Real Estate Deal Analysis & Advice

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated over 14 years ago on . Most recent reply

Input on prospective deal. newbie

I was hoping to get as much input as possible on my first deal

reo

purchase price- 300k

down payment- $10,500

fha owner occupied 3 unit

$1050 a unit gross rent

$2650- p.i.t.i,

vacancy rate- 4%

low maintenance, built in 2000, tenant paid utilites

estimated value after minor repairs- 360k-400k based on comps

any comments on this deal would be greatly appreciated

thanks

Most Popular Reply

So, again, spend some time reading in the Rental Property forum. You'll read about the "50% rule", which says all expenses, vacancy, and capital items will average out to about 50% of the gross scheduled rents. Of course, any particular property may have somewhat lower expenses any particular month or year. That's limited by the taxes and insurance, which are the start but hardly the end of expense. You have acknowledged vacancy, though 4% is unrealistically low. Maintenance is an ongoing issue, and is mostly caused by tenants. Then there are the nightmares like a long eviction or major tenant damage. There are also the occasional, but large, expenses like furnaces, sewer lines and roofs.

Now, if you're willing to do the property management for free, the actual expenses would be lower. I tend to use 40%, fully acknowledging I'm putting effort into the property without getting paid. So, how does this deal look:

Price: $300K

Down payment: $10,500 (plus closing costs, probably another $10K)

loan: $289,500

Payment: $1554 (5%, 30 years)

Scheduled rents: $3150

Expenses; $1260 (40%, yes, they will be that high)

NOI: $1890

Cash flow: $335

So, as an investment property, this one makes $335 a month. In reality, most of that is what you're earning by being the property manager. PM's typically take 10% of gross schedule rents, plus fees for filling vacancies. So, this one's really just break even. That's why I said this was a bad deal in my first post. If your $2650 PITI number is accurate, you have about $1100 in taxes and insurance. That's 34% of gross scheduled rents, so 40% is actually unrealistically low if your taxes and insurance are really that high. Perhaps you were using a higher interest rate.

But, you're living in one of the units. So, that's $1050 out of your cash flow. You're really looking at about $714 out of pocket each month.

Now, certainly it doesn't come out each month. If you're collecting $2100 and paying a $2650 nut, you're only out $550 most months. Nevertheless, you should take the additional $164 (more, really) and put it into a reserve account. Once you have at least $10K in that reserve account, you can relax a little. But rest assured at some point you will have something happen that eats some of that reserve account.

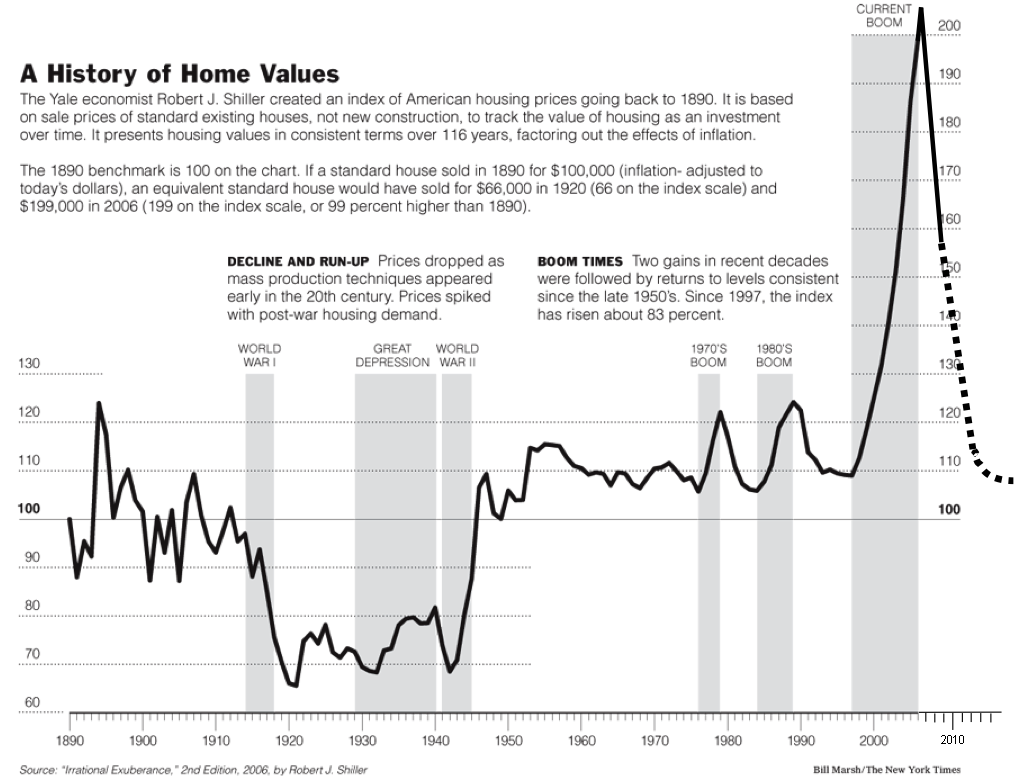

"Investing for appreciation" is speculation. Yes, it could happen. But it also can go very badly, as anyone who bought from about 1999 until 2009 knows. Historically, appreciation has just matched inflation:

Link to graph

That's the inflation adjusted, long term Case Shiller home price data, updated by the NY Times. The link will get you to a bigger one. The scale is 1890 to 2015. Historically, inflation has averaged about 3%. If that house appreciates by 3% for the next 30 years, it will be worth $728K. You might think "woo hoo, $428K in gains" vs the $300K purchase price (neglecting costs of buying and selling, which would only be about $80K total.) However, you'll have paid a total of $559K in payments, so the net gain on the property itself is $168K.

Now, one can hope that over the long term rents go up. You can pretty much count on expenses going up (whether rents do or not). Rents do sometimes go down, too. Assuming you hold onto a fixed rate loan, and don't refi, your cash flow can turn positive. If rents and expenses both increase by inflation, after 30 years you have:

Rents: $7646

NOI: $4588

Cash flow: $3033

Cash flow in 2010 dollars: $1250

So, this deal may improve over time. If you have tenants paying all the expenses, so you're not out of pocket while you hold, and we do get some appreciation, you can end up with a $728K property that didn't cost you anything to own and that you now own free and clear. But there are absolutely no guarantees on appreciation. Ask anyone who bought in 2006. I seriously doubt properties in the boom areas will see their 2006 prices anytime in the next 30 years.

Are you sure you can't find a better deal than this one?