All Forum Posts by: Eric Fernwood

Eric Fernwood has started 64 posts and replied 793 times.

Post: Best practice for requestimg an MLS drip

Post: Best practice for requestimg an MLS drip

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Allen Vestal,

In order to have a Realtor set up a useful drip for you, they need to know exactly what you are looking for. In this post I will show a process for determining which property characteristics will likely appeal to your target tenant pool. Let’s start with what I consider to be a “good” tenant.

Good Tenants

The only way to make money is to keep the property occupied by tenants who:

- Have stable employment in a market segment that is very likely to be stable or improve over time.

- Pay all the rent on schedule

- Take care of the property

- Do not cause problems with neighbors

- Do not engage in illegal activities while on the property

- Stay for many years

While the above may seem obvious it is not easy to achieve with any consistency because it depends on:

- Selecting properties that target a tenant pool with a high percentage of “good” tenants.

- Working with a skilled property manager who can select a good tenant from all the applicants.

Good tenants are not the norm and property managers who can consistently select good tenants are not common.

Selecting Your Tenant Pool

The first item under the good tenant description is that they have to be employed and stay employed. This means jobs. Your property is no better than the jobs around it. However, even if they are employed today it does not meant that they will remain employed. Employers are like people. They are born, mature, grow old and die. The average life span of a company on the S&P 500 is only 15 years. If new companies are not setting up operations in the location, long term you have a big problem. As the current employers naturally die off and there are no new jobs being created to replace these jobs, all that will be left is low paying service sector jobs. As the percentage of service jobs increases the median per capita income will fall and rents and property prices will follow. Remember that you will own the property for a long time so how the property performs today is not as important as how it is likely to perform over the long term.

Start by determining the key current and probable future employers. Is the market segment they service growing or static or shrinking. Once you identify major employers in a market segment with a good future, look at their employee pool. See below.

Companies generally have a wide range of jobs. Some may be minimum wage while others are highly paid. Based solely on income, there are characteristics which are generally true (which means that it can be false for any individual). See the image below.

Transient Renters

Low-income property tenants tend to be cash-based and have relatively few possessions. They tend to move often and are almost unaffected by an eviction, skip or a property damage judgment. This means that leases mean little or nothing so skips and evictions are common and expensive. In the C class properties our clients own, the average turn cost is between $1,000 and $2,000. The average tenant stay is typically 9 months to 1 year. You need large profit margins to make money with this tenant pool.

Also, in a financial downturn low wage workers are usually the first to be let go and the last to be rehired. In Las Vegas in 2008, vacancies ran higher than 50% in many C class properties forcing the owners into a short sale or to let it go back to the bank.

Unless you really know what you are doing, I do not recommend targeting this tenant pool.

Permanent Renters

As rents increase you move from largely cash-based tenants to largely credit-based tenants. There is a large segment of this credit-based population that, for whatever reason, choose not to or cannot buy a home. This rental population is highly dependent on credit cards, auto loans, and bank accounts. They know that if they pay the rent late or are evicted, they will suffer, credit wise, for a long time. This population has the greatest percentage of what we call good tenants. This is the population we target for our clients. Our average tenant stay for this population is about 5 years.

Transitional Renters

These are also credit-based renters and they make enough money to buy a home. They usually rent because they are in transition from a divorce, a death, or some other event. A soon as they resolve the issue, they move out and buy a home. Just looking at data, the average tenant stay is about 2 years. These tend to be larger homes and turn costs tend to be high. You also need large profit margins to make money with this tenant pool.

Choose Your Target Tenant Pool

Choose your tenant pool carefully based on the percentage of good tenants. Once you decide on your tenant pool, you are ready for the next step, the property profile. See the image below.

Property Profile

A property profile has at least 4 elements:

- Property Type - Condo, high rise, single-family, duplex, single-story, two stories, etc.

- Configuration - Two bedrooms, three-car garage, large lot, etc.

- Location - Reasonable access to the primary employers of your target tenant

- Rent range - What are members of the target tenant pool willing and able to pay

This is where phone calls to a few property managers will get you what you need. Some of it is fairly straight forward. For example, people tend to rent the best place they can reasonably afford and the maximum they can qualify for is about 1/3 of their monthly gross pay. So, if your target tenant pool makes between $3,000 and $4,000 per month, then the properties you target will need to rent profitably for between $1,000 ($3,000/3) and $1,300 ($4000/3) per month.

Work with your property manager to sort out the specifics for property type, configuration, location and verify the rent range. Let’s suppose that after your research you determine the property profile for your target tenant pool is as follows:

- Property type: single family, one or two stories.

- Configuration: three bedrooms and at least a 1 car garage. Two is better.

- Location: North of 11th street, east of the river, west of Grand street and south of the university.

Notice that I did not include the rent range. Realtors cannot search for properties based on what it might rent for. You need to convert property type, configuration, and location into actual properties and look up how much these properties sell for using Zillow, Redfin, or your Realtor. Once you know the price range, verify that you can cash flow with these properties before you continue.

If you find properties that meet the property profile and are profitable, time to provide the property type, configuration, location and price range to your Realtor. They can then set up a drip-feed that meets your needs.

On analyzing, never use the predictions from Zillow or any of the real estate sites. You need to look at historical data, what similar properties near the subject property recently sold or rented for, and base your estimates on them. Basically, run rental comps. Be certain to check for the time to rent. If it takes 6 months to get a tenant, it will be very difficult to make money. If you would like information on how to run rental comps, let me know and I will post how to do this.

Also, keep in mind that ROI and cash flow are snapshots in time. They only predict how the property will perform today but tell you nothing about how the property will perform in the future. You will hold that property for a long time so how the area is likely to perform over the next 10 to 20 years is more important than today. Pay attention to per-capita income, job creation, major employer growth and population growth. These are good barometers of a healthy market.

Allen, a long answer to a short question but I hope this helps. Feel free to post or email questions.

I wish you the best.

Post: Found a property in LV but worried about peak

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Brad D.,

We see a completely different picture of Las Vegas than what I believe you are stating. Yes, the Movoto chart shows that the YOY inventory snapshot is up 70%. However, a year ago there was just over two months of inventory. Today there is about 3 months of inventory. Six months inventory is considered balanced. So there is still a shortage of homes for sale.

