Real Estate News & Current Events

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated almost 5 years ago on . Most recent reply

How is the COVID-19 Crisis Impacting Retail Real Estate?

Bigger Pockets Community,

Before the COVID-19 crisis, my investing partner and I were analyzing deals for neighborhood strip centers in our home region. What a difference a month (or three) makes. Over the past several weeks, I've been doing a lot of research and analysis of how the crisis may create new opportunities (and amplify existing threats) for several retail categories as well as for retail real estate investors. I wanted to share the results of the deep dive with whoever might be interested in neighborhood retail or macro-trends. I hope you find it useful.

Retail Real Estate and the COVID-19 Crisis

Retail has developed a serious image problem in the past decade-- one that will be further complicated by the shock to the economy and consumer behavior caused by COVID-19. Over the ten plus years between the Global Financial Crisis and the current health crisis, Retail underwent a radical transformation driven by the growth of e-commerce and many companies failed to evolve and took on too much debt, resulting in numerous bankruptcies and thousands of store closures. During this period there have been over 35,000 news stories written about the “retail apocalypse.” Coverage has been narrowly focused on a limited number of chains that were heavily concentrated across a few segments that were most vulnerable to disruption, such as apparel, consumer electronics and department stores. The poster children for this are the department store anchor and the dying mall. As a result, the perception is often that retail is broadly in decline and that our future lies with e-commerce and its network of warehouses and trucks. This of course is an oversimplification and real estate investors would be well served by appreciating the nuances within retail that will determine the winning and losing concepts and locations during the next ten years, and specifically in the aftermath of the COVID-19 recession we have just entered.

