How to Make Money In Any Market

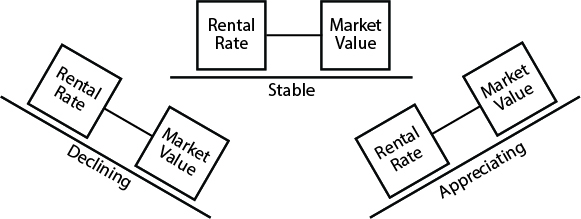

Simplistically, real estate markets are in one of three states:

- Declining

- Stable

- Appreciating

Obviously, there are many more states if you include transitions between states, seasonal variations, etc. However, for simplicity, I will just use the three states in this article.

You can make money in each of the three market states, provided you use the right strategy and are aware of the exit point and the risk. Also, you need to understand what causes a market to be in the different states.

Simplistically, it’s all about jobs.

Job Quality and Quantity

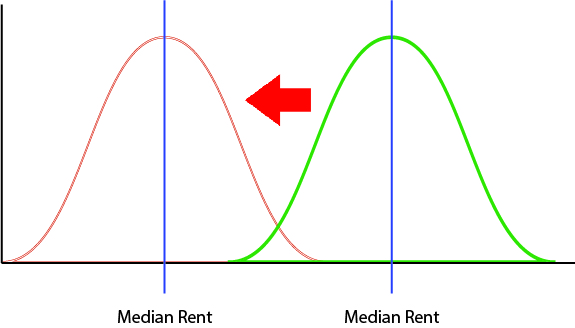

Any investment property is no better than the jobs around it. Simplistically, if your tenants are unemployed, they are not paying rent. However, just being employed is not the only consideration. In many parts of the US high paying manufacturing jobs have gone to more cost effective locations and what remains is service sector jobs, which drives down property prices and rents. Many manufacturing jobs paid $40/Hr plus benefits. Typical service sector jobs pay between $11/Hr and $13/Hr. What does this mean to you as a landlord?

The maximum amount of rent a tenant is willing and able to pay is about 30% of their monthly income. Below I compare the probable rent based on their monthly income:

- At $40/Hr.: $40/Hr. x $40Hr./Wk. x 4Wks/Mo. x 30% = $1,920/Mo.

- At $13/Hr.: $13/Hr. x $40Hr./Wk. x 4Wks/Mo. x 30% = $624/Mo.

Would you see such a drastic change overnight? Very unlikely. What you would see is a decrease over time in the median rent for the area.

The same is true with property prices. As the median income level falls for a location, so will property prices and rents. Bottom line, demand drives rent and property prices and demand is all about job quantity and job quality.

Nothing Stays the Same

“The only constant in life is change”-Heraclitus

ROI and cash flow are only snapshots in time. They provide a reasonable estimate of how the property is likely to perform today but nothing about how that property will perform in 5 or 10 years. What is happening with jobs will tell you what is likely to happen to property prices and rent.

Businesses (the provider of jobs) are like people. They grow, they mature, they die. Suppose you collected a fixed number of people (of the same sex!) in a sealed off location. Over time the population would dwindle to zero. However, if you added people over time, then the shrinking of the original population would not matter. The same is true with jobs. If a location is not desirable to new businesses, it is only a matter of time before the current employers die off and there are less and less jobs. That is why the ability of a location to attract new employers is critical. Said succinctly, if new employers aren’t moving to a location, the location is a declining market and prices and rents will fall over time. Remember that employers select the location that they think will best meet their needs from across all cities in the US. Cities with a reputation for high crime levels, anti business environments, high taxes, etc. will not even make the short list.

So, the barometer is not just today’s jobs, which is what return estimate reflects, it is about the ability of the location to attract new employers.

While jobs is the barometer, you can make money in any of the three market states as long as you use the right strategy.

Declining and Appreciating Market Similarity

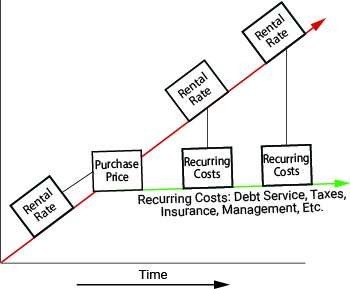

What makes investing in declining markets and appreciating markets similar is that rents lag property prices by 2 to 10 years. So, in a declining market, rents are artificially high. In an appreciating market, rents are artificially low. In a stable market, rents accurately reflect prices. The driving force is demand. If there is decreasing demand, prices and rents fall. If there is increasing demand, prices ands rents rise.

