:

- Strong, consistent population growth: More people needing housing drive up rental demand.

- Rapid property appreciation of existing properties: This lets you acquire more properties with less cash.

- Job growth: Your tenants need jobs to pay rent. Focus on cities that attract new companies. When companies choose a location, they consider:

- Metro population over 1 million: A large, skilled workforce and robust infrastructure. Wikipedia's Metropolitan Statistical Area page

- Low Crime Rates: High crime deters businesses and residents. Do not invest in any city on this list.

- Low Operating Costs: Companies seek locations that allow them to remain competitive, avoiding areas with high taxes and regulations. Property taxes are a good indicator of overall operating costs. LendingTree

- Low Risk of Natural Disasters: Companies are wary of areas prone to natural disasters. The best indicator of natural disaster risk is homeowners insurance costs. Do not invest in cities with high insurance rates.

Property Selection: Target Your Tenant

Instead of buying a property and hoping for reliable tenants, flip the script: identify a tenant segment with a high concentration of reliable people. Talk to local property managers to determine the right segment (reach out if you want specific questions to ask). Once you've identified your target segment, observe what and where they're renting. Then, buy similar properties. The key is meeting the housing requirements of the people you want as tenants, not guessing. Depending on the city and the tenant group, this approach is adaptable—it could be condos, single-family homes, or townhouses. And the principle applies universally to in-state or out-of-state investments.

I hope this helps.

Post: Machine Learning to predict comps

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Stephen Morales,

Accurate rent estimation is crucial for real estate investing, as it determines a property's viability. To ensure accuracy, we evaluate each property's rent three to four times, as detailed below.

First Estimate

We developed a data mining engine that evaluates 5,000 to 20,000 properties each morning, completing analysis of 15,000 properties in under five minutes. A significant challenge is the poor quality of MLS data. For example, the MLS once showed 62 bathrooms for a 1,600 sq ft property.

The data mining engine performs a two-step evaluation. First, it eliminates properties that don't match our target tenant segment's housing requirements. We believe tenants are the ones who pay the rent—the property is simply a vessel to attract the right tenant. To generate reliable rental income, you need tenants who stay many years, pay the rent on schedule, and maintain the property well. We vet each property against about 40 tenant segment behavioral characteristics. If a property fails any test, it is eliminated from further consideration.

Our track record demonstrates this approach works: our average tenant stays over five years, we maintain less than 2% vacancy rate, and we've had only 7 evictions in over 17 years across more than 1,000 tenants. Even during the 2008 financial crash, our clients experienced zero decrease in rent and zero vacancies.

Software cannot accurately estimate rent because rental prices are driven by human behavior. My research shows that people often make decisions that data models fail to predict. Additionally, there are fundamental flaws in how software estimates rental rates.

- Property condition is critical yet difficult to verify. MLS photos are often outdated and may not reflect the current state. For example, when I checked a fire-damaged property that was completely unrentable, the platforms estimated monthly rents between $1,900 and $2,200. This demonstrates how no software, including mine, can accurately evaluate a property's condition.

