All Forum Posts by: Oleksandr Tereshchuk

Oleksandr Tereshchuk has started 5 posts and replied 7 times.

Post: Who would buy a house with a swimming pool?

Post: Who would buy a house with a swimming pool?

- Toronto

- Posts 8

- Votes 1

Hello Comrades,

Pool business is currently booming. I try to understand what kind of person would buy a house with a swimming pool.

Please share your thoughts and insights on whom those buyers are and where they congregate. The age, income, interests, social media accounts they might follow.

Where, on your opinion, can I find those folks?

Looking forward to hearing your thoughts!

Cheers,

Alex

Post: London Cretive REI Meet-Up June 17,2020 (Tentative due to covid)

- Toronto

- Posts 8

- Votes 1

Great! I'll be there

Post: What it might take to build up to a passive $5,000 a month?

- Toronto

- Posts 8

- Votes 1

What Will it Take to Create Such Passive Stream of Income?

So you want to be financially free you say? Ok cool. I want to be an astronaut. There is a gap between what I want and what I have. I am about to make you feel uncomfortable by asking straight questions and telling you the things you don’t want to hear.To begin with – you are currently not “financially” free. Just because you say you want to be free, I assume that you are currently not.

“No-no. I am free. I just want to have more freedom” – I hear you say.

Alright, let’s define freedom. Merriam-Webster Thesaurus gives two definitions of freedom:

According to the first definition, freedom is a state of being. Also, it assumes that there was some sort of power or another person who was trying to control the one. Question: is the controlling force necessary for being or becoming free? If not, then definition should be the following: freedom is a state of being. Much shorter and simpler, isn’t it?

The second definition states that freedom is the right. Alright, what is the “right”? Google defines it as justified, acceptable, true, or correct as a fact.

My next question is: who is the one that justifies and defines what is acceptable, true, and correct? Who has the authority to extend you the right to be free? I don’t know anyone authorized to grant the right to be free. However, I know that the judicial system claims to have the right to limit or take away your freedom by putting you in jail or restricting you from doing certain things and being in certain places. So if there is no-one to ask for freedom, do we get it by default, at birth? Or maybe we need to obtain it somehow, somewhere? It’s confusing and neither of two definitions brought clarity into explaining what freedom is. Maybe other sources have better explanations.

Roget’s 21st Century Thesaurus says that freedom is the license to do as one wants and defines the following as the synonyms for it:

So freedom is a license. To be free, I need a license. Again, who is authorized to issue the license to be free? Does anyone know what it looks like? What are the requirements for obtaining one? Does it have an expiry day? How much does it cost? Again, the more I ask, the more questions I get? Let’s move on. Maybe if we try from the opposite end of the spectrum, we will be able to get to the truth.

What is the opposite of freedom? Below are the antonyms for freedom, according to Roget’s 21st Century Thesaurus:

Dependence and captivity… According to this definition, freedom is some sort of independence from some external force or power. Therefore to be free means to be in a state of independence. Let’s leave it as is and not dig deeper because I feel it’s a rabbit hole that has no end to it. Independence.

Impotence, inability, weakness…? This is ridiculous. Are there better ways to describe the lack of freedom? Let’s ask Google, he knows everything:

Financial Independence

Financial Independence

Every person has his magic number that will change everything and unlock the way to a beautiful, stress-free, happy life. Ha-ha… Anyways, let’s say you need about $5,000 /month to live comfortably, cover all your expenses. You strive to create a passive stream of income of $5,000 /month that will require little to no work from you. The money will simply land on your bank account while you lay on a couch and repost on Instagram the quotes about successful success. With this money, you don’t worry about where the next paycheck will come from. You think you outsmarted the entire world around you and the sky is not a limit for you. You figured it all out and now you can manage your time only as you decide to. No bosses, nowhere to go, nothing to do, only unless you decide otherwise. That’s cool? Sure it does.

You heard a lot of “success stories” in which people obtained that financial freedom or financial independence I should say, by investing in real estate. People often start their stories remembering the times, when they busted their asses at work, trying to squeeze as much cash as possible from their full-time jobs. Then savvy folks would pour all their savings into the rental properties for the monthly cash flow. By cashflow I mean the income you have left, after the mortgage, taxes, and other operating expenses. You hear a lot of stories like that and it seems that real investment is a way to go. You will need to build a portfolio of rental properties, which generates your passive income. Now you see the path. Pull up the pants, wipe your runny nose, grab the diet Coke – we are going to get FINANCIALLY FREE.

How much time do you think it will take you to set everything up? What did successful stories tell you about the timelines? Let’s see what it takes to build the stream of income that will generate you $5,000 /month.

Let’s say you are an educated, hard-working middle-class citizen, who annually makes approximately $100K. Day in, day out from 8 to 5 you grind your way to success working the full-time job. Your life is simple, you don’t overspend and have pretty good financial behaviors that allow you to set some money aside. You saved quite a bit and you are ready to step on the real estate investing path. You are about to buy your first property and already feel like a complete success. Life is great and easy, you figured things out. Everything goes as planned. Few months of house hunting and you finally bought your dream house. A bit of renovation, marketing and you have the tenants moved in. The house brings you about $500 a month of hustle-free cash flow. You feel on top of the world, you nailed it. Indeed, that’s great cash flow. To become financially free you only have left $4,500 /month. No problems, just repeat what you’ve done 9 more times and you can retire. The only problem is that you are out of cash after your first purchase. It’s hard to buy a property without a downpayment. Let’s do some napkin math to see how much time it will take to buy 9 more houses and get your freedom license.

