Reprinted and shared with permission

By Michael Catarevas October 23, 2024 Reading Time: 4 mins read

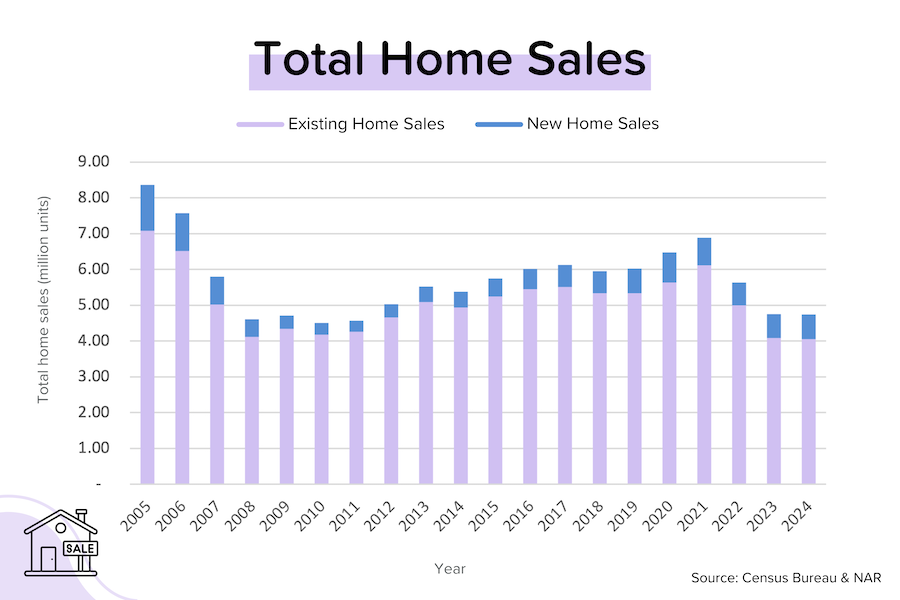

In September, total existing-home sales—completed transactions that include single-family homes, townhomes, condominiums and co-ops—receded 1% from August to a seasonally adjusted annual rate of 3.84 million. Year-over-year, sales waned 3.5% (down from 3.98 million in September 2023).

Existing-home sales dropped to a 14-year low, likely as prospective buyers held out for lower mortgage rates, with house prices remaining elevated. Sales fell month-over-month and year-over-year in the South, Midwest, and Northeast, while sales in the West grew.

According to National Association of REALTORS® (NAR) Chief Economist Lawrence Yun, "Home sales have been essentially stuck at around a 4-million-unit pace for the past 12 months, but factors usually associated with higher home sales are developing. There are more inventory choices for consumers, lower mortgage rates than a year ago and continued job additions to the economy. Perhaps, some consumers are hesitating about moving forward with a major expenditure like purchasing a home before the upcoming election."

Total housing inventory registered at the end of September was 1.39 million units, up 1.5% from August and 23% from one year ago (1.13 million). Unsold inventory sits at a 4.3-month supply at the current sales pace, up from 4.2 months in August and 3.4 months in September 2023.

“More inventory is certainly good news for homebuyers as it gives consumers more properties to view before making a decision,” Yun said. “However, the inventory of distressed properties is minimal because the mortgage delinquency rate remains very low. Distressed property sales accounted for only 2% of all transactions in September.”

The median existing-home price for all housing types in September was $404,500, up 3% from one year ago ($392,700). All four U.S. regions registered price increases.

“Moderating home price increases are welcome news for homebuyers,” Yun added. “With wage growth now outpacing home price appreciation, housing affordability will improve.”

Bright MLS Chief Economist Lisa Sturtevant had these thoughts:

"While mortgage rates have increased in recent weeks, rates are generally expected to fall through the end of the year. At the same time, the number of new listings coming on to the market is expected to continue to increase. At the end of September, NAR reported that total active inventory was up by 23% compared to a year ago. More inventory and lower rates should translate into more home-buying and -selling activity in the fourth quarter. Overall, therefore, the fourth quarter should be a busy time for the U.S. housing market, and total home sales for the year should edge up above the 2023 level.

“What are the downside risks to the performance of the housing market in Q4? Affordability is still a real challenge. Even with lower mortgage rates, some prospective homebuyers are still going to be priced out.

“If inflation takes a turn and mortgage rates do not come down, home sales could be lower. If the economy weakens significantly, there could also be a slowdown in homebuyer demand. However, neither of those prospects seems very likely.

“Political uncertainty, however, is a possibility and could also cool housing market activity. This fall, some buyers and sellers will be holding back, waiting for the outcome of the presidential election. A disruptive process could lead to higher mortgage rates, more anxiety among consumers, and a stuttering housing market this winter.”

According to the monthly REALTORS® Confidence Index, properties typically remained on the market for 28 days in September, up from 26 days in August and 21 days in September 2023.

First-time buyers were responsible for 26% of sales in September—matching the all-time low from August 2024 and November 2021—and down from 27% in September 2023.

All-cash sales accounted for 30% of transactions in September, up from 26% in August and 29% in September 2023.

Individual investors or second-home buyers, who make up many cash sales, purchased 16% of homes in September, down from 19% in August and 18% in September 2023. Distressed sales—foreclosures and short sales—represented 2% of sales in September, virtually unchanged from last month and the previous year.

Realtor.com® Chief Economist Danielle Hale added that “economic growth is a plus for housing demand, but higher mortgage rates in an era where current homeowners see record-high equity and a large majority have a cost of funds substantially below today’s market rate have created a conundrum for the housing market.

“Far fewer people are buying and selling homes. In a unique twist, because supply has generally been constrained alongside buyer demand, the housing market remains surprisingly resilient with rising prices and competitiveness indicators like down payment amounts softening only slightly from recent highs. As home prices remain high, builders have leaned into the opportunity to add much needed home inventory, with starts up among single-family and moderate-density two- to four-unit multifamily homes. This could help to make headway against the intractable decade-long housing shortage, but more is needed, which is why housing has become such a focal point among voters and politicians in this year’s election cycle.”

And this from CoreLogic Chief Economist Selma Hepp:

“Home sales activity in September got a boost from a sharp decline in mortgage rates during August, which considerably improved buyer sentiment and sent pending sales soaring. While the surge in activity illustrates pent-up demand waiting for rates to drop, volatility has once again reared its ugly head with a more recent jump in rates. Nevertheless, while that means slower home sales activity once again, buyers continue to show interest and readiness to step off the sidelines once mortgage rates ease up.”

Thoughts from Kristen: "Hopefully, the Feds continue with their likely rate cuts in November and January. Buyers are waiting on the fence to see if rates significantly drop, and others are concerned about the election and fallout afterwards in the markets. So, as expected, this looks to be a slow winter. If the stars aligh, we may have a feeding frenzy in the fall- and builders are getting ready to capitalize on it! I expect to see more housing starts with new construction last quarter 2024 and again in 1st quarter 2025. Stay tuned!"

Tags: Danielle HaleExisting HomesExisting-Home SalesHome Saleshousing market dataLawrence YunLisa SturtevantMLSNewsFeedNARReal Estate DataReal Estate Sales