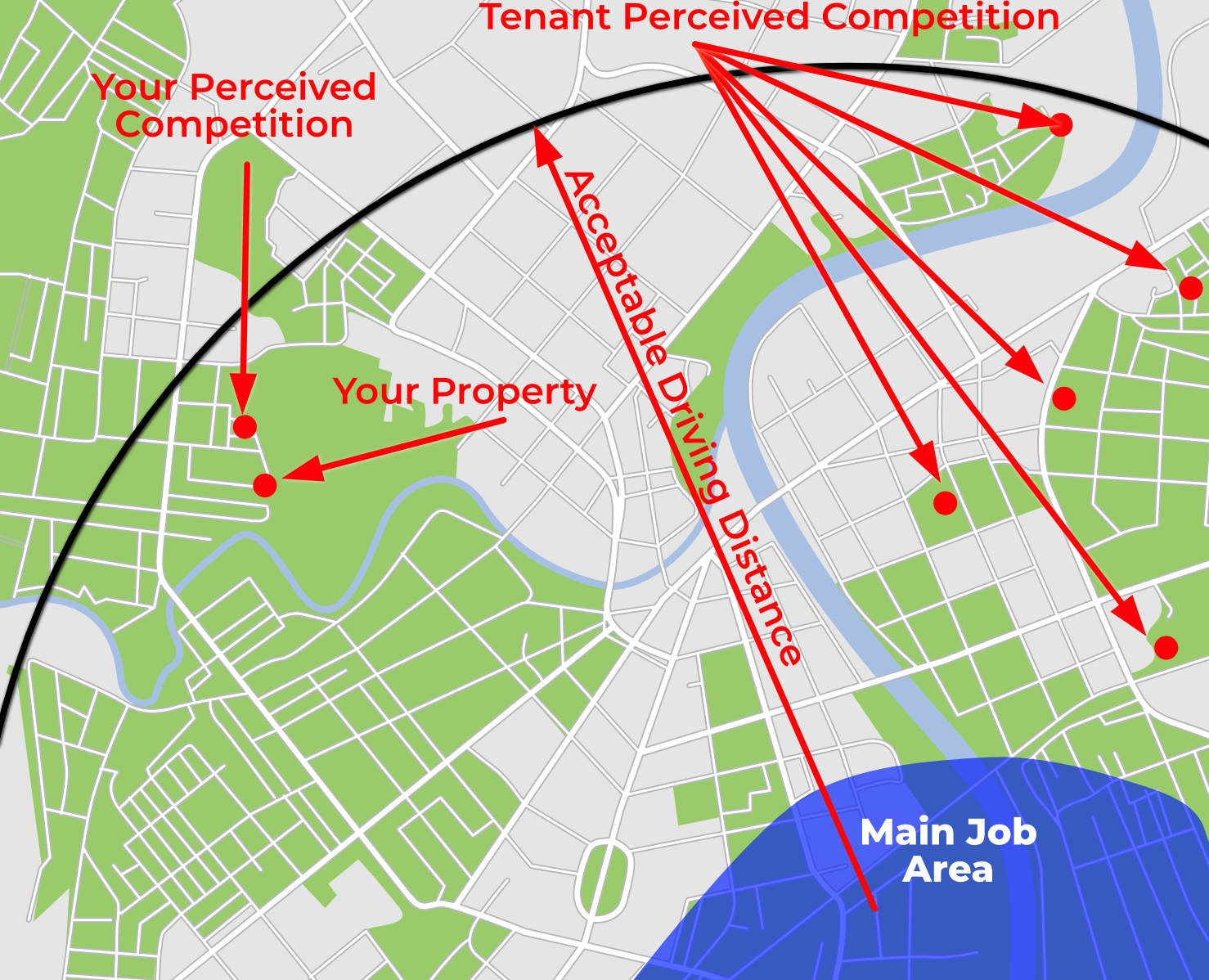

- Another misconception is that rental rates of nearby similar properties reliably predict a property's rental value. In reality, prospective tenants don't restrict their search to a single neighborhood. Instead, they primarily choose locations based on commute time to work. They'll consider any property that meets their needs, regardless of its location in the city. This means your true competition isn't just the property down the street—it could be a house across town.

Second Estimate

Properties that meet all criteria and match a client's specific financial requirements undergo a thorough manual evaluation. This crucial step addresses what software cannot evaluate—poor floor plans, nearby nuisances, lessons from past experiences, and the property conditions from MLS photos. Only an experienced professional can make these assessments. Here's an example: I visited the house marked on the map below several years ago. The traffic noise from I-15 was so overwhelming that my client and I had to shout to hear each other. Due to this severe noise issue, the property is essentially unrentable. Only an experienced person can recognize such property-specific challenges.

Third Estimate

For properties that pass the manual evaluation, we perform an onsite evaluation. Our assessment begins while we're still in the car. For example, if we hear a barking dog next door, we stop the evaluation immediately—our target demographic won't rent a property with that issue. If we believe the subdivision and the exterior will appeal to our target segment, we enter the property.

Properties are eliminated due to factors like poor flow, insufficient kitchen counter or cabinet space, odors, and other issues. Our evaluation is based on how our target demographic will assess the property. Our personal preferences don't factor into the decision.