If you are fortunate to live in Canada, please pay 27% taxes on your annual income. Taxes are a whole nother topic, which deserves separate attention. However, stay on the track, we are not getting into taxes here. Deduct the basic expenses from your annual income. They are different for every person (I don’t include the stacks of toilet paper you purchased during COVID-19 pandemic. Let’s keep it as your little secret). Deducting :

- Food (one person)

- Entertainment (movies, 1-2 nights out, nothing crazy, really conservative)

- Pet (a small dog shares miserable existence next to you)

- Commute ($7-10 /day)

- Car insurance payments

- Rent (So cheap because you try to save money and live in a ********. It also includes utilities)

- Travel (Once a year you fly out to a warm country. You work hard, you deserve it (sarcasm))

You don’t buy new clothes, toys, electronics, gadgets. A new iPhone is just a dream you can’t afford. No Christmas or birthday presents to yourself. Cancel Netflix and Spotify subscriptions. No kombucha or Starbuck coffees. No cab rides. You don’t pay for that cute chick at the bar, sorry honey. No new books or journal subscriptions. You don’t get sick. No dental treatment, no out of pocket medical expenses. You live a monk’s life, literally. From 8 to 5, day in – day out. You have a goal and you are committed to achieving it no matter what it takes. You’ve decided that you want to be free and this is the way to get that freedom. The napkin math showed you clearly – 10 houses – $5,000 /month.

A year later you saved $40,000. You look a little tired, but that doesn’t matter. Well done boy! Now let’s put this money to work and buy a second house. You’ve found a beautiful property listed for little over $300K and your *** got lit on fire. You expect to add another $500 to your monthly cash flow. $1,000 a month, doing little to nothing. No kidding, sounds great, let’s pull the trigger on it. A typical down payment is 20%, which equals $60,000 on a $300K house. What a bummer, you can’t buy it, because you have only $40K saved. You will need to work another six months to make up the difference. You realize that it takes approximately a year and a half to put aside enough money to buy a $300,000 property. Don’t forget that you will need to live the monk’s life and say no to anything that you can’t eat. How long do you think it will take to save up enough cash for ten of those $300k properties? Do you think you will still want that freedom by the time you reach it? By the way, how long do you expect to occupy this planet? Silence…

Ha-ha! Exactly! Don’t freak out yet… Such variables, like appreciation rate and investment income, will make things look slightly better. Let’s add them to the equation.

According to Remax: “Healthy price increases are expected next year, with the estimating a 3.7 per-cent increase in the average residential sale price.” According to the Royal LePage Market Survey Forecast: “The aggregate price of a home in Canada is forecast to rise 3.2 percent year-over-year to $669,800 in 2020”. This is a conservative number and it greatly varies, depending on the area of your purchase. We will use it for our financial projections. The number of 3.7% means that the house you purchased for $300,000, next year should increase in price for about $11,100. Will put appreciation to the side for now and run the numbers only including the rental income.

I assume you are being a good boy and don’t touch the monthly $500 you get from your rental property. You are not selling the house, therefore we don’t account for appreciation and use only the money you saved from the monthly cash flow. Annually the rental generates you $4,380 ($6,000 minus 26.8% tax deductions). This extra cash will save you about 3 months of hard work at your full-time job. You will need to hassle for 16.2 months (70.4 weeks) to save $60,000 of a down payment on your second house. (It’s almost 2 months faster having the cash flow of $500 /month from the first property).

One year and a little over 4 months, since you’ve become the landlord, you pull the trigger on the second property. Now, you are the happy owner of two properties which generate you (hopefully) $730 / month ($1,000 /month minus taxes) on top of your annual savings of $40,000. You continue living on the edge of starvation for another year and six weeks to save enough money to purchase your third house. Same deal, $300,000 purchase price, $60k downpayment. Rental income from the two houses you already own allows you to set aside $60,000 a little bit faster. To be exact, 2.7 months faster since the purchase of your first house. Great job, you’ve got the third house. All three properties bring you $13,140 in cash flow annually which correlates to $1,095 /month. It’s been a while since you stepped on this RE journey. Let’s do a quick check-in. How do you feel living the way you did? Because you were able to save $40k every year, I assume life has been very steady for you. No emergencies, no unexpected expenses. You didn’t get sick, nor met a loved one. No kids were born and your parents stayed healthy and well. All your tenants paid on time. No convictions. The vacancy rate is down to zero. No maintenance expenses, whatsoever. What a stress-free life! By the way, how long did it take you to come to this point, where you build such a passive income stream of “whopping” $1,095 /months?

2nd Home = 16.2 months

3rd Home = 14.8 months

Time Spent = 31 months = 2 years 7 months

For the past 2 years and 7 months, you lived like a monk. Skinny, tired, but determined to make it work. $5k /months is your dream and nothing can stop you. Great! I like the persistence with which you dig yourself into the grave. Now, please sit down for a second and answer the following questions:

- With three behind your belt, how many more houses will it take to get you to your goal?

- How long will it take to obtain those properties if you continue down this path?

Let’s run some numbers:

- It will take 9 houses to generate almost $40,000 /year of income after paying taxes.

- The yellow line down indicates the point at which your rental properties generate you $5,110 a month. This will happen 12 years later when you rent out 14 houses.

Just think about it, it will take you somewhere about 12 years of living like a monk, busting your *** day in – day out at the full-time job to finally get to the point where you can quit. How realistic is it to maintain such a lifestyle? Is it worth it? Are you ready to pursue this for 12 years? What are your thoughts?

