All Forum Posts by: Eric Fernwood

Eric Fernwood has started 63 posts and replied 773 times.

Post: Population Bust, Property Value Decline?

Post: Population Bust, Property Value Decline?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Mat Garcia,

While there may be population declines at national levels, local factors have a much bigger impact on RE. For example, from 1970 to 2020, Cleveland lost 50% of its population (from 750,903 to 372,624). This dramatic decline had nothing to do with birth rates. Meanwhile, Las Vegas's population increased by 410% during the same period (from 125,787 to 641,903), also not due to birth rates. So, while national and international population trends exist, they may not apply to individual cities within a country.

For the U.S., immigration will play a significant role in population growth for the next decades.

Population changes significantly impact real estate investors. In cities with declining populations, properties are typically much cheaper, but rents and prices rarely outpace inflation. Conversely, in cities experiencing significant and sustained population growth, while initial prices are higher, both property values and rents are more likely to outpace inflation.

Post: San Diego Investor looking to invest out of state, BUT WHERE?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello Kelby Kraft,

Whether a city is a good investment location depends on your goals. If your goal is initial cash flow, Midwestern cities are some of the better places to buy properties. The challenge with most Midwestern cities is that prices and rents haven't kept pace with inflation.

We don't live on a fixed number of dollars. As inflation rises, it takes more money to purchase the same goods and services. If your rental income isn't growing faster than inflation, you won't have the additional income to pay these higher prices. In this situation, your only options would be to either continuously reduce your standard of living or return to work.

An example will show the problem. Suppose your planned hold period is 30 years, the average inflation during this period is 5% per year, rent growth is 2% per year, and your initial rent is $1,000 per month. How much will the rent be in 10 years, 20 years, 30 years?

- Rent in 10 years: $1,000 × (1 + 2%)^10 ≈ $1,219

- Rent in 20 years: $1,000 × (1 + 2%)^20 ≈ $1,486

- Rent in 30 years: $1,000 × (1 + 2%)^30 ≈ $1,811

As you can see, over 30 years the rent increases from $1,000 to $1,811. However, because inflation rose more rapidly than rent, your buying power—what you actually live on—declined, as shown below.

- Buying power in today's dollars after 10 years: $1,000 × (1 + 2%)^10 / (1 + 5%)^10 ≈ $748

- Buying power in today's dollars after 20 years: $1,000 × (1 + 2%)^20 / (1 + 5%)^20 ≈ $560

- Buying power in today's dollars after 30 years: $1,000 × (1 + 2%)^30 / (1 + 5%)^30 ≈ $419

Therefore, if your goal is initial cash flow but not financial independence, most Midwestern cities are good investment locations. However, if your goal is financial independence, cities were rented and prices do not increase faster than inflation will not enable long term financial independence.

Post: San Diego Investor looking to invest out of state, BUT WHERE?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Anthony D'Angelo,

While I can't recommend a specific city without understanding your situation and goals, you're absolutely right to prioritize choosing the right city for your real estate investments. The city where you invest determines all long-term income characteristics.

Many people choose cities with low property prices or follow recommendations for specific cities. As an engineer, I believe in clearly establishing the goal and then working backward to where you are today.

The Goal of Real Estate Investing

The goal of real estate investing is lifelong financial independence. This isn’t a one-time milestone or a fixed amount of money—it’s about creating a sustainable income stream that meets two key criteria:

- Rents Outpace Inflation: Rental income must grow faster than inflation to cover rising costs. Cities with strong, sustained population growth are more likely to meet this requirement.

- Lifelong Income Stability: Your income must last a lifetime. This requires tenants to maintain stable employment, even as companies come and go. Cities that attract new businesses, have low crime rates, a metro population over 1 million (for infrastructure and skilled labor), and low operating costs are best positioned to meet this need.

Where to Start Your Search

Evaluating every city in the U.S. isn't practical. Start your search by focusing on cities with metropolitan populations over 1 million that have had significant and sustained population growth. This Wikipedia page has the data you need. Smaller cities are typically more vulnerable to economic downturns and market shifts and do not attract major employers.

After identifying cities that meet these basic criteria, apply the following filters to narrow down your list:

- Low Crime Rates: Avoid cities with high crime rates. Use resources like CBS’s list of the 50 Most Dangerous Cities in America to identify cities to avoid.