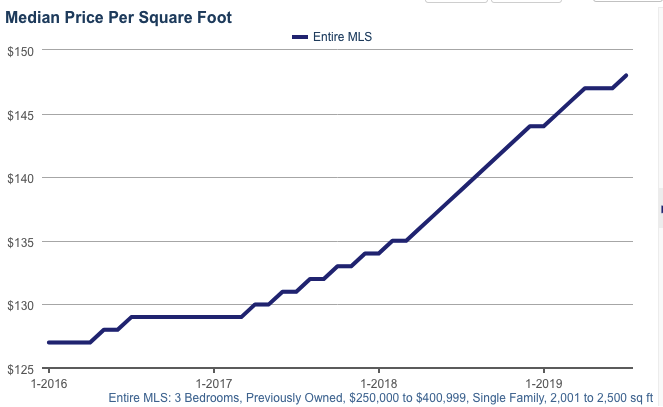

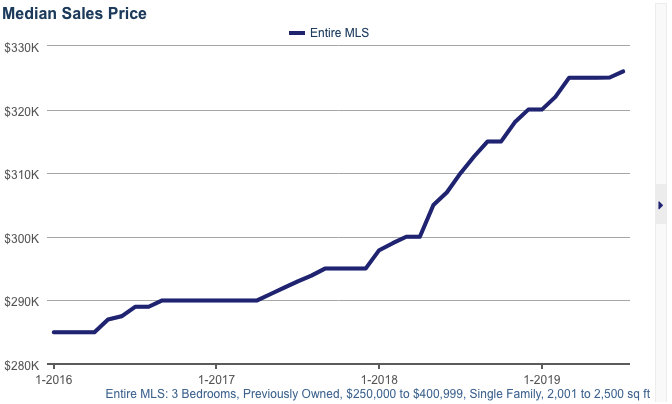

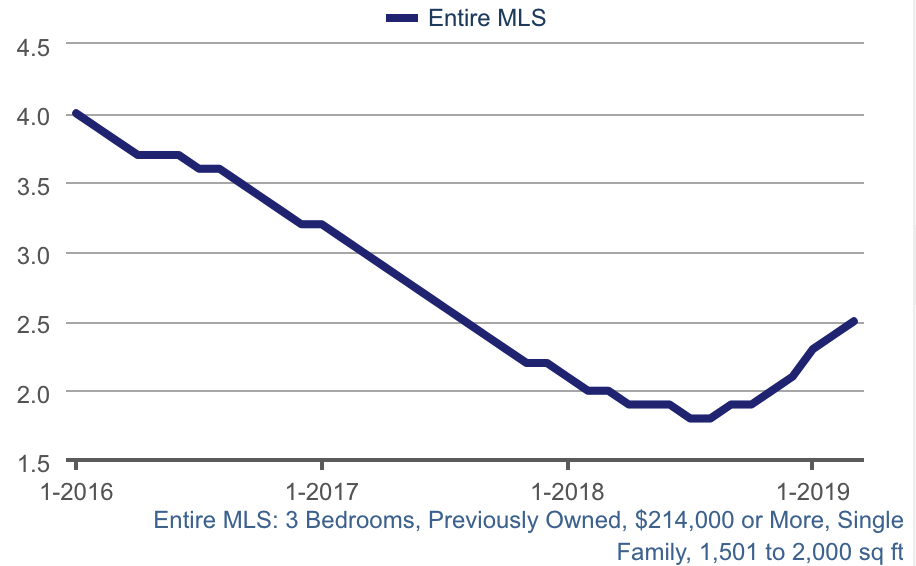

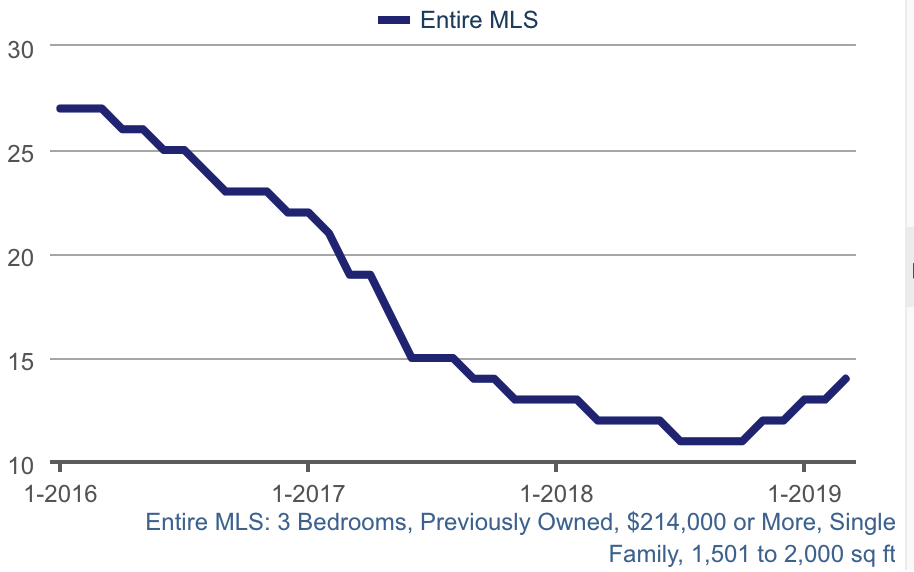

Below are updated charts I pulled from the MLS on 08/08/2019 for the period 2016 to the present, 3 bedrooms, single family, priced between $250,000 and $400,000, 2000SF to 2500SF, for the metro area.

Months of Supply

Note, 6 months of supply is considered a balanced market. We are currently at around 3 months.

Median $/SF

As you can see below, there has been no decrease in price/SF.

Median Sales Price

Based on the MLS data -

- The demand is still strong for single family homes. We are still in a seller’s market. Well priced good properties are still selling in a matter of days. Note that I am not considering million dollar or $50,000 dollar homes because we only deal in profitable investment properties.

- Prices continue to rise in 2019 but at reasonable rates. There has been no decrease in prices.

Market Update

Below are charts from SalesTraq.

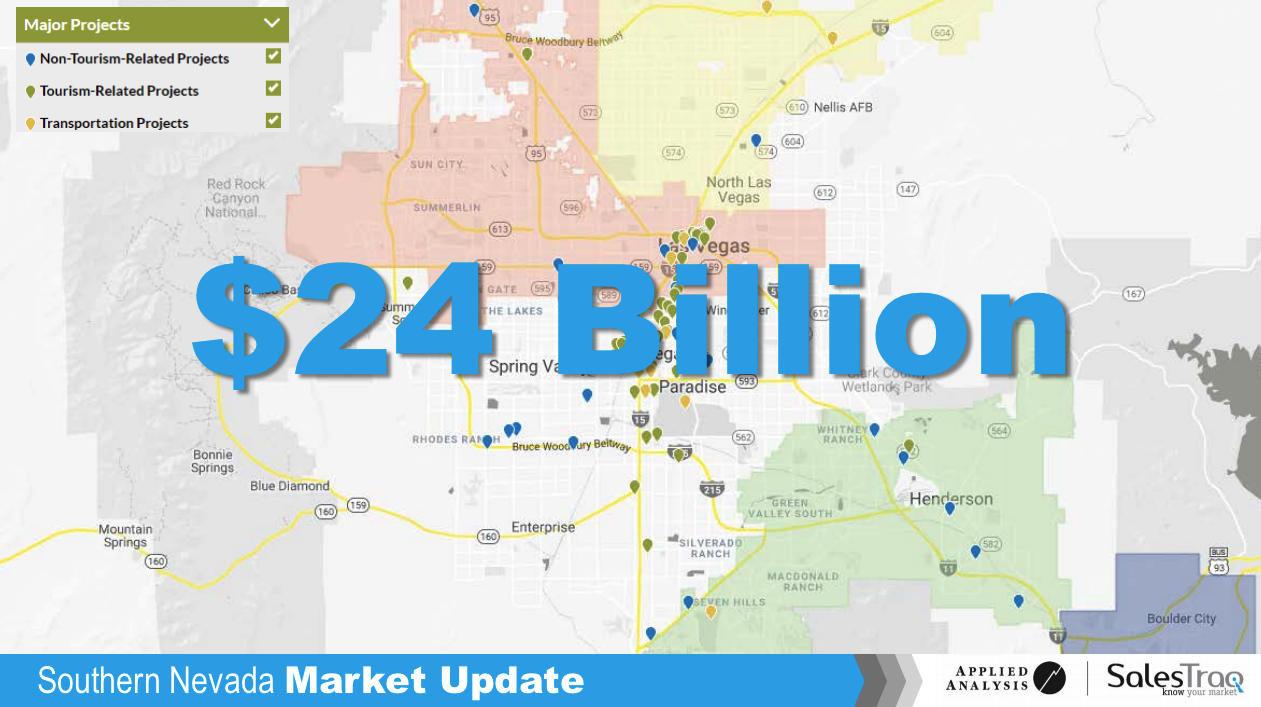

There is currently $24B in projects under construction in Las Vegas. Remember that this is a city of about 2.2M. These projects will create a huge number of new, well paying jobs. These people will need housing and will continue to drive up rents and prices. This is prime time to enter the Las Vegas market.

Las Vegas still has reasonable home prices.

Summary

The current market is strong and we do not see any signs or reasons for a significant downturn in the foreseeable future. The continuing job growth, rising per capita income and population growth will increase the demand. Now is a prime time to invest in Las Vegas market.

Post: Found a property in LV but worried about peak

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Austin M Margarida,

The statistics shown are the latest available. The data from the MLS was through 3/2019. So, not certain about your statement that the data is not current. We did include historical data to show market trends.

I inferred from your post, “What happens in Las Vegas when the next market crash occurs?” A good question but not an easy answer. I doubt that we will have a duplicate crash as we had in 2008, it will be something different. Maybe something we never imagined. So, let’s agree that at some time in the future a national crash will occur and all markets will be hurt, some more than the others. I believe it is impossible for an individual to prevent a national event from impacting the market value of a property. However, it is very possible to protect the income stream from the property. This is accomplished by targeting the right tenant pool.

You want to target a tenant pool with the highest percentage of what I call “good” tenants. I define a good tenant as someone who -

- Has stable employment in a market segment that is very likely to be stable or improve over time.

- Pays all the rent on schedule.

- Takes care of the property

- Does not cause problems with neighbors

- Does not engage in illegal activities while on the property

- Stays for many years

I can go into how to select such a target tenant pool if you are interested, plus how to select properties that target this tenant pool. We did and do target such a tenant pool in Las Vegas. So how did our client’s properties perform during and after the 2008 crash?

In 2014 a potential client (who has since purchased multiple properties through us) asked how our client’s properties performed during the crash. Being engineers we like to provide hard data as opposed to flowery statements. We choose to base our answer on one of our target rental areas, which is shown in the map below. The property profile we selected is: 3 bedrooms 2 car garage, 1,200 to 1,500 SqFt.

So how did these properties perform in terms of market value? In a word, badly. Below is a chart showing the monthly average $/SqFt sale price between 2008 and 2014 for the conforming properties in the selected area above.

During the crash conforming properties in the selected area were selling for an average price of approximately $120/SqFt. By 2012 the average price fell to approximately $70/SqFt.