Numbers above don’t include a lot of important things, such as:

- Renovation/Maintenance Expenses. Houses break, the roof will leak, AC will break, the basement will get flooded. None of those unexpected experiences were included;

- Evictions. Tenants don’t always pay rent and you will have to deal with courts, late payments, and evictions. Rooms stay unoccupied – rent doesn’t get paid;

- Life Situations. People want new clothes, people want ice cream from time to time. People get married, get sick, and die. People make babies. People divorce. People lose jobs, people find better jobs. None of those were included in calculations. Not a single calculator in the world can predict and account for the life situations that WILL happen to you;

- Property management fees. It will be hard to manage 14 houses without some sort of property management assistance. Especially if you are working at your full-time job. Especially if you want to make this income as passive as possible. As a baseline, expect to pay a typical residential property management firm between 8 – 12% of the monthly rental value of the property, plus expenses. Some companies may charge, say, $100 per month flat rate. 10% on your monthly rental income of $5,110 is $511. That’s an extra house for a second… Now you will need 15properties to keep you afloat;

- House appreciation. Typically, over the years, your house will be worth more than you paid for it. This extra value can be refinanced and put towards the purchase of the next home. It can be a huge help and dramatically speed up the process at which you get to your goal. It is really hard to predict how much the property will cost over time and the further you shoot, the more off you will be;

Over 12 years, you have saved and re-invested $840,000 worth of down payments (14 houses x $60,000) to buy 14 homes. Let’s see how well your investments paid off.

Capitalization Rate

Cap rate is the crucial piece of information that investors use to make their decision. You need to know for two main reasons:

- Analyze the performance, or expected performance, of your rental properties. For example, if there are three houses in your price range for sale, calculating the expected cap rates for all three can help you determine which is the best investment.

- Determine your property’s fair market value (FMV). This is important if you're selling a property. If you know how your property's net operating income and the industry average cap rate, you can determine your property's fair market value. Market value = net operating income / cap rate.

Cap Rate is the ratio of the property’s net income to its purchase price (or current market value). While the purchase price remains the same, the market value of the house raises year over year and gives more accurate calculations. $500 /month of cash flow results in a cap rate of 7.3%. What’s a good cap rate, you might ask? On the right are the averages according to CBRE’s North America cap rate survey for the first half of 2019. 7.3% is a good investment. Also since we included mortgage repayment into these calculations it can be considered a cash-on-cash return. Mortgage repayment is the variable that differentiates the two.

Inflation, The Rule of 72, and Home Appreciation

In light of recent, or I should say current events surrounding the COVID-19 pandemic we begin seeing the combination of inflation and low mortgage rates. What does it mean to real estate investors like us? High compounded rates of home appreciation. As a tenant or a typical consumer – you lose, because increasing rates of inflation are not very helpful for your consumer purchasing power of basic goods and services like food, utilities, gas or transportation prices. However, if you own the property, you should smile, because the best traditional hedge against inflation is, was, and probably always will be – the Real Estate. This is true because home values tend to increase at least as much as the reported annual rates of inflation. Let’s play around with numbers and calculate how soon your investments will double in value. We will use The Rule of 72. The use of it is very simple: you divide the number 72 by an estimate of annual appreciation gains. A home that appreciates at 10% per year (72 divided by 10 = 7.2 years) may double in value every 7.2 years. Another home that appreciates 7% each year can double in price every 10.2 years during a relatively strong economic period. Or, as in our case, home appreciating at 3.5% per year is quite likely to double in value every 20.6 years. However the rule of 72 is not 100% precise, it gives a glance at the real estate market condition.

As the house owner, you should also be familiar with Compound Interest. It refers to the idea that when you earn interest on an investment, that earned interest is rolled back into the investment and starts to build on itself. Let’s look at an example on the left. We know that the average annual appreciation rate on your house in Ontario, Canada is 3.5%. Therefore we assume that your $300k house appreciates by 3.5% at the end of the first year of ownership. You just made $10,500 out of nowhere it’s put into your home’s value. The next year you’re earning 3.5% on the new property value of $310,500. At the end of the following year, you’ll earn $10,868, which is $368 more from the previous. Your earning has gone up, even though you haven’t done anything more than just leave the money in place. If you have enough patience and allow the power of compound interest to do its magic, the house you bought for $300k will double in value in about 21 years.

Inflation is the counterforce and works in the opposite direction. You probably remember as a kid, buying a can of Coke for $0.50? The increase in prices over time is inflation, and it means that a dollar today simply does not buy as much as it once did. According to Statista.com, in 2018, the average inflation rate in Canada was approximately 2.24 percent. So let’s use that as the example here. Things don’t look so bright anymore. After keeping your property for 25 years, it will increase in price only by $105,165. Inflation just ate $279,834 of your money…

To make things worse I’ll remind you that you haven’t paid your taxes yet. According to the Government of Canada: “When you sell your home, you may realize a capital gain. If the property was solely your principal residence for every year you owned it, you do not have to pay tax on the gain. If at any time during the period you owned the property, it was not your principal residence, or solely your principal residence, you might not be able to benefit from the principal residence exemption on all or part of the capital gain that you have to report.” This means that if you are considering selling your principal residence, you can be reassured that you likely won’t have to pay any tax on your home provided that you meet certain conditions. However, if you are considering selling one of your investment properties, the tax implication can be a bit more complicated. There are two streams of income you would need to pay tax on:

- Capital gain. Say you purchase a property for $300,000, and you sell it for $405,165 in 25 years. Capital gain = $405,165 – $300,000 = $105,165. In Canada, 50% of capital gain is taxable, hence 50% of $100,000 is taxable = $52,582. If you own the property in your name, this $52,582 is added on top of your other income and is subject to the marginal tax rate for the respective tax brackets you are in. For example, let’s use the tax rate we used in previous calculations – 26.8%. Hence tax liability is roughly $52,582 x 26.8% = $14,092

- Recapture. You are allowed to claim the wear and tear on the property to defer your rental income. The wear and tear are called capital cost allowance. Assume that 90% of the value belongs to the building and 10% of the value belongs to the land, the capital cost of the building is therefore 90% x $300,000 = $270,000.