The Evolution of Retail

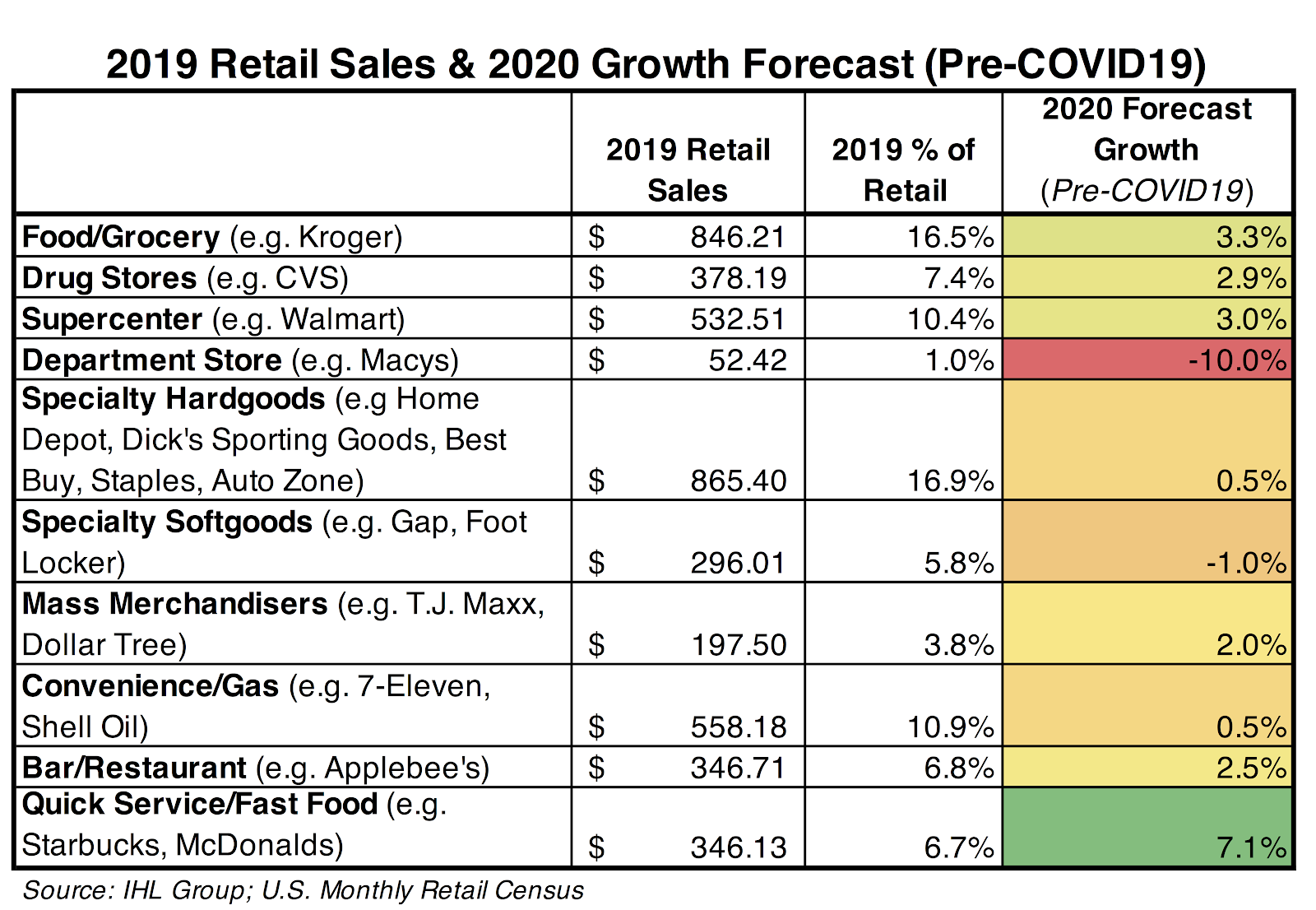

Rather than showing absolute decline, the numbers tell a story about retail evolution. Consumer spending accounts for more than two-thirds of U.S. economic activity, with retail purchases making up approximately 25% of the average American’s annual spending, according to the Bureau of Labor Statistics. Retail sales have been growing by almost four percent annually since 2010, with over five times as many companies opening stores as closing them. Last year, a steady increase in consumer spending, bolstered by record low unemployment helped to sustain GDP growth even as business spending declined across the second (1%), third (3%) and fourth (2%) quarters. Through the last quarter of 2019 and start of 2020, the pace of retail spending was showing signs of slowing but continued to grow steadily. IHL Group, a company focused on research in retail and hospitality, projected strong growth in quick service restaurants, steady growth for restaurants/bars, grocery stores, drugstores, and superstores, such as Wal Mart and Target. IHL forecast a continued decline for department stores and specialty softgoods which includes retail apparel. Prior to the impacts from COVID-19 retail was continuing its recent trends with apparent winners and losers.

Any conversation about retail sales must also acknowledge the effect of e-commerce, which has been growing rapidly over the past decade, and makes up a significant share of overall retail sales growth. The rise of e-commerce has been enabled by an increasingly frictionless customer experience through the sales funnel from awareness to purchase in just a few clicks. E-commerce has also been bolstered by offering free-shipping and easy returns. External factors, such as low oil prices and a flood of cheap financing from venture capital and the public markets, have allowed some e-commerce companies to focus on driving exponential growth and capturing market share over profits. This has put acute pressure on the most vulnerable physical retailers, but many have continued to thrive. While e-commerce has been growing quickly and increasing its share of retail spending, Americans finished the decade making 84% of their purchases in retail store locations with the total dollars spent in-store increasing by over 26%, from $2.4 Trillion to $3.2 Trillion, over the past 10 years.

As retail has changed, the distinction between a purchase made through the internet and a physical location has been blurred. Many traditional retailers have invested heavily in online infrastructure, allowing purchasers to do research online, shop, and pay, and then pick up their item in the store. Best Buy and Home Depot are two prime examples of this. Restaurants and grocery stores have internet purchasing infrastructure that drives delivery or pick-up from their retail locations. Amazon purchased Whole Foods and is looking to get into convenience retail. It is also investing heavily in using technology to reduce human interaction and labor costs within physical stores. This all suggests an evolution, not an absolute decline of retail locations and a complete move to internet driven transactions with deliveries coming from warehouses.