For promising properties, we capture a video walkthrough and forward it to the property manager. To ensure objectivity, we provide only the MLS number and our video—nothing else. This forces the property manager to evaluate based purely on market conditions, property condition, and her expertise. Her assessment includes projected rent ranges, estimated leasing timeframes, and recommended renovations, all based on current market competition.

Fourth Estimate

The fourth estimate takes place during due diligence, after all inspections are complete and vendor quotes are received. The final rental rate largely depends on the scope of renovation and other key factors. All these elements must be carefully considered to accurately estimate both the rental rate and time to lease.

Summary

- Understanding tenant segment behavior: Through years of studying our target demographic's housing preferences, we've identified key factors that make properties undesirable to them. For example, yards must be larger than 3,000 square feet. These criteria are implemented through rule-based software.

- Undesirable streets and floor plans: This is a large dataset we accumulated and use as another elimination filter.

- Property evaluation: This involves applying weighted scores to each property's characteristics.

- Once we have a set of properties that match our target demographic, we continue to evaluate the property through highly trained professionals.

Stephen, after exploring various options over the years, including AI, I've concluded that nothing matches the accuracy of a skilled team. Software can provide a starting point but accuracy requires human expertise.

Post: Vegas a good place to move to from Lose Angeles

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Ivaylo Chaprazov,

I've lived in Las Vegas for nearly 20 years, having moved here from NYC. It took me about a year to adjust to life in the Mojave Desert, but Las Vegas is the best place I've ever lived—and I've lived in various cities and countries. I plan to stay here permanently.

- Nevada casinos had their second-best win performance in history in January, the Nevada Gaming Control Board reported Thursday.

- And that came a month after recording their best month ever.

The actual results do not match what you heard.

On crime, here is an episode of “The Ben (Horowitz) and Marc (Andreessen) Show” on Las Vegas becoming the SAFEST City in America. Here is an article (Yahoo News): “Homicides, robberies, burglaries, and car thefts dropped in 2024 compared to the year before.”

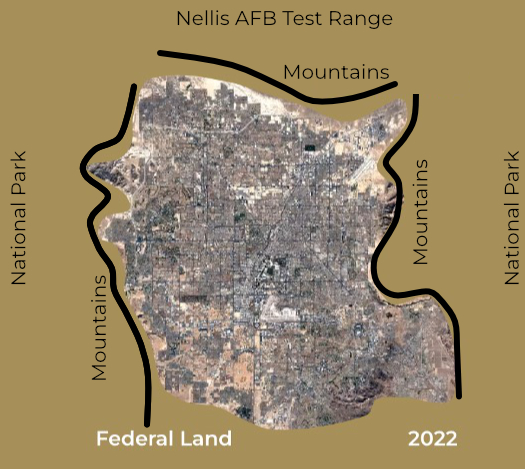

If your goal is financial independence, Las Vegas is an outstanding location for investing due to its rapidly increasing population and little room for expansion. See the 2022 annotated map below.

Today, I estimate only about 16,000 acres of raw land remain, and this cannot be increased due to natural boundaries (mountains) and various tribal, DOD, federal, and state parks. The result is that the remaining land in desirable areas sells for $1M/acre.

Our target tenant segment can afford rental properties priced between $350,000 and $475,000. However, due to high land costs, new single-family homes in desirable areas start at $550,000 and come with extremely small lots.

With Las Vegas adding 40,000 to 50,000 residents annually, primarily families renting single-family homes, demand keeps rising, but inventory is (almost) fixed. Since 2013, prices and rents have increased by 10%/Yr and 8%/Yr, respectively (for our segment).

If you want to know more about investing in Las Vegas, DM me.

Other advantages of Las Vegas:

- No state income tax.

- Pro-business environment. For example, an eviction typically takes between 17 and 35 days.

- Reasonable cost of living

- Rapid job growth. With over $28B under construction or in the late planning stages, jobs and a reasonable cost of living will continue to draw people to Las Vegas, increasing demand (and prices and rents) for the fixed housing inventory.

- Strong law enforcement is significant to me, having lived in cities like Oakland, NYC, and similar places.

- Always something to do. If you are bored in Las Vegas, it’s your fault.

