-

All Forum Categories

-

Followed Discussions

-

Followed Categories

-

Followed People

-

Followed Locations

-

Market News & Data

-

General Info

-

Real Estate Strategies

- House Hacking

- Commercial Real Estate Investing

- BRRRR - Buy, Rehab, Rent, Refinance, Repeat

- Innovative Strategies

- Mobile Home Park Investing

- Land & New Construction

- Multi-Family and Apartment Investing

- Wholesaling

- Rehabbing & House Flipping

-

Short-Term & Vacation Rental Discussions

presented by

- Tax Liens & Mortgage Notes

- Medium-Term Rentals

- Buying & Selling Small Businesses

- Outdoor Hospitality

-

Landlording & Rental Properties

-

Real Estate Professionals

-

Financial, Tax, & Legal

-

Real Estate Classifieds

-

Reviews & Feedback

Velocity Banking / HELOC Checking Acct - It Works (Proof)

Hi, everyone. I wish everyone knew how great this strategy is, so I'm trying to spread the word. I'm not selling anything, just trying to let people know how it works.

When you're paying your mortgage month in and month out, you are paying MOSTLY interest for many years. That's because you are paying interest on the whole loan - $200K @ 4%, let's say. In the first year you'll only bring the balance down about $4K, but you'll pay about $8.5K in interest - twice as much, obviously. To pay the balance down $10K it will take you 2.5 years and over $20K in interest. To me, that's a sickening waste. Check out from Sept to Sept on this pic. Only $4K in principal yet $8.5K in interest. Work it out on bankrate yourself (link at bottom) and you can see how long and how much interest is wasted to pay off $10K from your mortgage. And this should go without saying, but if you're further along in your mortgage then your savings will be less, because you are paying less in interest at that point. This strategy is more suited to someone who is in their first decade of a mortgage.

Now, follow me here. You can take all of your extra money and put it toward your mortgage which will shorten your mortgage and save you on interest. Most people know this. But most people also realize that money is usually tight and many people don't have $400 for an emergency let alone a bunch of extra money to put against their mortgage. Anyway, do that if you want, but there's also another better way to accomplish the same thing.

Here's how it works. You get a HELOC or a PLOC with a reasonable rate. It doesn't have to be 4%, but it also shouldn't be 18% like a credit card. You take a portion of your mortgage ($5-10K, for example) and put it on the HELOC. Then you put all of your income toward the HELOC and try to depress the balance as much as possible all month. When bills come you use HELOC funds to pay them, because you're not putting your income into a checking account anymore. You continue like this, putting all bills and income toward the HELOC balance. Since you make more than you spend, the balance will gradually come down. Then you put another portion of your mortgage on the HELOC and repeat the process.

Here's how and why it works (and works better than just paying extra principal when you have the money):

1. You are putting all of your available "checking" funds toward your mortgage at all times, yet you still have money to pay bills due to the revolving credit line.

2. Money that you DON'T end up using toward bills stays on the mortgage balance permanently, limiting the amount of interest you will pay.

3. Money that you DO end up using toward bills temporarily "leans" on the mortgage balance keeping it down and limiting the amount of interest you will pay.

4. Here's the silver bullet, though, that most people can't fully grasp. On the above mentioned $200K / 4% loan you will pay $144K in interest over 30 years paying by the amortization schedule. For that amount, you might as well have purchased an extra smaller house. But here's the thing - the interest is SCHEDULED, but hasn't been CHARGED TO YOU YET. If you struggle with this idea, imagine that you won the lottery tomorrow and wanted to pay the house off. You'd pay off the balance of your mortgage, but not the balance and all the scheduled interest charges. In other words, the interest can be AVOIDED COMPLETELY by paying the principal back early, but time is of the essence. The more you pay and the faster you do it the better. So, remember above when I explained that it takes a person about $20K in interest to pay down $10K in principal? Well, when you put that $10K on the HELOC, you COMPLETELY AVOID the $20K in corresponding interest payments on the mortgage (like the lottery example, just a smaller amount) and it will cost you about $1000 in interest to pay off on the HELOC. This allows you to save TENS OR HUNDREDS OF THOUSANDS OF DOLLARS simply by adjusting the way you pay it. It's not a scam or a method of gaming the interest rates or anything like that, it's simply a way of paying more efficiently without having thousands of dollars lying around to throw at your mortgage.