Next let’s look at the rent these properties generated during this time period. Below is a chart showing $/SqFt rental rates for conforming properties in the same area for the same time period as the above.

As the above shows, rental rates were virtually unaffected by the 2008 real estate market crash. This means that if you purchased an investment property in late 2007 that targeted the right tenant pool and the property was generating an 8% return in 2007, it would still be generating an 8% return during the crash and afterwards, even if the market value of the property went down over 40%.

My point is that no matter where you buy, if a crash occurs you cannot protect the market value of a property. You can protect the income stream from rental properties by selecting the right tenant pool.

Hope I addressed your concerns. If not, either contact me or leave another message.

Post: How to research real estate markets

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello Erica,

Thank you for your kind words. People were very kind to me when I first started investing in real estate. My way to repay their kindness is to help others.

We've decided to patent the algorithm for the break even tool so until that is complete we are not allowing access. On the the while paper on selecting a good property manager, happy to provide it. Just send me an email and I will respond with the paper. This is true for anyone who wants the paper.

My partner and I are engineers and have had to replace property managers a few times. We decided to create a process to make finding the next property manager faster and easier. Later we decided to turn it into a white paper since it worked well for us. Especially the interview questions. I hope you find it useful.

Best regards,

...Eric

Post: Found a property in LV but worried about peak

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Jack B.

We just conducted our Q1 Las Vegas Investor Update and below are our findings.

Market Update

Note that the following data comes from the Las Vegas MLS and is only for properties that conform to our target tenant pool.

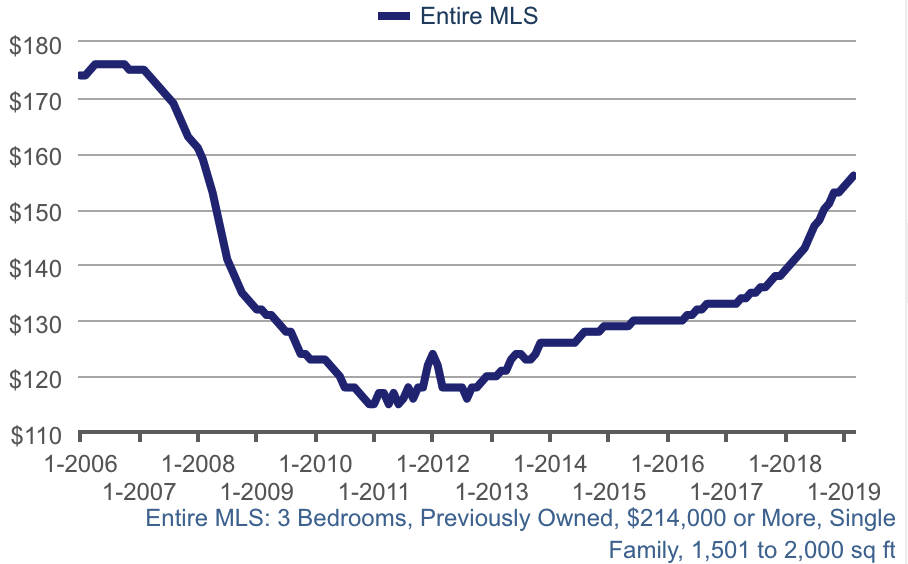

Median $/SqFt for Single Family Homes - The $/SqFt continues to rise. We expect the rate to increase towards the end of the year, likely driven by Californians looking for a more cost effective place to live. Already 30% of all sales today are to Californians. Also, we are still 20% below the peak prices of 2006. If you take inflation into account we are about 35% below peak 2006 prices.

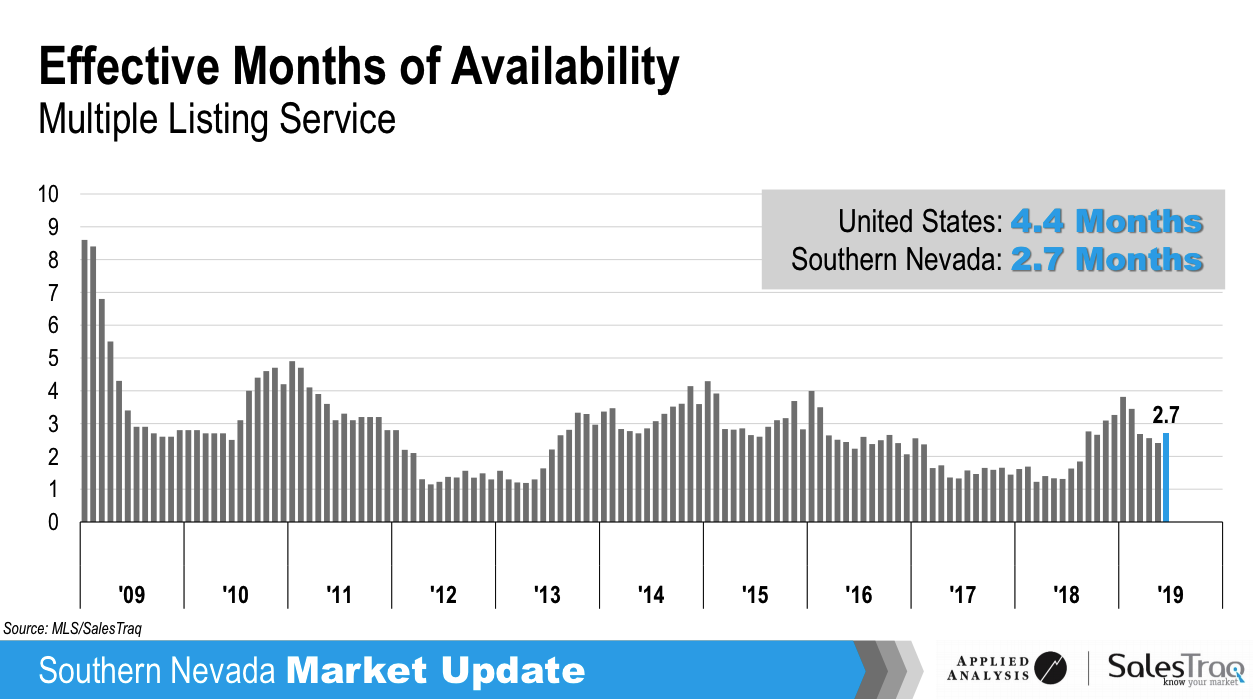

Months of Supply - The months supply of properties has risen since late 2018, but still below 3 months where 6 months is considered a balanced market. The effect of the increased supply is that we are seeing increasing ROI and facing less competition from buyers.

Median Days on Market - The median days on market has risen from 12 to about 14 days. Not a significant change. There is still high demand for the type, configuration and price range we target.

Available Conforming Rental Units by Month - There has been steady decline in available rental units over time. This is what is driving up rents (6.6% average increase in 2018) in the property profile we target.

In summary, the real estate market is very strong. Demand for rental properties is outpacing supply resulting in rising rents. We expect demand to increase during the rest of 2019.

Other Information Worth Noting

Resident Population Growth - 2017 to 2018

Nevada ranks #1 in the US for population growth.

Source: U.S. Census Bureau

Driver's License Surrenders to Nevada by State for 2018

This shows which states people are moving from.

