A Skeptical Real Estate Dude - Inflation is Officially On Fire

Welcome to A Skeptical Dude’s Take on Real Estate: a weekly frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

Coming at you live from Nashville, no AI generated content here folks.

Today We’re Talkin:

- -The Weekly 3 - News and Data

- -Inflation Report Today!

- -Real Estate Doomsdayers be Damned!

- -I am …. Postive?

- -The Skeptics Take: Good Vibes in the Market.

The Weekly 3: News and Data to Keep You Informed

- -11 Studies, 1 Conclusion: Housing market is underbuilt (ResiClub).

- -Would the Fed actually RAISE rates? Possibly, if inflation keeps rising (Bloomberg).

- -President Biden says Fed will Cut Rates this year. "Before the year is out there’ll be a rate cut.” (Bloomberg)

Today’s Interest Rate: 7.06%

(Flat from this time last week, 30-yr mortgage)

Today is a big day for us folks in the arena, it’s inflation day for consumer prices (CPI). Price action today will be heavily watched, more than usual. We have had 2 months of higher than expected inflation numbers. So according to NBA Jam rules, we are “heating up.” A hot inflation number for March, a trend it would make. And many believe, myself included, that if the Federal Reserve sees a trend up in inflation, they will be less inclined to lower interest rates. After, all, why would they? The economy is humming and we have very low unemployment (3.8%).

So get to it Skeptical Dude! What does today’s CPI number tell us?

January and February were not seasonal irregularities. CPI was up 3.5% YoY.

This was hotter than all estimates by the big financial institutions and higher than CPI in February (3.4%):

- Kalshi: 3.4%

- Barclays: 3.4%

- Citigroup: 3.4%

- Deutsche Bank: 3.4%

- Goldman Sachs: 3.4%

- JP Morgan: 3.4%

- Morgan Stanley: 3.4%

- UBS: 3.4%

- Bank of America: 3.3%

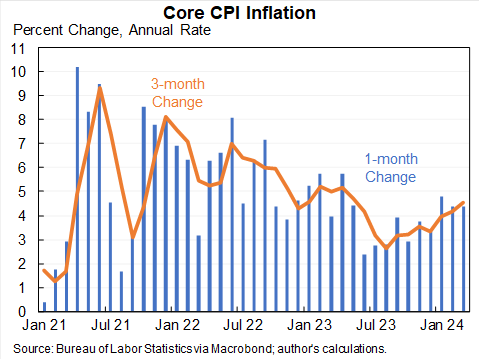

Core CPI has risen at a 4.6% annual rate, faster than any three month period from August 1991 to 2020 (Furman).

In the words of oft-cited economist Mark Zandi of Moodies Analytics… “Ugh. March CPI was a bummer…”

Ditto.

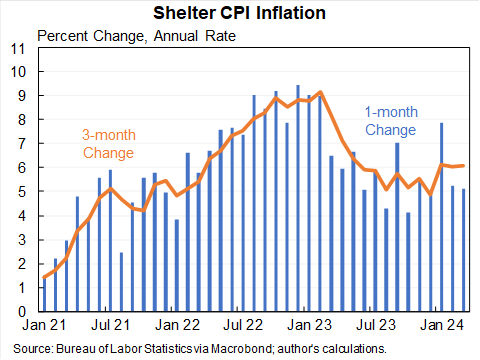

Shelter inflation is one of the major forecasts by economists watched by real estate investors. And the assumptions most economists made in projecting inflation numbers these past few months was that shelter would come down from its 9% to the 2-3% range. It hasn’t; in fact, it seems to have bottomed / plateaued at 5.5%. In fact, in fact… core goods (stuff you can buy) are underperforming services (people do/provide labor for you). In fact, In fact, in fact…Much of services’ increase is shelter. Shelter and gas prices were more than half the monthly increase for all items measured in the CPI for March.

Of note, recently you may have read quite a lot about the tremendous apartment unit growth we are in the midst of (as I have written about). But it hasn’t had a significant effect above the market’s ability to absorb that supply. Anecdotally, in Nashville, where we are in the middle of an apartment supply “surge,” rents are not ebbing. Not for anyone I know. This despite article upon article of impending supply doom!

Slight Tangent!