- Low Operating Costs: High operating costs erode your profits. Key considerations include property taxes and insurance rates. Resources like ValuePenguin and LendingTree can help you compare your operating costs across cities.

- No Rent Control: Rent control can limit your ability to raise rents, screen tenants, or evict non-performing tenants. Avoid investing in cities with rent control policies.

By filtering out cities that don’t meet these criteria, you’ll create a shortlist of potential investment locations for further evaluation.

Operating Costs

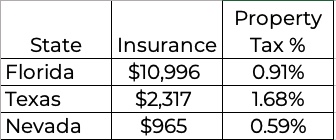

Operating costs are such a huge factor for investors that I wanted to provide more detail. Below is a comparison between Nevada, Texas, and Florida.

- State average property tax source.

- Texas and Nevada average insurance source.

- Florida's average insurance cost source

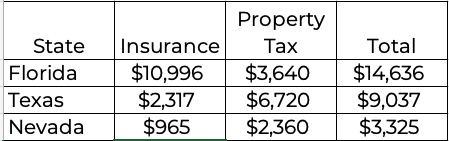

To put this in perspective, below is the estimated annual operating costs for a $400,000 property.

Compared to a property in Nevada, properties in other states require additional cash flow to compensate for their higher operating costs.

- Florida: +$11,311 ($14,636 - $3,325)

- Texas: +$5,712 ($9,037 - $3,325)

The takeaway is that operating costs can have a huge impact on financial independence.

Remote Investing

Live where you like, but invest where you can achieve lifelong financial independence.

Most investors don't live in cities that meet all the requirements for financial independence. Therefore, the real question isn't whether to invest remotely—it's where and how to do it safely.

Once you've selected a city that meets the requirements, you'll need an experienced local investment team. While books, seminars, podcasts, and websites offer valuable general knowledge, ultimately, you're investing in a specific property in a specific city. This requires deep local expertise. Only an experienced investment team can provide the local market knowledge and resources you need.

Post: How To Analyze the Market??

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Emily Strong,

The first step should be selecting an investment city. The city where you invest determines all long-term income characteristics. I will share a straightforward process for creating a short list of cities for potential further consideration. And, you will not have to pay for any of the data. It's publicly available.

Before I do, I want to ensure we have a common understanding of the goal of real estate investing.

The Goal of Real Estate Investing

The ultimate goal of real estate investing is lifelong financial independence. This isn’t a one-time milestone or a fixed amount of money—it’s about creating a sustainable income stream that meets two key criteria:

- Rents Outpace Inflation: Rental income must grow faster than inflation to cover rising costs. Cities with strong, sustained population growth are more likely to meet this requirement.

- Lifelong Income Stability: Your income must last a lifetime. This requires tenants to maintain stable employment, even as companies come and go. Cities that attract new businesses, have low crime rates, a metro population over 1 million (for infrastructure and skilled labor), and low operating costs are best positioned to meet this need.

Where to Start Your Search

Evaluating every city in the U.S. isn't practical. Start with cities that have a metropolitan population of over 1 million and have significant and sustained population growth. This Wikipedia page has the data you need. Smaller cities are typically more vulnerable to economic downturns and market shifts. Plus, they don't tend to attract new major employers that will create the replacement jobs your tenants will need over time.

After identifying cities that meet these basic criteria, apply the following filters to narrow down your list:

- Low Crime Rates: Avoid cities with high crime rates. Use resources like CBS’s list of the 50 Most Dangerous Cities in America to identify cities to avoid.

- Low Operating Costs: High operating costs erode your profits. Key considerations include property taxes and insurance rates. Resources like ValuePenguin and LendingTree can help you compare your operating costs across cities.

- No Rent Control: Rent control can limit your ability to raise rents, screen tenants, or evict non-performing tenants. Avoid investing in cities with rent control policies.

By filtering out cities that don’t meet these criteria, you’ll create a shortlist of potential investment locations for further evaluation.

Remote Investing

Live where you like, but invest where you can achieve lifelong financial independence.

Most investors don't live in cities that meet all the requirements for financial independence. Therefore, the real question isn't whether to invest remotely—it's where and how to do it safely.

Once you've selected a city that meets the requirements, you'll need an experienced local investment team to minimize risk and maximize returns. While books, seminars, podcasts, and websites offer valuable general knowledge, ultimately, you're investing in a specific property in a specific city. This requires deep local expertise. Only an experienced local team can provide the local market knowledge and resources essential for success.