Declining Markets

Situation:

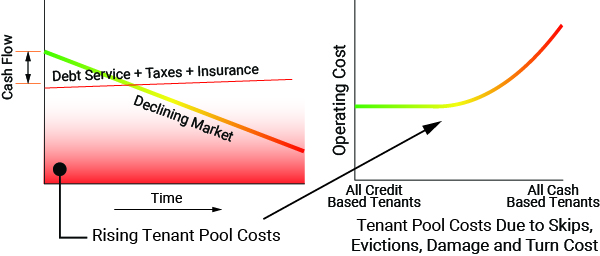

Since rents historically lag property prices by 2 to 10 years, the rents you see today reflect property prices in the past. The result is relatively high levels of return.

Characteristics - some or most of the following:

- Declining population

- Declining job quantity and/or quality

- Declining inflation adjusted per capita income

- Declining employer base

- Declining property prices and rents

- Large housing supply (>6 months inventory)

- High return

- Properties tend to be older

- Higher crime levels

- Anti business environment

- High state income tax and property tax

Strategy:

This is a high risk market. Focus only on current return, appreciation is not a factor in declining markets. The goal is to buy a property and only hold it long enough that you make significant money and get out before the price falls so low that you can’t get out. With proper execution, even if you sell the property at a loss, you will have made enough in cash flow so that you come out ahead. Focus on minimizing acquisition cost (down payment + closing costs + rehab) and minimizing ongoing maintenance costs. Pay attention to the condition of: roofs, plumbing, window frame, siding, painting, etc. As rents and prices fall, your tenant pool will become more dependent on public transportation. Focus on properties near major transportation routes that will deliver them to their jobs if you plan to hold the property for more than a few years.

Stable Markets

Situation:

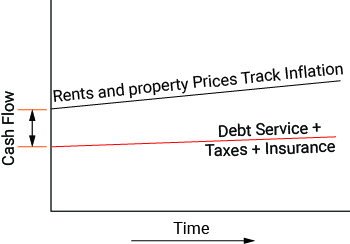

Stable employment, stable population. Property prices and rents track inflation.

Characteristics - some or most of the following:

- Medium return

- Stable job quantity and/or quality

- Stable population

- Stable inflation adjusted per capita income

- Stable employer base

- Stable property prices and rents

- Balanced housing supply such as 6 months inventory

- Neutral business environment

- Average or below average state income and property tax

Strategy:

Buying in a stable market is about cash flow. Appreciation and rents historically track inflation. The goal is to buy a performing property and hold it indefinitely. Focus on minimizing acquisition cost (down payment + closing costs + rehab) and minimizing ongoing maintenance costs. Pay attention to the condition of: roofs, plumbing, window frame, siding, painting, etc. to keep long term costs down.

Appreciating Markets

Situation:

- Increasing returns because rents rise while costs are relatively constant.

- Since rents lag prices by 2 to 10 years, your exit watch is when property prices start to decline. You will have time since rents will continue to rise when prices start to level.

Characteristics - some or most of the following:

- Lower return

- Increasing job quantity and/or quality

- Increasing population

- Increasing inflation adjusted per capita income

- Increasing employer base

- Increasing property prices and rents

- Tight housing supply (< 3 months inventory)

- Pro business environment

- Below average state income and property tax

Strategy:

Buy a positive cash flow property in a desirable location and ride the appreciation and rent increase curve. This is a very low risk market. As long as you buy property in a good location, all but the worst mistakes will be corrected over time through appreciation, inflation and rent increases. What contributes to the low risk of this type of market is that rents lag property prices by 2 to 10 years. If you see property prices start to level out, you have plenty of time to sell (1031) at a profit.

Summary

Every market is different so you must adjust your strategy accordingly. However, the above should provide a reasonable understanding of:

- The importance of job growth.

- Declining markets are all about current return and timing your sale.