Source: UNLV CBER

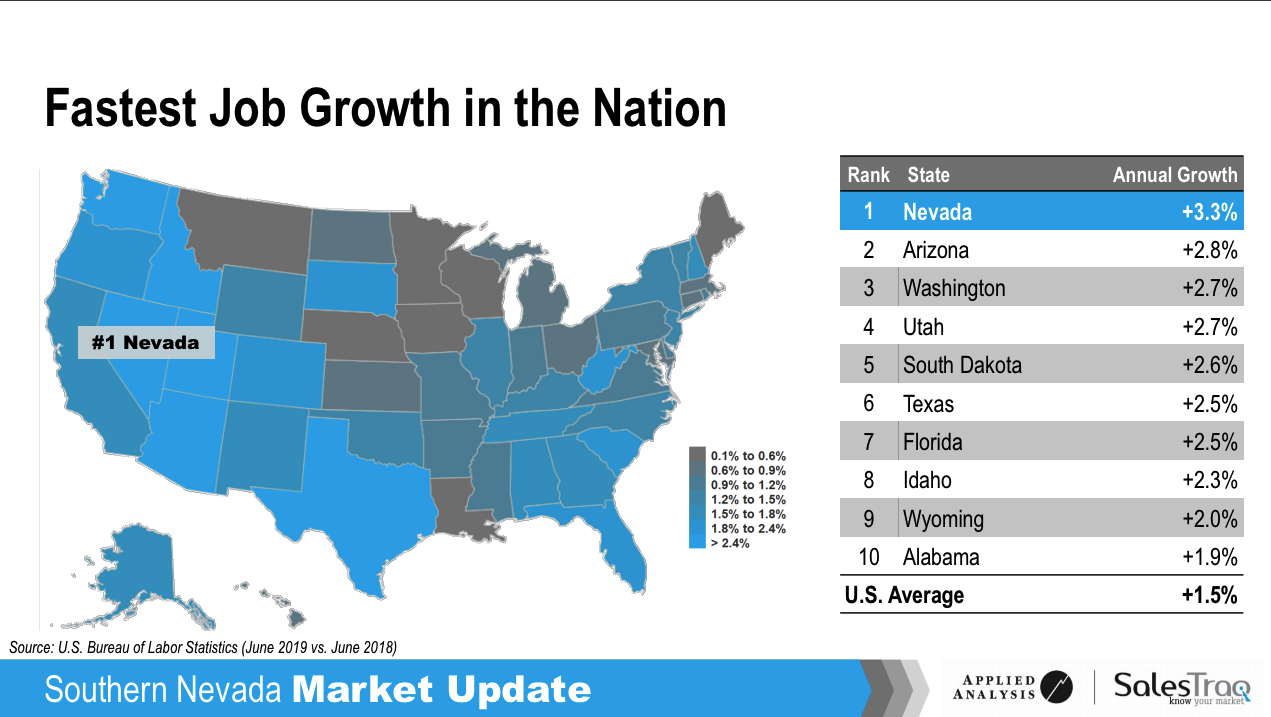

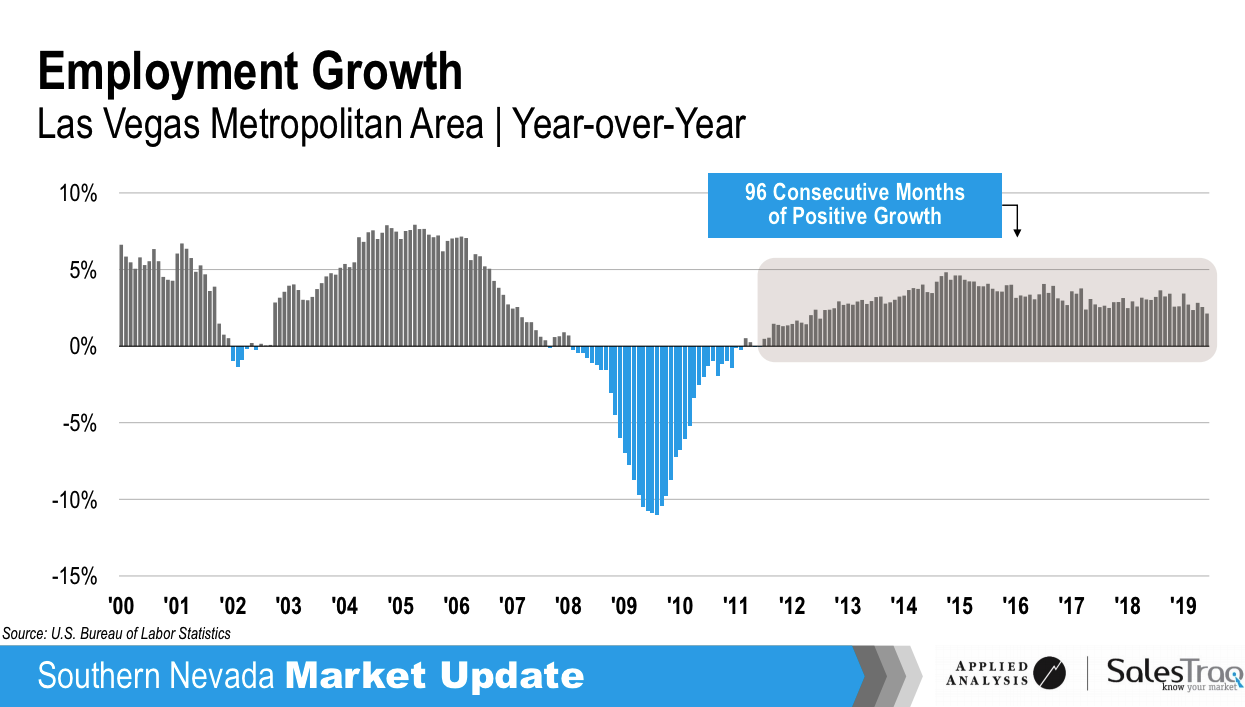

Fastest Job Growth in the Nation

Source: U.S. Bureau of Labor Statistics (December 2018 vs. December 2017)

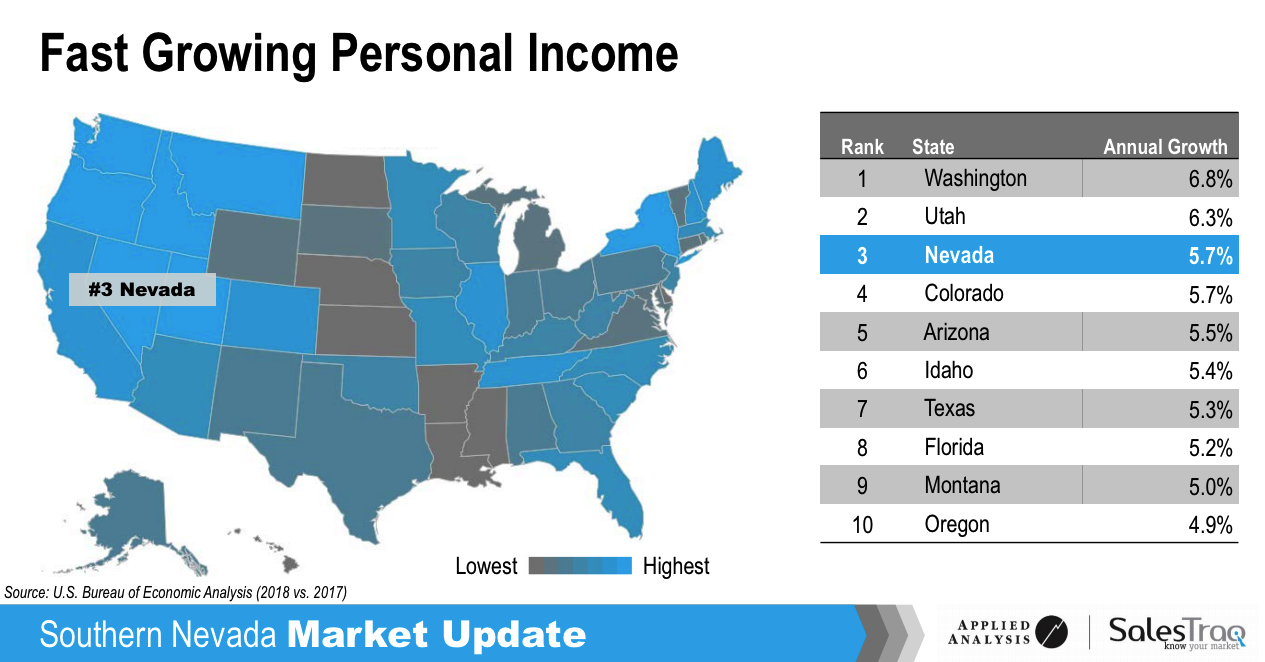

Fastest Personal Income Growth

This shows that the jobs being created are not low end jobs. They pay well and the wages are increasing with the current jobs.

