-

All Forum Categories

-

Followed Discussions

-

Followed Categories

-

Followed People

-

Followed Locations

-

Market News & Data

-

General Info

-

Real Estate Strategies

- House Hacking

- Commercial Real Estate Investing

- BRRRR - Buy, Rehab, Rent, Refinance, Repeat

- Mobile Home Park Investing

- Innovative Strategies

- Land & New Construction

- Multi-Family and Apartment Investing

- Wholesaling

- Rehabbing & House Flipping

-

Short-Term & Vacation Rental Discussions

presented by

- Tax Liens & Mortgage Notes

- Medium-Term Rentals

- Buying & Selling Small Businesses

- Outdoor Hospitality

-

Landlording & Rental Properties

-

Real Estate Professionals

-

Financial, Tax, & Legal

-

Real Estate Classifieds

-

Reviews & Feedback

Velocity Banking / HELOC Checking Acct - It Works (Proof)

Hi, everyone. I wish everyone knew how great this strategy is, so I'm trying to spread the word. I'm not selling anything, just trying to let people know how it works.

When you're paying your mortgage month in and month out, you are paying MOSTLY interest for many years. That's because you are paying interest on the whole loan - $200K @ 4%, let's say. In the first year you'll only bring the balance down about $4K, but you'll pay about $8.5K in interest - twice as much, obviously. To pay the balance down $10K it will take you 2.5 years and over $20K in interest. To me, that's a sickening waste. Check out from Sept to Sept on this pic. Only $4K in principal yet $8.5K in interest. Work it out on bankrate yourself (link at bottom) and you can see how long and how much interest is wasted to pay off $10K from your mortgage. And this should go without saying, but if you're further along in your mortgage then your savings will be less, because you are paying less in interest at that point. This strategy is more suited to someone who is in their first decade of a mortgage.

Now, follow me here. You can take all of your extra money and put it toward your mortgage which will shorten your mortgage and save you on interest. Most people know this. But most people also realize that money is usually tight and many people don't have $400 for an emergency let alone a bunch of extra money to put against their mortgage. Anyway, do that if you want, but there's also another better way to accomplish the same thing.

Here's how it works. You get a HELOC or a PLOC with a reasonable rate. It doesn't have to be 4%, but it also shouldn't be 18% like a credit card. You take a portion of your mortgage ($5-10K, for example) and put it on the HELOC. Then you put all of your income toward the HELOC and try to depress the balance as much as possible all month. When bills come you use HELOC funds to pay them, because you're not putting your income into a checking account anymore. You continue like this, putting all bills and income toward the HELOC balance. Since you make more than you spend, the balance will gradually come down. Then you put another portion of your mortgage on the HELOC and repeat the process.

Here's how and why it works (and works better than just paying extra principal when you have the money):

1. You are putting all of your available "checking" funds toward your mortgage at all times, yet you still have money to pay bills due to the revolving credit line.

2. Money that you DON'T end up using toward bills stays on the mortgage balance permanently, limiting the amount of interest you will pay.

3. Money that you DO end up using toward bills temporarily "leans" on the mortgage balance keeping it down and limiting the amount of interest you will pay.

4. Here's the silver bullet, though, that most people can't fully grasp. On the above mentioned $200K / 4% loan you will pay $144K in interest over 30 years paying by the amortization schedule. For that amount, you might as well have purchased an extra smaller house. But here's the thing - the interest is SCHEDULED, but hasn't been CHARGED TO YOU YET. If you struggle with this idea, imagine that you won the lottery tomorrow and wanted to pay the house off. You'd pay off the balance of your mortgage, but not the balance and all the scheduled interest charges. In other words, the interest can be AVOIDED COMPLETELY by paying the principal back early, but time is of the essence. The more you pay and the faster you do it the better. So, remember above when I explained that it takes a person about $20K in interest to pay down $10K in principal? Well, when you put that $10K on the HELOC, you COMPLETELY AVOID the $20K in corresponding interest payments on the mortgage (like the lottery example, just a smaller amount) and it will cost you about $1000 in interest to pay off on the HELOC. This allows you to save TENS OR HUNDREDS OF THOUSANDS OF DOLLARS simply by adjusting the way you pay it. It's not a scam or a method of gaming the interest rates or anything like that, it's simply a way of paying more efficiently without having thousands of dollars lying around to throw at your mortgage.

5. When you pay these large chunks, your subsequent REGULAR PAYMENTS are also more effective, because your principal / interest ratio is improved by quite a lot. Normally, every month you will pay $1-$2 less toward interest than the previous month, but the month after you take $10K off of the mortgage your regular payment will charge about $30 less toward interest than the previous month - and every month thereafter. So, you are saving all the interest from #4 as explained, but every month you're also paying significantly less toward interest (and more toward principal) than you were before. Each time you take another "chunk" off of the mortgage your regular payments also become that much more efficient.

Hopefully, that covers the explanation, but I told you there was proof, so here you go. Here's my closing package where it says that this month I should be at a balance of about $290K.

And here's my actual loan balance of $236.5K. So, as you can see I've been able to put $53.5K extra toward my mortgage over the last two years (started the strategy May 2018) and I haven't been skipping lattes or doing any other financial voodoo. All I have done is started using the HELOC to pay off chunks of the mortgage like I explained and because of all the various mechanisms I described I've been able to put a ton of extra money toward the mortgage. When I look at the balances of $290K and $236K on my closing doc, I find that it is about 85 regular payments (7 years) shaved off the mortgage at an average of $825 interest per month (first payment in range $907 / last payment in range $743). 85 payments at an average of $825/month is $70K worth of interest savings in only two years. Obviously, I have a higher dollar mortgage, so your results may vary, but this isn't milk money, it's life changing money simply from rearranging the way you pay your number one expense. Let me know if you have any thoughts or questions. Thanks!

- Rental Property Investor

- Clarkston, GA

- 1,906

- Votes |

- 2,039

- Posts

- Rental Property Investor

- Clarkston, GA

Hi Thanks for posting this! I've read much about this tactic some from orgs wanting to coach you. I'm replying not to say anything negative re saving on interest paid but on what just my thinkig is. Possibly also on lost opportunity costs of using ones HELOC to buy a one time gain (interest avoided) vs a lifetime of appreciation and cash flow.

Just my thinking; the best use for me of my HELOC is to buy rentals, rinse and repeat. I've calculated the IRR that includes appreciation, pay down, net cash flow; a batch of my houses in a high appreciation area i earning 60% IRR (modifiec)/yr. Every year. Most of my houses earn around 30-40% total return year after year.

Sure for most occupant home owners with no money in the stock market and cash tight perhaps (just my views mind you) use of their HELOC to have a house they live in paid off sooner makes perfect sense. But to a Kiosoki'esk (Rich Dad) investor my best use of cash is buying income producing appreciating assets in the path of progress.

Thanks for this effort to share how to save a bunch on interest paid. Which yeilds a paid off house much faster.

My views re investment debt: In support of BRRRR I like debt! I want debt! Leveraged houses perform 3x better then the stock market. Paid off rentals perform a bit worse then the stock market. Makes sense to keep 60-80% LTV debt on rentals (to me).