5. When you pay these large chunks, your subsequent REGULAR PAYMENTS are also more effective, because your principal / interest ratio is improved by quite a lot. Normally, every month you will pay $1-$2 less toward interest than the previous month, but the month after you take $10K off of the mortgage your regular payment will charge about $30 less toward interest than the previous month - and every month thereafter. So, you are saving all the interest from #4 as explained, but every month you're also paying significantly less toward interest (and more toward principal) than you were before. Each time you take another "chunk" off of the mortgage your regular payments also become that much more efficient.

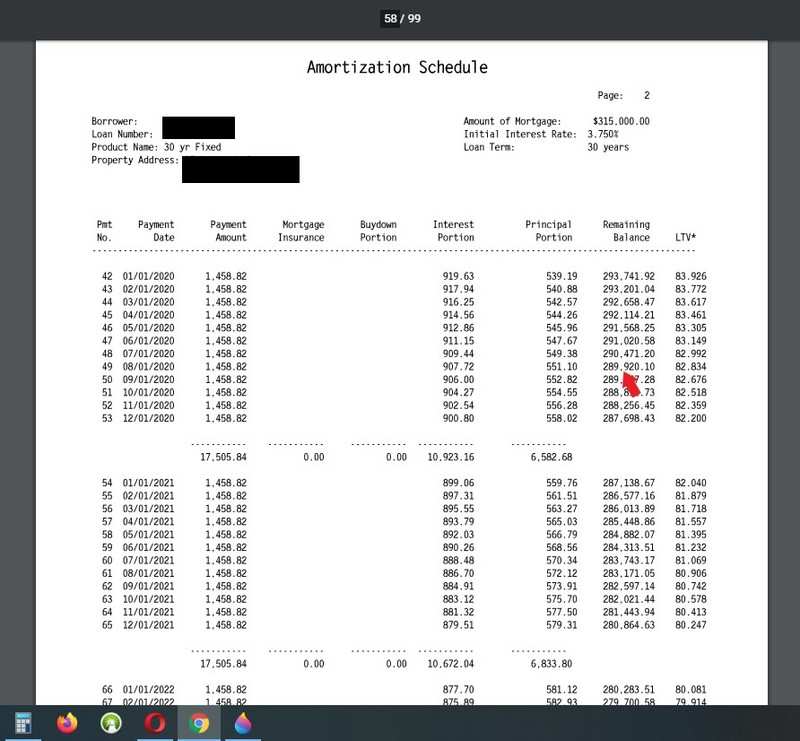

Hopefully, that covers the explanation, but I told you there was proof, so here you go. Here's my closing package where it says that this month I should be at a balance of about $290K.

And here's my actual loan balance of $236.5K. So, as you can see I've been able to put $53.5K extra toward my mortgage over the last two years (started the strategy May 2018) and I haven't been skipping lattes or doing any other financial voodoo. All I have done is started using the HELOC to pay off chunks of the mortgage like I explained and because of all the various mechanisms I described I've been able to put a ton of extra money toward the mortgage. When I look at the balances of $290K and $236K on my closing doc, I find that it is about 85 regular payments (7 years) shaved off the mortgage at an average of $825 interest per month (first payment in range $907 / last payment in range $743). 85 payments at an average of $825/month is $70K worth of interest savings in only two years. Obviously, I have a higher dollar mortgage, so your results may vary, but this isn't milk money, it's life changing money simply from rearranging the way you pay your number one expense. Let me know if you have any thoughts or questions. Thanks!

Joshua, I get what your doing man. This debate is hilarious especially when mortgage brokers or hacks get on and can't see the advantage and flexibility Lines of Credit allow you if you are responsible and know what your doing. Replace that **** with a HELOC in the first Lien position and be done with the mortgage ( it confuses people obviously but also it will simplify what your doing altogether). If your like most homeowners you should be able to take advantage of a higher LTV right now that will provide you with a higher credit line tied to this property for years to come and it will help if you do want to pick up other assets like cheap rentals or whatever you prefer coming up soon. Promo rates can be as low as .99 for 6 - 24 months with no closing costs and if you still have this HELOC in two years refi again doing the same thing as most banks don't charge back application / appraisal / closing costs or have early prepayment penalties after the two year period anyway. Plug it in through bankrates calculators and run it compared to the amortized mortgage ******** that bankers blindly push on people because that is what they have been trained to do. See what you think. Numbers don't lie and in todays world I don't know any investor given the choice who would want there money tied up in a mortgage with this as a viable alternative to have liquid damn cash. Even Cash out refi's don't give you the flexibility of the HELOC because you don't have to use it if you don't need it and therefore save on not having as much interest costs when paying installments to contractors or bills of any sort while still getting tax advantages, pay for down payments or cut outright cash deals for ANYTHING. You don't pay commission fees, capital gains or other ******** taxes on good debt and that is nice especially if someone else could be paying it down for you.

