Strengths & Weaknesses of Your Appraisal Department

A famous quote from Saint Augustine reads, “The higher your structure is to be, the deeper must be its foundation.” While Augustine wasn’t exactly speaking of the appraisal process, your financial institution, or AMCs, he does make a valid point that we can all relate to. In order to truly be great you must start with the foundation of your company, and that means analyzing the strengths and weaknesses of your appraisal department.

KNOW WHO DOES WHAT.Evaluating the structure of your appraisal department can help identify things you do well as well as things you need to improve upon. The first step we suggest you to start with is paying close attention to your loan production staff. These are your people who are out in the field drumming up business. For regulatory purposes, it’s imperative that you separate your loan production staff from your appraisal processes. This ensures that your appraisers are operating independently from loan production and with clean motives. It also verifies that those two pieces of your puzzle properly fit within regulatory guidelines.

UNDERSTAND HOW EVERYONE GETS PAID.Along the same lines of knowing who does what, make sure that you understand your appraisers’ day to day function as well as the roles of your loan production staff. You not only need to understand what these two jobs do, but also how these two individual roles get paid. We recommend looking at anyone who has a bonus plan, a compensation plan, or a commission plan that has anything to do with how and when loans get approved or the appraised value. If their compensation is related to loan approval or value, then they are a part of your loan production staff.

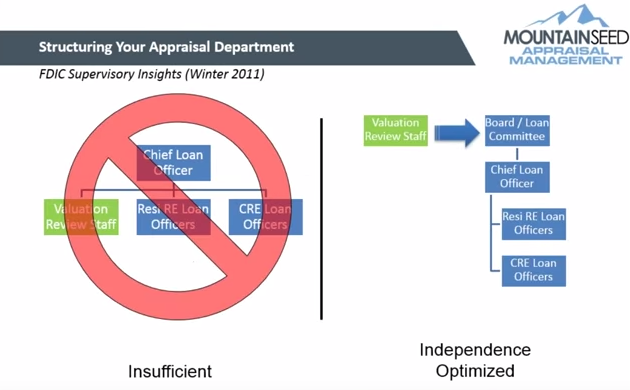

BE SMART ABOUT YOUR FINANCIAL INSTITUTION’S STRUCTURE.The FDIC recommends (and for all intents and purposes, requires) that your valuation review staff should report directly to your board or loan committee or your Chief Loan Officer. From there, your Resi RE Loan Officers and your CRE Loan Officers will follow. You should be able to look down or up any structure and determine who might be loan production staff.

While the regulators have said that for smaller financial institutions there might be a small break with these rules, the reality is that it’s better to be safe than sorry. If your bank or institution has less than 50-75 million in assets, than you can breathe easy. If you have more than that, say around 250 million in assets, we suggest that you have pure separation of the reporting line.

ALLOW SERVICE LEVELS TO GUIDE YOUR STRUCTURE.If you could always predict the number of new loans and new appraisals each month, life would be so much easier. Unfortunately, new customers don’t spread themselves out evenly and seasonality in lending can also make things more complex. Because of this, you may have times with an internal appraisal department that is either overworked or underutilized. In the former situation, lenders are frustrated because it takes too long to get an appraisal review completed. In the later, you have too much staff for the small number of appraisals. Outsourcing this function allows you to use an AMC only when you need to, turning a fixed cost into a variable cost and maintaining appropriate service levels at all times.

If ultimately you decide to keep your appraisal department in-house, make sure that you understand all of the changing regulations regarding banking and appraisal legislation. An internal department can be great for tackling orders, but it rarely makes sense for a financial institution to have all of the management level staff required for ensuring compliance for both banking and appraisals. At MountainSeed we have a compliance officer that tracks state and federal regulations, a Chief Appraiser that has major bank experience, and senior review staff that helps our clients with compliance. None of these team members do reviews, but they are critical to a successful appraisal department, and most banks or credit unions can’t justify that type of overhead expense.

A good alternative? Some banks choose to have internal staff and use an AMC’s appraisal review services as a supplement to their internal staff. This can either be to outsource 20% or so of the reviews to be able to compare quality against internal staff, or to manage the fluctuations in volume and seasonality. Whatever you choose to do, make sure that you are structuring your team for success and building a strong foundation for appraisals and beyond.

For more information on this topic, take a look at our recent webinar.

Comments