I will add; I'm fortunate enough to invest in a lower cost higher performing rentals state of GA and I do advocate buying at DSCR of >1.5 absolute min and my typical was 1.7 and due to rent appreciation all are over 2.0. Conservative leverage where you have safety margin (>1.7 ish) debt is a good thing. Just my views and thanks again for this explaination of this technique.

-

Property Manager

- Sweetgum Properties

- 678-948-7151

- http://GaREIA.com

- [email protected]

Originally posted by @Curt Smith:Hi Thanks for posting this! I've read much about this tactic some from orgs wanting to coach you. I'm replying not to say anything negative re saving on interest paid but on what just my thinkig is. Possibly also on lost opportunity costs of using ones HELOC to buy a one time gain (interest avoided) vs a lifetime of appreciation and cash flow.

Just my thinking; the best use for me of my HELOC is to buy rentals, rinse and repeat. I've calculated the IRR that includes appreciation, pay down, net cash flow; a batch of my houses in a high appreciation area i earning 60% IRR (modifiec)/yr. Every year. Most of my houses earn around 30-40% total return year after year.

Sure for most occupant home owners with no money in the stock market and cash tight perhaps (just my views mind you) use of their HELOC to have a house they live in paid off sooner makes perfect sense. But to a Kiosoki'esk (Rich Dad) investor my best use of cash is buying income producing appreciating assets in the path of progress.

Thanks for this effort to share how to save a bunch on interest paid. Which yeilds a paid off house much faster.

My views re investment debt: In support of BRRRR I like debt! I want debt! Leveraged houses perform 3x better then the stock market. Paid off rentals perform a bit worse then the stock market. Makes sense to keep 60-80% LTV debt on rentals (to me).

I will add; I'm fortunate enough to invest in a lower cost higher performing rentals state of GA and I do advocate buying at DSCR of >1.5 absolute min and my typical was 1.7 and due to rent appreciation all are over 2.0. Conservative leverage where you have safety margin (>1.7 ish) debt is a good thing. Just my views and thanks again for this explaination of this technique.

Hi, Curt. You're welcome. I appreciate the reply and I can see some value in what you're saying, but the spirit is a little off, I think. This technique is just a better way to pay off your house and keep your checking account working for you, that's it. When you start comparing it to other investment strategies and things (that most people aren't doing, btw), I can understand that, because you're trying to answer the question, "What should a person do with their HELOC and/or extra money?" - but this isn't really an investment strategy.

It'd be like if I told you I have a Groupon for some event Saturday night and asked if you wanted to check it out - the question is, "What are you doing Saturday night?". If you answer that you like Groupon, but you decided not to buy stock in it and that you wanted to start your own company called "Curton" and that events downtown are so expensive because you have to pay for parking and a babysitter when the grandparents are out of town and so on - you're not answering the actual question.

Does that make sense? The question here isn't, "What is the best way to invest your extra money?", it's "Is there a better way to pay off your mortgage and save a bunch of money on interest?". And the answer is Yes.

So, to clarify - I have a couple rentals and I have stocks and an emergency fund, too, but I didn't bring them up, because it was obviously already long-winded and those things are beside the point. The point I'm making is that regardless of any other investments or anything that people have going on, most of them (and probably you) have money that is just sitting in their checking account NOT working full time on saving them interest and paying their houses off - that's a shame to me. I agree that leverage and debt are good to a point, but many people just want a paid off spot to live in and maybe some extra income if it's easy enough (and/or low enough risk) to come by. Those are the people I'm trying to help. Once you start comparing it to a bunch of investment strategies now we're in a very abstract place, you know? I really like the investment style you brought up, but c'mon Curt, if you're going to invest you should use your HELOC to buy the Yankees or Disney World! I mean, THOSE are way better investments than what you're suggesting! Whoa, buddy, you purchased the Yankees and Disney World, but I bought the country of Denmark, so you really blew it, man! Do you see what I mean? There's always a better investment out there, I'm just saying that if you have money sitting in your checking account right now you could be putting it to use and saving a bunch of money simply by changing the way you pay. Or if you need another way to look at it, using some leverage and buying income properties pays off pretty well, you're right. But the mortgage and interest on your residence is all expense / cost - you're not earning any income on it, it's sucking your income away. I mean, isn't that what Kiyosaki says? Your residence in a liability, because it's costing you money and not making you any money? It's been awhile, but that's my takeaway of his message. Buy rentals, yes, but pay off where you live so it's not cutting into your income. This is a way to do that.

- Rental Property Investor

- Clarkston, GA

- 1,906

- Votes |

- 2,039

- Posts

- Rental Property Investor

- Clarkston, GA

Nothing beats buying leveraged rentals! Not even the stock market (as long as the rental leveraged). I also feel the same about residentds. They should be leveraged TOO. The funds used to pay off the residence loan should be used to buy income property. See my DSCR comment a above. A heloc in my view is best used to provide the down payment and rehab funds, rent, REFI, repeat. Fortunately we are all afforded our own opionion. :) Best to you.

-

Property Manager

- Sweetgum Properties

- 678-948-7151

- http://GaREIA.com

- [email protected]

- Lender

- The Woodlands, TX

@Joshua Smith

I’ve thought about how to explain the fallacy of so called “velocity” so that people without advanced degrees in finance can understand it. In previous posts people have used both financial analysis/projections, and point to point critique to try to explain this, but it hasn’t resonated with the true believers. So I’ve decided to simplify.

All the verbiage about amortization schedules, compound interest, eliminating your checking account, etc. is just window dressing made to confuse the issue and distract the “victim”. There are really just three points worthy of consideration

1. By borrowing from a HELOC to pay off principal of a mortgage, you save no money, in fact you actually spend more in interest, because you are saving low mortgage interest by paying higher HELOC interest.

2. Paying all you bills from a HELOC account accomplished nothing. If you're income is more than you spend, you can always use the difference to pay down your mortgage. You don't need a HELOC for this. This is one aspect of the "window dressing" to which I defer.

3. So, eliminating the window dressing which is meant to confuse the issue and deflect attention away from financial analytics, the theory boils down to should you save the interest you pay on the mortgage by paying off principal early. This is no special aha moment. The same question is analyzed every day by millions of businesses, investors, wealth managers, financial analysts, and corporate treasurers world wide. And the answer is that it’s a matter of the decreased risk associated with lower leverage vs. the expected greater return that the funds that would payoff the mortgage principal can generate when used for a different investment. Add risk tolerance of the principal(s) involved, and the answer can be worked out.

Eliminate the nonsense of misconstruing amortization tables, misunderstanding compound interest, and misunderstanding lines of credit (HELOCs) and the above three points should enable you to see the tree in the forest.

Originally posted by @Don Konipol:@Joshua Smith

I’ve thought about how to explain the fallacy of so called “velocity” so that people without advanced degrees in finance can understand it. In previous posts people have used both financial analysis/projections, and point to point critique to try to explain this, but it hasn’t resonated with the true believers. So I’ve decided to simplify.

All the verbiage about amortization schedules, compound interest, eliminating your checking account, etc. is just window dressing made to confuse the issue and distract the “victim”. There are really just three points worthy of consideration

1. By borrowing from a HELOC to pay off principal of a mortgage, you save no money, in fact you actually spend more in interest, because you are saving low mortgage interest by paying higher HELOC interest.

2. Paying all you bills from a HELOC account accomplished nothing. If you're income is more than you spend, you can always use the difference to pay down your mortgage. You don't need a HELOC for this. This is one aspect of the "window dressing" to which I defer.