Summary

By following the steps outlined above, you can quickly narrow your focus to cities that support lifelong financial independence. However, if you invest in a city that doesn’t meet these criteria, no number of properties will compensate for the long-term challenges you’ll face.

Post: Best markets to invest in?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Eric Shim,

You’re absolutely right to prioritize choosing the right city for your real estate investments. Where you invest determines all long-term income characteristics. While I can’t recommend specific cities without understanding your current situation and long-term goals, I will share a straightforward process for creating a short list of cities for potential further consideration.

Before I do, I want to ensure we have a common understanding of the goal of real estate investing.

The Goal of Real Estate Investing

The ultimate goal of real estate investing is lifelong financial independence. This isn’t a one-time milestone or a fixed amount of money—it’s about creating a sustainable income stream that meets two key criteria:

- Rents Outpace Inflation: Rental income must grow faster than inflation to cover rising costs. Cities with strong, sustained population growth are more likely to meet this requirement.

- Lifelong Income Stability: Your income must last a lifetime. This requires tenants to maintain stable employment, even as companies come and go. Cities that attract new businesses, have low crime rates, a metro population over 1 million (for infrastructure and skilled labor), and low operating costs are best positioned to meet this need.

Where to Start Your Search

Evaluating every city in the U.S. isn't practical. Focus instead on cities with metropolitan populations over 1 million that show significant, sustained population growth. This Wikipedia page has the data you need. Smaller cities are typically more vulnerable to economic downturns and market shifts.

After identifying cities that meet these basic criteria, apply the following filters to narrow down your list:

- Low Crime Rates: Avoid cities with high crime rates. Use resources like CBS’s list of the 50 Most Dangerous Cities in America to identify cities to avoid.

- Low Operating Costs: High operating costs erode your profits. Key considerations include property taxes and insurance rates. Resources like ValuePenguin and LendingTree can help you compare your operating costs across cities.

- No Rent Control: Rent control can limit your ability to raise rents, screen tenants, or evict non-performing tenants. Avoid investing in cities with rent controls.

By filtering out cities that don’t meet these criteria, you’ll create a shortlist of potential investment locations for further evaluation.

Remote Investing

Live where you like, but invest where you can achieve lifelong financial independence.

Most investors don't live in cities that meet all the requirements for financial independence. Therefore, the real question isn't whether to invest remotely—it's where and how to do it safely.

Once you've selected a city that meets the requirements, you'll need an experienced local investment team to minimize risk and maximize returns. While books, seminars, podcasts, and websites offer valuable general knowledge, ultimately, you're investing in a specific property in a specific city. This requires deep local expertise. Only an experienced local team can provide the local market knowledge and resources essential for success.

Summary

By following the steps outlined above, you can quickly narrow your focus to cities that support lifelong financial independence. However, if you invest in a city that doesn’t meet these criteria, no number of properties will compensate for the long-term challenges you’ll face.

Post: May Las Vegas Rental Market Update

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

It's May, and it's time for another Las Vegas rental market update. For a more comprehensive look at the Las Vegas investment market, please DM me for a link to our blog. There, you'll find detailed information on investing, both in general and specifically in Las Vegas.

