The Investor Mindset in the Age of Coronavirus: Strategies for Success

Due to the coronavirus pandemic, investors are currently operating in uncharted territory. Navigating this landscape can be fraught with new and unexpected obstacles.

In the second article of this three-part series, we’re examining the mindsets investors can take in approaching these challenges, discussing strategies to determine the best course of action, and sharing tactics for achieving success. Check out the rest of the series here:

- Part One:

- Part Three:

The market during this pandemic has been largely unpredictable, but there are some things we can count on when markets are unstable:

- People will begin selling assets , especially where they feel overextended.

- Because of this, credit starts drying up.

- Buyers are put into more conservative positions as credit markets shrink. Thus, fewer people are able to acquire assets because they have less capital.

- Those who still have access to capital are less willing to take a risk since they are now gambling with their own money.

- Less competition leads to falling prices as supply exceeds demand.

- People who are overextended and trying to sell will become desperate and drop their prices even more.

- This cycle can repeat often enough to reinforce the negative feedback loop and create a chain reaction that becomes uncontrollable.

Now that you’ve achieved some clarity in your mindset and how you approach investing, it’s time to plan how you’re going to thrive in this new environment.

Related: __

In a healthy market with freely available capital and steady demand, cash flow is king. It’s less important to sit on your mountain of cash than to actively grow it by seeking out new investment opportunities.

But currently, we are not in a healthy market, and thus…

Strategy #1: Cash Is King

If you want to come out of a crisis wealthier than you went in, you need to conserve your cash and wait for amazing opportunities.

Having money doesn’t mean you have to spend your money. If you aren’t finding great opportunities, keep your cash in the bank instead. The worst-case scenario is you break even, which is certainly better than losing your money if you get restless and dump it into a bad deal.

When markets go down, people’s behavior changes. Tenants may refuse to pay rent, government intervention can be unpredictable, and frivolous lawsuits may increase as people start seeing “opportunities.” The last thing you want in a situation like that is to overextend yourself on a bad—or even just OK—deal. Shore up your financial foundation to ensure you can survive any unforeseen setbacks instead.

The great thing about cash is it works in every scenario. If you guess wrong about what will happen during this crisis, cash is your leverage when true opportunities arise. In a crisis, the best way to minimize risk while simultaneously maximizing the ability to capitalize on opportunities is by conserving cash.

Strategy #2: Cash Flow Is Queen

Now that I’ve ranted about the importance of cash, let’s talk about cash flow.

The best way to conserve cash is to maintain cash flow.

One of the worst things that can happen during an economic downturn is your sources of cash flow dry up—whether from losing a job, vendors stopping payments, tenants withholding rent, or governments preventing evictions.

You can’t avoid spending money—you need it to buy food, keep the lights on, and any number of unavoidable situations. If order to have cash to spend, you need money coming in the door. Replacing non-paying renters will be difficult if there’s a shortage of demand (like there is now), so it’s crucial you protect what you have in place already, even if it means taking partial payments.

Related: __

Tip #1: Communicate

If you sit back and hope for the best, you’re allowing people to fill in the blanks themselves without taking your interests into account. You are the only person who cares about your cash flow, so establish an open line of communication early to support the people who are paying you.

Tip #2: Educate

Once you’ve begun the conversation, you can explain to your tenants the importance of continuing to pay their rent.

If your tenants are struggling financially, provide a solution to them by offering the option of temporary partial payments with the goal of catching up once the economy stabilizes. And explain to them that if too many payments are missed, they will be at risk of eviction once those are allowed to proceed again.

Practice humanity when dealing with your tenants. When times are good, it’s easy to mistakenly see them as an expendable resource. But they are not, and times are not good right now. Establish a personal relationship with them to make this situation easier to navigate. Let them know you’re compassionate and trustworthy.