Hypothetically 400k home @ 85% LTV provides new HELOC of 340k. If your mortgage and existing LOC was 230k or whatever it is just pay those off with this new first lien Heloc of 340k. You will have 110k now to do whatever you want and just push your cash flow through new HELOC in first position just like you were doing before because now there is no need to throw chunks at a mortgage. Less risk that it gets frozen first of all if or when things go south again. Numbers work way better especially with promo interest rates because interest savings during that period adds up to thousands in addition to what you will already be saving. Of course it shouldn't need to be mentioned but the more expendable cash flow you have going through this the better and the faster you can pay this down or off and utilize the HELOC in any other way people can think of. Flexibility is unmatched with no downside as if interest rates ever start getting out of hand you can still lock in portions to be amortized or the whole thing if you want to so don't let that scare nobody either. Hope this helps Josh

Here's a quick update for my ninjas. I've been using this strategy for 3 years now and I'm already at the point where I'm paying more to principal than to interest. That typically takes about 13 years.

You might say so what, you're just dipping into your savings or skipping avocado toast and this is a hoax and fake news, but I can assure you I'm just doing the strategy. I actually took about $3000 out of savings recently to put toward the house, but soon realized that that was sort of "cheating" the system and decided not to do it again. Anyway, that was only $3000 out of about $40K put toward principal, so as far as cheating goes that's a pretty lame attempt. Everything else is simply using the HELOC like a checking account and you can see how much it's accelerated my mortgage.

I also refinanced to a lower rate, but didn't cash out equity or anything, just wanted a lower rate.

Original balance $315K June 2016.

Started this strategy May 2018.

Current balance $197K May 2021.

Savings still intact.

But I'm sure it's all a bunch of lies and stuff, which is why I'm posting my statements trying to help people. 🤣

Lmk if you have any questions or anything. ❤️

PS - In case anyone thinks that I'm distorting the mortgage balance by putting part of it on another vehicle or that I'm able to do this because I'm getting a better rate somewhere else.

Oh noes I've got a whole $7K to pay off on the HELOC and I'm paying over 8% on it. That amounted to under a thousand dollars last year and $45 so far this year. That really negates the thousands and thousands of dollars I'm saving on mortgage interest and makes me regret using this strategy to pay my mortgage down $115K in 3 years. I hope you can pick up on the sarcasm, because I'm doing it as hard as I can. 👍

Way to go in reducing the principal balance of your primary residence. Over these past few years how much has your net worth grown? How has your overall portfolio been enlarged?

I personally have a couple of 10.5 interest loans on properties that I am not paying off early, because I am earning so much more by being an active investor and I getting a lot better that 10.5% . I can assure you I’m not trying to argue with you , because I have seen that it’s Impossible to win an argument with you. LOL

Originally posted by @Joe S.:Way to go in reducing the principal balance of your primary residence. Over these past few years how much has your net worth grown? How has your overall portfolio been enlarged?

I personally have a couple of 10.5 interest loans on properties that I am not paying off early, because I am earning so much more by being an active investor and I getting a lot better that 10.5% . I can assure you I’m not trying to argue with you , because I have seen that it’s Impossible to win an argument with you. LOL

Thanks. My net worth has grown exponentially, but that's beside the point. This is the problem with everyone's thinking. Correct me if I'm wrong, but you're basically saying that I'm putting all my extra money into my mortgage, therefore I'm not using it to earn elsewhere, but that makes no sense.

I have savings, stocks, and rentals just like you. I have all the earning power that you do with your money PLUS I have my checking account funds earning because I'm using them to bring my mortgage down and save on interest. So, if I'm understanding you correctly, where is my missed opportunity if I have all the same vehicles you have going PLUS another one keeping all my money working for me?

Please, anyone that can explain this, I'm so curious.

