Buying & Selling Real Estate

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated over 4 years ago on . Most recent reply

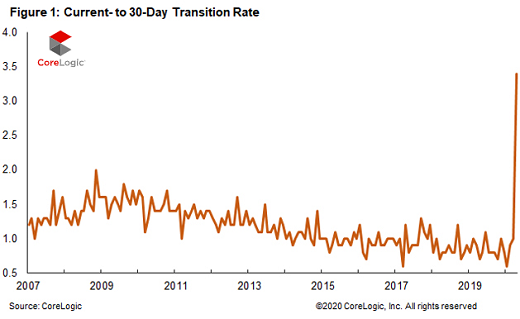

Delinquent FHA Mortgages Soar By Record 60% To All Time High

This is NOT news I wanted to hear, but it is what it is . . . That is a Nasty uptick.

Delinquent FHA Mortgages Soar By Record 60% To All Time HighAs a reminder, "mortgages that are in forbearance and have not missed a payment before going into forbearance don’t count as delinquent. They’re reported as “current.” And 8.2% of all mortgages in the US, some 4.1 million loans, are currently in forbearance according to the Mortgage Bankers Association. But if they did not miss a payment before entering forbearance, they don’t count in the suddenly spiking delinquency data."

Everything changed in April when there was a sudden onslaught of delinquencies according to CoreLogic, which came after 27 months in a row of declining delinquency rates. These delinquency rates move in stages – and the early stages are now getting hit, with the Transition from “Current” to 30-days past due suddenly soaring.

According to Bloomberg, New Jersey had the highest FHA delinquency rate, at 20%.

Most Popular Reply

Originally posted by @Jason Wray:

John, Luckily FHA has an extenuating circumstance rule that allows for a borrower to still purchase or refinance if they show the late payments, forbearance, modification was due to unforeseen circumstances. Not only that but when you modify a mortgage your still going to see a reduction in Fico scores due to the lesser of the payment reporting. Generally the scores will improve after 12 months of payment or once the modification is completed. I also can tell you that some of that data is also reporting the Covid-19 Cares data.

Those reports are using algorithms that do not have perfect data and will include additional trade lines that are are distressed but being forgiven. None the less these are government insured loans where the buyers pay a ridiculous amounts of UFMIP up front Mortgage insurance premiums and MIP monthly insurance premiums. The values are also very lean due to the AMC appraisals being so strict with comps and active listings. So for once instead of relying on the market to self regulate, Dodd Frank has ensured regulations to reduce the overall losses...

Only thing that may come out of this would be that it opens up more inventory for distressed sales and more rental opportunities for investors.

Lol, I think you are missing the point. We are talking mortgages here, not credit card or auto loan debt and not FICO scores or how to fix your credit. ;-)

"Good mortgage underwriting" is extending loans ONLY to people who "have the ability" AND the "willingness" to repay.

Whichever one it is, one of those is missing now and that brings down the whole system. It's simple monetary physics and a matter of time. In a healthy economy, most people pay their mortgage. This is obviously not a healthy economy with no relief in sight.

It's kind of like, "I like living in a house, instead of on the street, therefore I will pay my mortgage". If that many people can't or won't (whichever it is really doesn't matter) then it's time to change your real estate investing strategy because we are no longer in a normal market.