Personal Finance

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated over 2 years ago on .

What are High Net Worth Individuals And Why They Continue to Buy

According to Forbes, the U.S. has the most High Net Worth Individuals in the world. A High Net Worth Individual (HNWI) is generally accepted as person who has $1,000,000 or more in liquid assets. A liquid asset is money held in brokerage and/or bank accounts. Examples of a non-liquid assets are, collectibles, NFTs, outstanding loan balance on primary residents, durable goods, etc.

Calculating net worth is rather simple. Net Worth = Assets – Liabilities.

Examples of labilities are outstanding loans on a car and/or home, student debt, credit card debt, etc. If the difference between your assets and liabilities is $1m or more in the green then you are a HNWI.

Along with a substantial amount of liquid assets a HNWI also receives a number of perks such as concierge level treatment from financial advisors, reduced rates based on the size of ones account, tickets to entertainment events, and even investment opportunities that are not available to the common client. An example of this would be an offering from Morgan Stanley. Recently Morgan Stanley announced they were offering select HNWI an opportunity to invest in 1 of 3 different Bitcoin funds, but made only available to HNWI.

Now that we have explained what a HNWI is, let’s dig into some of the benefits all home owners can utilize when purchasing property, but can be extremely powerful for a HNWI in particular.

Some of the greatest benefits of owning a home are the tax incentives. When an individual or family files their tax returns the IRS will give the individual or family an option to choose either a) standard deduction or b) itemized deduction. These deductions will lower your income. You or your accountant will decide if you should file using the standard deduction or itemized deduction.

Typically you or your accountant will decide what deduction option will save you more in taxes.

The standard deduction are the following:

- $12,550 for single filers

- $12,550 for married couples filing separately

- $18,800 for heads of households

- $25,100 for married couples filing jointly

Cost that can be used for itemized deductions:

- Real estate taxes

- Personal property taxes

- Mortgage interest

- Student loan interest

- Gifts to charity

- Possibly medical and dental expenses

The mortgage interest deduction is a tax incentive for homeowners. This itemized deduction allows homeowners to count interest they pay on a loan related to purchasing, building, or making improvements to their primary home against their taxable income.

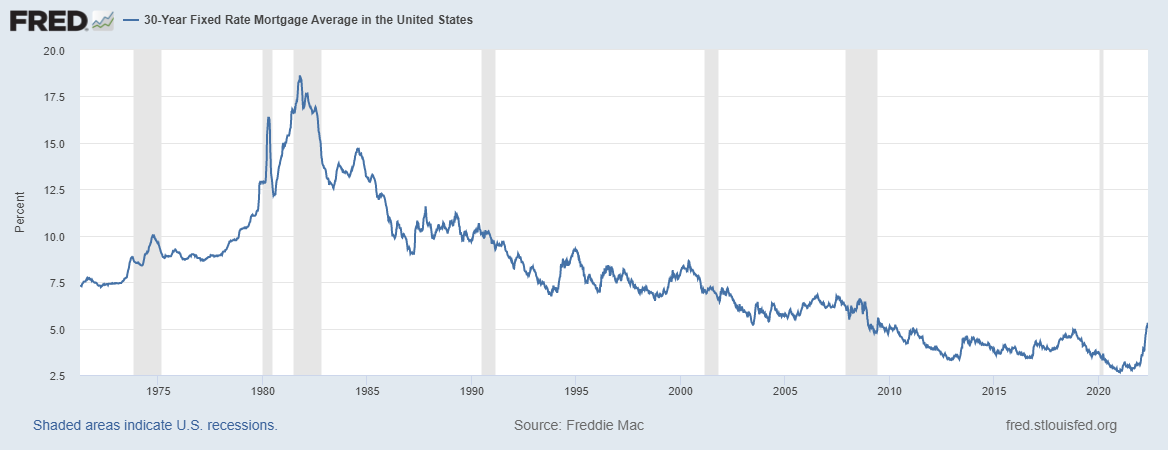

The reason why higher net worth individuals will continue you buy, and take out a mortgage, is because even with higher rates the mortgage interest can be used to lower their income. Even in today’s “elevated” interest rate environment (5.5% 30 year fixed at the time of writing this blog) it is still rather “cheap” to borrow money, historically speaking. Over the last few years it hasn’t been uncommon for people to finance their purchase even if they have enough cash available to buy outright. One reason for this is what we just discussed, the ability to lower their income via mortgage interest. Another reason is to use that cash to roll into another investment vehicle such as equities, bonds, crypto, NFT’s, art, etc.

For example:

Single Borrower:

400,000 Loan Amount

3.00% Interest Rate

First Year of Interest: $11,885.79

- this individual may decide to use the standard deduction because they would leave $664.21 in unclaimed deductions if they choose to itemized her/her deductions.

Single Borrower:

400,000 Loan Amount

5.50% Interest Rate

First Year of Interest: $21,865.51

- this individual may decide to use the itemized deduction because they would leave $9,315.51 by choosing the standard deduction.

This is not tax advice and I am not a tax accountant

HNWI’s can utilize a jumbo loan in their favor as well. While you do not need to be a HNWI to access this loan, the more money you put down the better rate you can obtain and that is especially important given the size of the loan.

When the loan amount is above $647,200 this is considered a jumbo loan. You can still put a low down payment of 3%, 5%, 10%. But if you put 15% to 20% down payment you could obtain lower interest rates or lower cost scenario.

To obtain a better interest rate or loan scenario with a jumbo loan amount you will need to meet a higher standard of qualifying. For example credit scores above 750, credit history, 12 months in reserves (funds left over in case of a financial emergency), lower debt to income ratios.

If you can meet the higher standard of qualifying you might be eligible for a 15% down no mortgage insurance scenario.

As you already knew there are many benefits to being classified as a High Net Worth Individual but the reason that you are seeing them continue to invest in real estate are, tax benefits, stable growth in value, equity, savings, hedge against inflation, and stability over the long term. These reason are why you are continuing to see HNWI purchase property while many are deciding to sit on the side lines as we wait to see what mortgage rates and the US economy do moving forward.

Special thanks to:

William Mitchell IV

Closing Purchase Transactions in 11 Days

VP Mortgage Advisor