3. So, eliminating the window dressing which is meant to confuse the issue and deflect attention away from financial analytics, the theory boils down to should you save the interest you pay on the mortgage by paying off principal early. This is no special aha moment. The same question is analyzed every day by millions of businesses, investors, wealth managers, financial analysts, and corporate treasurers world wide. And the answer is that it’s a matter of the decreased risk associated with lower leverage vs. the expected greater return that the funds that would payoff the mortgage principal can generate when used for a different investment. Add risk tolerance of the principal(s) involved, and the answer can be worked out.

Eliminate the nonsense of misconstruing amortization tables, misunderstanding compound interest, and misunderstanding lines of credit (HELOCs) and the above three points should enable you to see the tree in the forest.

Hi, Don. You're right that simple is better, so I just have a couple questions for you if you're game.

1. In case you didn't read my post, I have been able to put around $50,000 extra toward my mortgage using this strategy (in 2 years) without skipping lattes and dinners and so forth. Your contention is that this extra money would have shown up in my checking account over that course of time without this strategy, but BEFORE I was doing this strategy it didn't grow at that rate. Of course, a person's checking fluctuates, but most people have a general level that they hover around - myself and my wife included. How is it possible that we hovered around a $5-$7000 for ten years through a couple other houses and so forth, but the minute I start this strategy all of a sudden my checking is growing at a rate of $25K/year? Of course you'll say that we just happened to get promotions or there was some other mechanism for savings, but that's not the case. If anything, we actually moved to a place where the cost of living is higher and I've been trying to find other ways to save or make extra money, but this is the only change I've made so far. How is this possible?

2. If there was a mortgage product that was the same as whatever you have now (same interest rate and duration, same company, closing costs, etc.) everything EXACTLY THE SAME EXCEPT that it also functioned like a line of credit, ie. you can put all of your income toward it, but still get your money out to pay bills - would you want that or no? Why or why not? You can still invest whenever you want to, you still have a savings account and you can get that to whatever level you want, etc. - everything is exactly the same as it was before, but now you can put all of your income (the money that would typically rest in your checking account) into your mortgage and still get it back out when you need it. Yes / no / why / why not?

- Lender

- The Woodlands, TX

@Joshua Smith

1. To answer this question I would need to do an analysis of your income and expenses for the years in question. Since I don’t have this information how can I possibly answer it?

2. Many people juggle lines of credit to meet current obligations. Let’s simplify it. The amount of money most people carry in their checking account fluctuates, but what’s ever there is called reserves. So, looking at your bank statement, you can find your “average daily balance”.

So instead of keeping this "reserve" you use an overdraft account, or HELOC. You then take the reserve amount and pay off principal of your mortgage. Assuming that you pay exactly the same rate on the mortgage as you do the HELOC, this is the result. The amount you pay in interest on advances in the HELOC, plus the amount you could have earned if the "reserve" had been invested, is equal to the amount you saved on mortgage payments. No magic, simple math.

Now, there are unusual circumstances in which using a HELOC, or any personal loan, to pay down mortgage principal can be financially beneficial. For example you own an investment property that does not qualify for institutional financing, and you're paying 12% interest to a hard money lender. Then borrowing from your HELOC at 4.5% will save a significant amount of interest. But, this has absolutely nothing to do with living out of a line of credit rather than a checking account.

Even not counting the opportunity cost credit given in the analysis for the "reserve" theoretical investment, the additional nickel and dime fees associated with the HELOC will eat up any savings.

Perhaps you became much more vigilant at controlling expenses when you decided to use the HELOC to pay your everyday bills. Perhaps your total expenses have gone done because you didn't have a big bill you had the year before. Perhaps the timing of your payments for major expenses changed. And of course you would need to take the amount of your mortgage at the time you began using the HELOC to pay it down, and compare that with the total of your mortgage balance, your HELOC balance, and subtract the increase in your cash on hand. Then subtract any decrease in expenses from before to after, or add any increase. Then you'll have a better idea of where you stand and what caused the difference, if any. I have found that just being aware of how much you spend on each expense category leads to a better savings rate.

Originally posted by @Don Konipol:@Joshua Smith

1. To answer this question I would need to do an analysis of your income and expenses for the years in question. Since I don’t have this information how can I possibly answer it?

2. Many people juggle lines of credit to meet current obligations. Let’s simplify it. The amount of money most people carry in their checking account fluctuates, but what’s ever there is called reserves. So, looking at your bank statement, you can find your “average daily balance”.

So instead of keeping this "reserve" you use an overdraft account, or HELOC. You then take the reserve amount and pay off principal of your mortgage. Assuming that you pay exactly the same rate on the mortgage as you do the HELOC, this is the result. The amount you pay in interest on advances in the HELOC, plus the amount you could have earned if the "reserve" had been invested, is equal to the amount you saved on mortgage payments. No magic, simple math.

Now, there are unusual circumstances in which using a HELOC, or any personal loan, to pay down mortgage principal can be financially beneficial. For example you own an investment property that does not qualify for institutional financing, and you're paying 12% interest to a hard money lender. Then borrowing from your HELOC at 4.5% will save a significant amount of interest. But, this has absolutely nothing to do with living out of a line of credit rather than a checking account.

Even not counting the opportunity cost credit given in the analysis for the "reserve" theoretical investment, the additional nickel and dime fees associated with the HELOC will eat up any savings.

Perhaps you became much more vigilant at controlling expenses when you decided to use the HELOC to pay your everyday bills. Perhaps your total expenses have gone done because you didn't have a big bill you had the year before. Perhaps the timing of your payments for major expenses changed. And of course you would need to take the amount of your mortgage at the time you began using the HELOC to pay it down, and compare that with the total of your mortgage balance, your HELOC balance, and subtract the increase in your cash on hand. Then subtract any decrease in expenses from before to after, or add any increase. Then you'll have a better idea of where you stand and what caused the difference, if any. I have found that just being aware of how much you spend on each expense category leads to a better savings rate.

Don, I think we have a misunderstanding somewhere or you understand and you're not being honest.

Refer to my second question - would you want this product - yes / no / why / why not? We both know the answer to this - that yes, you would obviously want it and there are some advantages, but I want to understand what you think the advantages are vs what I think they are. If you can't answer this question honestly and simply, then it seems to me you're being dishonest for the sake of your argument and I have no reason to try to come to any understanding with you. Would you want the product described - yes / no / why / why not?

- Lender

- The Woodlands, TX

I think I've had my last conversation with you. You're an insulting ingrate.

Originally posted by @Don Konipol:I think I've had my last conversation with you. You're an insulting ingrate.

Right, because rather than give the actual correct answer and suffer the blow to your ego that you've been doing something wrong for decades, you'd prefer to take a swipe at my ego. Classic!

Anyway, I accept. You can blame it on my "insults" (you know, asking you simple / direct questions) and I'm in the wrong for saying words. You are totally right for not answering my simple questions and then calling me names like a grade school student. Have a good one.

Just a quick update - strategy still going really well. People are missing out bigtime.

Here's a question for anyone who wants to play. If you could have the exact same mortgage you have now EXCEPT that it functioned like a line of credit (ie. you can put all of your income toward it, but then still have access when you need it), would you want that?

