How to Grow Retirement Wealth Tax- Free

We often hear that we are never too young to start planning ahead for retirement, but the words “young” and “retirement” may not immediately strike you as synonymous. Many investors, especially those just starting out, are not familiar with self-directed investing and its tax benefits. Some investment companies don’t recommend, or even offer, the option to invest in “alternative assets,” as in anything beyond traditional stocks, bonds, certificates and mutual funds. Other investment companies, advisors, or attorneys are limited in their knowledge of alternative investments. For investors, not having this information readily available can mean losing out on more of what they earn to Uncle Sam.

Some investors discover self-directed tax-deferred and tax-free investing due to prior involvement in real estate, finance or venture funding. Some of these not only become self-directed investors, but go on to raise money from other self-directed investors to fund their real estate deals and ventures. But for the average investor, stumbling upon self-direction often involves curiosity or luck. No matter how you found this article, you reached a good place to begin.

No matter what stage you find yourself in on your road to retirement, the tax-advantages of self-directed accounts are not only one way to diversify your portfolio through alternative investments, but these accounts will also help you hold onto more of what you make. With accounts like Health Savings Accounts (HSAs), Educational Savings Accounts (ESAs) and Roth IRAs, you can build retirement wealth tax-free, as well as enjoy the benefits in the here and now.

Benefits of the Top 3 Tax-Free Plans

1. Health Savings Plans (HSAs)

Are you an employee of a company that offers the HSA as an option? Are you part of a high-deductible health insurance plan? Are you not claimed as a dependent on anyone else’s tax return or covered by any other major medical health insurance policy? If you answered yes to these questions, then you are entitled to significant tax advantages with a HSA.

Health Savings Plans allow you to generate tax-free income, while managing the rising costs of healthcare. This type of account is tax-exempt, meaning that it can be BOTH tax-deferred and tax-free. The money you contribute to an HSA is tax-deductible, but it is not taxed when you withdraw it for qualified medical expenses, including prescription drugs, insulin, physician visits, hospital fees, and other out-of-pocket medical and dental procedures.

You are able to use your HSA to invest in a wide range of alternative assets, including real estate, gold and silver, private placements, mortgage notes, and more. The income generated from these investments can be used for the qualified medical expenses mentioned above.

There is no time limit for reimbursement on these medical expenses from an HSA as well. Even if you take money from your account to pay back what was spent out-of-pocket on a procedure or doctor’s visit years after the visit, this money will have earned interest and can be withdrawn tax-free and without penalty (after you reach the age of 65, there is no penalty for withdrawing for non-qualified expenses). As long as you keep a detailed record of your medical expenses, you can ensure that our withdrawals will not be subjected to income taxes.

2. Educational Savings Accounts (ESAs)

For those continuing their education or saving up for their child’s college, an Educational Savings Account (ESA) is an excellent option. This trust account can be established for any qualified beneficiaries, as long as they are under the age of eighteen or have special needs. ESAs are designed to pay qualified higher education expenses.

ESAs are an excellent way to diversify your portfolio all while growing your savings for your children’s future education. Real estate, gold and silver, private placements, and loans are all examples of investments that can be held in an ESA.

Similarly to the HSA, the ESA can be funded with post-tax dollars (meaning there’s no deduction on your taxable income) and can be withdrawn tax-free for qualified educational expenses like tuition. These accounts have tax-deferred contributions, but the funds in the account grow tax-free. Any distributions taken from the account that are less than the qualified education expenses in a given year are tax-free as well. As long as these account balances are distributed to the beneficiary before they reach the age of thirty (an exception being those with special needs), funding an ESA can not only help save up for your child’s tuition, but it can provide benefits for elementary and secondary school education expenses as well. The designated beneficiary can be changed, and unused funds can be rolled over tax-free to an ESA for another family member under thirty.

3. Roth IRAs or 401(k)s

Many associate these types of accounts with employers, and if you have one, always take full advantage by saving the maximum amount you can. If your employer is matching all of part of your contribution, it’s essentially free money. But many are surprised to learn that individuals, self-employed workers and small business people can not only create their own 401ks, but make them self-directed as well.

