General Real Estate Investing

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated 11 months ago,

- Real Estate Broker

- Greater Charlotte NC and Charleston, SC areas

- 54

- Votes |

- 96

- Posts

Nationwide Housing Stats - And What's Expected Going Forward With Interes Rates?

Re-Posted by Kristen Haynes, New Home Buyers Brokers/Realty Pros- from Talking Points – ‘Rebuild’ by Scott Brixen February 9, 2024

Friday, February 9, 2024

Want to learn more about it first? Read this detailed blog post.

https://medium.com/p/ef0480228574

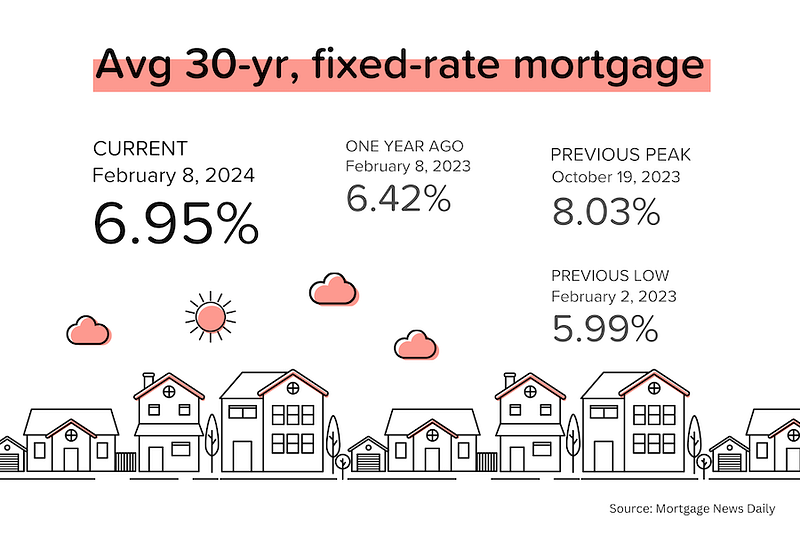

While it’s disappointing to see average mortgage rates back near 7%, the rate cuts will come eventually, and the increase in the national inventory of homes available for sale is encouraging. Let’s just pray that lower rates arrive in time for the spring selling season!

Housing sentiment improves, sort of. Fannie Mae’s Home Purchase Sentiment Index for January 2024 climbed 3.5 points to 70.7, the highest figure since March 2022. Yet, 83% of respondents still thought it was a “bad time to buy.” The improvement came elsewhere, with 82% feeling secure in their jobs, and a survey high 36% expecting mortgage rates to fall in the next 12 months. So perhaps a “good time to buy” later? [Fannie Mae]

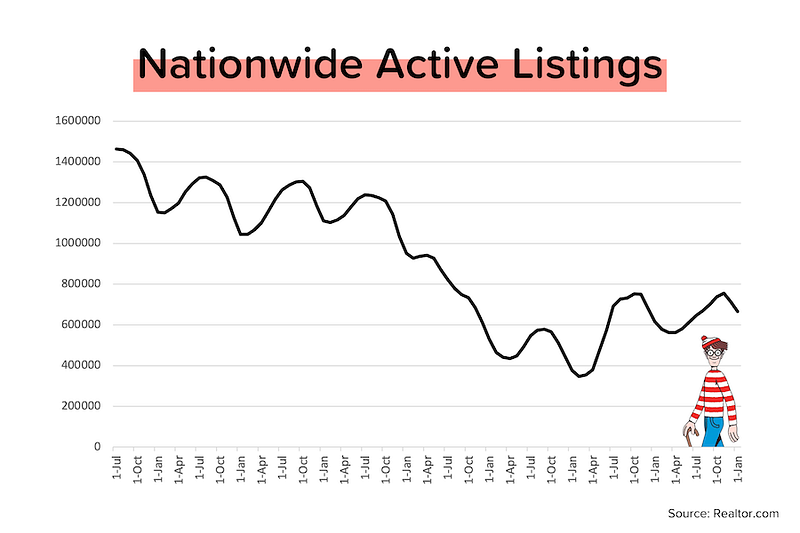

A stealthy rebuild. The Realtor.com data for January 2024 showed that the active inventory of homes for sale rose 8% year-over-year to 665,000. Struggling to see that in the graph below? Just find Waldo. Normally, inventory levels begin to contract in Sept/Oct. But in 2023, that didn’t happen until December. Net result: inventory levels have been slowly expanding. [Realtor.com] More on this later.