Where am I getting with all this?

ConclusionsIt will take time. A long time to build the income that will support your lifestyle and allow you to retire. And if you start late enough, you might retire around the retirement age. The example used in this study is just one of the ways things might unfold. It is steady but very freaking slow to build your way out of the 8-5 system. Now I am going to ask you:

- Does it worth spending 12 or even 10 years of your life living only on rice and beans?

- Do you think, 12 years later, when you get that $5,000 check it will all seem worth the time and effort you put in?

- Will you be able to hold on to your full-time job for at least another decade? Or find another boss, who will pay you at least the same salary.

I am pretty sure that those questions got you thinking. Here is a thing, if you want to break free from the hamster’s wheel, you have to get creative! There are ways to speed up your way to the goal of yours. Some, but not all of them are:

- Reinvest Positive Cash Flow;

- Re-finance;

- Keep the full-time job. If you quit your day job early you will lose your steady and secure income stream and lenders may refuse to lend to you because they believe you cannot support the repayments that the loan requires;

- Tax Advantages of Real Estate Investing. Real estate is one of the most tax-advantaged investments compared to other investments.

- 1031 exchanges

- Tax-free or tax-deferred retirement accounts

- Appreciation;

- Equity Build-up;

- Team up with others.

- Syndications

- Partnerships

Simply saving every dime won’t get you far… Saving is better than spending, however, it will not make you rich. Don’t spend your cash on stupid stuff, but realize that it’s better to make more, rather than save more. Doesn’t matter how savvy you are, you can not save your way to wealth. In 99% of cases, your full-time job’s salary will be enough only to meet your basic needs. See below the Maslow’s hierarchy of needs:

You will live a pretty comfortable life:

- Always fed, never hungry;

- Live in a comfy warm little cave;

- Healthy, with access to quality medical treatment;

- Happy in your relationships with friends and family…

Indeed, that’s a great life to live. However, there are a lot of people I know who live such lives, but they don’t seem to be very happy. Some people are different breeds. Those folks stagnate in the certainty and safety that the modern world brings. They strive for a challenge, they are hungry for achievement. Those people strive in crisis and hardships. When it comes to your life – you are the ultimate decision-maker.

You decide, either navigate for miles on woods roads or play it safe take a short trail.E-Book: FINANCIAL FREEDOM. What does it take to get there?

References- Keshner, A. (2019, February 4). Most Americans who earn $90,000 a year say they don’t consider themselves rich. Retrieved February 29, 2020, from https://www.marketwatch.com/story/most-americans-who-earn-90000-a-year-say-they-dont-consider-themselves-rich-2019-01-24

- Canadian real estate market to appreciate 3.2% in 2020 reflecting similar price growth in both condo and detached segments. (2019, December 12). Retrieved April 24, 2020, from https://finance.yahoo.com/news/canadian-real-estate-market-appreciate-110000867.html

- Frankel, M. (2020, April 17). What is a Good Cap Rate for an Investment Property? Retrieved April 24, 2020, from https://www.fool.com/millionacres/real-estate-basics/articles/what-good-cap-rate-investment-property/

- Plecher, H. (2019, October 22). Canada – Inflation rate 1984-2024. Retrieved April 24, 2020, from https://www.statista.com/statistics/271247/inflation-rate-in-canada/

Post: Pandemic REI history

- Toronto

- Posts 8

- Votes 1

Not exactly what you asked, but somewhat similar:

https://www.biggerpockets.com/forums/52/topics/829442-usa-great-depression-rental-housing-market-analysis

Post: USA Great Depression Rental Housing Market Analysis

- Toronto

- Posts 8

- Votes 1

USA Great Depression Rental Housing Market Analysis

Table of contents:

Apartment-House Game

House Values

Land Value

Construction Costs

Rents

I have several letters that rents are being increased, but also we get word from two or three rental agencies here that they are starting to seek a reduction in rents.

Mr. BRINKMAN. In a case where a building is mortgaged for $200,000 and the interest is 6 percent, if that interest rate were lowered to 5 percent and some of the excessive commissions charged for renewals every three years on these loans were eliminated, you would have a saving in interest charges and commissions of $2,500 on that loan. The usual rental of a building of that type is about $33,000. You could give the tenants of that building a 7 percent reduction in their rent, without diminishing the return to the owners at all, simply by lowering the interest rate 1 percent.

Mr. BowTE. Do you mean a building that you would loan $200,000 on would only produce $30,000 a year?

Mr. WHITEFORD. That is the worst loan I ever heard tell of.

Mr. BRINKMAN. $33,000. Mr. Bowie. Nine times.

Mr. WHITEFORD. You talk about vicious loans. I am surprised at how little you know after all your study about this.

Mr. BRINKMAN. Thank you for the insult.

The Rust firm took in the 'Clifton Terrace Apartments at $750,000. The income from that property is sufficient to produce a net return of about 13 percent on the investment.

Apartment-House GameSenator Copeland. Are you familiar with the apartment-house game at all?

Mr. GoRDON. Fairly well. I know they are all broke.

Senator Copeland. Well, is your business comparable to theirs? Are they better or worse off than you are?

Mr. GoRDON. Well, I would say—I can not swear to this—more than half of the apartment houses in Washington have been foreclosed through the inability of the people to carry them. Either the Second or first trusts have been foreclosed and the people lost them. I think that is the best proof that they do not pay.

Senator CAPPER. Well, were not the most of them financed for a great deal more than they had in them?

Mr. GoRDON. Some of them, although a few firms here, which you probably know about, did some very wildcat financing, we don’t account that. That was the exception. Most of our lenders here lend on an apartment house about 60 percent to 65 percent of the actual cash cost of the building and ground. That isn’t bad. Then, this man will have a second trust above that, maybe of 20 percent, and then when a smash comes, he gets squashed.