Roth accounts ensure you can save more of what you make and allow you to grow your retirement wealth tax-free. Favored by taxpayers since its inception in 1998, a Roth account’s long-term tax advantages allow your money to grow as long as you’d like for a tax-free retirement. They are the proactive option against future tax increases, financial crises, and more unknown factors that can affect your retirement.

The rules of Roth IRAs or 401(k)s are similar to traditional IRAs, but the major difference is that you pay taxes on the principal upfront. Unlike a traditional account, interest and returns are never taxed upon distribution. As you earn more income throughout your career, your tax bracket is likely to rise along with it. With a Roth, you can avoid that higher tax rate when you pay taxes on your contributions (i.e. on the front end). These contributions can be withdrawn without penalty after the age of 59.5, and there is no age for requirement minimum distributions like there are for traditional accounts. Some examples of qualified withdrawals of earnings within a Roth account includes first-time home purchases and higher education. As long as your income and earnings qualify you for a Roth, you can open an account and begin investing at any age.

Just like in an ESA or HSA, a self-directed Roth IRA or 401(k) can be used to grow wealth from investing in alternative assets. For instance, you can purchase a rental property in your Roth IRA, have all the rental income flow directly into your IRA tax-free, and years down the line, the profits from the sale of that property can also flow into your IRA tax-free. Those funds can continue to remain in your Roth IRA until you reach retirement, or can remain in your account for a beneficiary to inherit.

Do your income limits exceed what is needed to contribute to a Roth? If so, you may have the ability to open a Traditional account and later move funds into a Roth in a workaround “back door” method.

Why Now?

Now that you’ve read up on the different types of tax-free accounts you can invest with, perhaps you’re still wondering: Why now? Retirement is too far off on the horizon for you to be thinking about it, especially when there are bills to pay, kids to raise, college loans to pay off, and more expenses.

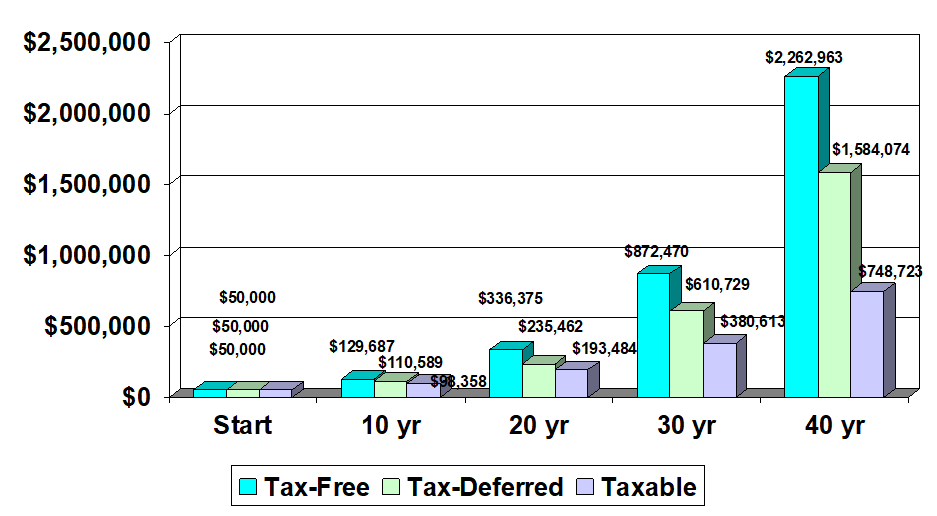

Starting early can be very powerful. With the help of compound interest, tax-advantaged accounts help you hold onto more of what you make, and shelter your funds in the event of financial crises or major changes in the market that can occur over time. See the chart below to view the impact of investing through tax-advantaged accounts over time, and how they compare to your regular taxable income.

When it comes to your financial future, it is never too early to start saving. Taking the necessary steps to become financially free can help you unlock a future and retirement that grants you tax-free income for life.

Do you have any experience with tax-free vehicles that you'd like to share? Comment below!

Comments