Real Estate News Roundup: Foreclosures Low, Delinquencies Up; Frenzied Homebuying Persists

A roundup of news and information from around the web about real estate, personal finance, and the economy.

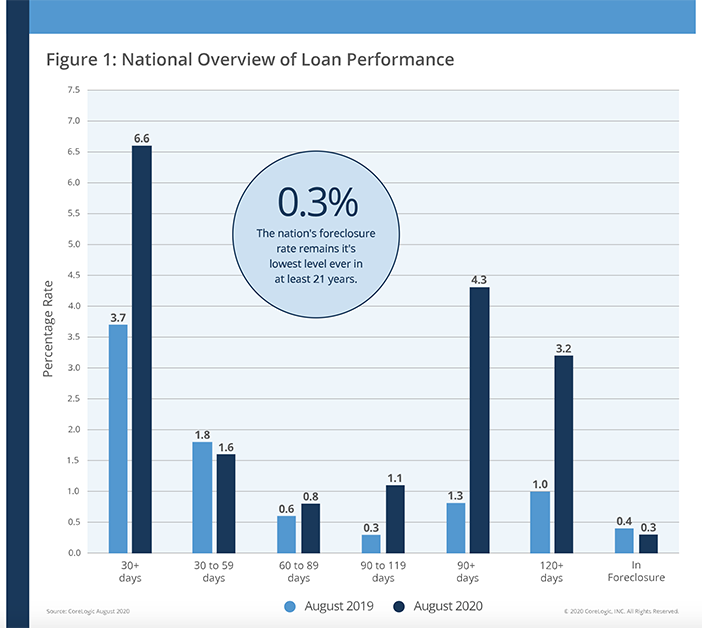

Holding Steady: Foreclosures Remain Low While Serious Delinquencies Continue to Build Up

CoreLogic, a leading global property information, analytics, and data-enabled solutions provider, released its monthly Loan Performance Insights Report for August 2020. On a national level, 6.6% of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure). This represents a 2.9-percentage point increase in the overall delinquency rate compared to August 2019, when it was 3.7%. To gain an accurate view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency, including the share that transitions from current to 30 days past due. In August 2020, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.6%, down from 1.8% in August 2019, and down from 4.2% in April when early-stage delinquencies spiked.

- Adverse Delinquency (60 to 89 days past due): 0.8%, up from 0.6% in August 2019, but down from 1% in July and from 2.8% in May.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 4.3%, up from 1.3% in August 2019. This is the highest serious delinquency rate since February 2014.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, down from 0.4% in August 2019. The August 2020 foreclosure rate is the lowest since at least January 1999.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.9%, up from 0.8% in August 2019. The transition rate has slowed since April 2020, when it peaked at 3.4%.

[caption id="attachment_132056" align="alignnone" width="702"]  Source: CoreLogic, Inc._ Homeowners nearing the end of the first 180-day grace period (afforded to borrowers with federally backed mortgages) can request an extension of an additional 180 days, which is keeping foreclosure rates low while serious delinquency continues to climb. However, back-mortgage payments continue to add up for those unable to exit forbearance periods early. Looming unpaid mortgage payments, paired with sharp declines in income for many families, point to a potential wave of home sales triggered by financial distress in 2021 as forbearance periods end. Read the rest of the report here.

Source: CoreLogic, Inc._ Homeowners nearing the end of the first 180-day grace period (afforded to borrowers with federally backed mortgages) can request an extension of an additional 180 days, which is keeping foreclosure rates low while serious delinquency continues to climb. However, back-mortgage payments continue to add up for those unable to exit forbearance periods early. Looming unpaid mortgage payments, paired with sharp declines in income for many families, point to a potential wave of home sales triggered by financial distress in 2021 as forbearance periods end. Read the rest of the report here.

Intense Buyer Demand Continues to Drive Hot Housing Market

Intense and persistent buyer demand is keeping the time on market for houses at incredible lows and pushing prices ever higher above 2019, according to . Sales remain high above last year and are expected to stay robust in the coming months.  Time on market still short as pending sales stay high over 2019

Time on market still short as pending sales stay high over 2019

- Robust buyer-side demand persisted through October. For the fourth consecutive week, houses are typically staying on the market for 12 days, a full 17 days faster than last year.

- Pending sales are up 19.7% year over year, though they have slowed 3.1% since last month and 1.3% since last week.

Related: __ Scalding homebuyer demand keeps inventory in a vise-grip

- Available inventory fell for the 23rd straight week and is now down 37.4% compared to last year. Demand for homes is still sky high, while current homeowners cite a lack of confidence in their ability to secure and afford a new home among .

- New listings dropped 7.4% year over year and 7.9% since last week.

Price growth over 2019 increases as hot market stretches further into fall

- Median list prices have risen further above last year's figures every week since early May and are now up 11.8% year over year. List prices fell $500 since last week to $345,500—the first weekly drop since mid-April.

- Homeowners who decide to sell are benefitting from insatiable demand. Median sale prices rose to $289,625 in the week ending September 19, up 12.5% over 2019.

Find out more .