Senator CAPPER. The second trust is where the high financing took place?

Mr. GoRDON. Not necessarily.

Senator Copeland. Your idea and contention is that even though there has been a foreclosure and new owners have taken possession, that with the amount of the investment they have to make, it goes up to the original cost?

Mr. GoRDON. Well, maybe not that. He takes it over at $150,000. Maybe he will have to spend $15,000 to fix it up, but he may lose that much in vacancies before it is filled up again. Sometimes you have to take these houses and fumigate them with poison to get the bedbugs out.

Senator KING. What do you allow for deterioration in buildings here per year?

Mr. GoRDoN. Well, 2 percent or 3 percent.

Senator KING. In 10 years a building costing $200,000 would deteriorate 20 percent?

Mr. GoRDON. It may go further than that; and if the neighborhood goes back, you get hit awful hard. It is a very risky business.

Senator Copeland. Well, the present investment in an apartment house, according to your figures, is at least 25 percent less than the investment made by the original builder?

Mr. GoRDON. I would say so, yes; but he hasn’t got a new building and is not getting the same rents, either. Keep your mind fixed on this: One-half of the apartment-house owners have lost their buildings because they would not pay. That is a fact. Look at the Star every evening and you will see big foreclosures all the time.

Senator CAPPER. Do not the loan companies—the loan companies. are companies—the loan companies who are doing the financing—make the clean-up? They get the money.

House ValuesSenator KING. Has there been a reduction in the value of the real estate in Washington during the past few years?

Mr. GoRDoN. You can build houses now, the actual cost bein about 30 percent less than you could four or five years ago. The ground has held its own. I am surprised it has, really. In many places, the vacant ground has gone up a little bit.

Senator CAPPER. Are conditions in Washington in that respect better than probably any other city in the country?

Mr. GoRDON, I consider Washington the safest city in the world.

Senator CAPPER. Is it not due largely to the fact that there is a steady payroll here out of the Government Treasury?

Mr. GoRDoN. Yes, sir.

Senator Copeland. And no industrial life.

*Note: Construction and building new houses had become 30% cheaper. During the financial crisis, it is safer to live in non-industrial cities.

Land ValueSenator Copeland. And, as a matter of fact, the present value of the property is probably not half that?

Mr. GoRoon. No; I would not say that. I would say the building is 30 percent off and the ground has held its own. I think that is it. The ground has held its own.

Senator Copeland. Then, your judgment is that the average apartment house, thoroughly modern, is worth about 30 percent less?

Mr. GoRDON. The building; yes. The ground at the same value. The ground has held up very nicely.

*Note: Buildings had ost about 30% in value!!! However, what is really interesting is that the land price remained the same… Investments in lad are much safer.

Senator Copeland. What about land values?

Mr. Do YLE. They are off in the majority of cases. There are instances where surrounding improvements naturally are holding or maintaining values, and in some places, they are going up, depending on the use of the particular property.

Senator Copeland. Has there been anything abnormal in that?

Mr. Do YLE. Just a general lack of demand caused by general conditions.

Mr. BRINKMAN. If a building is worth given amount to-day, and if it would cost to reproduce that building 25 percent less than it cost to put it up originally, ought not rents to come down proportionately assuming the building was on a fair rental basis before? You would have a building worth less and you could not sell it on the market for the same price as when it was constructed. Should there not be a reduction of rentals?

Mr. Doyle. There is no arbitrary situation where the landlord can dictate what he will get out of his property. He has to take what his tenant will pay. That is regulated by supply and demand.

Mr. BRINKMAN. How much of a reduction should occur?

Mr. Do YLE. It is not dependent on what costs have gone down, because we have in mind normal conditions and not abnormal conditions.

Mr. BRINKMAN. You had a good many vacancies at 3901 Connecti cut Avenue, had you not?

Mr. Do YLE. Yes. Mr. BRINKMAN. You reduced rents substantially, did you not?

Mr. Doyle. They have been reduced.

Mr. BRINKMAN. Did you rent a great many of the apartments?

Mr. Do YLE. When we first took it over we did not reduce them as much. Vacancies occurred to some extent afterward. Rents were reduced in the last two months quite materially, and old tenants were given a month's rent.

Mr. BRINKMAN. And you were able to rent some of those empty apartments?

Mr. Doy LE. It has been, through very careful and good management, rented up, and I think it is practically 100 percent rented. They are very reasonable rents, but it pays no return on its cost.

Construction CostsMr. BRINKMAN. How much have apartment building construction costs come down approximately in the last few years?

Mr. Doyle. Approximately 25 percent.

Mr. BRINKMAN. Twenty-five or 30 percent, would you say?

Mr. Do YLE. I said 25. Of course, I am testifying.

*Note: The cost of construction reduced by 25%. It got much cheaper to build, hence it made sense to buy deteriorated houses just for the value of its land. Demolish -> Build a new house. However, if you wanted to build an apartment house and had to have a first-trust loan of $300,000 or $400,000, I do not think it would be humanly possible to get it. Build for cash?

Mr. WHITEFORD. I would not put a dollar in any building enterprise, and I do not think any other sagacious businessman would.

Senator Copeland. I know you can now build property very much less than you could two or three years ago. I built a building three years ago and another this past summer. My cost on the second building was about one-third less than on the first one. There is not any question about that.

