How and why NNN construction loans go up to 100% LTC

A commercial mortgage for construction (construction loan) at 100% Loan-to-Cost (LTC) covers both hard and soft construction costs in full, meaning the developer doesn’t need to put any of their own capital to work. It’s a dream scenario for sponsors (borrowers) that do not have the capital to invest in the project themselves (or don’t want to put their money to work), but have the right experience and capabilities to execute on the vision of a new development deal. These days high LTC construction deals aren’t super common, and getting a construction loan at all takes a strong plan from an experienced developer/sponsor.

But there is a class of construction loans going all the way up to 100% LTC, and that’s construction with an in-place NNN lease for the completed building. If you’re not familiar with the NNN lease investment structure, read our previous blog post here.

How to get 100% LTC?

There are a few private construction lenders who specialize in underwriting this type of NNN financing. The first step in getting 100% LTC from them is to arrange the construction deal with a suitable tenant, with a solid NNN lease. The lease should allow the developer to bill all real estate costs back to the tenant once the property is ready to be occupied. The three N’s charged to the tenant are property taxes, property insurance, and maintenance, in addition to the monthly base rent.

With the tenant promising to pay all the occupancy costs in NNN fashion, the developer can then show the lease and the construction budget to the lender in order to request a quote on construction financing. The lender will underwrite the strength of the tenant, examine the experience of the developer, and scrutinize the construction budget. If all three check out, they will issue a term sheet up to 100% LTC.

Why does the tenant do it?

If the real estate deal works for the developer, why doesn’t the tenant cut out the “middle man” and develop the property for themselves? A few reasons:

- The tenant will usually lack of development expertise of building suitable real estate.

- The tenant can usually achieve a higher return on their time and money through their core business.

- Leasing real estate rather than owning may put the tenant in an advantageous tax position.

Why does the lender do it?

So why would the lender risk offering up to 100% of the construction cost?

- Safety of a “bankable” tenant locked in through the NNN lease.

- Receive higher interest rates than loans on most in-place properties.

- The leverage point is reasonable upon completion.

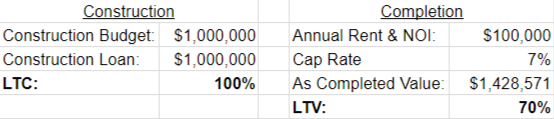

To illustrate that last point, let’s use an example. Let’s assume it will cost $1,000,000 to develop a particular property for a national restaurant chain, and that upon completion, the tenant will be paying $100,000/year in rent, and covering all taxes, insurance, and maintenance on the property:

Note that the Rent number here is pulled straight into Net Operating Income because the tenant is paying all expenses.

So it’s actually the negotiation of the strong lease relationship with a quality tenant and the ability to execute on the real estate development that the developer brings to the table here. If you’re able to get both in place, the deal should be able to achieve a very high LTC, sized up by as-completed value.

In completing 10 locations for a net-lease client, I had maxed out my two $5 Million community bank lines. When the client called and asked that I purchase an additional 9 properties by year end, I was definitely worried about finding additional financing, and was tapped out on equity.

As luck would have it, I came across StackSource, reading online that it gives developers like myself the “upper hand” when it comes time to raise capital for their projects. With my client relationship on the line, I reached out. Within a few days, I was connected with a private lending group that presented us with a 100% LTC term sheet.

We ended up closing 9 deals with a total project value of ~$9 Million in less than 60 days. More importantly, I was able to do it without bringing on an equity partner. If I had not read that article <about StackSource>, I most likely would have an equity partner to answer to, as well as lost my preferred developer status with my client.

- Anderson Jarman, Jarman Development Group

Learn more about the availability of construction financing on your deal by chatting with a StackSource Capital Advisor, or submit your loan request now.

Comments