Don't rush into that long-term, fixed-rate commercial loan

The 10-year, fixed rate commercial mortgage is a beautiful thing. When buying or refinancing a commercial asset you have a good sense of the asset’s value and cap rate, and in a period like this where we’re still seeing historically low interest rates, not needing to worry about interest rate risk for a full decade provides serious peace of mind.

But don’t rush into it, because it’s not right for every deal.

I’m looking at you, value-add investor. One of the most common mistakes we see in the market is a multifamily investor looking for 10-year fixed rate financing, and describing the deal as a “value-add”. It’s a simple issue of managing your leverage point and avoiding costly prepayment penalties.

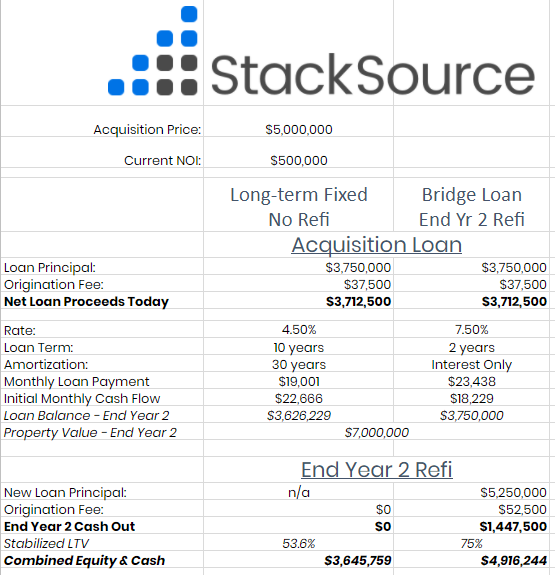

The math

Let’s say you’re looking to acquire a property at $5,000,000, but you think you’ll be able to make some adjustments, raise rents, and raise the value to $7,000,000 within three years.

If you take a long-term, fixed rate loan at 75% LTV on day one, that loan will only represent 54% LTV at stabilization. Can you refinance your fixed rate loan at year three to raise your leverage? Maybe, but there’s often a prepayment penalty that will hurt your returns in that scenario. Taking out a mezz loan at that time may be no better, as mezz loans typically come in at 10%+.

The art

Putting aside the math, if you’re working on a significant value-add and the property’s current financials aren’t strong, other reasons to skip the bank for your first loan are speed and certainty of execution. Closing a bank loan typically isn’t quick — if you’d like to move more quickly and with less red tape on your heavy value-add, closing with a private bridge lender might be the ticket.

Sure — a stabilized multifamily investment could rise in value too, so any loan ideally falls as a percentage of property value closer to maturity. But if the point of the transaction is to add significant value in the short term, then you should be seeking capital to match that goal.

Comments