Tax, SDIRAs & Cost Segregation

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated 7 months ago,

- Specialist

- West Palm Beach, FL

- 1,459

- Votes |

- 4,299

- Posts

Amending Your Tax Return vs Form 3115

- Specialist

- West Palm Beach, FL

Everyone makes mistakes now and again when filing a tax return whether it be forgetting a deduction, missing a portion of your income, or improperly depreciating an asset. The IRS has multiple ways that these errors can be fixed. The two most primary tools are by filing a Form 3115 or by amending your tax return. Let’s discuss when it is appropriate to utilize each of these tools.

AMENDING A TAX RETURN

An amended return is a revised version of the tax return that you previously filed. This is a way to let the IRS know that you made a mistake and you are requesting to fix it.

When should you amend a tax return?

- Mathematical errors: If you miscalculated a deduction or credit, an amended return can help correct the error.

- Filing status change: If you originally filed as single but are now married or qualify as head of household, you can amend your return to update your filing status.

- Missing or incorrect income: If you missed reporting income or reported an incorrect amount, you can amend your return to get this corrected.

- Missing deductions or credits: If there was a deduction that you were entitled to, but you forgot to claim it, you can amend your return to include the deduction.

How should you amend your tax return?

- You or your CPA will need to use Form 1040-X and provide explanations for the IRS as to why you are making these changes. Note that you typically have two years from the date you paid the tax or three years from the date you filed the original return (whichever is later) to submit an amended return.

FORM 3115

This is a specialized IRS form that is used to request permission to change an accounting method. There are many accounting methods utilized in a business as these are the rules that dictate how businesses report their income and taxes for tax purposes.

When should you use a Form 3115?

- Switching to a new accounting method: You may decide that another accounting method better reflects your business’s financial activities or is more tax advantageous. Some examples of this would be 1) depreciation calculations such as switching from straight-line depreciation to accelerated depreciation (often used for cost segregation studies when not performed in the year placed in service), 2) income recognition, and 3) inventory valuation such as changing from LIFO to FIFO.

- Correcting a mistake: If you realized that you used an incorrect accounting method after you filed your tax returns, you can file this form to request permission to change to the correct accounting method so that your tax reporting is accurate.

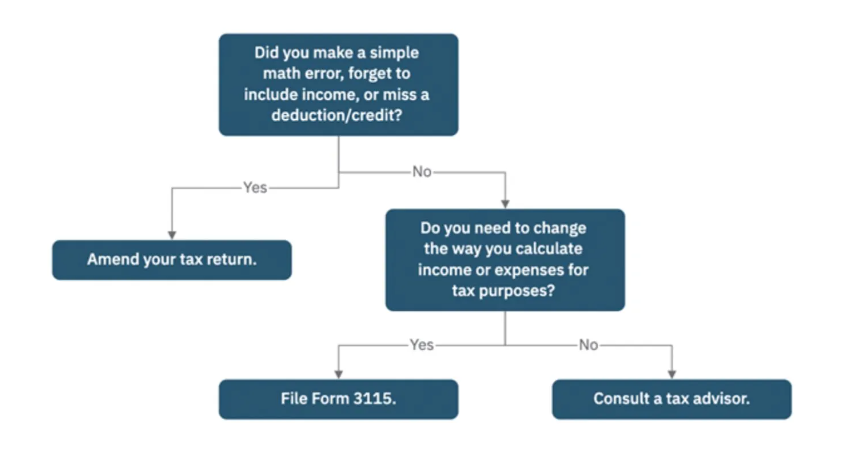

Here’s a chart that you may find helpful when deciding whether you need to amend your return or file a Form 3115.

As always, I recommend consulting your CPA or tax advisor as the rules can be complex.

What is your experience with filing a Form 3115 or amending your tax return?