An Opportunity for Investors

While many investors have decided the evolving retail landscape is too risky and perhaps have been scared off by the overwhelming negative sentiment driven by the failing concepts and asset-types, such as enclosed malls, opportunities within retail remain, provided investors are willing to move past the headlines and perform the necessary due diligence that is required for any real estate acquisition: carefully analyzing the type of property, the tenants and the location characteristics. For investors who are willing there is an opportunity to find value in specific retail assets where net operating income is primarily driven by grocery, restaurant, convenience, fitness, services, and experiences--the most e-commerce resistant uses. These locations should be in dense trade areas with solid demographics. The long-trip to the mall or the outlet center might be going away, but people still enjoy getting out of the house and will continue to frequent these types of establishments within their communities.

We can see the potential opportunity in retail when looking at the cap rates (the relationship between the income the asset produces and its price) investors are paying for the assets. A higher cap rate indicates investors are anticipating more risk and slower growth, while a lower cap rate shows strong investor demand for an asset type and the expectation for future growth and lower risk. For example, prior to the impacts of COVID-19 cap rates for grocery-anchored neighborhood retail in top markets were between 5.50% for class A (the best) and 7.00% for class B (older, no longer the best assets), compared to 4.5% for Apartments and Industrial, which is primarily driven by the demand for e-commerce warehouse space. Apartments and Industrial were priced for perfection, with investors betting heavily on limited downside and continued rent growth. The spread in yields between these property types and retail is not totally unreasonable, but the best positioned retail assets appeared under-priced relative to other asset types due to indiscriminate negative sentiment.

Retail and the COVID-19 Recession: Permanent Changes and Severe Temporary Impacts

Retail’s slow start to the year turned into a sudden free fall as governments around the country and the world issued stay-at-home directives and ordered non-essential businesses closed to hasten the rampant spread of the virus. By the time 30 states had announced closures across the U.S. on March 30th, the S&P 500 had declined by almost 24% from a record high five weeks earlier, and SPDR S&P Retail Index ETF, which includes companies like Rite Aid, Kroger, and Dollar General, dropped by over 35% during that same period.

The crisis is having a dramatic impact on the public market pricing of retail real estate. For example, Retail Opportunity Investment Corporation (ROIC), which is a REIT composed of necessity-based neighborhood shopping centers, anchored by national or regional supermarkets and drug stores located in densely populated areas with strong income fundamentals across growth markets in the western U.S, has dropped by over 46% since the start of the year - down almost 20 percentage points more than the SPDR Retail Index ETF.

The value of retail real estate assets is largely dependent on the health of its tenants. Nearly all retailers are taking a direct hit, with stores in many parts of the country already closed, or operating under drastically different circumstances, for two weeks or longer. Many retail stores and services are seeing a sharp decline in demand or are totally closed, while others are adapting customer experiences and distribution channels to conform to new norms around social distancing, and a few are capitalizing on emergent needs, such as for consumer staples like packaged food, household cleaners, medication and home office supplies. While these changes are severe, many are temporary. Investors must separate these impacts and evaluate various types of retail differently.

Grocery, Drug Stores, Supercenters and Discount Stores:

Retailers in these categories have been outperforming initial forecasts for 2020 due to a surge in sales on par with the holiday season as customers flocked in store to stock up on essentials. These stores have been deemed essential services which will allow them to remain open and continue operations throughout the shutdown. Shopping centers anchored by these types of retailers should be well-positioned to weather the economic downturn. These retailers are not at risk of disappearing during the recession.

Department Stores and Retail Apparel:

Several retailers in these categories have already been in a prolonged state of decline for over a decade, but the shock of forced closures and lack of consumer demand will be the final straw that accelerates the demise for many. Malls and lifestyle centers anchored by these types of tenants will face dual challenges of a sudden loss of rent revenue, as many stores have already defaulted on April payments, and accelerated closures and bankruptcies combined with the costs associated with repositioning and leasing the large spaces they once occupied. Any asset where these tenants comprised a significant portion of income or where responsible for driving foot traffic is at high risk of becoming distressed during this recession.

