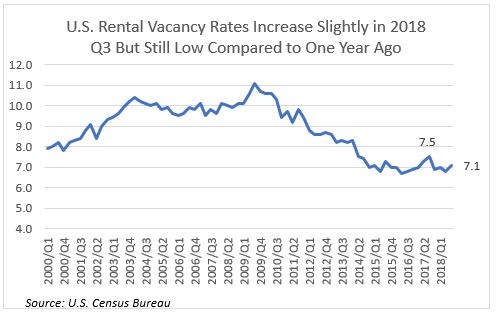

The U.S. rental vacancy rate edged slightly higher to 7.1 percent in 2018 Q3, but this is still below the 7.5 percent vacancy rate in 2017 Q3. The U.S. rental vacancy rate averaged 9.6 percent from 2000 Q1 through 2011 Q4, so rental vacancy rates are still trending below historical levels. Low vacancy rates indicate that the multi-family real estate market still has a growth potential in several metros in 2019.

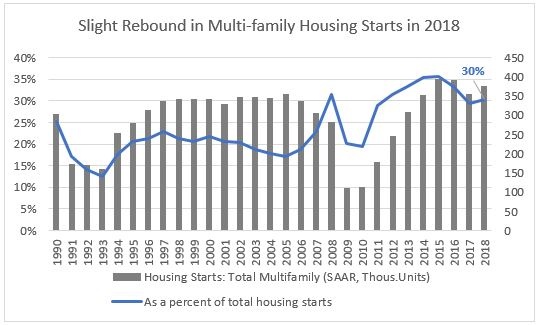

Multi-family housing starts appeared to have rebounded in 2018. Multi-family housing starts fell to 376,000 in 2017, or 29 percent of housing starts, but rose again to 376,000 units in 2018, accounting for 30 percent of total housing starts of 1.245 million. The construction of multi-family housing peaked during 2015 and 2016, with multi-family housing starts of 393,000/394,000 units on a seasonally adjusted annualized rate (SAAR) basis, accounting for 36/33 percent of total housing starts (1-family and multi-family) in 2015/2016.

Multi-family housing starts fell to a seasonally adjusted annual rate of 320,000 in December 2018, as housing starts in the West Region declined by about half from 127,000 (SAAR) to 62,000 (SAAR). However, the drop in December 2018 housing starts should not be taken as an indicator of a long-term trend steep fall in multi-family housing starts, given that the housing authorizations (permits) rose 27 percent in December 2018 to 176,000 from 139,000 in December 2017.

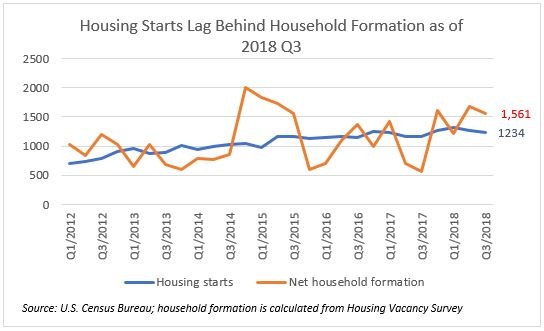

The demand for both multi-family homes (usually apartments for rent) and 1-family units (usually for home purchase) is expected to remain strong because housing construction for 1-family and multi-family units is still behind the demand arising from household formation and demand for replacement housing. As of 2018 Q4, seasonally adjusted annualized level of housing starts totaled 1.17 million, while building permits totaled 1.30 million, both of which are below the 1.5 million net new households were formed during November 2017- September 2018, according to data from the U.S. Census Bureau’s Current Population Survey. In addition, there is demand for about 400,000 to 500,000 housing units to replace damaged or lost housing stock.[1] So supply is still broadly behind demand for both 1-family and multi-family units, though the tightness of supply varies across metro areas.