Source: U.S. Bureau of Economic Analysis (Q2 2018 vs. Q3 2018)

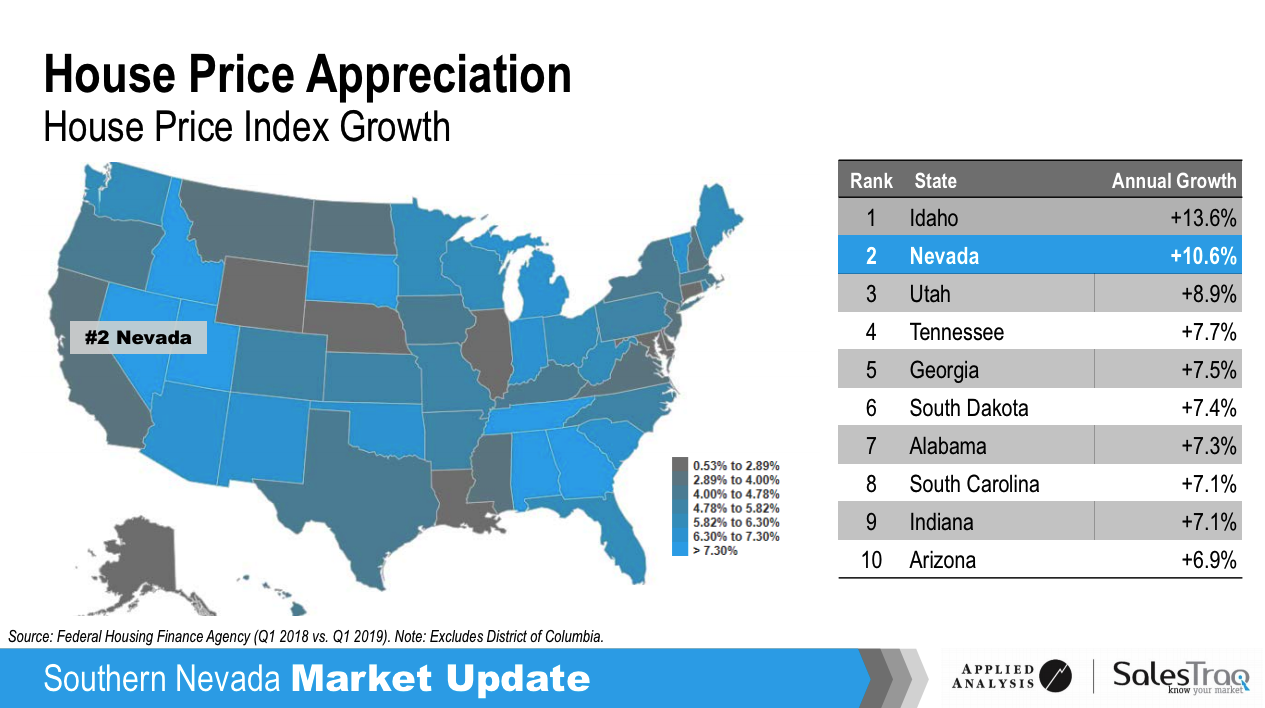

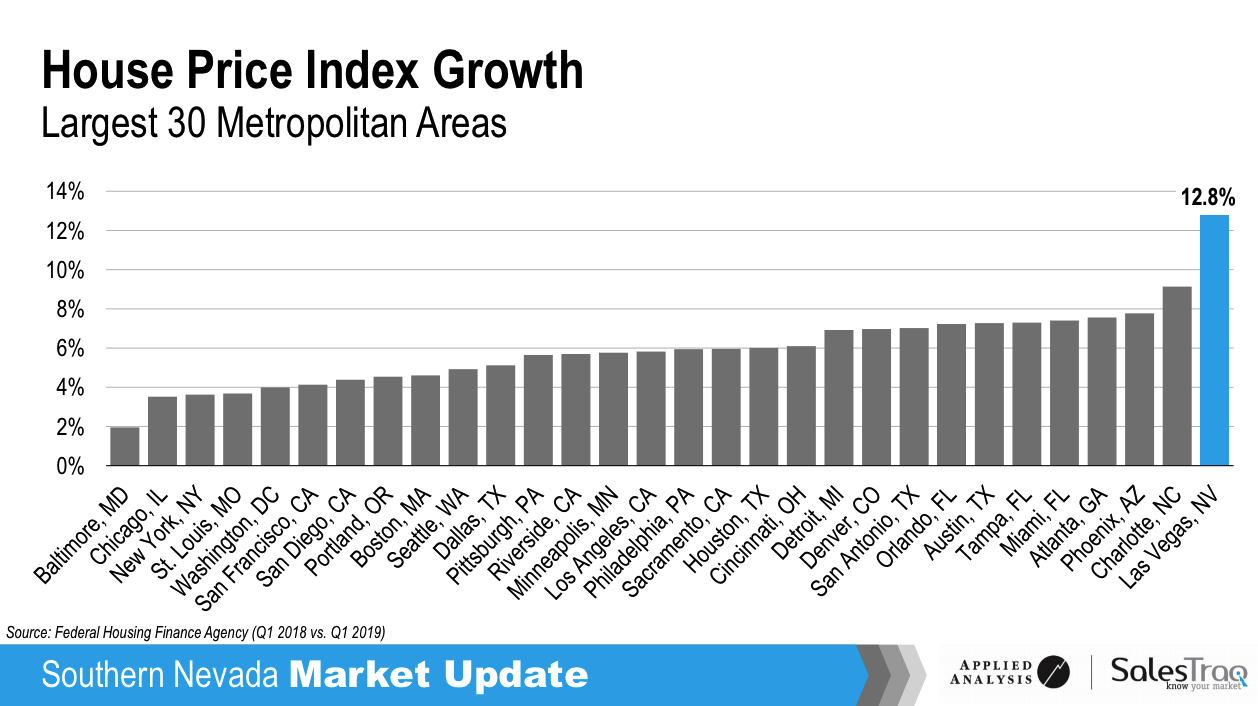

Fastest House Price Appreciation

Source: Federal Housing Finance Agency (Q3 2017 vs. Q3 2018)

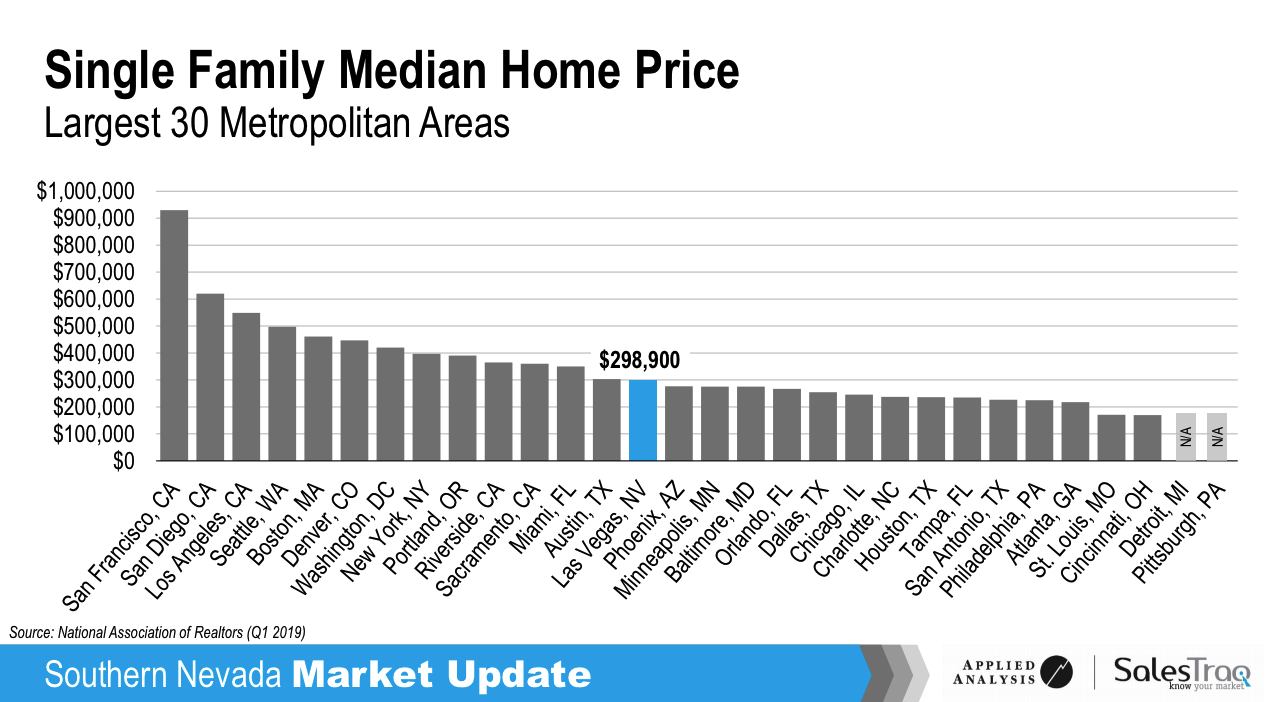

New Home Median Price - Median new home price is $410,000 which is well above the sweet spot for renters. The price of new homes is largely driven by the high cost of land, which is in short supply. Resales will still be the pool for investment properties and will not be diluted by new homes.

Major Projects

Major projects are big drivers of the future economy for Las Vegas. In the 2000 to 2010 era, there was a push to add hotel rooms. The problem was that it was effectively a zero sum game since there were no new attractions added to draw more visitors. This has completely changed in the last few years in that new attractions are being added instead of simply hotel rooms. The nature of Las Vegas has changed too. Until only a few years ago Las Vegas was just "Sin City", a great vacation destination. Today it has changed into a great place to live with endless entertainment, affordable housing and low cost of living. Below are some of the major projects currently under construction (not just planning):

- Sphere Las Vegas - $75M

- Resorts World Las Vegas - $7B

- Drew Las Vegas - $3B

- Raider's Stadium - $2B

- Las Vegas convention center expansion - $750M

- Google - $600M data center

- Union Village - $1.2B

- Project Neon - $900M

- Palms Casino Resort Renovation - $690M

- Caesars Forum Conference Center - $375M

There are many other projects underway but the above are the largest we know of. Any one of the above projects would be huge for a 2.2M population city. These projects will create a large number of additional well paying jobs which will attract even more people to Las Vegas.