You: Savings, stocks, rentals, etc. and money rotting away in your checking account.

Me: Savings, stocks, rentals, etc. and money in my checking account earning 4% bringing my mortgage balance down.

How is this a missed opportunity for me? Someone let me know. 🙂

Originally posted by @Joe Erdmann:Joshua, I get what your doing man. This debate is hilarious especially when mortgage brokers or hacks get on and can't see the advantage and flexibility Lines of Credit allow you if you are responsible and know what your doing. Replace that **** with a HELOC in the first Lien position and be done with the mortgage ( it confuses people obviously but also it will simplify what your doing altogether). If your like most homeowners you should be able to take advantage of a higher LTV right now that will provide you with a higher credit line tied to this property for years to come and it will help if you do want to pick up other assets like cheap rentals or whatever you prefer coming up soon. Promo rates can be as low as .99 for 6 - 24 months with no closing costs and if you still have this HELOC in two years refi again doing the same thing as most banks don't charge back application / appraisal / closing costs or have early prepayment penalties after the two year period anyway. Plug it in through bankrates calculators and run it compared to the amortized mortgage ******** that bankers blindly push on people because that is what they have been trained to do. See what you think. Numbers don't lie and in todays world I don't know any investor given the choice who would want there money tied up in a mortgage with this as a viable alternative to have liquid damn cash. Even Cash out refi's don't give you the flexibility of the HELOC because you don't have to use it if you don't need it and therefore save on not having as much interest costs when paying installments to contractors or bills of any sort while still getting tax advantages, pay for down payments or cut outright cash deals for ANYTHING. You don't pay commission fees, capital gains or other ******** taxes on good debt and that is nice especially if someone else could be paying it down for you.

Hypothetically 400k home @ 85% LTV provides new HELOC of 340k. If your mortgage and existing LOC was 230k or whatever it is just pay those off with this new first lien Heloc of 340k. You will have 110k now to do whatever you want and just push your cash flow through new HELOC in first position just like you were doing before because now there is no need to throw chunks at a mortgage. Less risk that it gets frozen first of all if or when things go south again. Numbers work way better especially with promo interest rates because interest savings during that period adds up to thousands in addition to what you will already be saving. Of course it shouldn't need to be mentioned but the more expendable cash flow you have going through this the better and the faster you can pay this down or off and utilize the HELOC in any other way people can think of. Flexibility is unmatched with no downside as if interest rates ever start getting out of hand you can still lock in portions to be amortized or the whole thing if you want to so don't let that scare nobody either. Hope this helps Josh

I missed this post previously. I appreciate what you're saying, but I don't like the idea of exposing my whole loan to a variable rate, plus first lien HELOCs are harder to get. I'm doing the same thing with "chunks" of my mortgage and I'm happy with that. If I ever run into a snag and want to stop using this strategy, I can just pay off the HELOC and go back to normal. Thanks, though.

Just wanted to give a quick update for anyone that might be interested.

My original post on this thread was around August of 2020 and I had paid my mortgage down to about $236K (should have been at $289K according to my amortization table, so obviously I was already way ahead). See original post for details.

Today, in December of 2021 my mortgage stands at $190K, so I've paid down an additional $46K in around 16 months.

Once again for anyone with a short attention span or reading comprehensive issues - I'm doing this by simply using a different way to pay, NOT liquidating my savings, stocks, properties, or receiving some sort of inheritance or any other voodoo. It's money that comes from my checking account.

Here's a screen shot to show my balance.

Anyone that's not using this strategy is leaving a lot of money on the table and staying in debt on their house way longer than necessary.

PS - According to previous commenters, mortgage debt is "good debt" and therefore shouldn't be paid down more quickly. That's incorrect. Mortgage debt is good debt COMPARED TO OTHER KINDS OF DEBT. There's nothing inherently "good" about being in debt if you are interested in cash flow. Debt hinders cash flow. And yes, I understand leverage, but what other people don't understand is that you borrow to purchase a house and then essentially have to pay it back one and a half times. You have to pay the principal back and also owe about 50% of the principal on interest. That's if you have a really good rate. How much leverage are you really getting if you are forced to pay 50% more for your house and be in debt for the rest of your life? Just sayin'.

Just to be crystal clear with everyone:

I bought my house in July of 2016 for $350K, the mortgage was $315K.

I started this strategy in May of 2018.

December of 2021 my balance is $190K.