Feel free to answer, but it's rhetorical. Obviously, you would want that. If you answer no you're clearly being dishonest. It's simple - your money helps keep your interest costs down while you wait for your bills to come due.

By moving a portion of your mortgage balance to a revolving line of credit (HELOC, etc.) you can accomplish exactly that. All of your income goes toward your mortgage every month and you still have access to it. End of story. Feel free to let me know what you might not understand. <3

@Joshua Smith

For me I am paying the minimum every month on my mortgage as it is very cheap money that I can invest somewhere else to get a better return.

And the fact that you pay more in total interest in the first years is totally normal. You are paying the same rate of interest every year, but the higher the balance, the more the amount of interest.

I want my balance to stay as high as I can as that is money in my pocket that I reinvest. When my balance is going down I can either get a HELOC in second position to recapture the blocked value or do a cash out refi.

So no, velocity banking is not for me. I understand the concept and it may be useful for some people who have difficulty managing their money by giving them a structure, but I do better myself.

Originally posted by @Mike S.:@Joshua Smith

For me I am paying the minimum every month on my mortgage as it is very cheap money that I can invest somewhere else to get a better return.

And the fact that you pay more in total interest in the first years is totally normal. You are paying the same rate of interest every year, but the higher the balance, the more the amount of interest.

I want my balance to stay as high as I can as that is money in my pocket that I reinvest. When my balance is going down I can either get a HELOC in second position to recapture the blocked value or do a cash out refi.

So no, velocity banking is not for me. I understand the concept and it may be useful for some people who have difficulty managing their money by giving them a structure, but I do better myself.

That's cool, but this is what's hard about this subject. No one said anything about investments or savings. I said that it's obvious that every person would want a mortgage that also acts like a line of credit and that's true. It's irrefutable. Any honest, intelligent person can see that there would be benefits to having a set up like that. It doesn't matter what you're doing in terms of investments or savings aside from this. Having a mortgage that functions like a line of credit where your CHECKING ACCOUNT FUNDS can go against your mortgage and then still be used to pay your bills is superior to letting your CHECKING ACCOUNT FUNDS sit around. You can "not want to do it" - great. It's still superior. So, do it or don't do it, but it's better than letting your money sit around, so I'm just getting the word out. Have a good one. :)

Sorry, let me clarify what I'm talking about, because it's unfathomable that a bunch of people who are supposedly into investing and finance can't get this and I feel like I must be explaining it wrong.

Hypothetically, when your income comes in, you put $1000 each into three buckets:

1. Stocks and mutual funds. You pay yourself first through investments.

2. Savings account. You want to buy a rental at some point and you're building up your cash.

3. Checking account. You need to pay your mortgage, car, electric, water, phone, etc.

Now, here's where it gets super tricky, I guess, so I'll try to be as clear and concise as possible:

DON'T TOUCH THE FIRST TWO. KEEP DOING THOSE. DON'T CHANGE THEM.

Now here's the point. The third one. Number 3. The money that's just sitting there all month in your checking account waiting to be used. That money could be helping hold your mortgage balance down and save you money on interest. That's the point of the strategy and it's unequivocally, undeniably, unquestionably ***BETTER*** than just letting it sit there while you wait for bills.

Now you can do what you want with that information. You can do it, not do it, deny it, agree with it, write it out on paper and ball it up and shove it - that's up to you, but it's the truth and there's no way to change it. Putting your disposable income - your "checking account" funds against your mortgage is BETTER than letting it sit there doing nothing for you. That's all I'm trying to help people understand. Hope this clarifies for everybody! Good luck.

"Any honest, intelligent person can see that there would be benefits to

having a set up like that. It doesn't matter what you're doing in terms

of investments or savings aside from this. Having a mortgage that

functions like a line of credit where your CHECKING ACCOUNT FUNDS can go

against your mortgage and then still be used to pay your bills is

superior to letting your CHECKING ACCOUNT FUNDS sit around. You can "not

want to do it" - great. It's still superior."

You're not getting this benefit for free. You're paying a higher interest rate because the bank has factored in their cost of this benefit to you and is charging you accordingly.

Just curious if you know how much you've overpaid your mortgage using this strategy over the years and have run the alternative of just simply using those funds to overpay your mortgage the "normal" way. In theory, you'd be in an ever better financial position as your money would have gone further because the rates would be lower on a conventional loan than on a HELOC.

In the end, I'd suggest paying the minimum on your mortgage and investing what you have left over in an S&P 500 fund (or something of the like). Once the balance is high enough, you can simply write a check for the balance of your mortgage. You'd pay off your house more quickly, have more liquidity along the way, and ultimately end up in a superior financial position.

Interesting strategy and best wishes.

@Joshua S., you wrote: "The question here isn't, 'What is the best way to invest your extra money?', it's 'Is there a better way to pay off your mortgage and save a bunch of money on interest?'", whereas, I reckon the question should always be: "What is the best way to invest your extra money?"

So, those of us who ask the correct question can safely ignore the "velocity" part of trying to pay off our low interest rate mortgage, in favor of putting any extra money we have into buying extra assets that (also) return a higher interest rate / appreciation (just like our primary has already been doing).

HELOCs help us do that, so why are you in hurry to have zero balance owing? That means giving up investing altogether. You get that, right? Cheers...

[Oh, and for those who just like owning their primary free and clear because they're scared to invest their excess income to actually increase their eventual wealth, just give your Lender extra "Principal-only" payments as often as deemed appropriate to the "velocity" you're trying to achieve. Make sure that the receipts you receive verify "Principal-only", so you never pay interest on those amounts from then on].

Originally posted by @Chris John:"Any honest, intelligent person can see that there would be benefits to

having a set up like that. It doesn't matter what you're doing in terms

of investments or savings aside from this. Having a mortgage that

functions like a line of credit where your CHECKING ACCOUNT FUNDS can go

against your mortgage and then still be used to pay your bills is

superior to letting your CHECKING ACCOUNT FUNDS sit around. You can "not

want to do it" - great. It's still superior."You're not getting this benefit for free. You're paying a higher interest rate because the bank has factored in their cost of this benefit to you and is charging you accordingly.

Just curious if you know how much you've overpaid your mortgage using this strategy over the years and have run the alternative of just simply using those funds to overpay your mortgage the "normal" way. In theory, you'd be in an ever better financial position as your money would have gone further because the rates would be lower on a conventional loan than on a HELOC.

In the end, I'd suggest paying the minimum on your mortgage and investing what you have left over in an S&P 500 fund (or something of the like). Once the balance is high enough, you can simply write a check for the balance of your mortgage. You'd pay off your house more quickly, have more liquidity along the way, and ultimately end up in a superior financial position.

Interesting strategy and best wishes.

That's the thing that people can never understand. I don't have $25K/year extra just sitting in my account (see above, that's what I've been able to pay extra over the last two years). If I did, then I WOULD have a choice to make - should I invest these funds or pay my house down faster?

The extra money that's going toward my mortgage IS COMING FROM THE STRATEGY ITSELF, that's what people don't understand. When I pay the mortgage the normal way (and remember, I did this for years, so I know that depending on other bills, I'd have $5-$6K in checking pretty consistently), I'm paying about $20K in interest and taking about 2 years to pay down the first chunk of $10K on the mortgage. It's true, you can go calculate it on your own mortgage, but if it's an average size loan you should get somewhere in that range.

