3 Reasons the Housing Market is NOT a Bubble

It’s the question on everyone’s mind: “Is the housing market in a bubble?” Google searches are up 2,450% in the past month, and for good reason. In Denver, single family home prices increased almost seven percent in the past month, which would be strong appreciation for an entire year. Since March 2020, the same market has appreciated almost 20 percent. These red-hot numbers are shocking, but if one simply examines the underlying data, the evidence for a bubble is lacking. Instead, it’s the free market forces of supply and demand and a pandemic economy that are driving record prices.

Demand

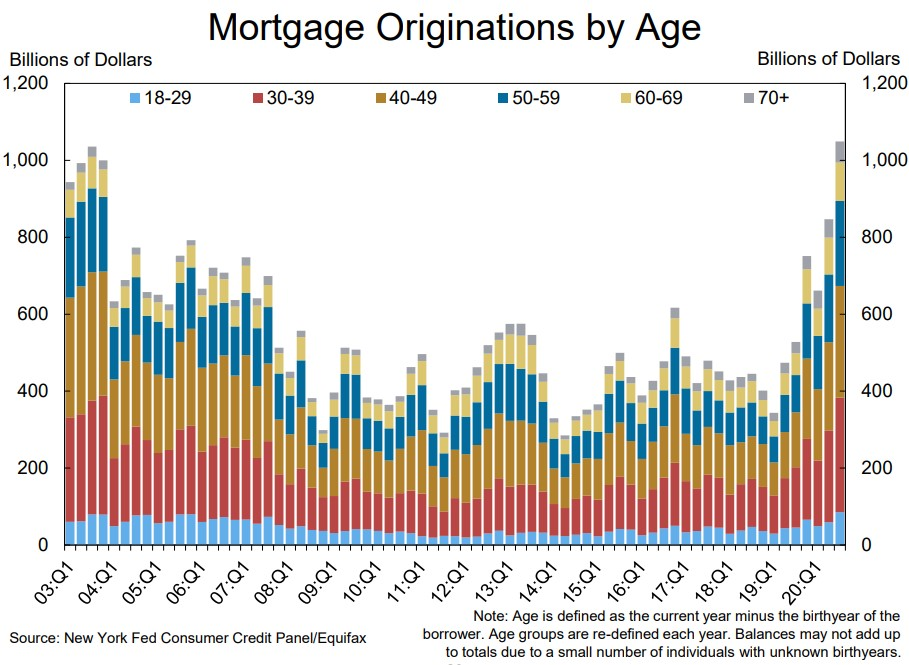

Various factors are escalating demand. Millennials, the largest generation of Americans, are finally buying. In 2011, people in their 30s made up around 20% of all mortgage originations and ten years later that number is almost 30%.

Millennials will continue to make up the biggest demographic in our country is entering their prime homeownership years, so don't expect demand to slow down.

Interest rates are at historically low levels, and recently dropped back below 3%. Less known than its 2%/1% rule cousins, the 1%/11% rule of interest rates is driving up home affordability.

Source: MyMortgageInsider

This basic math principle shows that when interest rates drop by one percent, the corresponding mortgage payment drops by 11 percent. Mortgage interest rates have dropped from a recent high of 4.94% in October 2018 to a low of 2.65% in January 2021.

Source: YCharts

This drop in interest rates alone causes an over 25% increase in affordability and can explain some of the surge in housing prices!