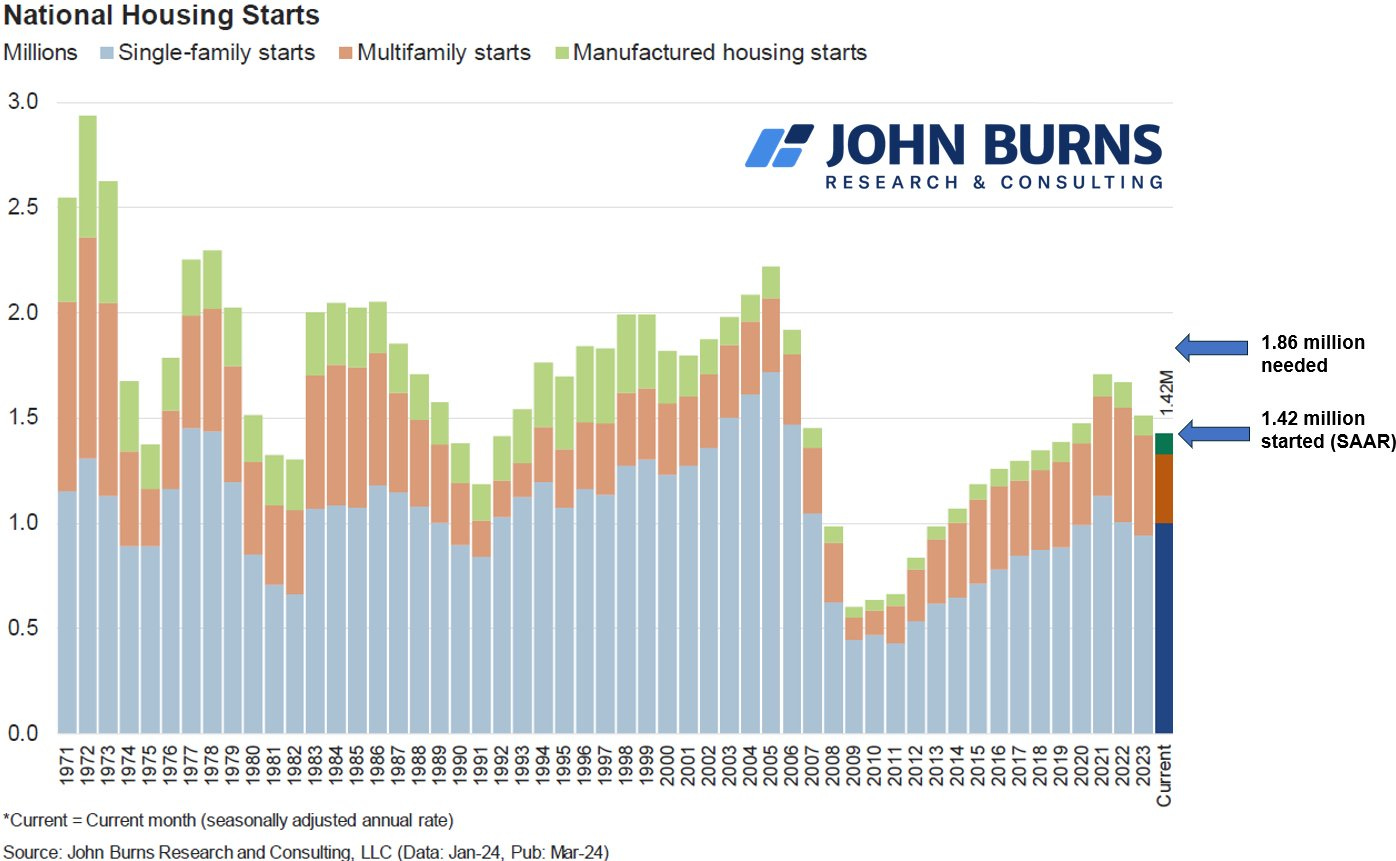

By the way doomsdayers…. a “surge” of housing supply is good thing. The US housing market is deficient in its supplyfor homes and apartments both, which is why price growth hasn’t abated. If we had more supply, that would be great for these things you may remember…people. “To keep up with annual demand, the US needs 1.86M new homes (for-sale and for-rent) per year through 2033, based on underlying demographics and current undersupply. We're currently starting homes at a [rate] of 1.42 million homes, ~400K fewer than needed.” (JBRE)

Real estate investors are long term thinkers and are a part of their community. We need a healthy supply of homes. It’s not healthy for the longterm viability of the/a housing market to be structurally undersupplied. The benefit of raising rents in the short term, on the back of strong demand, is far outweighed by a potential structural supply problem over the longterm. Those backs will break. Plus, high inflation and shelter costs hurt productivity, damaging economic growth. Large multifamily developer/operator worried about a high vacancy rate? It’s your fault if you built into your numbers ever exploding rent growth. That’s on you. Skeptic investors know you have to be conservative in your rent projections and ensure resiliency in a potential downturn.

Speaking of which. There are soooo many of these doom / salacious articles re: housing apartment supply. Like this one. And this one… and this one…

Are you wanting for an economic crash?

Blah, gets me fired up! I need more coffee now. Side note, just tried a new coffee this week: Death Wish coffee. It’s fantastic, super bold. Especially the dark roast. Highly recommend.

But I digress….