When I move that same $10K over to the HELOC, it costs me about $1000 and 6-8 months to pay down depending on other bills. That difference - $20K vs $1K savings is where the extra money is coming from to pay down my principal. People think it's financial voodoo and don't want to believe it, but it's not. The $10K chunk of my mortgage costs so much to pay down normally, because I'm paying for interest on the whole loan as I do it. Now if I just had an extra $10K lying around in my checking account to pay down the mortgage every six months, then your discussion would be valid - "Why don't you just invest that money in the S&P 500 or pay it directly to principal?" - but I don't. Most people don't. And the extra money people do have is going toward saving and investing and therefore they don't want to put it toward the mortgage, anyway, so it's a circular argument.

Hopefully you and other people can understand this at some point. No one is sitting around with extra tens of thousands of dollars and comparing it to this HELOC strategy. The idea of the strategy is just that's a better, more efficient way to pay off the mortgage WITHOUT having to have a bunch of extra money lying around. In other words, it's a self-defeating argument that makes no sense. It'd be like if I told you I was thinking about buying a hybrid car to save on gas and your counterargument was that I shouldn't do it, because if I had a solar powered jetpack I wouldn't need to pay for gas at all. I would stare at you blankly until you realized how much of a nonsense words you just said and now I wish you would say right or get out of my house.

When I'm talking about using a HELOC to pay the mortgage, the answer isn't - "Well, why don't you just pay your mortgage down with all the extra tens of thousands of dollars you have lying around that you aren't using for something else?". I mean, no offense, but doesn't that sound stupid now? Most people don't have that lying around. But this strategy CREATES EXTRA MONEY THROUGH INTEREST SAVINGS.

The whole misunderstanding people have comes from the fact that they can't understand that moving some of your mortgage balance to the HELOC helps you SKIP interest on the mortgage. You literally skip it completely. If you can't understand that, calculate how much you'll pay in interest for the rest of your mortgage and then imagine you won the lottery and paid off the house tomorrow. Do you have to pay the interest? No, you only pay the interest if you pay it back on their schedule. If you pay it back early, you skip it and it's not owed, period. This works whether you pay off the house tomorrow or pay a few thousand dollars extra to principal. If you don't believe that, calculate how much interest you owe today, then imagine you won the lottery but it would only pay off half of the house. How much interest do you owe now? Regardless of how you work it out, when you pay extra toward your mortgage, you are literally skipping the corresponding interest payments that were scheduled for that portion of the balance. It's not magic, it's just something people don't know or don't understand or something.

All I'm telling you is that using the HELOC accomplishes the same thing without having the money lying around. You skip over the $20K interest on the mortgage and pay around $1000 interest to the HELOC over 6-8 months and then you do it again. And meanwhile, all of your extra checking funds are going toward the mortgage, too, so that saves you more money on top of what I just described. There's no smoke and mirrors or anything. Paying principal back early LITERALLY LETS YOU SKIP TENS OF THOUSANDS OF DOLLARS IN INTEREST. That works whether you get a gift from your dad and owe him $10 in interest, borrow it from the HELOC and owe a $1000 in interest, or you have it lying around. The difference is that yeah, if dad hands you $10K or you have it lying around you might put it in a mutual fund, but if you take it out of the HELOC and do that, now you're going into additional debt to invest, which can be irresponsible and dangerous. But when you move a chunk of your mortgage balance onto the HELOC you're in the same amount of debt, you're just paying a lot less interest on one portion, so there's no danger.

Anyway, hope this clarifies, I just think it's a shame that people can't understand this. They want to turn it into the jetpack argument instead of understanding that the extra money in the system comes from HOW you pay the debt off, so there's no way or reason to compare it to "just taking your extra money and investing it".

Originally posted by @Brent Coombs:@Joshua S., you wrote: "The question here isn't, 'What is the best way to invest your extra money?', it's 'Is there a better way to pay off your mortgage and save a bunch of money on interest?'", whereas, I reckon the question should always be: "What is the best way to invest your extra money?"

So, those of us who ask the correct question can safely ignore the "velocity" part of trying to pay off our low interest rate mortgage, in favor of putting any extra money we have into buying extra assets that (also) return a higher interest rate / appreciation (just like our primary has already been doing).

HELOCs help us do that, so why are you in hurry to have zero balance owing? That means giving up investing altogether. You get that, right? Cheers...

[Oh, and for those who just like owning their primary free and clear because they're scared to invest their excess income to actually increase their eventual wealth, just give your Lender extra "Principal-only" payments as often as deemed appropriate to the "velocity" you're trying to achieve. Make sure that the receipts you receive verify "Principal-only", so you never pay interest on those amounts from then on].

Brent, I just covered this in my response to Chris John, so please read that for clarification. The money in question is coming from the interest savings, it's not money that's lying around. That's why the question is incorrect. You're asking, "What's the best way to invest money that I don't have, because I haven't saved it yet?". It just makes no sense. In other words, moving a portion of your mortgage to the HELOC is something anyone can do whether they are scraping the bottom of their checking account every month or have a few thousand extra lying around. What I'm asking you to imagine is the person who is scraping. That person can use this strategy to save money on interest without having extra money just lying around. Once you grasp that it's not about the extra money a person has, you'll understand the strategy.

Originally posted by @Joshua S.:When I'm talking about using a HELOC to pay the mortgage, the answer isn't - "Well, why don't you just pay your mortgage down with all the extra tens of thousands of dollars you have lying around that you aren't using for something else?". I mean, no offense, but doesn't that sound stupid now? Most people don't have that lying around. But this strategy CREATES EXTRA MONEY THROUGH INTEREST SAVINGS.

You are saving interest if your HELOC interest is lower than your mortgage interest. If the HELOC interest is higher you are not saving money at all, you are paying more interest.

The only point of velocity banking is that instead of keeping some money idling in your bank account for a few days or week, you put everything back into the HELOC and use it as a bank account to withdraw money when you need it. Indeed the compounding effect of never having anything idling in your bank account can be powerful. However, be mindful that line of credit can be shut down or frozen by the bank for any reason. If you lose your job, get into a financial problem that your bank learn about, bank will cut you off your HELOC lifeline in a snap and you will not have anything left to recover as all your money will be stuck into your home principal. You still need to have a minimum cushion into your bank and/or savings account for these situations.

As I wrote earlier, velocity banking is a system that can be helpful for people who don't know how to manage their money and are prone to overspend. It will give them a frame on how to it. If you are budget conscious and keep track of your expenses, it will not add any value and can even be riskier and more expensive as the rate arbitrage between HELOC and mortgage is not in your favor.

Originally posted by @Mike S.:Originally posted by @Joshua S.:When I'm talking about using a HELOC to pay the mortgage, the answer isn't - "Well, why don't you just pay your mortgage down with all the extra tens of thousands of dollars you have lying around that you aren't using for something else?". I mean, no offense, but doesn't that sound stupid now? Most people don't have that lying around. But this strategy CREATES EXTRA MONEY THROUGH INTEREST SAVINGS.

You are saving interest if your HELOC interest is lower than your mortgage interest. If the HELOC interest is higher you are not saving money at all, you are paying more interest.