- Stable markets are primarily cash flow and long hold periods.

- Appreciating markets are about starting off with an acceptable cash flow and riding the appreciation curve.

Comments (1)

REAL ESTATE OUTLOOKMAY 2018

LOS ANGELES, CA. Recently, we have seen a cyclone of economic and political news and developments that has affected the real estate industry. Overall, these developments have created somewhat higher downside risks. Growth and inflation data over the last month have not come up to our forecasts. In our view, the mixed data suggests a temporary pause in growth. Lower inflation data could indeed imply slightly higher labor costs and perhaps the continuation of a Pollyanna outcome.

The Federal Government is moving ahead with monetary tightening. Several risks are rising, in our view. First, the risk of an escalation in trade tensions, with the investigation into Chinese intellectual property practices. Second, risks in the Middle East are rising again. Third, rising tensions with European countries could hinder an already-difficult reform process. In addition, there is a flattening in the US Treasury yields. Currently, we do not think that these developments have a major significance for the real estate markets. However, if there is a return to a situation of rising risk in the US dollar, this upset could cause prices to become volatile again.

Although Treasury yields have flattened again, they are close to the recent lows. At this point, we think there is no major cause for concern yet. In the US, the downward revision of the first quarter 2018 is partly offset by some upward revision for fourth quarter 2017, and employment remained strong. . Overall, growth in the first quarter still appears to be at a 3% pace, and is expected to pick up later in the year, because of the effects of the US fiscal stimulus.

Because of robust growth and subdued inflation, we believe that this has supported valuations of the industry over the last few years. Keep in mind, there are questions during the period of moderate financial market volatility. The most recent data suggest that the Pollyanna effect may persist for a little longer. Therefore, we are staying with our belief of economic growth. However, it is still too early to jump to a conclusion as to the end of the current upswing, despite ongoing trade tensions.

The Los Angeles Times recently reported that institutional investors bought more single-family rental homes in 2017 than in previous years, the first increase since 2013, according to data compiled by Amherst Holdings.

Wall Street firms such as Blackstone Group and Tom Barrack’s Colony Capital Inc. rushed into the single-family rental business when U.S. housing markets were reeling from the foreclosure crisis and homes were available and cheap. The feeding frenzy was short-lived. By 2014, big landlords were already paring back their purchases as foreclosures dried up and they tackled the challenge of managing widespread homes. Now they’re buying again, at a time when single-family landlords are raising rents faster than apartment owners are. While multifamily landlords face pricing pressure from new supply, very few single-family homes are built specifically for leasing.

Demand for rental houses “feels like it’s insatiable,” Gary Berman, chief executive of Tricon Capital Group Inc., said in an interview.

Tricon, the third-largest publicly traded owner of U.S. rental houses behind Invitation Homes Inc. and American Homes 4 Rent, bought about 850 homes last year, said Amherst, which analyzed data from CoreLogic Inc. The biggest purchaser was Cerberus Capital Management, with an estimated 5,100 houses. Amherst itself bought almost 4,900 homes through its Main Street Renewal subsidiary.

There’s another factor driving Wall Street’s renewed acquisitiveness. Now with their businesses well established, the large landlords are having an easier time financing purchases, said Greg Rand, CEO of OwnAmerica, an online platform for buying and selling rental houses.

Rental properties should remain well ahead of other major property types because they are generally more stable. Three important factors account for this stability:

1.They are less dependent on business cycles for occupancy than anyother types of real estate investments. It does not matter if interest rates and home prices are high or low, rental properties are generally more affordable.

2.Rental properties have shorter leases; thereby offering greater protection from inflation than the long-term leases associated with other properties. That is, rents can be negotiated more frequently.

3.The pool of tenants is much greater for rental properties than other types of properties. This ensures a more consistent occupancy than industrial and commercial properties, which usually have only a few tenants from which to choose.

ABOUT THE AUTHOR: Eugene E. Vollucci is the Director of The Center for Real Estate Studies, a real estate research institute.He is author of four best selling books and many articles on real estate rental income investing and taxation. To purchase a subscription to Market Cycles and to learn more about the Center for Real Estate Studies, please visit us atCALSTATECOMPANIES.COM

Eugene Vollucci, over 7 years ago