Updated over 5 years ago on . Most recent reply

Hard money loan example

I'm looking to understand hard-money loans better and I'm hoping to get some help from the BP community.

Are most hard-money loans interest only?

For an interest-only loan, to calculate the cost, does the following look correct:

Principal = $100,000

APR = 10%

Loan duration = 4 months

Total cost = (($100,000 x 0.1)/12) x 4 = $3,333.33

And assuming that is correct (please let me know if it's not), how do you calculate non-interest-only loan costs? Is it amortized over the course of a set term? Or is it amortized at a longer term with a balloon payment after 1 year (or some other term)?

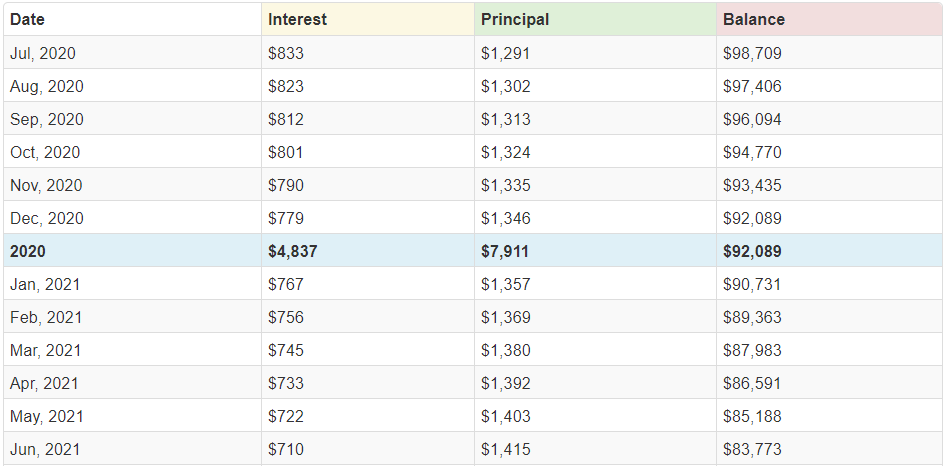

Example A:

Principal = $100,000

APR = 10%

Amortization term = 5 years

Balloon payment = due after 1 year

So on July 1st 2021 the remaining $83,773 is due?

Example B:

Principal = $100,000

APR = 10%

Term = 1 year

Are either of these examples correct, and if not, can you help me understand better?

Thanks in advance!

I'm looking to understand hard-money loans better and I'm hoping to get some help from the BP community.

Are most hard-money loans interest only?

For an interest-only loan, to calculate the cost, does the following look correct:

Principal = $100,000

APR = 10%

Loan duration = 4 months

Total cost = (($100,000 x 0.1)/12) x 4 = $3,333.33

And assuming that is correct (please let me know if it's not), how do you calculate non-interest-only loan costs? Is it amortized over the course of a set term? Or is it amortized at a longer term with a balloon payment after 1 year?

Most Popular Reply

Hard money loans very dramatically and how they're structured. What I typically see is some kind of origination fee such as one to three points and then some interest only payment with the maximum holding time between six and 12 months.

For example with your $100,000 loan what I think is most likely as you would see something like two points and 12% interest

Which means that you would pay $2,000 (two points or two percent of loan) at origination. This might mean that you pay interest on $102,000 or it might mean that you received $98,000 but pay interest on $100,000.

The second part of your question is how to calculate an interest only payment and you did that part correctly. At 10%, your payment would be $833.33 per month. Some hard money lenders would require you to pay that $833 each month. Some would allow it to accumulate and be paid at the end of the holding period.

hopefully this helps clarify