Land Shortage

Not many people realize that Las Vegas is an island surrounded by federal land. Approximately 84% of all land in Nevada and 87% of Clark County (in which Las Vegas is located) is owned by the federal government. See the map below for what has happened between 1984 and 2016. Note that 2017 and 2018 were huge growth years for Las Vegas so even less land is available now.

Since there is limited room for expansion, Las Vegas will not have urban sprawl, the only growth path is redevelopment. This is a huge advantage for investors. In most cities, urban sprawl leaves formerly desirable areas "behind" and they tend to decline with increased crime and falling rents and prices. Not the case for Las Vegas:

- Class A properties will stay class A in the future.

- Due to the lack of expansion room, increased demand created by people and companies migrating to Las Vegas will almost guarantee price and rent increases.

Summary

The current market is strong and we expect it to get stronger as 2019 progresses. A significant number of Californians are already moving to Las Vegas and the 2018 Tax Act will drive more people to look for a more affordable place to live. The lack of room for expansion almost guarantees prices will continue to rise as more and more people bid for the limited number of available properties. Las Vegas remains an outstanding investment location for the foreseeable future.

Post: Best cities to buy and hold

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @John Finch,

Thank you for your kind words. People were very kind to me when I first started investing in real estate. My way to repay their kindness is to help others. In this post I will respond to your question concerning obtaining critical local knowledge. Note that the assumption is that you will be evaluating a potential remote investment location.

It is critical to keep a property consistently occupied by a good tenant. So we have a common understanding of "good tenant", below is my definition.

- Has stable employment in a market segment that is very likely to be stable or improve over time.

- Pays all of the rent on schedule

- Takes care of the property

- Does not cause problems with neighbors

- Does not engage in illegal activities while on the property

- Stays for multiple years

Good tenants are not common. Good tenants are the result of targeting the right tenant pool and careful selection by the property manager. In order to have enough applicants so the property manager can select a good tenant, you need to target the right tenant pool.

In my experience you can subdivide tenants by the amount of rent they are willing and able to pay into three groups. While not always true, you can make certain assumptions that are valid a high percentage of the time. See the chart below.

1. Transient - The people in segment ① are primarily hourly workers. They are different than segments 2 and 3 because they live cash based lives. They may not have a bank account, credit card or loans and they tend to have little or no financial history. Without a financial history, there is no effective way to screen out bad actors. Also, since they do not depend upon credit, their actions today have little or no impact on their future. Therefore skips, evictions and damage judgements are more common. In times of economic stress, they are the first to be laid off and the last to be rehired. In my experience, there are relatively few "good" tenants in this segment.

2. Permanent - The people in segment ② are primarily credit based. You can obtain a detailed financial history which includes how often they move and how good they are at paying bills. This is the type of information the property manager needs in order to select good tenants. They tend to follow the "rules" and pay the rent on schedule. This segment knows that a skip, eviction or property damage judgement will hurt them financially for years to come. Most are "permanent" renters, they stay a long time. This is the pool with the highest concentration of "good tenants" and is the tenant pool we target for our clients.

3. Transitional - The people in segment ③ are also credit based but they make sufficient income that they would normally buy a home. Typically they will only stay one to two years before they buy a home and move out. I call this group "transitional" because they do not stay long. With the short stays it is hard to make money with this pool.

How do you determine critical information like the right rent range to target, property type, and configuration from the other side of the country? Talk to local property managers. Local property managers deal with tenants every day. They have a wealth of information.

Start by Googling for property managers in the location you are considering. You will likely find many. However, not just any property manager will do. Select property managers with the following characteristics:

- They are mid sized for that area. If they are too large, you will not appear on their radar. If they are too small, they will not have the processes, procedures or software to be effective .

- Property managers tend to specialize in specific types of properties in specific areas. You want a property manager that specializes in the geography and type of property you are considering.

Once you have identified 5 to 10 interesting property managers, create a written list of questions. You will ask the same questions of each property manager and write the answers down for later comparison. You will learn a lot about the area from the property managers during this exercise. Below are some example questions.

- How many properties are you currently managing?

- I am looking for properties to attract long term tenants that will take care of the property. If you were looking for such a property what type and where would you buy?

- What is the rent range for such properties?

- What is the average length of time your tenants stay in such properties?

- What is your typical time-to-rent for such properties?

- Is there anything you can think of that I should have asked about. (This is a hugely valuable question. You would not believe how much insight I got from this question.)

- What advice would you give a new investor buying their first property in this area?

- What geographical area do you service?

- What is your mix of properties (single family, condos, commercial, etc.)?

After talking to several property managers, you will have a pretty good idea about the area, tenant pool, major employers, regulations, etc. Plus, you should have a pretty good idea of what types of properties do the best and where they are located. Armed with this information, time to do some homework on Zillow, Redfin or whatever real estate site you prefer. Look for properties that match what you learned from the property manager interviews. You now have what you need to do some guesstimating on whether the location is worth further investigation. The data you will need includes the following:

- Property price(s)

- Taxes

- Landlord insurance cost - call a local agent

- Management fee - You learned this from the property manager phone calls

- Periodic fees - the property details

- State income tax rate

You can now plug this information into the proper formulas. Below are the formulas we use:

- ROI = (Income - DebtService - ManagementFee - Insurance - RETax - PeriodicFees) x (1 - StateIncomeTax) / ( DownPayment + ClosingCosts)

- Cash Flow = (Income - DebtService - ManagementFee - Insurance - RETax - PeriodicFees) x (1 - StateIncomeTax)

The results will enable you to make an informed decision on whether this location makes sense or if you need to look for another location.

Another long post but I hope it helps.

Post: Best cities to buy and hold

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Justin Franklin,

Sustained profitability is what I believe you are seeking. While it sounds simple, you have to get the location, investment team, rehab and the right property to achieve long term profitability. So we have a common goal, I believe any long term buy and hold property must meet three criteria:

- Sustained profitability - The property must generate a positive cash flow today and into the foreseeable future.

- Likely to appreciate over time - Properties appreciate in locations that have increasing demand, which is the key driver for sustained profitability.

- Located in an area where you can make money and business risks are low. Only in such an environment can you achieve both current and long term profitability.

Below are comments on what the above actually encompass before I cover the criteria I followed when selecting my long term buy and hold location.

Static Prices And Rents Are Not Static

Official inflation is running at about 3%, which does not include food or energy. I will use 5% as a more realistic inflation rate (if you drive a car or eat). If you are renting out a property today for $1,000/Mo. and rents are static, what is really happening with buying power?

This is why rent and price appreciation must equal or exceed inflation.

ROI and Cash Flow are Only Snapshots in Time

Too many people choose an area due to the current ROI and cash flow. However, ROI and cash flow are only a snapshot in time. They only predict how the property is likely to perform today; they tell you nothing about how the property is likely to perform in the future. See the diagram below where two properties in two different markets currently have the same ROI.

The red line represents a declining market (rents are constant or declining) and the green line represents an appreciating market (rents and prices are increasing). If you only looked at ROI, the markets would appear to be the same. You need to carefully consider how the location is likely to perform in the foreseeable future and not just assume it will remain as it is today.

Rents Lag Prices

Rents lag prices by 2 to 10 years. See the illustration below.

In a declining market, the current rent actually reflects property prices or 2 to 10 year ago when prices were higher. In an appreciating market rents reflect property price 2 to 10 years ago, when prices were lower. This is why declining or static markets have the highest return, today. Over time, they will continue to decline. In an appreciating market rents (and ROI) and prices will continue to rise over time while your major cost (debt service ) is constant.

Population Growth

If people are moving into a location, it is probably a good location for jobs and a desirable place to live. If people are moving away, demand will drop and prices will be static or declining. Do not buy in places with static or declining populations.

Urban sprawl

Not talked about much but you have only to look at any major city and you will see locations that were once the best in town and are now distressed. This is usually the result of urban sprawl. You need to be very aware of which way the city is expanding and buy in areas where the population is moving. See this site for time lapses. Try:

- Memphis

- Atlanta

- Austin

- Las Vegas - Almost no urban sprawl

- Cleveland

Crime

High levels of crime and long term profitability do not go together. I would not consider any city on the top 100 most dangerous cities list. You might know one of these cities well and know that there is a great area in the city. The problem is that companies looking to open new locations will not choose high crime cities. So, even though there may be good areas in these cities, companies will not choose cities that are perceived as a high crime location.