Strategy #3: Protect Your Assets

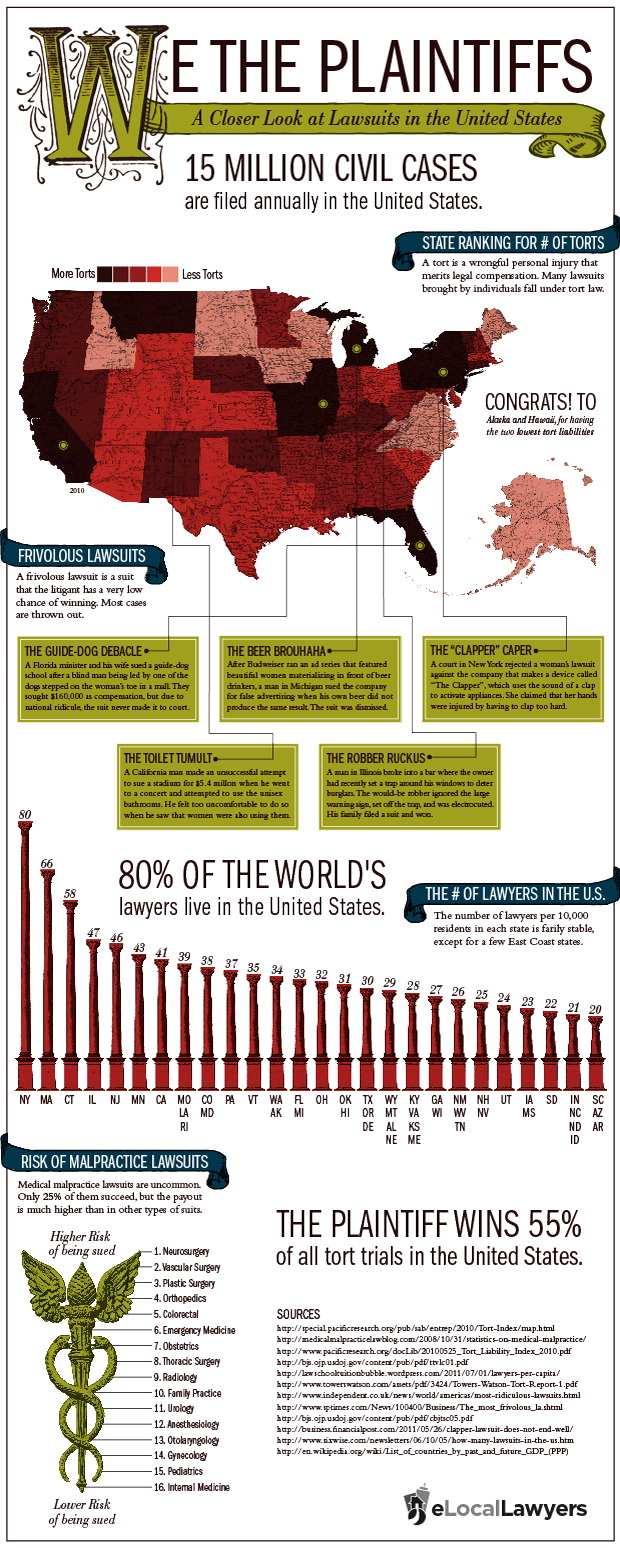

When the economy tanks, lawsuits start popping up. In fact:

- Over 80% of lawyers live in the United States.

- 15 million civil lawsuits are filed every year.

- Lawsuits can take anywhere from 6 months to over 3 years.

- 92% of lawsuits are .

- The , plus another $15K in legal fees.

- If you go to court and lose, the .

{kind=link}

Real estate investors are the most common target and face an 80% chance of being sued at some point in their lifetime. It’s not a matter of if you will get sued but when.

Advance preparation for lawsuits is your best protection, and the most valuable prep work you can do is asset protection.

5 Pillars of Asset Protection

There are five basic pillars to asset protection, each of which undermines the financial incentive of a lawsuit:

- Anonymity. There is a wealth of information about you available online—everything from your home value to your work history—if someone has your name and a general idea of where you live. Anonymity makes this information harder to track down and can demotivate a litigation attorney.

- Liability. Creating a limited liability company (LLC) draws a line between your personal wealth and your business wealth, thus protecting your family from financial ruin if your business is sued. It’s the perfect work/life balance.

- Separation. Shell companies can act as decoys in lawsuits, as well. It can conduct day-to-day operations while holding nothing of any value. Contract language in a lease can require tenants to sue the shell company, which grants them access to none of your financial holdings.

- Isolation. Rather than creating multiple LLCs and managing them individually, a more robust entity like a Series LLC or Delaware Statutory Trust (DST) allows you to scale infinitely while providing better levels of protection for each individual asset.

- Insurance. Most importantly, insure yourself. Don’t put your full faith in an insurance company to protect you. After all, they’re a for-profit corporation themselves—but they are a key part of your protection strategy.

With these in place, the likelihood of being successfully sued is nearly zero. You have removed any financial incentive for doing so and thus protected your assets from being taken.

Related: Can I (and Should I) Move My Property Into an LLC and Out of My Name?

Strategy #4: Protect Your Family

Most of us don’t want to think about themselves or their family getting sick or—God forbid—dying. Planning for this is exceedingly important during a pandemic, though.

Estate planning isn’t a sexy topic. In fact, it’s quite boring. But it’s of vital importance for your family’s survival if anything happens. Your parents and your children need to know what is in place, documents should be up to date, and everyone should know who to contact for estate matters if anything were to happen.

You have everything to lose if you fail to plan your estate.

5 Components of an Estate Plan

Your estate plan needs to have the following in it:

- Living Trust. This will give your family or trustee the ability to bypass probate court and gain direct control of assets upon your death.

- Pour-Over Will. Anything not mentioned specifically in your living trust will automatically be “poured over” into it and distributed as dictated in the trust.

- Health Care Power of Attorney. If you end up incapacitated in the hospital, this gives you advance decision-making for what should happen regarding your level of care.

- Durable Power of Attorney. The DPOA will redirect financial decisions to another if you are incapacitated. I recommend allowing a limited scope here to prevent anyone from being “too helpful” with your finances.

- HIPAA Authorization. This is necessary in conjunction with a medical power of attorney so your decision-maker can be fully informed of your medical status.

Having these five pieces of an estate plan in place can provide you with peace of mind during a very difficult time.

In our third and final installment of this series, we’ll show how the mindsets and strategies you’ve established can be put into action for financial success.

Questions? Comments?

Let’s talk in the comment section below.