A recovery in refis ahead? The ICE Home Price Index (formerly Black Knight) saw home prices rise 5.6% YoY in December 2023, up from +5.1% YoY in November 2023. The report also suggested that refinancings could come storming back if mortgage rates move towards 6%. How? All those millions of people that bought homes in 2023 only wanted to “date the [high] rate” they ended up with. [ICE]

All about appreciation. The Wall Street Journal/Realtor.com Emerging Markets Index attempts to identify the best cities to buy a home (or investment property) in. For Winter 2024, more affordable Midwestern and Northeastern markets dominated the Top 20 list, with Ohio alone taking 5 slots. Despite having a median listing price of $1.8 million, Santa Barbara was selected as the #1 market. [WSJ/Realtor.com]

How we gonna pay this month’s rent? Half of US renters are “cost burdened,” meaning that they spend more than 30% of their income on housing (rent + utilities). And 27% of renters spend more than 50% of their income on housing! [Joint Center for Housing Studies]

Mortgage rates are back near 7%. We’re close, so close to rate cuts, but Jerome Powell and his fellow Fed members won’t admit that publicly. Instead, they keep talking about needing “confidence” that inflation will reach their 2% target, when it is already there if you annualize recent monthly data. As a result of Fed members talking tough, and the strong January jobs figure, the market no longer expects a rate cut on March 20. [Mortgage News Daily, CME]

A closer look at active inventoryOver the last three months, we’ve seen year-over-year growth in new listings for the first time in what feels like forever. Active inventory (this excludes pending sales) was up 8% year-over-year in January 2024. More listings = more options for buyers & more transactions.

I don’t want to get too excited. After all, national active inventory is still 30% below where it was pre-pandemic. But then again, it wasn’t that long ago that it was 50% below pre-pandemic levels! Things are definitely improving, albeit slowly. Ultimately, we need mortgage rates to move down to improve both affordability (lower monthly payments) and availability (‘freeing up’ previously ‘locked in’ sellers).

Drilling down to the city level

The inventory situation is very different from city to city, and that’s driving divergent pricing trends. So we dove into Realtor.com’s residential listing database to look at the metro-level data.

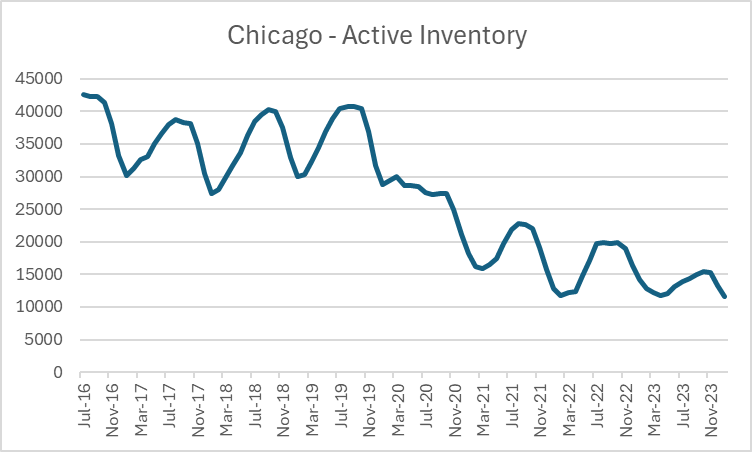

- 43 of the Top 100 cities by population saw active inventory decline YoY in January 2024. The largest drops were in Las Vegas (-42%), Boise (-36%), Stockton (-25%), Bridgeport (-24%), San Jose (-19%), Chicago (-18%), Raleigh (-17%), and Phoenix (-15%).