The Market may be Sniffing Something Out

As it stands today, the stock and bond markets are taking the inflation news with zero grains of salt. Stocks have so far fallen +1% and long dated treasuries are down +1.5%.

The market may be starting to realize something else than just inflation. It may be that the Fed may never get inflation under 2%.

So what? Why do I care? You are too Skeptical, Dude.

Well, to complete the sentence of Mark Zandi above…. “Ugh. March CPI was a bummer… and will surely delay the Fed’s first rate cut.”

I agree.

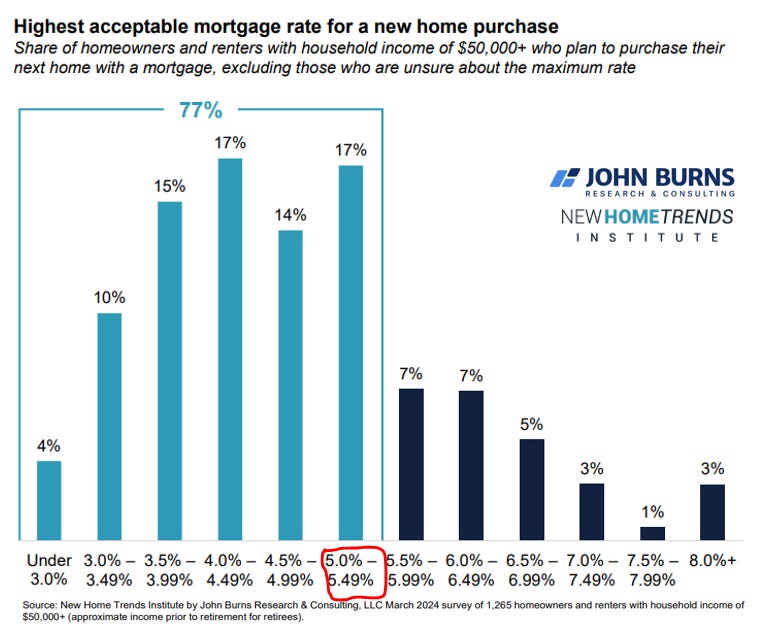

I am officially revising my rate cut estimate for 2024 from three .25% cuts to two .25% cuts. While the Fed may cut in June or July, to signal to the market all is healthy and / or to provide confidence (or for us conspiracy theorists because it’s an election year), they will then pause. Mortgage interest rates will remain elevated for a longer time period and I am estimating we won’t be back to an attractive rate - below 6%, where folks storm back to the market and feel comfortable leaving their home w/ a low interest rate mortgage - until the 2nd or 3rd quarter 2025. I would say 5-5.5% is the sweet spot for when folks will demand will rush back, partially due to mortgage payment affordability and partly psychological, after seeing both 8% rates and 2% rates in just the last handful of years. JBREC has a great chart on this:

Higher for longer interest rates could be a GOOD thing for the real estate investors.

High interest rates will continue to suppress demand for homes, build inventory, and allow for buyers to better negotiate for home prices. If they are able to afford that 7% mortgage for 1-2 years, they can then refinance having bought an asset for under what it will be worth in a “normal” market.

In the words of famed real estate mogul / investor Barbara Corcoran:

"If rates go down just another percentage point, that's what I'm hoping for by year-end, prices are going to go through the roof...Everyone will come out and buy. There are probably 10 buyers on the sidelines waiting for interest rates to come down that are actually active in the market. So everybody's going to charge the market...I wouldn't be surprised if real estate went up by another 8 or 10% if interest rates come down."

The Skeptics Take:

I remain quite positive on the real estate market, and asset markets in general.

Inflation has risen a few months in a row, but barely, and much of that growth is concentrated as of late. We are still likely on the down slope, but it will be more cross-country vs slalom. Up, down, flat, up, flat, down, down, repeat…

And to quote Economist Mark Zandi for the third time today, “[The Fed’s] got everything they need to start cutting rates…It’s just a question of precisely when.”

The housing market is improving, the supply of homes on the market is up double digits this month, and in my business I am seeing a healthy spring flow of demand for both homebuyers and investors. Very healthy. I had a few multiple offers last week. That was 2021 nostalgic.

Home prices, like wages, aren’t likely to go down (deflation) but we are likely to see the rate of increase slow as the Fed keeps rates restrictive (lower inflation, disinflation). I am still on alert for stagflation. This last longer than folks think + harm labor market = stagflation. Labor numbers remain important to watch. So far not though.

But for now, call me positive. It’s Spring! Get out there and start doing. My home market of Nashville is heating up, literally. And I bet your local market is too.

Don’t be an armchair sourpuss critic. It’s time to get in the arena.

That’s it for this week. If you are interested in talking real estate investing especially here in Nashville, reach out! You can message me right here on BP.

Until next time. Stay curious. Stay skeptical.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

Comments