Rents

Mr. WHITEFORD. … we hear these complaints of distress that can not pay any rent. I know of people who are living in houses, in apartments, where they are not paying rent. They can not pay it. There are homeowners who can not keep homes. A man came in my office yesterday and asked me to loan him $200 to pay the little installment of interest due to his home, and it is a nice, great big home worth $20,000 odd. That man is suffering. He is in danger of losing his home for a few hundred dollars, but you can not do it by wishing you could. These property owners are in a jam. They are in difficulties and have their properties on valuations and purchase prices that go back for several years. Many of them are losing them now. Their security is jeopardized, for a lot of these properties are not worth the trust.

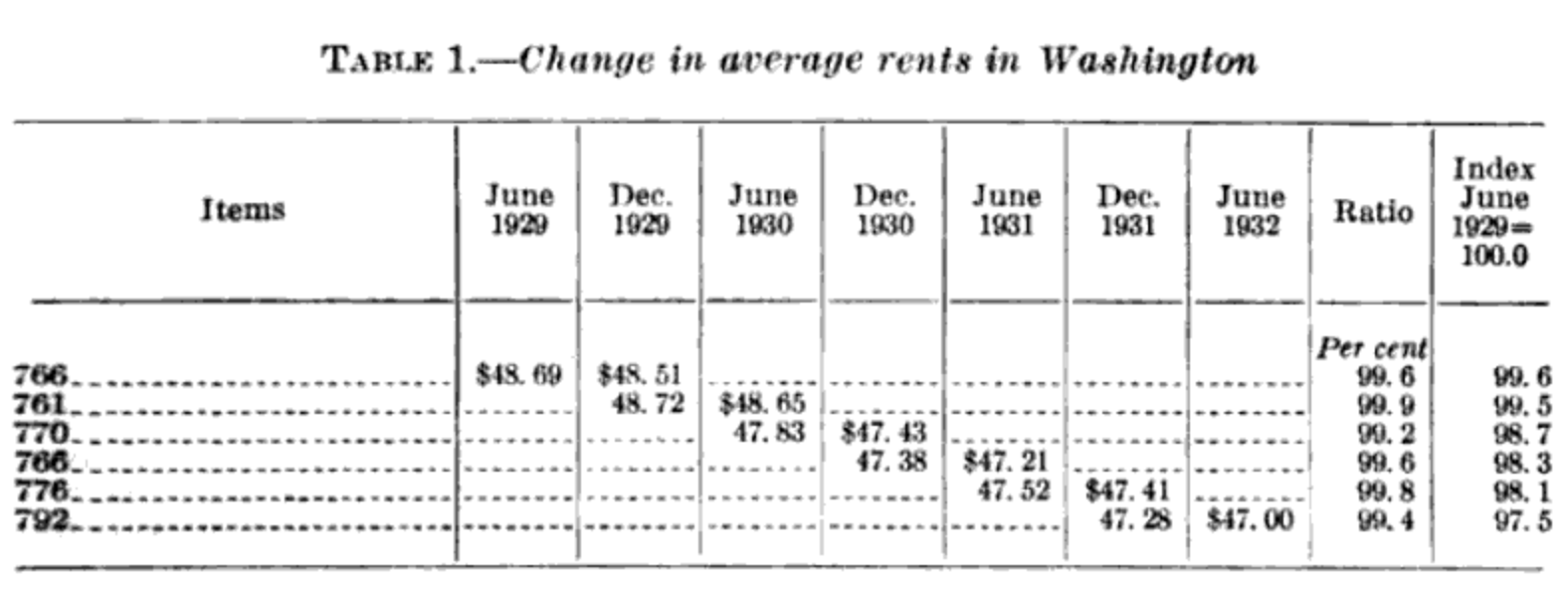

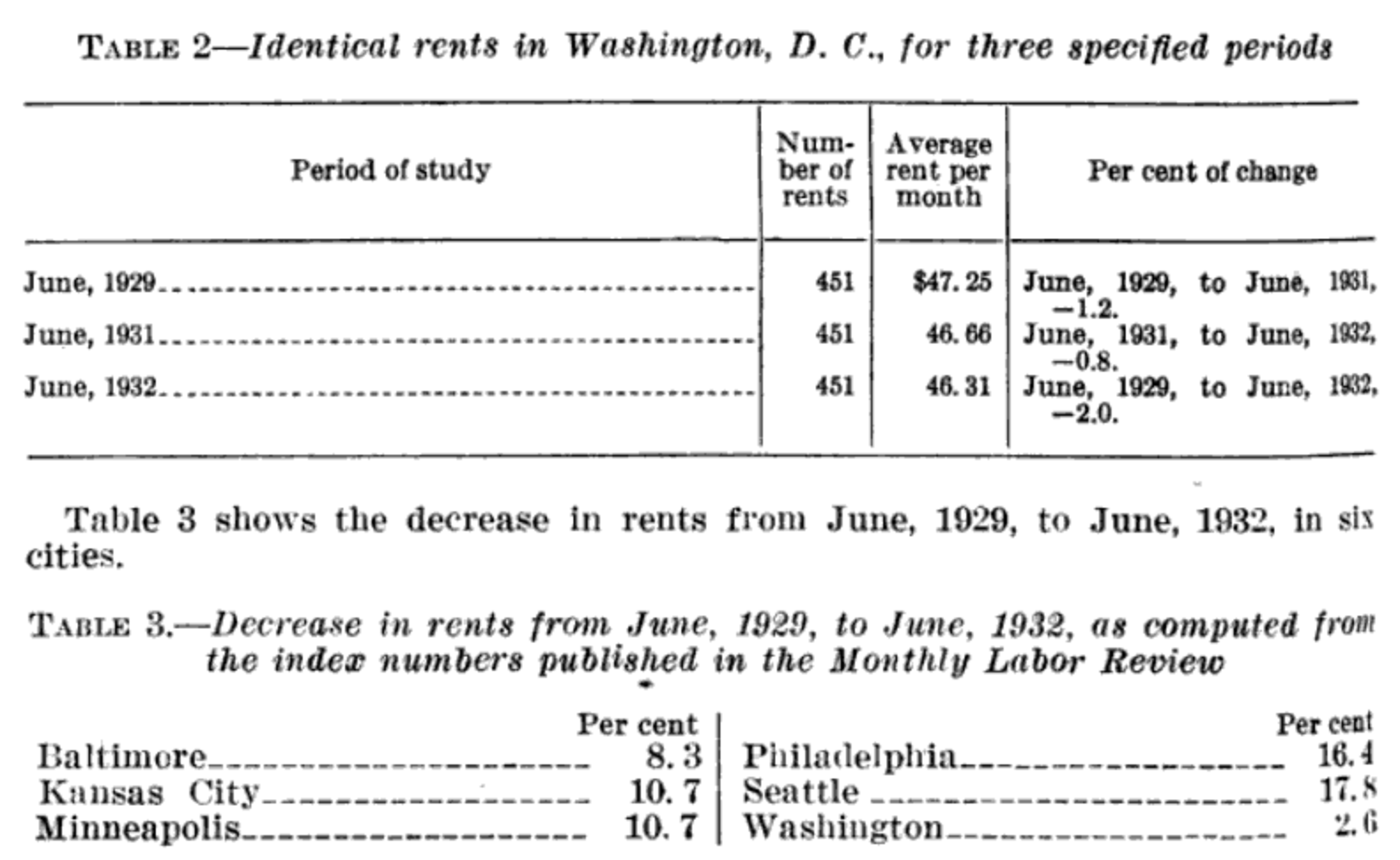

A drop of 2.5 percent in rents in Washington between June 1929 and June 1932.

The CHAIRMAN. In looking over Mr. Brinkman's report I see that the reductions are very small.

Mr. BRINKMAN. That is correct.

Senator KING. You mean it is to the personal advantage of an owner to take charge of the rental of his own property?

Mr. BRINKMAN. If I were the owner of the property I would not put it in the hands of a real estate agent, because I would have to pay them 5 percent commission, have to let him manage the property, buy supplies for it; pay in some cases 8 to 10 percent discount on purchases for the property, let them fix the scale of rates, and if a tenant is already a tenant of another member of the Real state Board, they will not accept him as a tenant. I will say it is a disadvantage in many respects for an owner of a property to turn it over to real-estate agents.

*Note: In order to reduce operational costs, owners will start managing properties on their own. Not the best time to be in the property management business.

Increase in rents by colored people

Mr. J. C. OLDEN. I represent the Better Citizens Bureau. I have made some further investigations with reference to the reduction of rent during the last week or so. I was to bring that further testimony to Mr. Brinkman, but they said they had closed reports on that matter. I can give the facts to this committee; as far as I have been able to find out in the apartment houses and houses that are rented by colored people there has been an increase in rents in the last three years and in some cases no reduction at all, possibly $2.50 or $3 reduction in an apartment.

Senator Copeland. Does this cover a good many houses?

Mr. OLDEN. Practically all the apartment houses rented by the colored in Washington.

Senator KING. Are any of those apartment houses owned by colored people, to which you refer?

Mr. OLDEN. No; they are owned by white people. Some have white agents and some have colored agents.

Might not be the case in the modern world. I suspect there was much more racism back in the 30th.