Quick Service, Fast Casual, Bars/Restaurants & Fitness:

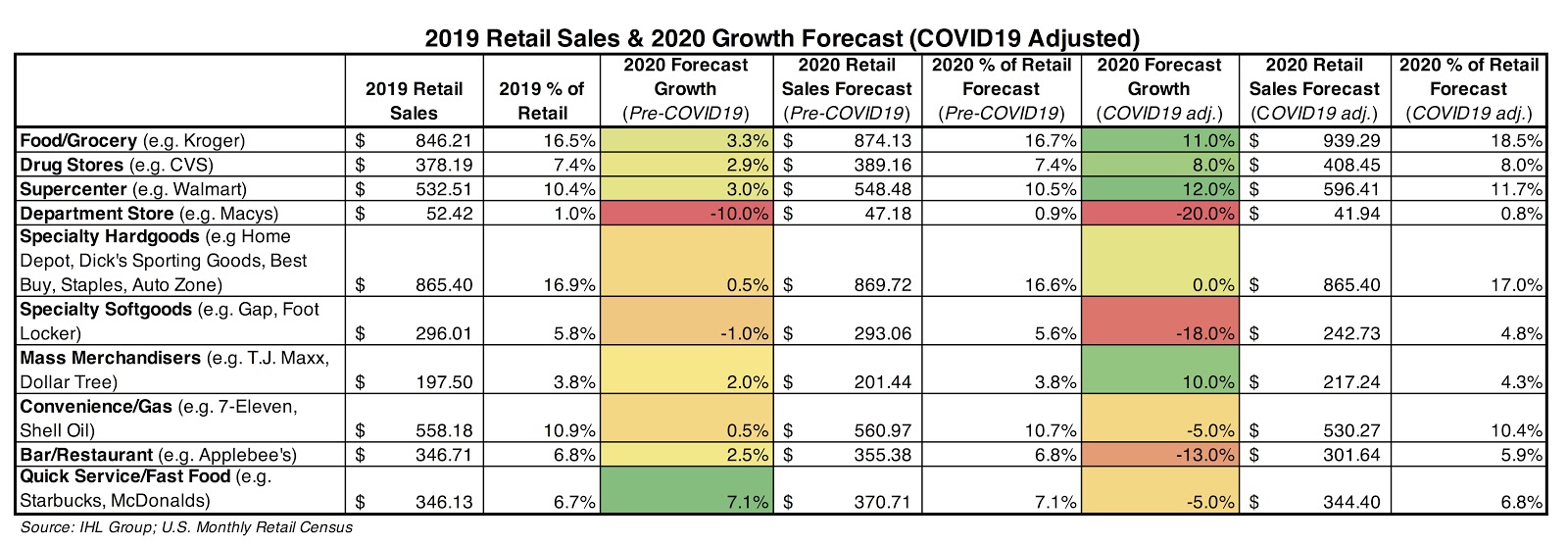

Service-based retailers that rely on face-to-face interaction with customers and social gatherings started the year strong and were forecast to outpace other retail categories in growth. These businesses are extremely vulnerable to forced closures and will likely be the first expenses consumers cut back during a recession. Quick service restaurants, which were projected to grow by over 7% in 2020, are now expected to decline by -5%. Shares in Planet Fitness, the largest gym operator in the U.S., fell more than 70% last month. This will certainly cause near-term financial strain for the operators of these mainly franchise-owned service businesses and their landlords. However, dining out and fitness are often the first categories to snap back in an economic recovery as people prioritize convenience, wellness and simple indulgences again. The locations that can survive the temporary closures will likely see steady growth as we begin to emerge from the social distancing restrictions and the recession. Investors can proceed with caution in the short-term but this may become an opportunity to acquire assets that will recover sales quickly and are likely to emerge as winners during the longer-term retail evolution.