Supply

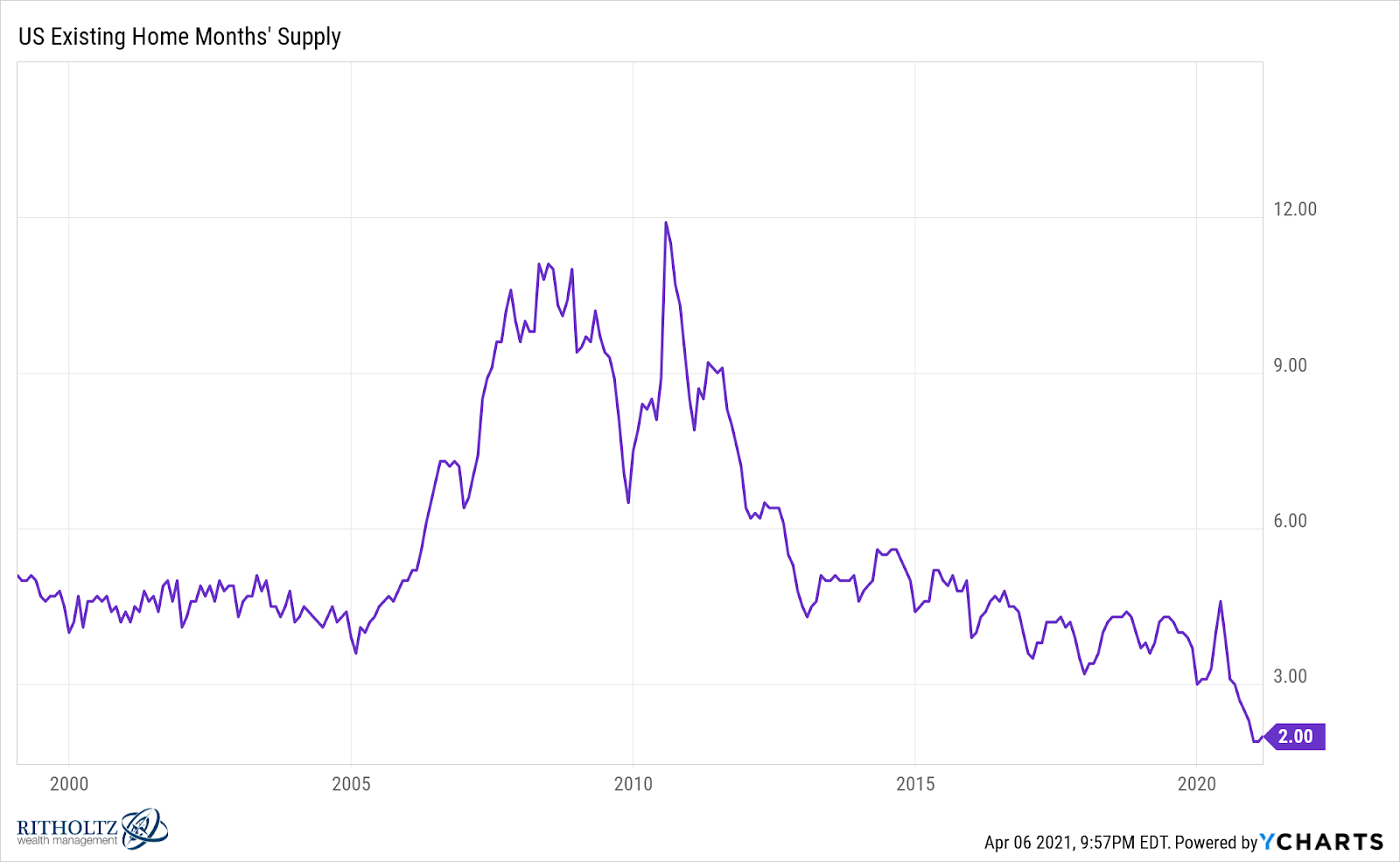

In Denver, Month of Inventory (MOI) at the end of March dropped to 0.39 months. Given our current inventory and current rate of sales, it would take 0.39 months or less than 12 days to deplete that inventory.

The supply of existing home sales on the market is the lowest on record since the late-1990s:

One commonly cited source for the lack of new listings is the pandemic. Understandably, potential sellers do not want possible-COVID infected, prospective buyers touring their homes during showings.