Mr. BRINKMAN. Properties are not worth the assessments?

Mr. WHITEFord. Not to-day, they are not.

Senator Copeland. I do not know any reason in the world why the landlords of Washington expect they are going to make money when nobody else in the world is doing it.

Mr. WHITEFoRD. Most of them are not.

Property owners and landlords, in particular, are losing money.

If you had $500,000 you would not buy a piece of property and pay for it in cash. All large rental properties have trusts or mortgages on them made by an insurance company or trust company. There is no way in heavens world that they can escape paying 5 or 6 percent interest on their trusts and that interest rate was incurred several years ago. When you figure these properties have got to go on and pay that interest if they do not they will lose them.

*Note: Cash is King. Save cash, leverage.

Mr. WHITEFORd. The landlord gets to it every six months when he pays his interest. Sixty percent of the assessed value represents a fair mortgage, which is a fair way to approximate it.

Senator Copeland... What percentage?

Mr. WHITEFORD. Sixty percent of the assessed value. If that be true, then our figures show the property owner is getting less than 3 percent on his equity.

Mr. WHITEFORD. Yes; and as Mr. Lusk says, it is less than savings bank interest; it is less than Liberty bond returns.

Senator Copeland. Do you not think he would be lucky if he got enough to pay carrying charges?

Mr. WHITEFORd. That is true. When you reduce the rent, you will have people that can not do it which will result in a series of foreclosures in the community.

*Note: Only sixty percent of the houses’ value is backed up by mortgage.

It seems to me that the owner and the agents overlook the great opportunity to increase the number of their tenants, and increase their income by reducing the rent.

Senator Copeland. I will tell you about my experience. I just came from Michigan where I went to see my father. My sister and I own some modest little homes and I asked her how she was getting along with the tenants. She said she cut the rent in two, in each instance, because by doing that she kept the tenant. They could not pay more than that, and if they had moved out because of the rental they had been paying, certainly she could not have rented the property to anybody else, because nobody else would pay it, but by making those reductions houses are occupied. As the chairman said, it seems to me in view of this great crisis, as it is going to be worse after this Congress adjourns, we have got to do something to take care of these people, and the landlords have just got to face the situation. If they do not cooperate they are go ing to lose anyhow, because these people can not the rent. They will have to reduce them or they will move out.

Mr. WHITEFord. We are reducing them. We have shown a lot of reductions, and experience shows it every day. Many of them are losing their property under foreclosure, anyhow, whether they reduce them or not.