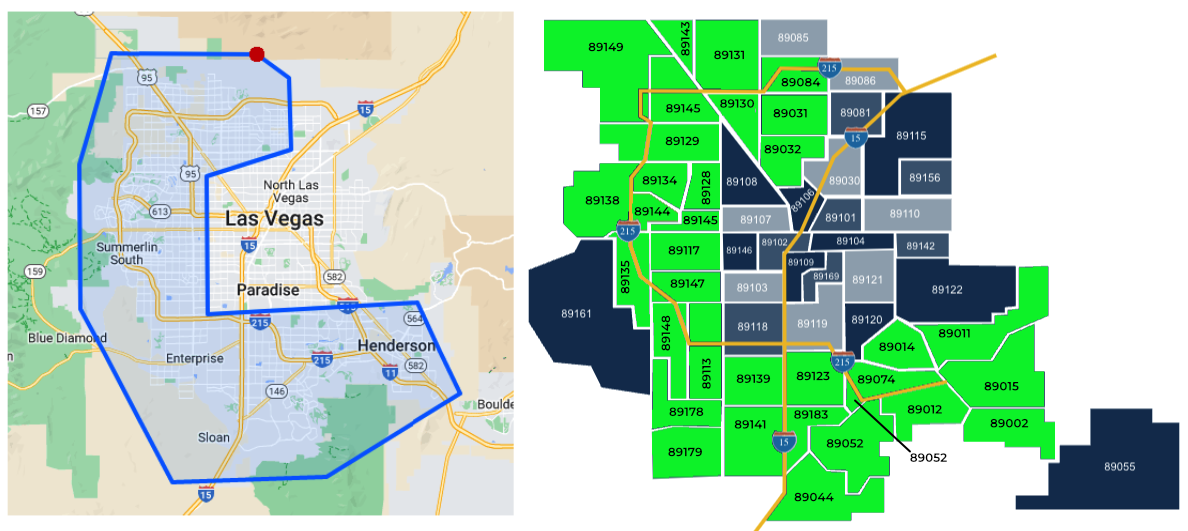

Before I continue, note that unless otherwise stated, the charts only include properties that match the following profile.

- Type: Single-family

- Configuration: 1,000 SF to 3,000 SF, 2+ bedrooms, 2+ baths, 2+ garages, minimum lot size is 3,000 SF.

- Price range: $320,000 to $475,000

- Location: All zip codes marked in green below have one or more of our clients’ investment properties.

Overall market inventory:

The chart below, from the MLS, includes ALL property types and price ranges.

Rental Market Trends

The charts below are only relevant to the property profile that we target.

Rentals - Median $/SF by Month

Rents increased MoM, in line with our expectations. YoY is flat.

Rentals - Availability by Month

The number of homes for rent continued to decrease MoM, in line with our expectations.

Rentals - Median Time to Rent

The median time to rent continued to decrease rapidly in April, now just above 20 days. This is in line with our expectations for this time of year.

Rentals - Months of Supply

Only about 0.9 months of supply for our target rental property profile. This low inventory will continue to pressure up rents.

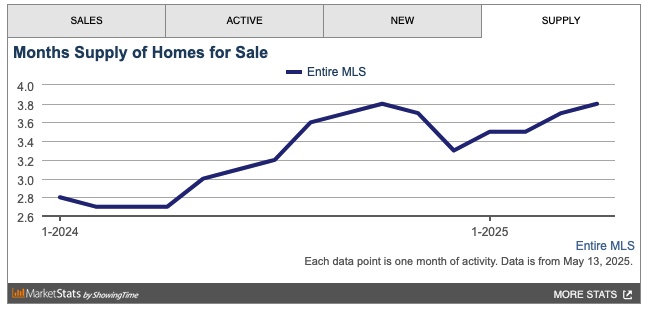

Sales - Months of Supply

There is about 1.9 months of supply for our target property profile. A six-month supply is considered a balanced market. This limited inventory will likely continue to drive up prices.

Sales - Median $/SF by Month

The $/SF had a marginal drop MoM (from $262 to $261), likely due to the tariff effects. YoY is up 6.1%.

Why invest in Las Vegas?

The goal is to achieve and maintain financial freedom. Financial freedom means more than just matching your current income—it's about sustaining your lifestyle permanently. To accomplish this, you need income growth that exceeds inflation. Without this growth, you won't be able to keep up with the rising costs of goods and services.

What causes rents (and prices) to increase?

Supply & Demand

Unlike financial markets, real estate prices and rents are driven by supply and demand. What is the supply and demand situation in Las Vegas?

Supply

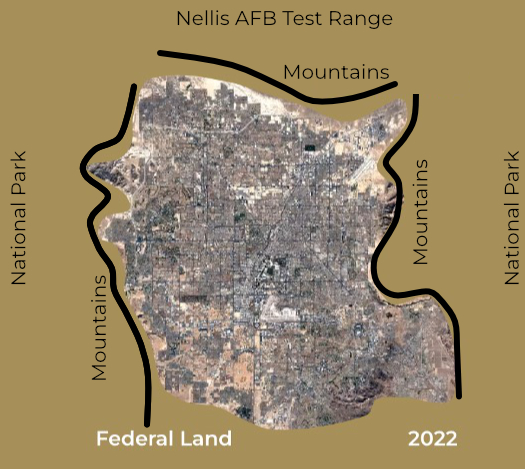

Las Vegas is unique because it is a tiny island of privately owned land in an ocean of federal land. See the 2022 aerial view below.

