Tax, SDIRAs & Cost Segregation

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated 6 months ago on . Most recent reply

- Specialist

- West Palm Beach, FL

- 1,484

- Votes |

- 4,367

- Posts

Cost Segregation on Office Building

- Specialist

- West Palm Beach, FL

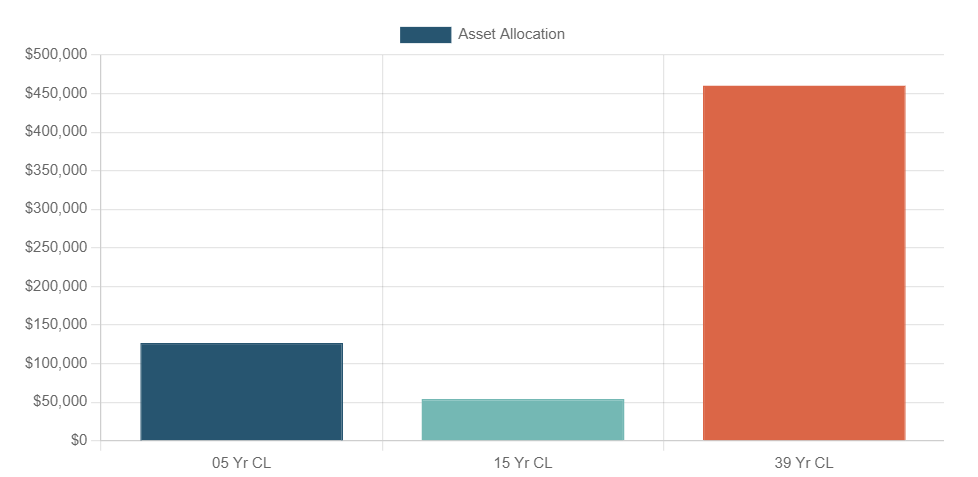

A Cost Segregation Study was performed on a 2-story, 5,237 square foot Office Building located in Louisville, KY that was built in 1946 and purchased by its new owners in 2021. The depreciable basis of the property was $641,100. After the cost segregation study was performed, this was the new asset allocation breakdown by useful life.

Here are some examples of what types of assets are included in each of these asset classes.

5 Year Useful Life

- Specialized equipment

- Cabinets and counters

- Refrigerators and microwaves

- Security alarm systems and telephone connections

- Decorative wall treatments, ceiling fans and flooring

15 Year Useful Life

- Sidewalks, landscaping and asphalt paving

- Signage and site lighting

39 Year Useful Life

- Doors, walls, roofing and windows

- Flooring, drywall partitions and ceilings

- Emergency lighting and restroom fixtures

- Plumbing, HVAC, and electrical distribution

The use of the accelerated depreciation strategy helps real estate investors to reduce the tax liability immediately which therefore increases their bottom line due to the offsetting of income. An additional benefit of a detailed engineering-based Cost Segregation Study is that it can increase potential insurance premium savings as well as provide support for the property tax appeals process. Additionally, it can help maximize renovations and improvements.

A Cost Segregation study is an IRS approved federal income tax tool that increases near term cash flow by utilizing shorter recovery periods for depreciation to accelerate return on investment. For newly constructed, purchased or renovated properties and also retroactive generally over the last 10 years, building components are properly classified into individual units of property and accurate recovery periods for computing depreciation deductions. The study identifies with forensic engineering detail the immediate Bonus Depreciation 5, 7 and 15-year personal property class lives qualifying portions of a building that are normally buried in 27.5 year residential or 39 year commercial categories.

The Cost Segregation Study was performed on the Asset Depreciation Range (ADR) and is based on a 40% tax bracket for State and Federal Taxes. The financial benefits of a cost segregation study are realized through using increased cash flow to scale your business or strengthen your portfolio which is done by maximizing the net present value through deferring tax payments.

As a reminder, bonus depreciation started to phase out in 2023. It’s 100% bonus depreciation for properties placed into service in 2017-2022, 80% in 2023, 60% in 2024, 40% in 2025, 20% in 2026 and completely phased out in 2027.

For additional questions, checkout this article on Cost Segregation FAQs.