Senator KEAN. In the city of Elizabeth, where I come from, there is a row of apartment houses that used to rent for from $55 to $60 a month. They had been getting it right along, but now they are down to $27.

Mr. WHITEFORD. If they have any trusts on the property they can not carry them.

*Note: Increase the number of their tenants, and increase their income by reducing the rent. How many tenants can you put under one roof? Now there are a lot of regulations that will restrict that

Reference

The United States. Congress. Senate. Committee on the District of Columbia. Subcommittee on Rental Investigation. (1932). Rents in D.C.: hearings before the United States Senate Committee on the District of Columbia, Subcommittee on Rental Investigation, Seventy-Second Congress, second session, on June 17, July 28, Sept. 9, Nov. 10, 30, Dec. 1, 2, 17, 20, 21, 23, 27, 29, 1932. Washington: U.S. G.P.O.

https://oleksandr-tereshchuk.com/2020/04/29/usa-great-depression-rental-housing-market-analysis/

Post: The First Step: Sarnia, Ontario

- Toronto

- Posts 8

- Votes 1

About Me

Hello Comrades.

My name is Oleksandr. I'm a full-time professional, working as Autonomous Vehicle Test Engineer in Toronto, Canada. Outside of work I compete in Ironman triathlons on semi-professional level. I am stepping into the real estate world and eager to learn from people more experienced and knowledgeable than me. I am looking for knowledge, advice and connections with like minded people. I am also hoping to be able to provide value to Bigger Pockets community.

I love my job, however I have always felt there is something more behind the office window and meaningless conversations with your colleagues over the lunch. I knew I can do more, I knew I can be more. Not to prove, not to show off, but because I can.

What happens to a tree when it stops growing?

Same with people.

I discovered this simple truth while cycling in Spain, on the hills of Marbella. I always draw the analogy between humans and trees and see it works in every aspect of our lives. The environment we grew up in is the soil. Clay or sandy, low in organic matter soils are the synonyms of the environments filled with drugs and abuse, poverty, fighting parents, tears and pain. Family, friends, our core beliefs and principles - are the roots. Work, relationships, health etc. are the branches of our tree. If we put all ourselves into work and forget about health or relationships with others we are risking to crack the tree. Without counterbalance work branch will grow so big and heavy that it will bend the tree to the side and can even brake it under its weight. Ugly tree.

If we stop improving spiritually, mentally and physically we degrade, we die. I live by the mottoo: To be the best myself - To be the most impactful. Only by being the best version of ourselves, striving for excellence and improving, we find peace and happiness. Once we "filled our cup", we then can give back to the World, create, build and love. Achieving the mastery, when we are at our best at whatever we decide to put our minds to, we begin to love ourselves and we spill the love into the world and people around.

Why am I here?

I am looking for freedom. Financial freedom will allow me to do the things I truly enjoy and become the expert in them. I strive for mastery in anything I put my mind to. I am passionate about writing, finding a problem other people have and solve it. I enjoy training and seeing my physical body evolve and improve.

Working at my full-time job I essentially traid my time for money, I sell my life. Again, don't get me wrong, I love the job! Working with self-driving cars, being in this industry at this amazing time, working with some of the smartest people I ever met, are you kidding me? This is a dream-job! I truly believe it is and I am endlessly grateful for doing what I'm doing. However it's not about the job, its "coolness" or money it brings. There is something inside of me that whispers there is something bigger, I can create something that will bring the value to others, there is another path to take, there is a new world to discover...

There are so many ways I can give back to the world once I am 100% in control of my time. My search for financial freedom led me to real-estate as a vehicle to achieve it. Besides my work and training I ran few side-project businesses. Quickly I discovered that they didn't make me any happier. I didn't feel I got the opportunity to give my all and use my mind to its full capacity. My biggest strength is analysis and analytical thinking. That's why I want to try myself in investing and specifically real-estate investing. Based on my goals I believe that real estate is the perfect vehicle for getting me to destination I travel.

I am looking to create several "passive" streams of income that will generate monthly income of CAD$5,000 (cash flow). I am planning to build a real estate portfolio of several units to achieve my financial goal.

How did I come up with the number?

Great question! I live a very simple life and try to take from this World only what I need, no more or less. I've had luxury cars, I lived in big houses, I stayed at the best 4/5-star hotels and went to fantastic restaurants, I wore nice clothings and traveled to some of the most exotic and expensive destinations in the World. In my short life, I've been all over the places just to discover that none of those things or places made me any happier. I realized I don't need much to be happy and in fact much less than I ever thought. How much is "not much"?

To get the number I did a simple napkin math see how much I need to cover my basic life expenses while staying happy.

The plan

Property Type

I realize that it’s very difficult to achieve great appreciation and a cash flow simultaneously. I use conservative approach and looking for investment properties that will bring the maximal cash flow. My research has shown that small multifamily houses tend to be the most profitable rental investment in terms of cash flow (please correct me if I’m wrong).

Financing

I recently got pre-approved for a mortgage and planning on buying a house as soon as I find a good one, ideally sometime this fall (Oct-Dec). I applied for the First-Time Home Buyer Incentive provided by Canadian government and expect to receive about $120 off my monthly mortgage payments.

Location

I don’t have any personal preference for location, condition or the look of the house, as I am buying it strategically to generate positive cash flow by renting it out. My research has shown outskirts of GTA to hold a strong cash flow potential.

Not to mention that I am able to fix minor things around the house as well as to perform some improvements.

As I already mentioned before the main thing I care about is monthly cash flow. I currently live and work full-time in Toronto Downtown.

I will greatly appreciate any advice or suggestion.

Also I am looking to connect with people in the area and opened to different investment opportunities.

Cheers,

Oleksandr