Very little undeveloped private land is left in the Las Vegas Valley, and desirable areas cost more than $1 million per acre. Consequently, new homes in these locations start at $550,000. Homes that appeal to our target tenant segment range from $350,000 to $475,000, so the supply of housing we target remains almost the same regardless of how many new homes are built.

Demand

Population growth drives housing demand and price and rent increases. Las Vegas's average annual population increases by 40,000 to 50,000 per year. What attracts people to Las Vegas? Jobs. Ongoing construction projects valued between $26 billion and $30 billion fuel employment opportunities. The most recent job fair featured over 20,000 open positions.

In Conclusion

While nothing is guaranteed, the combination of population growth and limited land for expansion virtually assures that prices and rents will continue to increase.

Thanks for reading my post. Reach out if you have questions or would like to discuss investing in Las Vegas.

Post: How do you manage properties that are hours away?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Christopher Carrese Gougeon,

Whether your property is next door or across the country, you simply cannot afford to manage it yourself.

Many landlords mistakenly believe that a property manager's only value is collecting rent. While rent collection is important, it's just one small part of their essential services. Here's what truly matters:

- Tenant Screening: The single most important service a property manager provides is selecting reliable tenants. Most issues can be avoided by not putting a problem tenant in the property. If you think you can handle it yourself, watch the movie Pacific Heights. There are many people who cruise sites like Craigslist and others looking for privately managed rental properties. These people know they can take advantage of you, and they will. However, they know they are very unlikely to pass screening by an experienced property manager and will just look for an easier target.

- Property Marketing: Property managers have access to multiple listing services, which feed popular real estate sites such as Zillow, Redfin, Realtor.com, etc. They can give the property a much bigger market exposure than an individual landlord can.

- Compliance: Property/tenant laws are complicated and change frequently at every level, federal, state, county, and city. Only a skilled property manager keeps you compliant, often through organizations like NARPM. One mistake could land you in court.

- Cost Management: Small repairs can become costly headaches without the right vendor relationships. Property managers have buying power and trusted vendors, saving you time and money. You are just one low-dollar nuisance to most service people.

- Lease Enforcement: Many tenants will push boundaries. A strong property manager enforces leases and handles difficult situations professionally, saving you from potentially expensive litigation.

- Rent Collection: It's not just about receiving payments. Good property managers have processes in place to act immediately when rent is late, which helps educate tenants and protect your cash flow.

Even if your rental is next door, can you truly handle all these responsibilities? Even creating a compliant, enforceable lease is a challenge unless you’re deeply involved with professional organizations.

Do I manage my own properties? My team has delivered over 560 investment properties. I currently own five myself, with the farthest one just five miles from my house. Even though they're close, I simply can't afford the time and risk to save on property manager fees. One bad tenant can cost you more than years of property manager fees.

Summary:

The money you think you'll save managing your own property isn't worth the liability, hassle, and risks. You simply can't afford to do it yourself, no matter where your property is located.

Post: Am I wasting time looking for a “perfect” market?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Jackie Mcmorrow,

You did a great job on the criteria you specified. The city you choose to invest in IS your most important investment decision. The city defines whether you can maintain lifelong financial independence. Below are some considerations (not in any order).

Landlord-Friendly Laws

Never invest in any cities or states with rent control or restrictive rental regulations. These can make selecting performing tenants, evictions, and rent increases nearly impossible, jeopardizing your ability to maintain profitability.

Lifelong Income

Initial cash flow only predicts initial return under ideal conditions. Financial independence requires rent growth and appreciation that outpaces inflation. Growing markets with higher property prices may offer lower initial cash flow, but their rent growth typically outpaces inflation, enabling lifelong financial independence.

Jobs

An investment property is no better than the jobs your tenants have. For your income to last a lifetime, your tenants must remain employed at similar wages. Since companies have limited lifespans, only invest in cities that attract new businesses that will create the replacement jobs. Look for cities with:

- Low crime rates

- Metro populations over 1 million (for infrastructure and skilled workers)

- Low operating costs.

- Business-friendly regulations

Tenant-First Approach

No property pays rent—tenants do. To have a reliable income, you must have reliable people in your property. A reliable person stays for many years, pays rent on schedule, and takes good care of the property. These people are the exception, not the norm. Work with property managers to identify properties that attract reliable tenants. Then, buy properties similar to what they rent today. Selecting a property first and hoping for good tenants is a risky approach.