The only point of velocity banking is that instead of keeping some money idling in your bank account for a few days or week, you put everything back into the HELOC and use it as a bank account to withdraw money when you need it. Indeed the compounding effect of never having anything idling in your bank account can be powerful. However, be mindful that line of credit can be shut down or frozen by the bank for any reason. If you lose your job, get into a financial problem that your bank learn about, bank will cut you off your HELOC lifeline in a snap and you will not have anything left to recover as all your money will be stuck into your home principal. You still need to have a minimum cushion into your bank and/or savings account for these situations.

As I wrote earlier, velocity banking is a system that can be helpful for people who don't know how to manage their money and are prone to overspend. It will give them a frame on how to it. If you are budget conscious and keep track of your expenses, it will not add any value and can even be riskier and more expensive as the rate arbitrage between HELOC and mortgage is not in your favor.

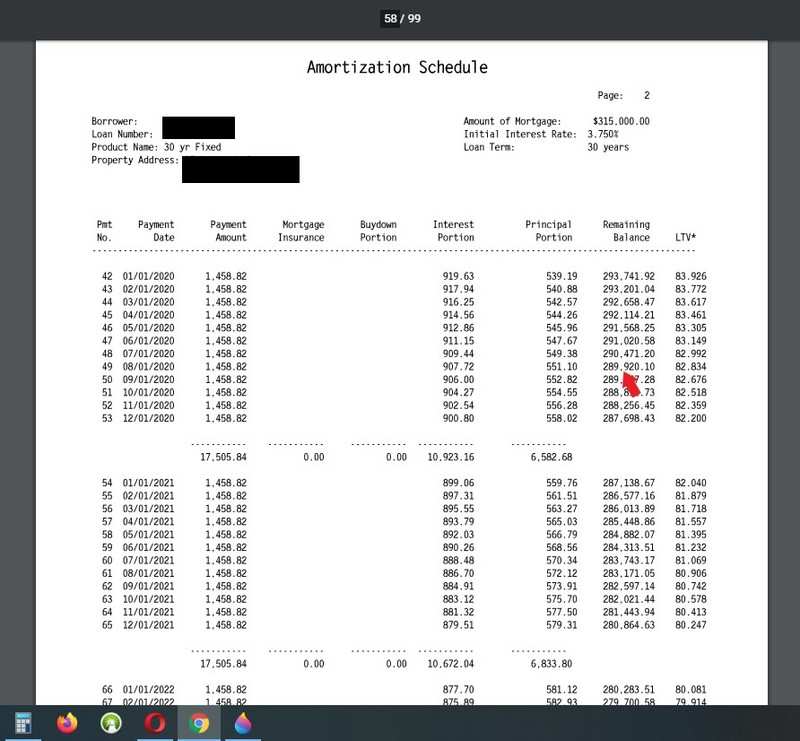

Sorry, but I don't know how to make it any clearer, so maybe pictures will help. :) As you can see from my amortization schedule as of January I should be at a balance of $287K and as you can see from my corresponding statement I'm at a balance of $229K. That's a difference of about $58K (and I have more to put on there soon, but I have been waiting to see what will happen with my taxes). We bought the house in the summer of 2016, started the strategy in May of 2018. I guess you have to take me on my word that I haven't had $20K extra per year for these last 3 years lying around to put on the mortgage, but it's the truth and.... you know.... pretty believable. If you notice, I'm paying almost $200 less in interest per month ($700 vs $900) than I should be according to my amortization schedule. That's not magic. Since I'm paying them back early using the HELOC my principal / interest ratio is skewing in my favor. A couple more years and I'll be at the tipping point where I'm paying more to principal each month and then I'll REALLY take off. Normally it would take about 13 years to get to that point and I'm not skipping lattes or anything, it's just a more efficient way to pay.

The whole thing has nothing to do with arbitrage or rates. If someone handed you $50K tomorrow and you put it on your mortgage, you skip down to that point in your amortization table on your next payment. That means that all of the corresponding interest that you would have paid (ie. for all those months you skipped), you saved that amount on interest. Again, that's the same whether you use a HELOC to do it or lottery winnings or whatever. I'm giving my mortgage lender the money early, so I'm skipping the corresponding interest payments ($917.94 + $916.25 + $914.56, etc. in that middle column there), which saves me tens of thousands of dollars. The whole thing "costs" me about about $1000/year in interest on the HELOC and I actually have a crappy rate as you can see below. The "cost" of my $1K in HELOC interest is obviously covered by my savings, so net net I come out way ahead. If you find yourself struggling with this idea, just do it yourself. Go to this bankrate calculator and plug in your numbers and add in an extra $20K principal payment for your first year and see how much you'd save on interest. When I put the $20K in the interest jumps down about $40K. Now ask yourself if paying $1000 to get that savings would be worth it. You ever pay extra to insulate your house better so you can save on heating costs or anything? Same idea. Once again, NOT doing any scrimping and saving or doing any voodoo, it's just the effect of skipping over interest payments they can't charge you for, because you gave the money back early. Hope this helps.

https://www.bankrate.com/calcu...

Originally posted by @Joshua S.:

Let's make it clear.

The difference between a $100k or $90k balance in your mortgage principal is $10k.

If your mortgage rate is 3% with a balance of $100k you will pay $3k of interest that year. If you had only $90k balance you would pay $2.7k of interest. The difference is $300. $300 is also 3% of 10k.

Now if you use your HELOC to get this $10k, but your HELOC is 4%. You will pay $400 interest in your HELOC to pay your mortgage down and save $300 in interest. So yes it is negative arbitrage. But because you are still paying the same payment each month to your mortgage, you will pay your principal down a little bit more because the portion of interest vs principal has changed. But that additional amount is not magically appearing, it is just a shift from one pocket to the other. You are forcing yourself to save more because not only you are paying the same mortgage payment as before, but now in addition you are paying the interest of the HELOC on top of it. That is what is making the difference and eventually pays your principal down (with the penalty of the negative arbitrage).

Instead of paying that $400 HELOC interest, you would have used that additional money to add to your mortgage payment, you would get a better result eventually.

Many gurus are trying to explain that because you are paying more

interest in the first years of your mortgage it is at the bank's

advantage. It is not. You are paying the same exact rate of interest

each year based on your outstanding balance. If I could find a 30 years

mortgage at 2.75% interest only, I would jump on it as I don't mind not

paying any principal back at all as the equity in the home is frozen

money that I can't use unless I am doing a cash out refi or getting a

second position HELOC.

I repeat that for people who have problem managing money, velocity banking is a good script to follow to keep them in check. But if you are financially savvy, you may loose money due to negative arbitrage, and it can put you in a dangerous situation if your bank freeze your HELOC has you would have less reserve available.

Originally posted by @Mike S.:Originally posted by @Joshua S.:Let's make it clear.

The difference between a $100k or $90k balance in your mortgage principal is $10k.

If your mortgage rate is 3% with a balance of $100k you will pay $3k of interest that year. If you had only $90k balance you would pay $2.7k of interest. The difference is $300. $300 is also 3% of 10k.

Now if you use your HELOC to get this $10k, but your HELOC is 4%. You will pay $400 interest in your HELOC to pay your mortgage down and save $300 in interest. So yes it is negative arbitrage. But because you are still paying the same payment each month to your mortgage, you will pay your principal down a little bit more because the portion of interest vs principal has changed. But that additional amount is not magically appearing, it is just a shift from one pocket to the other. You are forcing yourself to save more because not only you are paying the same mortgage payment as before, but now in addition you are paying the interest of the HELOC on top of it. That is what is making the difference and eventually pays your principal down (with the penalty of the negative arbitrage).Instead of paying that $400 HELOC interest, you would have used that additional money to add to your mortgage payment, you would get a better result eventually.