An Area Where You Can Make Money

There are many locations that have enacted regulations that limit property owners rights to control their properties. A good example is rent control. I would never consider any location where rent control is implemented. Beyond rent control, the next best barometer is the time and cost to evict. As a comparison, in Las Vegas, a full eviction is $500 and less than 30 days. In some cold weather states you cannot evict people during the winter. Or, if someone is sick or over 65. In other locations it can take 1 to 2 years to evict. Tenants are very aware of such laws and know how to work the system. Some people might say that nightmare evictions are rare. I agree. However, I view nightmare evictions like cancer. As long as someone else has the cancer, it is a statistic. If you have cancer, it is a nightmare.

Operating costs vary greatly between cities. Significant cost factors include: property taxes, insurance costs, state income taxes, property age and construction and climate. As an example, we have a home in both Las Vegas and Austin. Below is a comparison of three cost differences:

Remember that it is not how much money you make, it's how much money you keep. Construction and climate are also cost drivers. When I owned properties in Houston and Atlanta it seemed that I was always replacing: roofs, siding, wooden windows and dealing with landscaping issues. Below is a typical Las Vegas property. Not a lot of maintenance cost with Las Vegas properties due to the climate and construction.

The Steps I Followed

Before I continue, the steps below were the result of false starts and failures. Do not think I figured all this out at once. Also, there is no perfect city, you want to choose the best city for you. My criteria:

- Metro size > 1,000,000. Small cities are too dependent on narrow market segments and single employers. High risk over the long run.

- Increasing population - I discussed this earlier.

- No location on the top 100 most dangerous cities list due to declining (or static) property prices and rent.

- Increasing job quality and quantity - You need new employers setting up operations.

- Investor friendly - Check for rent control (os similar restrictions) and the actual cost and time to evict.

- Property cost - There is a tendency for new investors to choose locations with very inexpensive properties. Remember that price is a function of demand. No demand, low price. High demand, high price. Of course, you need to hit a balance. If your budget allows a maximum of $250,000, do not consider coastal California.

- Climate - Properties in areas with hard freezes and excessive moisture will tend to require more maintenance than in milder and dryer climates.

- Property age - The older the property, the more maintenance it will require, unless all the major systems and components have been updated recently.

- Taxes - Both income tax and property taxes are a direct hit on profitability. Look carefully.

- Insurance cost - Insurance cost is a good barometer of the likelihood of damage, usually due to climatic or seismic events. Be certain to take the cost of landlord insurance into account when comparing locations.

This post is already long so I will end here with three additional considerations:

Investor team

You simply cannot do it by yourself and there is no reason to try. You need a solid investment team and the most important member is the property manager followed by the Realtor. Keep in mind that extremely few Realtors have any investment knowledge or experience. And, while property managers know what rents well, they generally know little about profitability. You need a strong team that can work together or I would skip the location. (I can expand on this if interested.)

SWOT

When you are comparing different locations you will have a combination of objective data (numbers - easy to compare) and subjective data (opinions, interpretations, points of view, emotions and judgment - hard to compare). An excellent tool of organizing the date is SWOT Analysis. If there is an interest, I can provide more information on SWOT.

Local Knowledge

Books, seminars, podcasts all provide general knowledge. When you buy a property, you are buying a specific property in a specific location subject to the local costs and regulations. If there is interest in how you can get this local information, let me know.

A long post but I thought your question was a good one and wanted to provide the best answer that I could.

Post: Most important criteria for selecting a market?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Jon Schwartz,

Great question. Below is my $0.02.

You are focusing on the most important element, location. If you buy in a bad location, there is little you can do to recover. As long as you buy property in a good location, all but the worst mistakes will be corrected over time through appreciation, inflation and rent increases. My definition of a good location and investment property (you must have both):

- Sustained profitability - The property must generate a positive cash flow today and into the foreseeable future.

- Likely to appreciate over time - Properties appreciate in locations that have increasing demand, which is the key driver for sustained profitability.

- Located in an area where you can make money and business risks are low. Only in such an environment can you achieve both current and long term profitability.

A few comments on the above:

Return - Return (ROI, cash flow) are only a snapshot in time. These calculations only predict what the property is likely to do today; it tells you nothing about how the property is likely to perform in the future. See the diagram below.

The red line represents a declining market (rents and prices are constant or declining) and the green line represents an appreciating market (rents and prices are increasing). You need to carefully consider how the location is likely to perform in the foreseeable future.

A comment on static prices, they are not static. Official inflation is running at about 3%, which does not include food or energy. I will use 5% as a more realistic inflation rate (if you drive a car or eat). If you are renting out a property today for $1,000/Mo. and rents are not increasing, what is really happening?

This is why appreciation, at least equal to inflation, is critical.

Another reason appreciation is important is that appreciation is a good indicator of economic health. If a location is not appreciating or is static or declining, it would be unwise to invest in such a location. Also, rents lag prices by 2 to 10 years so the trend you see in property prices now is what you can expect rents to do in the future.

The last criteria I listed was, located in an area where you can make money. This is a big factor. In some places it is very hard to make money due to the cost of doing business and regulations. Significant cost factors include: property taxes, insurance costs, state income taxes, property age and construction, climate, and eviction cost and time.

As an example, we own homes in both Las Vegas and Austin. Below is a comparison of three cost differences:

Remember that it is not how much money you make, it's how much money you keep. Construction and climate are also major cost drivers. When I owned properties in Houston and Atlanta it seemed that I was always replacing: roofs, siding, wooden windows and dealing with landscaping issues. Below is a typical Las Vegas property. Not a lot of maintenance cost with Las Vegas properties due to the climate and construction.

The cost and time to evict is also a good barometer of how owner friendly the location is. In Las Vegas, a full eviction is $500 and less than 30 days. In comparison, in some cold weather states you cannot evict people during the winter. Or, if someone is sick or over 65. In other locations it can take 1 to 2 years to evict. Tenants are very aware of such laws and know how to work the system.

Some people might comment that nightmare evictions are rare. I agree. I view nightmare evictions like cancer. As long as someone else has the cancer, it is a statistic. If it happens to you, it is a nightmare.

With all the above said, my list for selecting an investment location is as follows:

- Appreciation - I covered the importance of appreciation due to inflation and as a health barometer. Check the property price trends for the location.

- Population growth - If people are moving into a location, it is probably a good location for jobs and desirable place to live. If people are moving away, demand will drop and prices will be static or declining.

- Urban sprawl - Not talked about much but you have only to look at any major city and you will see locations that were once the best in town and are now distressed. This is usually the result of urban sprawl. You need to be very aware of which way the city is expanding and buy in newer areas. See this site for time lapses. Try:

- Memphis

- Atlanta

- Austin

- Las Vegas - Almost no urban sprawl

- Cleveland

- Demographic trend - Be aware that the population of many locations are aging. You need to match the property to the demographics. For example, if the median population age has risen from 35 to 40 over the last ten years, buying a three bedroom home targeting young families may not be the best option.

- Crime - High crime areas and long term profitability do not go together. I would not consider any city on the top 100 most dangerous cities list. You might know one of these cities well and know that there is a great area near the city. The problem is that companies looking to open new locations will not choose high crime cities. Also, people with sufficient funds will leave these areas and the area will go into decline.

- Climate - Properties in areas with hard freezes and excessive moisture will tend to require more maintenance than in milder and dryer climates.

- Age of the property - The older the property, the more maintenance it will require, unless all the major systems and components have been updated recently.

- Property cost - There is a tendency for new investors to choose locations with very inexpensive properties. Remember that price is a function of demand. No demand, low price. High demand, high price. Of course, you need to hit a balance. If your budget allows a maximum of $250,000, do not consider coastal California.

- Taxes - Both income tax and property taxes are a direct hit on profitability. Look carefully.

- Insurance cost - Insurance cost is a good barometer of the likelihood of damage, usually due to climatic or seismic events. Be certain to take the cost of landlord insurance into account when comparing locations.

This is getting to be a long post so I will end it here. If anyone is interested in how to easily obtain deep local knowledge about any given location, let me know and I will do a follow up post.

Johnathan, best wishes on your hunt for a good investment location.

Post: Single Family or Apartments? First investment suggestions please

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Bridget Scileppi,

I believe that the property type is not important. What is important is whether the property meets the following three criteria:

- Sustained profitability

- Likely to appreciate over time

- Located in an area with acceptable business risk

The property that best meets the above criteria is the property you should buy. Let the numbers be your guide on property selection, not any preconceived bias. Also, remember that ROI is only a snapshot in time, an estimate of how the property will perform today, not 5, 10 or 20 years from now.

So how do you determine which property type to buy?

