The Power of 72: Prepare for Retirement by Making Money Work for You

I first heard of the rule of 72 at my local County Chapter REIA monthly meeting. We had a guest speaker from a local Self Directed IRA Company, NuView IRA. I was excited to hear his presentation because I love hearing new ways to shelter and grow my wealth using alternative methods such as solo 401Ks and Self Directed IRA's. During his speech he showed us a very odd-looking chart that had the numbers 1 - 65 on them. There were 7 consecutive squares of the chart blocked out in white instead of the bold blue color of the remaining 58 blocks. He began to explain what we were looking at and the "Rule of 72", a simplified method that helps you determine the amount of time that would be needed to double your investment (72/interest rate = time to double).

I first heard of the rule of 72 at my local County Chapter REIA monthly meeting. We had a guest speaker from a local Self Directed IRA Company, NuView IRA. I was excited to hear his presentation because I love hearing new ways to shelter and grow my wealth using alternative methods such as solo 401Ks and Self Directed IRA's. During his speech he showed us a very odd-looking chart that had the numbers 1 - 65 on them. There were 7 consecutive squares of the chart blocked out in white instead of the bold blue color of the remaining 58 blocks. He began to explain what we were looking at and the "Rule of 72", a simplified method that helps you determine the amount of time that would be needed to double your investment (72/interest rate = time to double).

"The most powerful force in the universe is compound interest" - Albert Einstein

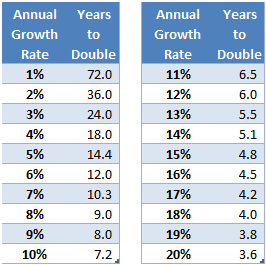

The 7 white blocks on the chart he showed us was demonstrating the doubling period or 7 years time it would take to double your money if you were receiving a 10% interest rate, which let's be real - the average person is nowhere near receiving. The point of the chart was to emphasize how important time is when investing money. With that being said, your age can greatly affect your ability to double your money or not. The chart below should give you a better idea of that timeline.

So let's give an example. If you are 25 and you are receiving a 5% interest rate on the $100,000 you have in your IRA (which is a higher than average rate of return, even for investing in stocks/mutual funds). That means it would take you 14.4 years to double your money and you would have $200,000 in the IRA by the time you are 39. If you did nothing additional to the money and continued to receive that 5% interest rate, by the time you were at retirement age (65) you would have around $775,000 in your IRA. That's not a bad amount of savings if you have a good pension plan with benefits from your previous employer. If you have no additional pension plan; with the average life expectancy rate rising, you will be living on a $51,000 year salary that will disappear at the age of 80 (15 years from retirement).

Can you imagine what your rate of return would be if you started with $100,000 at 5% interest at the age of 45, or 55...You're ability to double your money is greatly diminished in return affecting your ability to retire at the age you desire.

So what's the solution?

To be honest, there is none; but there are ways that you can grow your wealth at a much faster rate than the annual contribution limit (which is $5,500 for anyone under the age of 55) or from putting your money into a savings account (current national average 0.21%), CD (5 year CD average 1.34%), or Mutual Fund/Stocks (current average yield 3.4%).

A Self-Directed IRA (SDIRA) is similar to a traditional IRA with the exception that you as the individual owner are allowed to choose and direct what investments you would like to pursue with your IRA such as real estate, gold, promissory notes, and even limited liability companies (LLC) or partnerships while receiving the traditional tax benefits such as tax deferment and even tax-free growth within your IRA.

A Self-Directed IRA (SDIRA) is similar to a traditional IRA with the exception that you as the individual owner are allowed to choose and direct what investments you would like to pursue with your IRA such as real estate, gold, promissory notes, and even limited liability companies (LLC) or partnerships while receiving the traditional tax benefits such as tax deferment and even tax-free growth within your IRA.

When used properly, SDIRA's can be an incredible vehicle for building wealth inside your retirement plan although there are regulations when using a Self-Directed IRA that should be closely followed and understood prior to making any investment decisions (you can see some of those rules and regulations by clicking here).

Our company, Seasoned Funding, LLC is a privately funded real estate investment company that works with private individuals who often have money sitting idle in IRA accounts, 401Ks, or even saving accounts. After becoming an approved investor, we assist the individuals in the process of rolling over their current IRA or 401K into a Self-Directed IRA. We then form a LLC or partnership with their SDIRA and invest in various forms of real estate such as residential and commercial properties and/or promissory notes. We give the individuals the opportunity to build their wealth at a much faster rate by giving a higher than average rate of return on investment and it's all done legally, passively, and tax deferred or tax-free. The IRA owner can make their annual contribution while putting their existing IRA money to work with a higher annual rate of return. The chart below is a great demonstration of how we work with SDIRA's (click on it to make it larger);

There are endless ways to build your wealth using solo 401K plans or Self-Directed IRA's. There is no need to fear retirement when you can learn alternative methods for investing and can take control of your future. Check out our website to see how we are getting higher than average rate of returns for our partners.

*This is not an offer to purchase or sell securities. This overview is for informational purposes only and is not an offer to sell or solicitation of an offer to buy any securities, and may not be relied upon in connection with the purchase or sale of any security. Interest in the fund, if offered, will only be available to parties who are

Comments