Many gurus are trying to explain that because you are paying more

interest in the first years of your mortgage it is at the bank's

advantage. It is not. You are paying the same exact rate of interest

each year based on your outstanding balance. If I could find a 30 years

mortgage at 2.75% interest only, I would jump on it as I don't mind not

paying any principal back at all as the equity in the home is frozen

money that I can't use unless I am doing a cash out refi or getting a

second position HELOC.

I repeat that for people who have problem managing money, velocity banking is a good script to follow to keep them in check. But if you are financially savvy, you may loose money due to negative arbitrage, and it can put you in a dangerous situation if your bank freeze your HELOC has you would have less reserve available.

Yes, I understand how the math works out, but this will make it even simpler.

When I put in an additional principal payment of $10K into your example, it shows just under $13K in interest savings. That's if I do nothing else, but since I'm making the same payments either way, that's also $13K that will go toward my principal faster than before, which accelerates the pay down faster and so on. You can think of it like a snowball effect.

You're saying that because I pay around $1000/year ($83/month) to run the strategy, that cancels out my $13K savings?

Originally posted by @Mike S.:Originally posted by @Joshua S.:Let's make it clear.

The difference between a $100k or $90k balance in your mortgage principal is $10k.

If your mortgage rate is 3% with a balance of $100k you will pay $3k of interest that year. If you had only $90k balance you would pay $2.7k of interest. The difference is $300. $300 is also 3% of 10k.

Now if you use your HELOC to get this $10k, but your HELOC is 4%. You will pay $400 interest in your HELOC to pay your mortgage down and save $300 in interest. So yes it is negative arbitrage. But because you are still paying the same payment each month to your mortgage, you will pay your principal down a little bit more because the portion of interest vs principal has changed. But that additional amount is not magically appearing, it is just a shift from one pocket to the other. You are forcing yourself to save more because not only you are paying the same mortgage payment as before, but now in addition you are paying the interest of the HELOC on top of it. That is what is making the difference and eventually pays your principal down (with the penalty of the negative arbitrage).Instead of paying that $400 HELOC interest, you would have used that additional money to add to your mortgage payment, you would get a better result eventually.

Many gurus are trying to explain that because you are paying more

interest in the first years of your mortgage it is at the bank's

advantage. It is not. You are paying the same exact rate of interest

each year based on your outstanding balance. If I could find a 30 years

mortgage at 2.75% interest only, I would jump on it as I don't mind not

paying any principal back at all as the equity in the home is frozen

money that I can't use unless I am doing a cash out refi or getting a

second position HELOC.

I repeat that for people who have problem managing money, velocity banking is a good script to follow to keep them in check. But if you are financially savvy, you may loose money due to negative arbitrage, and it can put you in a dangerous situation if your bank freeze your HELOC has you would have less reserve available.

Well, maybe you're done talking now, but hopefully you get it. I think the problem is that people think the $10K is just costing them "3%". The thing is, you're also paying interest on the entire loan balance, so it's costing you way more time and money that that. If you look at the amo table in your example you see that it takes 54 months (almost 5 years!) to pay the $10K down by the bank's schedule and that costs you an average of $238/month for a total of $13K.

In other words, you're paying off that $10K around Sept of 2025 after paying $13K worth of interest charges to get there, which is 130% interest when you look at your actual cost. I can pay off the $10K in between 6-10 months for less than $1000 on my HELOC. The difference is that I'm skipping over those amortized interest payments by giving the bank's money back sooner, so I'm annihilating. Every month I'm putting all my cash flow against that $10K to bring it down asap. Again, yeah, if you have $10K extra lying around every year then you could get similar results, but you might as well wish for a pony. Most people don't have the money lying around, which is why we're hacking and thinking outside the box in the first place.

"I mean, no offense, but doesn't that sound stupid now? Most people don't have that lying around. But this strategy CREATES EXTRA MONEY THROUGH INTEREST SAVINGS.

The whole misunderstanding people have comes from the fact that they can't understand that moving some of your mortgage balance to the HELOC helps you SKIP interest on the mortgage."

The same argument could be made to you. Have your paycheck direct deposited into a mutual fund so it gets to work immediately. Pay your bills out of the mutual fund. 11% average in the mutual fund > saving 3% interest on your mortgage. When you have enough money in your mutual fund, pay off your loan. It'll happen a helluva lot faster than velocity banking. Also, liquidity. However, when you can do that, you won't. Why? You'll realize how much faster your money grows at 11%. You'll borrow what equity you do have in your house and invest it.

It's just as easy (if not easier) to open a mutual fund than a HELOC. Also, in both examples, you don't need 10k to make a decision with.

I mean, no offense, but doesn't YOUR argument sound stupid now? By the way, your attitude and the way you communicate with people is something to behold.

PS. I think I might set that up with my mutual fund, so thanks for the idea!

Originally posted by @Joshua S.:

Let me present it in another way as obviously I didn't make my message clear.

Let's put the following scenario:

$100k mortgage, 3%, amortized over 30 years. (monthly payment: $421.60)

HELOC, $10k, 4%

Case 1:

Normal amortization of the mortgage without any additional principal payment and no use of the HELOC.

At the end of year 1 your mortgage principal will be down to $97,912 and you would have paid during the year $5,059.25 consisting of $2,087 of principal and $2971 of interest.

| payment | principal | interest | balance | ||

| 1 | ($171.60) | ($250.00) | $99,828.40 | ||

| 2 | ($172.03) | ($249.57) | $99,656.36 | ||

| 3 | ($172.46) | ($249.14) | $99,483.90 | ||

| 4 | ($172.89) | ($248.71) | $99,311.01 | ||

| 5 | ($173.33) | ($248.28) | $99,137.68 | ||

| 6 | ($173.76) | ($247.84) | $98,963.92 | ||

| 7 | ($174.19) | ($247.41) | $98,789.72 | ||

| 8 | ($174.63) | ($246.97) | $98,615.10 | ||

| 9 | ($175.07) | ($246.54) | $98,440.03 | ||

| 10 | ($175.50) | ($246.10) | $98,264.52 | ||

| 11 | ($175.94) | ($245.66) | $98,088.58 | ||

| 12 | ($176.38) | ($245.22) | $97,912.20 | ||

| ($2,087.80) | ($2,971.45) | ($5,059.25) |

Case 2:

Your scenario, taking a 10k HELOC loan, that will be payed back in one year. The HELOC is used to pay the balance down of the mortgage to 90k.

With this scenario, the balance of the mortgage at the end of the year will be $87,608 and you would have payed $2,391 +10,000 of principal and only $2,667 of interest.

However at the same time, you would have paid back $10,000 of principal of your HELOC and $216 of interest.