Renovation Considerations

Study comparable properties that rent quickly at full market value and make only the necessary changes. Your personal preferences don’t matter—focus solely on upgrades that increase rent or reduce vacancy time.

Summary

By focusing on these criteria, you’ll build a portfolio that supports lifelong financial independence.

Post: Realistic expectations for minimal effort?

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Thomas Slifka,

The best way to save time, reduce risk, and maximize your return is by working with an experienced local investment team. In other words, your best bet for hands-off investing is through a good team. Here’s how to find and qualify the right team.

Start with an Investment Realtor

Unlike residential (or “investor-friendly”) realtors, who focus on buying and selling homes, investment realtors specialize in income-generating properties. They provide the information you need, including:

- Price and rent ranges based on ROI goals

- Tenant demographics

- Area rent growth and appreciation trends

- Cash flow, ROI, and renovation cost estimates

- Local rent restrictions

Investment realtors are always part of a team because no one person can know it all. Investment realtors work closely with property managers and renovation experts, ensuring you have a team with the expertise to handle every aspect of your investment.

Finding an Investment Realtor

To start, compile a list of potential candidates from sources like the following:

- Real estate investing platforms like BiggerPockets

- Local property managers and investors

- Real estate brokers, Google searches, and meetups

How to Evaluate Candidates

Once you’ve identified potential realtors, interview them using these key questions:

- Do you have an investment team? They must be part of an investment team, or they bring little to no value.

- Do you own investment properties? Unless they are investors, they will not understand what you need to be successful.

- How many investment properties have you closed in the past year? Look for at least 12.

- Who selected the properties? Reject candidates who rely on clients to select properties.

- What criteria do you use for property selection? Expect data-driven answers, not opinions.

- What tenant pool do you target? They should demonstrate knowledge of tenant behavior and demographics.

- What’s the average tenant stay? Look for specifics—e.g., “Our tenants stay over five years.”

- How do you estimate rent and time to rent? Answers should reflect recent, comparable rentals, not unreliable online estimation tools like Zillow and Rentometer.

- What’s your renovation process? They should collaborate with property managers and contractors.

After each interview, assess their honesty, expertise, and whether you feel comfortable working with them. Adjust your questions as needed, and if they check all the boxes, you’ve likely found the right partner.

By following this process, you’ll build a team that minimizes your time and risk and maximizes your returns.

Let me know if you would like any details for the above. I had to be as brief as possible to keep the post at a reasonable length.

Post: newbie trying to learn about markets

- Realtor

- Las Vegas, NV

- Posts 804

- Votes 1,557

Hello @Marisa Opp,

Selecting the right investment city is crucial for achieving financial independence. Financial independence isn't a one-time event or a fixed amount—it requires an income that meets multiple characteristics, which are defined by the city where you invest. Below are two such characteristics.

- Rents outpace inflation: Your rental income must increase faster than inflation to cover rising costs. Cities with significant and sustained population growth are likely to meet this requirement.

- Lifelong income: Your income must last a lifetime, which depends on tenants maintaining employment at similar wages. Since companies have (relatively) short lifespans, tenants will need replacement jobs multiple times over your (property) hold time. Cities that attract new companies have low crime rates, a metro population over 1 million (for solid infrastructure and skilled worker pool), and low operating costs (such as low taxes and less regulation).

Evaluating every potential city is impractical, so use elimination filters:

- Population Growth: Start with cities having a metro population over 1 million and consistent and significant growth. Wikipedia

- Low Crime: Avoid cities on this list: CBS: The 50 Most Dangerous Cities in America.

- Low Operating Costs: High operating costs can turn a profitable property into a money pit. Consider property taxes and insurance. Insurance - ValuePenguin, Metro Property Taxes - LendingTree

- No Rent Control: Rent control may prevent you from increasing the rent fast enough to keep pace with inflation. It may limit your property manager's ability to select the best tenant. It may make evictions of non-performing tenants difficult or impossible. Never invest in any location with rent control.

- Local Investment Team: While general knowledge from seminars and books is helpful, local expertise is crucial for specific purchases. Only an experienced local investment team can provide the resources and knowledge you'll need.

When you filter out all the cities that do not match all the above requirements, you will have a shortlist of cities for further evaluation.