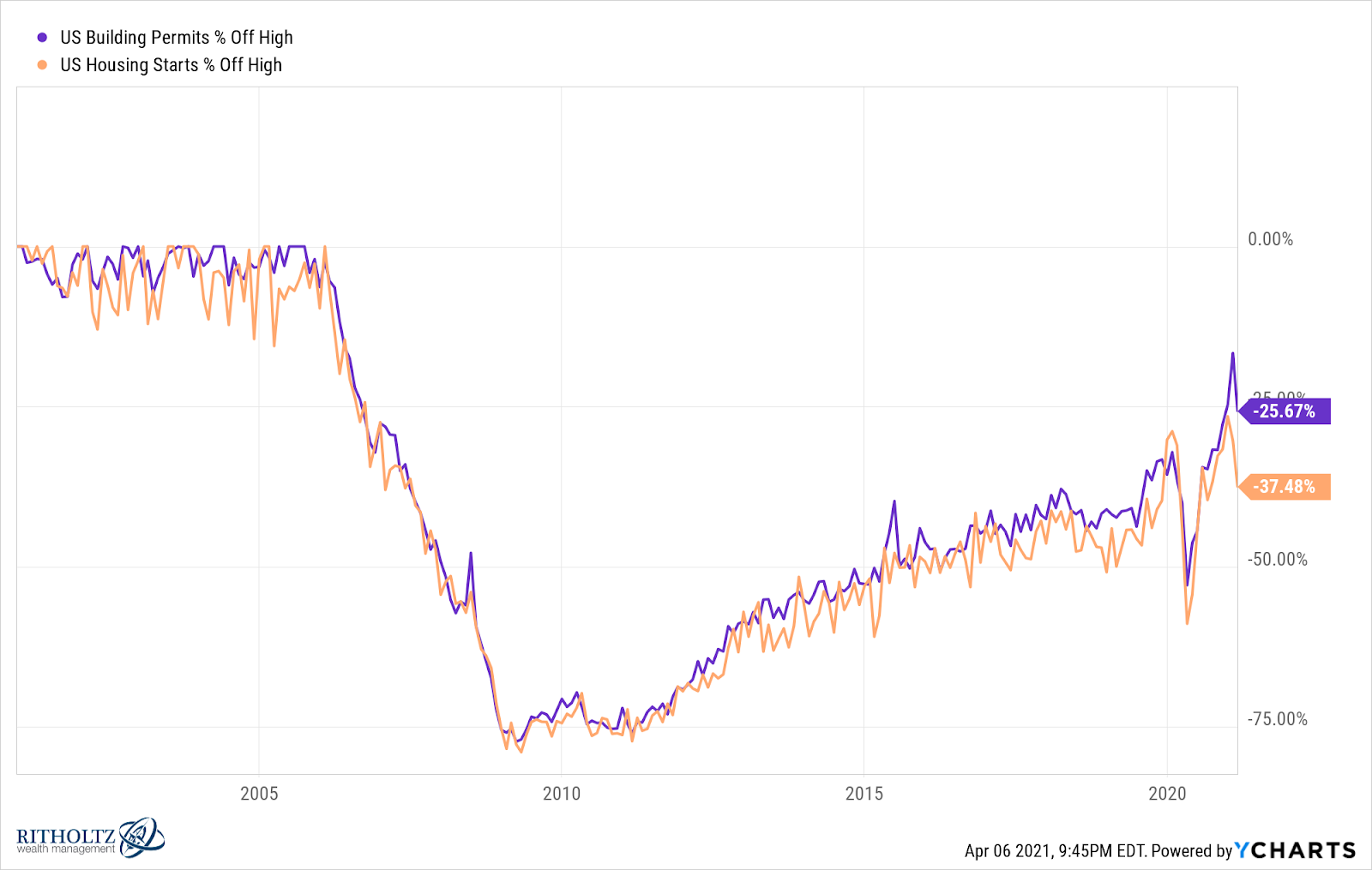

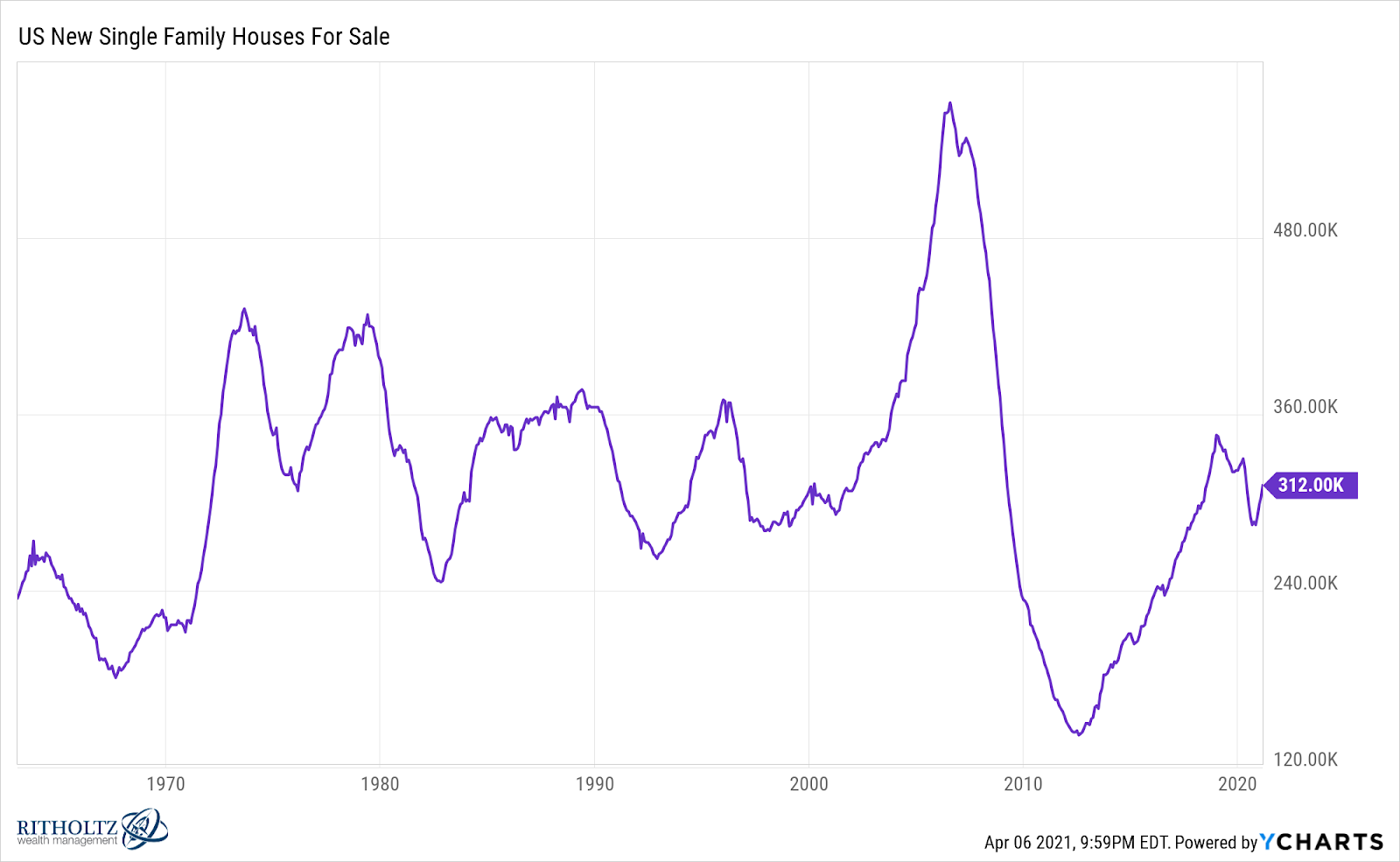

However, another cause of the dramatic shortage is lack of new starts from homebuilders. New home starts have not recovered since the last housing crisis in 2007-2008.

The Pandemic Economy

The third rail of this housing market is the rise of a new economic forces sped up by the pandemic. Remote workers now have the freedom to work from home and move to areas with better quality of life. Additionally, small time investors purchasing second homes are driving a surge in demand. Second homes and investment properties accounted for 14% of all purchase-mortgage applications in February, a record in data going back more than a decade, according to the Mortgage Bankers Association.

What's next?

It’s unclear what happens next in this market. It will take time for supply, especially new homes, to catch up with demand. Jerome Powell, Chairman of the Federal Reserve has maintained he intends to keep interest rates low, though recently Treasury Secretary Janet Yellen predicted interest rate need to rise at some point in the future. Even with a rise in interest rates, the market would soften, but with new trends in millennial buyers and a digital economy, it’s not clear that the demand for housing is going anywhere.

Comments