FHA Refinance: A Blessing in Disguise

FHA Refinance Letter 2010-23. Ever heard of it? You may have heard of the act on the news or from a fellow colleague or friend, but most likely you aren't aware of the benefits it can have for you as a non-performing note investor.

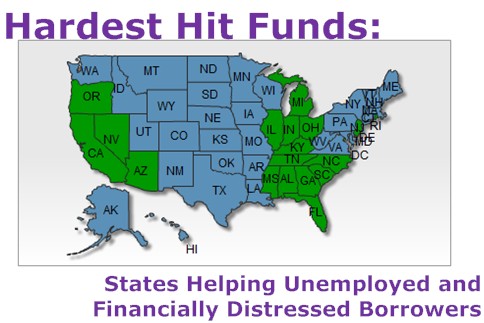

The FHA Refinance Letter 2010-23 was enhanced as a part of the "Hardest Hit Funds" in March of 2010 to continually assist homeowners who had negative equity in their homes find relief. The new enhancement was passed to better assist the borrower in maintaining ownership of the property through a loan modification. Currently, 18 of 50 states are eligible to receive federal aid as a part of the hardest hit funds. The 18 states were originally allocated 7.6 billion to assist in this process and have since used roughly 11% of those funds. That means from today to 2017 (the end date for HHF) they need to allocate an additional 6 billion dollars. Now, with that being said, each state varies in requirements, but if you have a NPN in one of the states the opportunity could a be perfect way to cash out quick!

The modification requires the lender to give a minimum of 10% loan forgiveness. In addition, it requires the borrower to have a minimum of 3 ledger payments (post modification) and to have not filed bankruptcy within the past 12 months. In addition to the requirements listed above, there are additional requirements that vary from state to state. Although these may not met by all of your borrowers, there are some who qualify.

*If your borrower qualifies, the lender may receive up to 12 months of monthly mortgage payments (including escrowed mortgage-payments), with up-front mortgage reinstatement funds, or funds to pay past due mortgage payments to bring a delinquent first current; these funds are paid directly to the loan servicer/lender. *

What does that mean for you as a non-performing note investor? Think of it as a the hidden gem of exit strategies!

I'll give you an example:

The note has an unpaid balance (UPB) of $150,000. The current market value for the note is $60,000. You purchase the note in a Hardest Hit Eligible state for 50% of the current market value (CMV), which means you're buying the note around $30,000. Taking the 10% loan forgiveness "hit" seems a lot sweeter when you only paid 20% of the unpaid balance (UPB) and you still have $30,000 in equity.

So you've given the 10% discount, and you've been working with the borrower to find a modification that works for them. They've paid three months of continuous payments so you ask them to see if they are eligible for the FHA 2010-23 Refinance program. This means they must fill out a lot of paper work, starting with the "letter". Although it seems like a simple letter, only a few people are legally allowed to have a homeowner fill out and then review it for approval. We use a company like FIC to handle the paperwork, helping us stay compliant and freeing up time to close more deals.

So referring back to my initial example, the original UPB was $150,000. After the 10% loan reduction, the new UPB is $135,000. You paid $30,000 for the note and after 5 months of continual payments get a FHA refinance payoff of $135,000. In addition, you receive the next 12 monthly payments, let's say of $600 monthly, you would get an ROI of 350%!! Not to mention, the following 12 payments, totaling an additional $7,200. That's an annualized return on investment of 364%.

Not only did you help the homeowner stay in their home and make their monthly payment more affordable, but you did that while getting a HUGE return on investment within 3-5 months.

I hope this opportunity is something you as NPN investor can take advantage of! The opportunities are they - now go take action!

Comments