Things that I had to adapt to:

- Mojave Desert: Moving here required adjusting my outdoor routines. Instead of visiting parks at midday like I used to, I had to work around the weather—summers are too hot and winters too cold (for me) for afternoon activities. Fortunately, all parks are well-lit, making summer evenings perfect for visits. With few insects around, nighttime activities are great. In winter, like in NYC, it's too cold to spend much time outside. The upside is that we get very little rain.

- Small yards: Land is very expensive in Las Vegas, so yards tend to be small. I was accustomed to spending time in my yard, gardening, and such. In Las Vegas, yards are less important because it's too hot or cold to enjoy them. Plus, there is little or no grass to mow—which makes sense since grass doesn't belong in a desert.

Summary

Like every place, Las Vegas has its pros and cons. However, I've found it an outstanding place to live and invest. With the continuous development, I believe the city will only improve over time.

Post: Starting with a Friend (LLC?)

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

Hello @Melissa Stanley,

Over the past 16+ years, I’ve worked with over 180 investors. A common question I get is about pooling resources to buy properties. While this can work, the biggest pitfall is assumptions.

NOTE: I’m not an attorney or business advisor. The following is based on my experiences and should be reviewed by an attorney.

Here's an example: Two friends teamed up to invest in a property. A few months in, the refrigerator broke. One wanted a used replacement to save money, while the other insisted on a new one with a warranty. This minor disagreement strained their friendship—and I've seen worse.

How do you avoid this? Create a detailed agreement upfront. A lawyer can ensure it's clear, legal, and comprehensive, but it's best to draft the basics together first. Below are key items I've seen in teaming agreements:

- Ownership Interest: Define each party's ownership percentage based on contributions like the down payment and ongoing costs.

- Financing Details: Clarify who pays for what—mortgage, closing costs, renovations, etc.

- Expenses: Outline how regular costs (taxes, insurance, upkeep) will be split.

- Management and Maintenance: Decide who handles repairs and improvements, including decision-making processes, funding, and responsibilities for performing or managing the work.

- Single Decision Point: Avoid deadlocks by assigning one person as the final decision maker.

- Dispute Resolution: Agree on a method (e.g., mediation or arbitration) to resolve conflicts.

- Life Changes: Plan for marriage, divorce, incapacity, or death.

- Exit Strategy: Define how a party can sell their share, including buyout terms and a method for determining the sale price.

- Rental and Use: Define the rules for renting out the property. Also, agree on how the property will be used, who can live there, and under what conditions.

- Financial Shortfalls: Address what happens if someone can’t meet their obligations.

- Legal/Professional Fees: Decide how legal and other professional fees related to the purchase and management of the property will be shared.

- Taxes: Determine how tax benefits will be divided.

Summary

Melissa, the time you spend creating a thorough agreement now will save you headaches—and possibly your friendship—later.

Post: Chicago Investors we have a serious problem : Call to Action

- Realtor

- Las Vegas, NV

- Posts 813

- Votes 1,563

It's hard to believe such regulations as described in the thread are implemented anywhere. The end result will be fewer rental properties, minimal maintenance (properties in poor condition to reduce maintenance costs), and higher rents to compensate investors for additional costs and risks.

A rental property is valued by the cash flow it generates and its appreciation potential. When regulations increase risk, cap rent increases, and make it difficult to evict non-performing tenants, it's time to consider a 1031 exchange.

I was living in NYC in 2004 when I decided to start an investor services business. It took little time to realize that New York, New Jersey, and similar states were not good for real estate investing. I chose to relocate to Las Vegas for the following reasons:

- Unless the courts are backlogged (like after the end of the eviction moratorium), an eviction takes between 17 and 35 days, if you know what you are doing. Because evictions are quick and cost effective, tenants know that if they don’t pay rent, they will be evicted.

- The standard leasing agreement has significant landlord protections, thereby keeping rents lower.

- There is no obligation to renew a lease.

- If a property is sold and there is a tenant in the property, the lease survives the sale. However, the tenant has no say in the sale, such as you stated.

There are many other advantages of where I chose to relocate.

The anti-landlord regulations in many states are why we've completed over eighty 1031 exchanges. At some point, rent control and high operating costs make real estate investing no longer viable.