Before I continue, understand the relationship between jobs and sustained profitability. The relationship is pretty simple: no jobs, no rent. A rental property is no better than the jobs around it. Let's start with location considerations.

Location

Some location characteristics to watch for:

- Long term major employer outlook, both the market segment(s) and the specific companies. How did they do in the last crash? Also, the average life of a S&P 500 company is 15 years. You have to assume that the current major employers (unless they are government or utilities) will die off over time.

- New business relocating to area - Unless new businesses are relocating to the area, the area is or will decline, as will your rent and property value.

- Population growth - Population trend is an excellent barometer. If people are leaving a location, the long term outlook is bad. If people are moving to a location, the prospects improve.

- Per capita income growth - If the increase in per capita income is not greater than inflation, incomes are going down.

- Taxes - High taxes are a direct hit on profitability. This includes income tax, property tax and any other kind of tax.

- Cost and time to evict - Tenants know the eviction laws and if they know it will take months to evict them they are more likely not to pay the rent. This can be mitigated by the tenant pool.

- Rent control - If governments are usurping the rights of property owners, look somewhere else.

The point is, only buy where you can meet the three criteria.

Target Tenant Pool

Once you have a location selected, it is time to select the key employers and market segments who that will do well in the foreseeable future. Once you select the employers, you can determine a tenant pool that best meets the following criteria:

- Has stable employment in a market segment that is very likely to be stable or improve over time. These are the target employers you selected.

- Pays all the rent on schedule

- Takes care of the property

- Does not cause problems with neighbors

- Does not engage in illegal activities while on the property

- Stays for many years

I can go into more details on tenant pool selection if you are interested.

Once you know your target tenant pool, determine the property characteristics that will target them:

- What type? Condo, high rise, single family, duplex, single story, two story, etc.

- What configuration? Two bedroom, three car garage, mud room, etc.

- Location - Acceptable access to the target tenant employers?

- Rent range - What rent range best matches the target pool?

Summary

Instead of deciding on a property and hoping it will meet the three criteria, do the homework, starting with the location, and let the target tenant pool determine the property.

I hope the above helps.

Post: Best city/area to in buy and hold for cash flow in the U.S.

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Selecting a good investment location for long term buy and hold is critical. What makes it more difficult is that traditional metrics like ROI or cash flow are only snapshots in time. They estimate how the property will ideally perform today but tell you nothing about future performance, maintenance costs, etc. And, on a long term hold, the foreseeable future is more important than what is happening today. In this post I will cover:

- A clear goal

- Using the right metrics for comparing properties

- The characteristics of a declining market vs. an appreciating market.

- The process I would follow for selecting a location.

My Goal

I believe every investment property should meet the following three criteria:

- Sustained profitability - The property must generate a positive cash flow today and into the foreseeable future.

- Likely to appreciate over time - Properties appreciate in locations that have increasing demand, which is the key driver for sustained profitability.

- Located in an area where you can make money and business risks are low. Only in such an environment can you achieve both current and long term profitability. Business risks refer to regulations such as rental control, code enforcement, eviction rules, etc.

Simplistically, if the property is not generating a positive cash flow today and is not likely to appreciate (price and rents), look somewhere else. I will talk more about declining markets vs. appreciating markets later.

Use the Right Metrics

I frequently see people making property and location decisions based on simple metrics like rent/price or simple ROI calculations. (Another mistake is using constants for maintenance and vacancy; each property is different but I will cover this if anyone is interested.)

The following are two similar properties, one in Las Vegas and one in Austin. Email me if you would like the details on the properties.

Notes:

- I used the same monthly fees for both properties to keep things comparable.

- Debt Service: 25% down, 5.125% rate, 30 year fixed.

- Management: 8%

- Closing costs: 3%

- Income tax rate: 0%, neither Texas or Nevada have state income taxes

If I used the popular rent/price ratio, here is the results:

The clear winner is the Austin property. But is this actually true? I will compare the two properties using the following formulas:

- ROI = (Income - DebtService - ManagementFee - Insurance - RETax - PeriodicFees) x (1 - StateIncomeTax) / ( DownPayment + ClosingCosts)

Below are calculations for both properties:

- Austin: (1,700 x 12 - 1100 x 12 - 8% x 1700 x 12 - 1625 - 6022 - 41 x 12) x (1 - 0) / ( 25% x 252500 + 3% x 252500) or -3.6%

- Las Vegas: (1,490 x 12 - 1110 x 12 - 8% x 1490 x 12 - 450 - 1490 - 41 x 12) x (1 - 0) / ( 25% x 255000 + 3% x 255000) or .98%

Despite the Austin property having a significantly higher rent/price ratio, it has by far the worst actual return by over 4%! The lesson here is that simplistic formulas can be very misleading. Even more important, this formula, like all others, only reflects an estimate of current return, not what will or is likely to be in the future.

Declining Market Vs an Appreciating Market

People generally buy investment properties with the intention of holding on to them for many years. If this is the case then what is likely to happen in the foreseeable future is actually more important than the current situation. ROI and cash flow only indicate today's return, they tell you nothing about future returns.

Multiple studies have shown a strong correlation between property prices and rents (see Federal Reserve study). Basically, rents lag property prices by 2 to 10 years or, if prices are stable (declining in real dollars) or declining, rents will follow. See the illustration below.

In a declining market, the current rent reflects property prices from 2 to 10 years ago and they are likely to be relatively high compared to areas with appreciation. Declining locations work for the short term but over time you can end up underwater and have insufficient rent to cover your operating costs. Another issue is the quality of the tenant. As rents fall, you are more likely to have increased problems with evictions, skips and property damage. The diagram below illustrates this problem.

If you doubt that this can happen, in every major city I know there are areas that were once the "best" in town are now distressed high-crime areas. The locations did not evolve from being the best to depressed over night, it happened over the years.

An appreciating market is the opposite of a declining market. Rents still reflect property prices from 2 to 10 years ago but since property prices have risen more than rents, initial returns will be lower than a declining market. Since your largest cost (debt service) is fixed, as rents rise over time your return increases, as illustrated below.

In summary, invest in an appreciating market if you plan to hold a property for some time. You initial return will be lower than a declining market but over time you will make far more money plus the property will appreciate.

My Process for Selecting a Good Investment Location

A little history. I was living in NYC when I decided to change my profession and sell investment real estate. I knew that NYC was not the place so I started my search for where to move to.

After a lot of consideration I decided that if I developed a criteria for a good investment property I could work backwards to select a good location. My original set of criteria was much more complex and it took me time to simplify and focus the criteria to what it is today. I listed them at the beginning of my post:

- Sustained profitability - The property must generate a positive cash flow today and into the foreseeable future.

- Likely to appreciate over time - Properties appreciate in locations that have increasing demand, which is the key driver for sustained profitability.

- Located in an area where you can make money and business risks are low. Only in such an environment can you achieve both current and long term profitability.

Evaluating each location at the level of detail to determine the above criteria is satisfied is not possible. So, some gross filters are needed to trim down the list:

- Minimum population - I would only consider cities with a population exceeding 1M. My concern is that if the population is less than a million it will be too dependent on a single industry or market segment.

- Not on the list of the 100 most dangerous US cities. Here is one such list. Why is this important? Long term growth. No one wants to live in a high crime environment so those with the means to move, do so. The median income of the people who remain falls and city services follow. Also, few non-government organizations will choose such a location to open new facilities.

- Taxes - There is a reason so many people and companies are leaving the "blue states". Here is one source.

- Rising $/SqFt property prices. I found no single perfect data source but here are some good sources: Zillow, Trulia, Redfin

- Increasing population: Simplistically, if people are moving out of an area, it is not desirable. Declining population means declining demand for housing which will result in declining property prices: US Census data

- Increasing inflation adjusted per capita income. One of the better sources.

At this point you should have a short list of locations and you can dig into each remaining location. Below is the process I would follow from here:

Summarizing the remaining steps:

- Already covered this step.

- Not all target tenant pools (or population segments) make equally good tenants. We carefully choose a tenant pool and the result is an average tenant stay of about 5 years, 3 evictions in 10 years and little tenant damage.

- Once you have a target tenant pool, you can determine the property profile that matches your target tenant pool. The four factors are: type, configuration, location and rent range. From the property profile you can determine the price range of such properties and profitability. If the prices are out of your budget or the properties are unlikely to cash flow, select another location and start with step 1 again.

- Unless you have a strong investment team, you will fail. The key member is the property manager followed by the Realtor. If you are unable to find a strong team, go to another location.

- You and your team evaluate individual properties based on: price, rent, time to rent, rehab cost and risk, average tenant stay, probable maintenance cost, etc.

Summary

I covered a lot of material in this post. If anyone has questions please post them or send me an email and I will do my best to respond.