So, out of pocket you would have to pay $15,275 that year.

| mortgage | HELOC | ||||||||

| payment | principal | interest | balance | principal | interest | balance | |||

| 1 | ($196.60) | ($225.00) | $89,803.40 | ($833.33) | ($33.33) | $9,166.67 | |||

| 2 | ($197.09) | ($224.51) | $89,606.31 | ($833.33) | ($30.56) | $8,333.33 | |||

| 3 | ($197.58) | ($224.02) | $89,408.72 | ($833.33) | ($27.78) | $7,500.00 | |||

| 4 | ($198.08) | ($223.52) | $89,210.65 | ($833.33) | ($25.00) | $6,666.67 | |||

| 5 | ($198.57) | ($223.03) | $89,012.07 | ($833.33) | ($22.22) | $5,833.33 | |||

| 6 | ($199.07) | ($222.53) | $88,813.00 | ($833.33) | ($19.44) | $5,000.00 | |||

| 7 | ($199.57) | ($222.03) | $88,613.44 | ($833.33) | ($16.67) | $4,166.67 | |||

| 8 | ($200.07) | ($221.53) | $88,413.37 | ($833.33) | ($13.89) | $3,333.33 | |||

| 9 | ($200.57) | ($221.03) | $88,212.80 | ($833.33) | ($11.11) | $2,500.00 | |||

| 10 | ($201.07) | ($220.53) | $88,011.73 | ($833.33) | ($8.33) | $1,666.67 | |||

| 11 | ($201.57) | ($220.03) | $87,810.16 | ($833.33) | ($5.56) | $833.33 | |||

| 12 | ($202.07) | ($219.53) | $87,608.09 | ($833.33) | ($2.78) | $0.00 | |||

| ($2,391.91) | ($2,667.29) | ($10,000.00) | ($216.67) | ($15,275.87) |

Case 3:

Instead of using the HELOC, you use the same $15,275 than in scenario 2, but you use it spread over 12 months to make additional payment to your mortgage.

At the end of the year you mortgage balance will be $87,555. Better than in case 2.

| payment | principal | interest | balance | |

| 1 | ($1,022.89) | ($250.00) | $98,977.11 | |

| 2 | ($1,025.45) | ($247.44) | $97,951.66 | |

| 3 | ($1,028.01) | ($244.88) | $96,923.65 | |

| 4 | ($1,030.58) | ($242.31) | $95,893.07 | |

| 5 | ($1,033.16) | ($239.73) | $94,859.91 | |

| 6 | ($1,035.74) | ($237.15) | $93,824.17 | |

| 7 | ($1,038.33) | ($234.56) | $92,785.84 | |

| 8 | ($1,040.93) | ($231.96) | $91,744.92 | |

| 9 | ($1,043.53) | ($229.36) | $90,701.39 | |

| 10 | ($1,046.14) | ($226.75) | $89,655.25 | |

| 11 | ($1,048.75) | ($224.14) | $88,606.50 | |

| 12 | ($1,051.37) | ($221.52) | $87,555.13 | |

| ($12,444.87) | ($2,829.81) | ($15,274.68) |

Originally posted by @Chris John:

"I mean, no offense, but doesn't that sound stupid now? Most people don't have that lying around. But this strategy CREATES EXTRA MONEY THROUGH INTEREST SAVINGS.

The whole misunderstanding people have comes from the fact that they can't understand that moving some of your mortgage balance to the HELOC helps you SKIP interest on the mortgage."

The same argument could be made to you. Have your paycheck direct deposited into a mutual fund so it gets to work immediately. Pay your bills out of the mutual fund. 11% average in the mutual fund > saving 3% interest on your mortgage. When you have enough money in your mutual fund, pay off your loan. It'll happen a helluva lot faster than velocity banking. Also, liquidity. However, when you can do that, you won't. Why? You'll realize how much faster your money grows at 11%. You'll borrow what equity you do have in your house and invest it.

It's just as easy (if not easier) to open a mutual fund than a HELOC. Also, in both examples, you don't need 10k to make a decision with.

I mean, no offense, but doesn't YOUR argument sound stupid now? By the way, your attitude and the way you communicate with people is something to behold.

PS. I think I might set that up with my mutual fund, so thanks for the idea!

Good luck with that. At some point you'll find out that you can't live in a mutual fund which is a pretty funny thought, so I hope you do it. You and the wife still paying on the house in 25 years calling your broker to see if you can retire and move into the mutual fund. Ah, I slay me! Anyway, once again, it's not about where to invest your money for a 3% or an 11% return. You think that's the discussion, but it's not. As I illustrated to the other gentleman - using his example of a $100K loan at 3%, you actually pay $13K worth of interest as you pay down your initial $10K. That's 130% interest when you work out your ACTUAL cost. Not per year, obviously, but it takes just under 5 years and you pay 130% interest in total to pay down that $10K if you do it on the bank's schedule.

So, since you guys are all about investments and that's the only thing you are willing to compare this to, let's do it! When you put that $10K into your mutual fund you'll end up with $16,850 (your initial $10K + $6850) after 5 years at 11%. Not bad - a 68.5% total return over that time. Let's see how I did.

When I put the $10K into my mortgage I end up with $23K (my initial $10K + $13K interest savings). So, I ended up with that 130% return I talked about. That's obviously almost double your return, but that's not all:

1. I leveraged debt in the HELOC to make this happen and you were using your paychecks, which is obviously less efficient. Notice I didn't TAKE ON MORE DEBT, I simply moved debt from one vehicle to another and leveraged a different payment method to get my savings.

2. You have to hope for 11% and my return is automatic and locked in, because it's savings on interest that's already scheduled. Obviously, the risk might be worth it if you were getting a better return, but I already showed that you didn't.

3. Your money had to work for 5 years to make that return happen and my money immediately saved me the $13K when I skipped over those payments on my mortgage. And over the next 5 years - because I'm making the same regular monthly payments either way, that $13K that I saved on interest is now going toward my principal earlier than it would have, which saves me even more money.

4. The money I'm paying to my mortgage was going there, anyway, so I'm really not even making an investment, I'm just changing the timing of my payments. So, you took on risk to get your returns and I didn't but still had a greater return. In other words, my "returns" are really just $13K worth of free money for flipping a couple switches and paying in a different way. You can't beat that no matter what your return is, because you're using capital and taking on risk. PS - I'm totally liquid, btw. I have a HELOC, so when I want money out of my house I just take it out.

Anyway, sorry if I hurt your feelings or anything, but it's a bit annoying to try to help people and have them bash you and refuse to listen, so I get a little carried away sometimes. It's astounding, the closed-mindedness that people exhibit, especially on an "Innovative Strategies" forum, so it gets a little frustrating, but I'm sorry if I was rude or anything. You can just chalk it up to passion, I don't mean it personally against you. To answer your question, though, no my argument doesn't sound stupid at all. There are probably benefits or aspects of the strategy that I haven't even thought of yet and buying a mutual fund is so basic that it's hard to believe I'm comparing the two. I'm honestly only doing it, because people refuse to see this strategy for what it really is, but when you compare it to a typical investment it actually makes me feel guilty about how much better it is. I think that's why I speak out about it so much, I feel a kid with his hand in the cookie jar and I'm trying to share the wealth or whatever. You should take a look at the screen shots I posted if you haven't already - I've put an extra $58K on my mortgage over the last three years doing this and there's no way you could put that amount toward a mutual fund. According to the bankrate calculator I posted earlier that $58K extra toward my $315K loan, it's saving me around $100K in interest, which is hard to believe. Anyway, good luck with the mutual fund if you go that way. :)