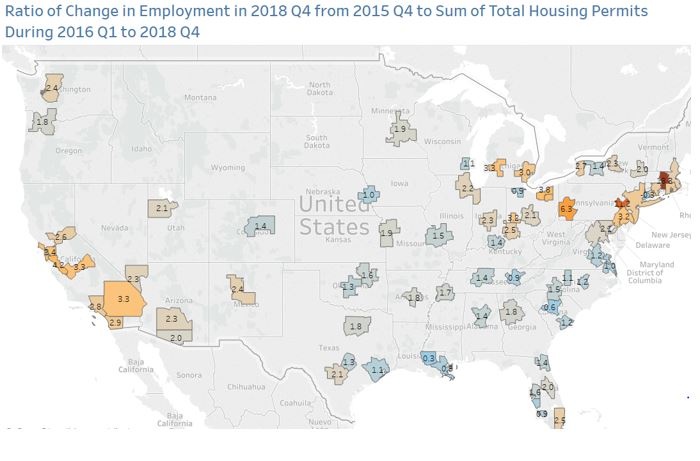

Supply for both 1-unit and multi-family homes is tight in many of the 75 largest metros. Over the past three years, the ratio of the number of payroll employment created in 2018 Q4 from 2015 Q4 to the total number of 1-family and multifamily housing permits issued during 2016 Q1 – 2018 Q4 has exceeded the ideal ratio of two. In Worcester, MA, there were 18 jobs generated for every housing permit issued during the past three years. In Pittsburgh, PA, there were about six jobs per housing permit issued. Total housing starts lag behind job creation in many California metro areas: San Jose-Sunnyvale -Sta. Clara, CA (4.2); San Francisco-Oakland-Hayward (3.4); Riverside-San Jose-San Bernardino (3.3); Fresno, CA (3.3); San Diego-Carlsbad (2.9), Los Angeles-Long Beach-Anaheim (2.8); and Sacramento-Roseville-Arden-Arcade (2.6).

Multi-family market investment potential in 2019?[2]

Among the largest 75 metro areas[3],vacancy rates are less than five percent and declined in 2018 Q1- Q3 compared to one year ago, indicating significant potential for multi-family commercial investment: Fresno, CA (1.9%); Worcester, MA (3.0%); Cincinnati, OH-KY-IN (3.5%), Denver-Aurora-Lakewood, CO (3.7%), Syracuse, NY (3.8%), Los Angeles-Long Beach-Anaheim (4.0%), Akron, OH (4.1%), Boston-Cambridge-Newton, MA-NH (4.1%), Portland-Vancouver-Hillsboro, OR (4.3%), New York-Newark-Jersey City, NY-NJ-PA (4.6%), Tucson, AZ (4.8%), and Riverside-San Bernardino-Ontario (4.9%).

In the large California and Washington metro areas, vacancy rates have eased, though they are still low —indicating an opportunity for multi-family commercial investments: Seattle-Tacoma-Bellevue (4.7%), San Jose-Sunnyvale-Sta. Clara (4.6%), Sacramento-Roseville-Arden Arcade, CA (3.3%), San Francisco-Oakland-Hayward, CA (5.5%).

In some metro areas, vacancy rates have dropped significantly in 2017 Q1- Q3 indicating that a fast absorption of apartments for rent and strong growth potential for multi-family investment if rates continue to fall. The large drops in vacancy rates in these metro areas indicates a potential for more multi-family investments also if vacancy rates keep falling in the coming months: Birmingham-Hoover, AL (12.3%), San Antonio-New Braunfels, TX (7.2%), Pittsburgh, PA (6.7%), and Kansas City, MO-KS (7.3%).

Vacancy rates are nearing or around 7 percent and are higher compared to one year ago in several “hot” metro areas, indicating a maturing of the investment cycle in these markets given the current level of demand: Dallas-Fort Worth-Arlington, TX (7.1%), Austin-Round Rock, TX (7.1%), Miami-Fort Lauderdale-West Palm Beach, FL (7.1%), Washington-Arlington-Alexandria, DC-MD-VA-WV (6.7%), and Raleigh, NC (7.3%).

Vacancy rates are above 10 percent in these areas and were higher compared to the levels on year ago, indicating low potential for multi-family investment given the current pace of demand: Albany-Schenectady-Troy (10.3%), Greensboro-High Point, NC (10.5%), Tulsa, OK (8.1%), Little Rock-North Little Rock-Conway, AR (11.5%), Toledo, OH (12.6%), Dayton, OH (12.7%) and Oklahoma City (13.1%). These metro areas also have a ratio of jobs to permit to less than 2.

Source: US Census Bureau rental vacancy rates for the 75 largest metro areas, downloaded from Haver Analytics