July '22 Housing Market Update + Intro to BRRRR

And we’re back! Thanks for the great feedback from Volume 1. I know it was a long read, and I’ll try to keep this one shorter (spoiler: I failed). But I first want to quickly revisit the Bubble question in light of recent events -- namely, soaring interest rates.

First off, I’m glad I included the “Yes, but…” section last time, which outlined a potential worst case scenario of rising rates causing a recession. I think that worst case scenario is playing out in front of our eyes - count me among those who think an inevitable recession is looming, contrary to the words of the President.

But I still feel exactly as I did six months ago: that a recession will not cause housing prices to drop significantly on average, though certain areas -- primarily the stretch from Phoenix to Boise -- are almost definitely going to feel some pain. This article from Fortune shows that, based solely on local incomes, most markets are “overvalued” -- and a few markets have risen to extreme levels. Though to be clear, they are not predicting that home prices will drop by anywhere close to the amount that they are “overvalued” by…so it’s dumb that they even use that term. But either way, this gives you a great view of which local markets might be overheated:

Meanwhile, a fresh look at everyone’s favorite chart, the M2 Money Supply, shows that the supply has flatlined since February, but it is still about 26% higher than where it otherwise would have been if it had risen at the pre-Covid pace (as illustrated by my masterfully drawn dotted line). This further suggests that prices will stall, not fall:

Point being, some markets are likely to lose some value, but the overall market still has too many factors that are continuing to put upward pressure on prices (as I outlined in January). So, as I said before, I’m still actively looking to buy, though I admit that right now it is hard to find a deal that will have enough cash flow for my liking. Which is exactly why my entire acquisition plan is based upon finding off-market properties, which I will get into more in a future letter. But first, I want to educate you on the best real estate strategy I’ve come across: BRRRR.

Okay - so what is BRRRR?

I’m glad you finally asked. BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat, and it is hands down the best way to turbocharge the growth of your real estate portfolio. In short, it is a process by which you create value in a property and quickly put money back in your pocket to do it again. Beth and I have executed the strategy twice -- the first went to perfection, while the second was a relative disappointment but still successful. I’ll get into those details later.

Buy

This part seems self-explanatory on the surface, but the key is to buy a house for below market value. And that typically means that the house has deferred maintenance. For example, if a house needs $60k of repairs to bring it back to its former glory, then you might be able to buy it for $100k below what it would go for if those repairs had already been done. That $40k difference (100 - 60) is your discount for the risk you are taking on to renovate it. But if you know what you’re doing, the reward far outweighs the true risk.

Rehab, Rent

In the interest of your time, I won’t discuss these two steps in depth. Suffice to say, it takes detailed and careful planning on the front-end, and disciplined execution on the back-end, for these two steps to go according to plan.

Refinance

Here is finally where the magic happens. Assuming you did the first three steps well, your house is now worth well more than your purchase price + renovation costs. Now it’s time for a cash-out refinance, which allows you to recover most of the cash you have invested up to this point. And now you own a house that is doing three beautiful things: 1) netting you monthly cash flow, 2) appreciating in value, and 3) housing tenants who are paying off your mortgage.

Repeat

What’s the big deal? Couldn’t I just buy a normal rental property like a normal person and still get those three things?

Yes…but you’d also have the entire 20%+ down payment invested in the property, and unless you’re filthy rich, you won’t have more cash to buy another property -- i.e., you won’t be able to repeat the process -- for a very long time. But if you have BRRRR’d correctly, you’ve pulled most of that cash investment back out and you’re immediately ready to do it all over again.

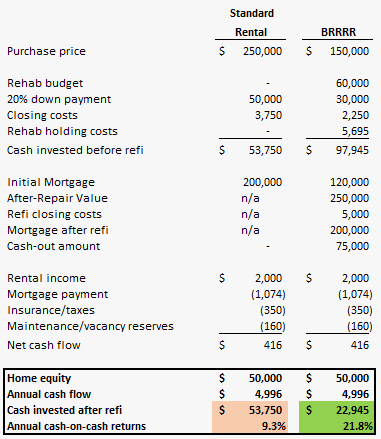

Let’s lay it all out for clarity. Here are the two scenarios: in the first, you buy a $250k house in great condition that will rent for $2k/month (realistic numbers here in Tally). In the second, you buy a house identical to the first, except it’s in poor condition so you get a $40k discount on it (as described above). Here’s the outcome:

Yes, but...

As with anything in real estate, there are risks and potential downfalls. Most are in your control, such as the risk of not planning or executing well. One downside is that you need a lot more cash up front ($54k vs. $98k in the example above).

Other risks are out of your control, such as getting a bad appraisal. This is exactly what happened with both our BRRRRs.

Our first one, a duplex in northern CA, we bought for $352k with a $90k down payment (split 50-50 with a partner). Then we put in $15k of rehab (plus a lot of work by the partner), so our total cash investment was $105k and we had a $270k mortgage. A few months later we began the refinance process, thinking the appraisal should come in at $475k. But it only came in at $410 - devastating, but we knew that appraiser was dumb, so we started over, and this time the appraisal came in at an even $500k, even better than we had hoped. So our new mortgage was $350k, and after paying off the prior one, we cashed out over $80k (350 - 270). So now our total cash invested is only $25k, and we are netting over $1k/month in cash flows, which means our annual cash-on-cash returns are around 50%. You simply won’t consistently find numbers like that with any other type of investment.

As we were getting ready to move to Tallahassee, we found a place that was a dump, but had lots of hidden potential. We got it for $234k and put over $100k into it, and I was very confident that an appraisal should value the home at $350k minimum, maybe even $400k. But alas, it only came in at $320k. And unlike the first one, we couldn’t start over because this was the end of 2021, and interest rates were rising so fast that our best choice was to stick with the 2.875% rate we already had locked in. So we stuck with the low appraisal, and pulled out $250k. In the end, we have $100k cash invested**, while the house is beautiful and doing great as a short-term rental, bringing in $1k/month (and I expect that might jump to $2k once everything stabilizes). That puts our annual cash-on-cash returns at a “disappointing” 12%+.

Now we have two properties with excellent cash flows, plus enough free cash to find another and do it all over again.

Conclusion

Investing in cash-flowing rental properties is exactly like pushing a little snowball downhill and watching it gain momentum as it grows ever larger. And BRRRR’ing is like getting behind that snowball and pushing, forcing it to roll and grow much faster.

If the numbers excite you but you don’t feel like you can go it alone, that doesn’t mean you can’t get involved! There are many ways to partner with others -- as one example, next week we are closing on a flip in Huntington Beach, but we are strictly passive investors with a 40% share in the profit or loss. It’s projected to bring a 25% return in as little as four months. Here’s hoping I’m not wrong about the Bubble…

**You might notice that if we had simply bought a nice house for $400k, then we'd only have $80k invested rather than $100k. This is true, but you'd also have a $320k mortgage rather than a $250k one -- so you'd be a much higher payment and $70k less home equity. So even a less-than-ideal BRRRR outcome is better than a traditional purchase.

Comments