How Pro Forma Works In Real Estate Investments

The first thing an investor must consider when looking at any potential real estate investment property is the cash flow projection. This is done through a Real Estate Pro Forma, which allows an investor to evaluate the overall profitability of a property.

Seller’s Pro Forma vs. Buyer’s Pro Forma

To state the obvious, the seller of a property wants you to buy that property, so he or she will frame the pro forma to make the cash flow look as positive as possible, which often means that several key considerations may be missing or oversimplified. As such, the decision to purchase a property should be based off of a buyer’s pro forma using true (or as close to true as possible) estimations and calculations.

How to Read and Understand a Pro Forma

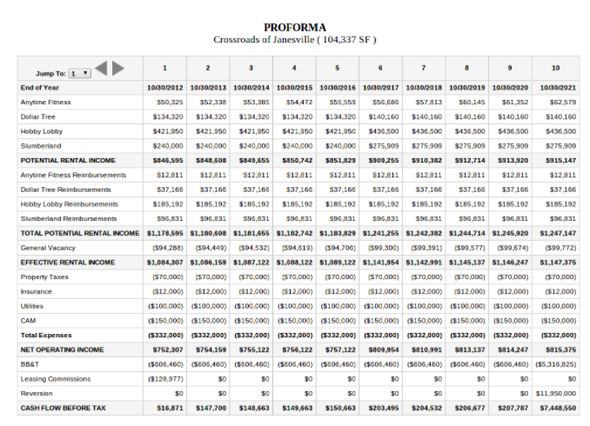

You’ll need to fully understand how to interpret and read a pro forma with each real estate investment you consider. Let’s take a look at one example.

(source)

The above example shows a ten year cash flow projection similar to what many real estate investors will build and study when evaluating any potential investment opportunity. This pro forma table includes the following:

- Potential Gross Income (PGI)

- Vacancy Allowance

- Other Income

- Effective Gross Income (EGI)

- Operating Expenses

- Net Operating Income (NOI)

- Other Expenditures

- Before Tax Cash Flow (BTCF)

- Reversion Cash Flows

You can find an in-depth explanation of each of the above items here.

What to Include in Your Pro Forma

There are 4 key line item considerations that should be included in every buyer’s pro forma: repairs, vacancy loss, property management, and miscellaneous.

(Thanks to HowToBuyUSARealEstate for the description of these four items. Read the full article here.)

Moving From Pro Forma to Actual Data

You’ll want to transition from examining cash flow projections to studying real life data as you advance through the real estate investment evaluation phase. You should ask the seller to provide you with the following: previous years’ tax returns, property tax bills, maintenance records, etc. This concrete data will give you a much more accurate picture than the estimated projections.

According to BiggerPockets.com, you’ll want to examine the following sources to gather this information and make you an informed real estate investor:

- Property Details: This information should be available from the seller, but more comprehensive and detailed information can also be obtained from your local County Records Office

- Purchase Information: Obviously the seller is going to name a purchase price (which will likely be negotiable, of course), but the more important information here will be any upfront maintenance or improvement work that needs to be completed to ensure that the property can (or continue to) meet its income potential. While there may be no extra cost here for properties in good condition, it’s worth having the property inspected by a professional building inspector to ensure that there are no hidden issues or problems

- Financing Details: You’ll want to talk to your lender or mortgage broker to get an idea (or better yet a letter of approval) about the cost of the loan and the necessary down payment

- Income: Details about income should come directly from the seller, but as mentioned above, don’t rely on pro-forma data for final analysis. You can also talk to the property management company currently running the property (if there is one) to get this information

- Expenses: Similar to income, details about expenses should come directly from the seller (last warning not to trust pro-forma data!) or the property management company currently running the property. This is another place where a building inspector could help warn you about any major repairs that may be coming due in the near future (new roof, new heating/AC, etc)

As you continue exploring and evaluating possible real estate investments, this Quick Proforma tool might come in handy for your projections. And when you’re ready to make the jump into building your global real estate investment portfolio, check out my real estate crowdfunding platform, Durise.

Comments (2)

A lender I'm working with to acquire a residential portfolio of 3 condo units (commercial loan) asked for pro formas of each unit... is this something for the Seller to provide, or am I supposed to create these?

Blake Aaron, over 8 years ago

To save some of your own time, you can definitely ask the seller to provide these. If they want to sell the property enough, there is a chance that they have either already done the work, or are willing to do so. If they have not or will not, then you will have to do it yourself. But you'll still need all of the required data from the sellers either way.

Anthony Andrew Young, over 7 years ago