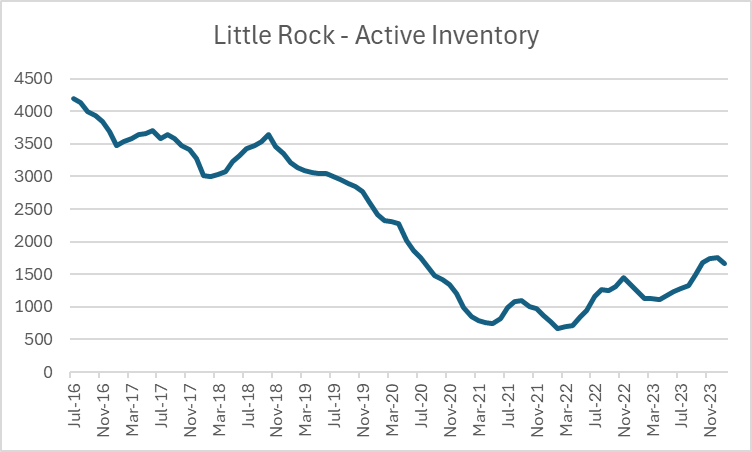

- 57 of the Top 100 saw active inventory rise YoY in January 2024. The biggest gains were seen in Little Rock (+36%), Deltona (+35%), Knoxville (+31%), Memphis (+29%), New Orleans (+28%), Miami (+25%), San Antonio (+24%), El Paso (+23%), Columbia (+22%), Omaha (+22%), and Tampa (+20%).

Just look at Las Vegas. In 2022, inventory shot up to above pre-pandemic levels, and prices fell for 10 straight months. But inventory has since come crashing down, and price growth has been on the order of +1% per month since July 2023. Quite a turnaround.

Chicago wasn’t exactly hot during the pandemic, but together with cities like Detroit and Cleveland, it sure is today. In fact, Chicago’s active inventory just set a new 7-year low! Can you guess which direction prices are going in Chicago? Up around 8% in 2023.

Realtor.com Residential Listing Database

Realtor.com Residential Listing Database

Realtor.com Residential Listing Database

Realtor.com Residential Listing Database

On the other side, let’s look at Little Rock. Inventory plunged 80% (!!!) between 2018 and 2021, but is now in recovery, likely because of: 1) higher prices dampening sales, and 2) a supply response from builders. Memphis, meanwhile, saw inventory drop 66% between 2019 and 2021, but it has recently recovered to pre-pandemic levels.

Realtor.com Residential Listing Database

Realtor.com Residential Listing Database

Realtor.com Residential Listing Database

Realtor.com Residential Listing Database

If you’d like me to send you a chart for your city, just send me an email. [email protected]

Mortgage MarketIt’s hard to believe that six weeks ago, average 30-yr mortgage rates were near 6.5%. Since then, Jerome Powell has “walked back” some of his more emotive comments, and the January jobs report was almost unbelievably strong. So here we are, back near 7%.

The next Fed rate decision is on March 20. The Fed Funds futures market is currently pricing in an 83% probability that the Fed will do nothing, and a 17% chance of a 25 bps cut. For the meeting on May 1, the probability of another “no cut” is now 40%.

They Said It

They Said It

“Basically, we want to see more good data. It’s not that the data aren’t good enough. It’s that there’s really six months of data. We just want to see more good data along those lines. It doesn’t need to be better than what we’ve seen, or even as good. It just needs to be good. And so, we do expect to see that. And that’s why almost every single person on the Federal Open Market Committee believes that it will be appropriate for us to reduce interest rates this year.” — Jerome Powell, Federal Reserve Chairman, during his “60 Minutes” interview.

“Over the last couple of quarters, the number of open jobs in construction is rising again — that’s a forward signal that suggests hiring is continuing and what’s happening, particularly in the homebuilding sector, is an expectation that single-family home buildings are going to expand in 2024. Builders are looking down the road and saying, ‘OK, we’ve got to have our workers in place.’” — Robert Dietz, NAHB’s Chief Economist

From Kristen: Fingers crossed that the Fed will 'reverse course' in either March or April, and give us a 'gift' of lowered interest rates to help fuel the spring real estate market! We're almost there- the spring market has already 'sprung', and we are starting to see more inventory come into the market- so make sure to keep a close eye on your home searches going forward from February into spring!

- Kristen Haynes