Sign #4: Does your appraisal process lack efficiency?

In case you’re just tuning in, we’ve been covering the top signs your team is stretched too thin. These signs can go unnoticed for far too long, so we wanted to pinpoint the top areas that might be affecting your team’s efficiency. The first few signs of an overworked team could be due to under-qualified reviewers, unpredictable appraisal report turn times, and not staying up to date on the latest financial regulations. Now it’s time to see if your bank or credit unions’ appraisal process is working as efficiently as it should be. Put it to the test with the following five questions:

Question 1: How do you manage your appraisal process?

Many financial institutions choose to handle their appraisal process internally. If your department falls in this bucket, it’s crucial that you take the necessary steps to ensure your process is both efficient and effective. Review the following tips to determine whether your process is running the best it possibly can be.

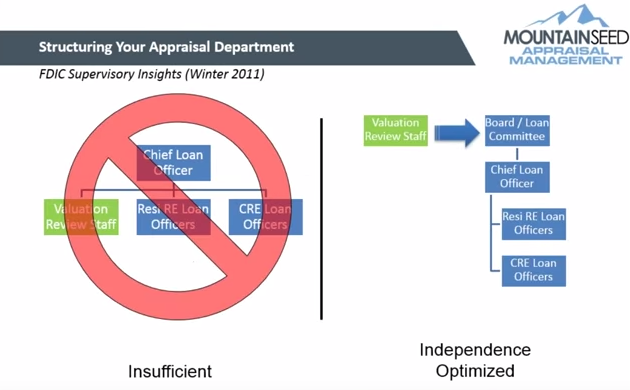

Tip 1: Review your department’s appraisal independence

Separating your appraisers from your loan production staff is a must in order to ensure that your department is working ethically and operating according to regulations. According to the FDIC, your valuation review staff should report to your board or loan committee or your Chief Loan Officer, and your Resi RE Loan Officers and CRE Loan Officers should follow suit.

Understanding how appraisers and loan production staff are paid will help you determine whether your department is properly separated. Any employee who has a bonus, compensation, or commission plan related to loan approval or value is part of your loan production staff.

Tip 2: Embrace the freedom of automation — Spend less time on email, Word, and more time focusing on your customers

Though on the surface it may seem inherently efficient to run order and review processes in-house, it can quickly result in a series of inefficiencies that clog up an appraisal process.

Even if your process is run internally by real estate experts, that doesn’t mean it’s efficient. Internal processes are a lot more time-consuming and manual than they may initially seem. If your current process looks a little something like this, it might be worth taking another look and seeing where you can create efficiencies:

- A Credit Analyst, Loan Assistant, or underwriter receives an appraisal request from a lender through a Word document attached to an email.

- Depending on the type of appraisal, the person handling the appraisal process either assigns it to a local market residential appraiser or bids it out to a commercial appraiser.

- The processor cross-references their request to an appraiser list (often in Excel) and then emails it to appraisers on their panel.

- If it’s a commercial appraisal report, the processor sends and tracks responses for three separate emails.

- The processor then emails the bids back to the lender, making sure to promote appraisal independence by removing the appraiser’s name and contact information.

- The lender emails the processor with their winning bidder selection.

- The processor creates an engagement letter to be signed by all parties in a Word document and emails the appraiser with the notice that they have been assigned or awarded a bid.

- At this point, commercial appraisals tend to enter a 10-20 day black hole of little communication between the appraiser, processor, and lender. This lack of communication can result in a nasty surprise if the deadline approaches and the appraiser hasn’t completed their work.

…That’s a lot of reliance on email, Word, and Excel, and a lot of opportunities to be more efficient.

A 2012 review by a large bank estimated that 85% of a bank’s processes could be at least partially automated. In this increasingly digital industry, automating some steps of your process just makes sense. Automation can free up some of your appraisal staff’s precious time by taking away the amount of time they’re spending on mundane tasks and giving them more time to complete reports and help customers.

Investing in current tech and automation will give your institution a competitive advantage. By keeping everything in one place (instead of making your staff hop around between email, Word, and Excel) and offering faster features like digital signatures, automation will make the appraisal process more efficient for you and your customers.

But… that doesn’t mean that automating your appraisal process magically fixes everything. Automation created without thought will only lead to more ineffective processes. Your automation will only ever be as good as the processes and people behind it.

Tip 3: Track everything — You can’t improve what you can’t measure

Running your internal process manually means you have no clear idea of how much time any part of your process takes. You can estimate all you want, but you still won’t have exact data on average response and review times.

Setting up a proper software system will help your department track every part of the appraisal process. Not only will that grant processors a more realistic idea of response times, but it will also allow your team to provide lenders with a more accurate timeline of when appraisal reviews will be completed.

Access to accurate data will also show crucial feedback on process bottlenecks and identify exactly where your department’s process can improve. After all, you can’t improve what you can’t measure!

Are your internal reviewers on top of everything?

Time and time again, clients and prospects have told us that they’re kept up at night by the question, “Are my internal reviewers actually catching everything they’re supposed to?” If they weren’t, would you know?

Departments with internal processes need some source of internal quality assurance program to test processors. Better that a gap in the system be caught now by you than later by a borrower, lender, or — worst-case scenario — a regulator.

Question 2: How many people are on your staff?

One way to determine whether your staff is working efficiently is to analyze your department’s deal volume, or how many reviews your team can complete per day.

The number (and type) of appraisers on your staff should depend on the number of deals your department typically handles. Residential appraisers can complete more reviews per day than commercial appraisers. Depending on the complexity of the deal, commercial appraisers could do anywhere from a half a review to three reviews in a day.

Question 3: What's your staff's salary range?

Appraiser salary ranges vary widely depending on factors like experience, location, and level of education. In February 2017, the median annual residential appraiser salary was $50,530, and the median annual commercial appraiser salary was $93,744.

If you’re working with a small team, it may be worth looking into an AMC instead of hiring another full-time appraiser. Here at MountainSeed, we work with retired or appraisers working on the side, who can be more competitive on salary.

Question 4: What's the cost difference?

It can be hard to predict when your department will see spikes and valleys of new customers, especially when working with seasonality in lending. This may leave you with a staff that varies wildly between overworked and underutilized.

While your staff is a variable cost, appraisal management companies like MountainSeed are a fixed cost. Financial institutions shifting from an internal process to an external process with MountainSeed report that they see no budget impact — and sometimes even see budget savings. That’s because nearly all of the 300-400 community banks and credit unions we serve pass our fee along to the customer as part of the closing process, which means you don’t have to bear our cost on your balance sheet.

Question 5: Would hiring an appraisal management company make your appraisal process more effective?

Internal departments can deftly knockout appraisal reviews, but many times it doesn’t make sense for banks and credit unions to have a full management staff that oversees compliance for banking and appraisals. In order to succeed, appraisal departments must have staff dedicated to tracking and complying with updated regulations. To help clients with compliance, MountainSeed has a compliance officer, a Chief Appraiser, and a senior review staff.

Some financial institutions choose to use AMCs to supplement their internal staff. Depending on your department’s needs, this could either mean outsourcing part of your appraisal reviews to compare the quality against your own internal staff, to managing fluctuations in volume and seasonality, or both.

Were you able to spot a few areas where you could improve? We’d love to hear from you and help answer any questions you might have. If you’d like to help your team even more, download your copy of this ebook to know in advance when your team is getting stretched too thin.

Comments