E-commerce:

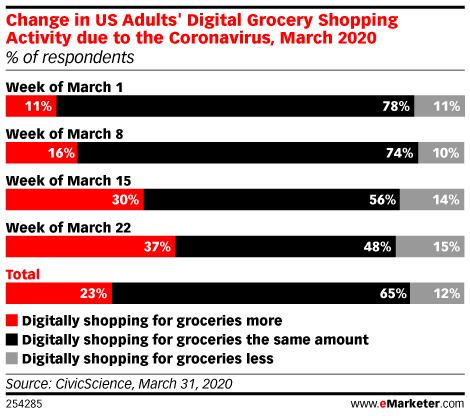

Although this constitutes a sales and distribution channel and not a specific category, the rise of online shopping and food delivery exerts a tremendous influence on brick-and-mortar retail and service businesses. Images of grocery stores running out of essential items circulating on social media, mandated restaurant closures and government issued stay-at-home orders, have all been significant recent drivers of online shopping. Last week, eMarketer cited a CivicScience poll of US adults and their digital grocery shopping habits, the percentage of those who said that they increased their online grocery shopping jumped from 11% to 37% in the first 3 weeks of March.

Brick-and-mortar retailers that previously invested in e-commerce fulfillment channels are best-positioned to capitalize on accelerated shifts in purchasing behaviors and emerge even stronger from the situation. According to a recent report from IHL Group, the traditional retailers across grocery, drug stores and supercenters that were growing their businesses by 10% or more prior to COVID-19, were many times more likely to have invested in offering the following customers journeys to make their physical locations complimentary to e-commerce:

Click & Collect: 13x

Buy Online, Return in Store: 1.6x

Ship to Store for Pickup: 1.3x

Ship from Store: 1.6x

Similarly, the Wall Street Journal reported that restaurants are seeing a surge in online ordering via platforms like DoorDash, Uber Eats, Grubhub and Postmates. Americans more than doubled their spending on restaurant delivery between February and March. However, many of these services offer unfavorable terms, such as 30% pre-tax commission and forced discounts to lure customers, that cut into food service business owners’ already low operating margins, as reported by TechCrunch. Although these services are an economic lifeline in the short-term, their unit economics are an unsustainable model for restaurants to rely upon over the long-term.

Conclusion

The effects of COVID-19 on public health, the economy and as a result retail real estate remains a fluid situation which I will continue to monitor in the weeks and months to come. In the meantime, my takeaways thus far are:

- Public market values of retail real estate with otherwise strong fundamentals have dropped dramatically which may imply a coming drop in private market pricing and open opportunity for investors to find value.

- Different sectors of retail, and therefore different categories of tenants, are experiencing the crisis across a broad spectrum. Neighborhood retail anchor tenants, like grocery and drugstore chains, appear to be thriving. Experiential services that provide people with a compelling reason to leave their homes, like restaurants and gyms, are suffering but poised for a comeback during a recovery. Categories that were already in decline like department stores may not recover.

- E-commerce is picking up the slack for some retail where store shelves are stripped due to hoarding, and is fulfilling a necessity for shipping goods to people who cannot leave their homes. Brick-and-mortar store and restaurant locations are proving to be a key component of last mile delivery, indicating a future where e-commerce compliments but does not close physical retail.

Finally, a note on human nature. There is a lot of speculation going around about how our behaviors may change as a result of the global health crisis - that we will become an anxious, homebound society which favors working remotely, homeschooling its children and ordering everything online. While that may be the case for some aspects, such as more flexibility to work from home or increased adoption of online learning, for many they just want to get back out there. Many people may now have a greater appreciation for their water cooler conversations at the office, the trip to the grocery store to hand-pick their meats and produce, a haircut at a barbershop, a workout at a gym, or a meal with their family in a restaurant. The social distancing rules have shown the need for human interaction in physical spaces and the limitations of ordering everything online and largely staying at home.

Google Trends: Web Searches for Cabin Fever (YTD)