I'm building equity very quickly and I have not touched my savings, stock investments, sold properties, received a lump sum from the lottery or inheritance or anything. I'm simply using a smarter way to pay and the money comes out of my checking / spending funds.

Later!

Originally posted by @Joshua S.:Just to be crystal clear with everyone:

I bought my house in July of 2016 for $350K, the mortgage was $315K.

I started this strategy in May of 2018.

December of 2021 my balance is $190K.

I'm building equity very quickly and I have not touched my savings, stock investments, sold properties, received a lump sum from the lottery or inheritance or anything. I'm simply using a smarter way to pay and the money comes out of my checking / spending funds.

Later!

Are you buying investment rentals at the same time? It looks like you had a little under 3% interest on your loan. That’s pretty low interest.

Originally posted by @Joe S.:Originally posted by @Joshua S.:Just to be crystal clear with everyone:

I bought my house in July of 2016 for $350K, the mortgage was $315K.

I started this strategy in May of 2018.

December of 2021 my balance is $190K.

I'm building equity very quickly and I have not touched my savings, stock investments, sold properties, received a lump sum from the lottery or inheritance or anything. I'm simply using a smarter way to pay and the money comes out of my checking / spending funds.

Later!

Are you buying investment rentals at the same time? It looks like you had a little under 3% interest on your loan. That’s pretty low interest.

No, but I will at some point if / when housing prices come down. Or we've also been exploring moving to a district with a better high school for the kids in a few years and turning the current place into a rental. Paying the balance down on it also gives me the flexibility to refi to a lower payment, which will help with cash flow if we decide to rent it.

Either way, if your real question is whether or not I can "afford" to buy another rental with this strategy going on the answer is yes. I could budget for saving toward a rental just like I budget for groceries. This strategy works independently and regardless of any other goals a person might have. It's simply a better way to pay.

Originally posted by @Joshua S.:Originally posted by @Joe S.:Originally posted by @Joshua S.:Just to be crystal clear with everyone:

I bought my house in July of 2016 for $350K, the mortgage was $315K.

I started this strategy in May of 2018.

December of 2021 my balance is $190K.

I'm building equity very quickly and I have not touched my savings, stock investments, sold properties, received a lump sum from the lottery or inheritance or anything. I'm simply using a smarter way to pay and the money comes out of my checking / spending funds.

Later!

Are you buying investment rentals at the same time? It looks like you had a little under 3% interest on your loan. That’s pretty low interest.

No, but I will at some point if / when housing prices come down. Or we've also been exploring moving to a district with a better high school for the kids in a few years and turning the current place into a rental. Paying the balance down on it also gives me the flexibility to refi to a lower payment, which will help with cash flow if we decide to rent it.

Either way, if your real question is whether or not I can "afford" to buy another rental with this strategy going on the answer is yes. I could budget for saving toward a rental just like I budget for groceries. This strategy works independently and regardless of any other goals a person might have. It's simply a better way to pay.

Glad it’s working out for you.

Originally posted by @Joe S.:Originally posted by @Joshua S.:Originally posted by @Joe S.:Originally posted by @Joshua S.:Just to be crystal clear with everyone:

I bought my house in July of 2016 for $350K, the mortgage was $315K.

I started this strategy in May of 2018.

December of 2021 my balance is $190K.

I'm building equity very quickly and I have not touched my savings, stock investments, sold properties, received a lump sum from the lottery or inheritance or anything. I'm simply using a smarter way to pay and the money comes out of my checking / spending funds.

Later!

Are you buying investment rentals at the same time? It looks like you had a little under 3% interest on your loan. That’s pretty low interest.

No, but I will at some point if / when housing prices come down. Or we've also been exploring moving to a district with a better high school for the kids in a few years and turning the current place into a rental. Paying the balance down on it also gives me the flexibility to refi to a lower payment, which will help with cash flow if we decide to rent it.

Either way, if your real question is whether or not I can "afford" to buy another rental with this strategy going on the answer is yes. I could budget for saving toward a rental just like I budget for groceries. This strategy works independently and regardless of any other goals a person might have. It's simply a better way to pay.

Glad it’s working out for you.

Thanks!

One-word: Re-cast.

Just want to add my two cents since I took the time to read through this entire post. I am 100% writing this post assuming that the intent of the article was to pay off your home quicker and "save" interest on primary residence. I think that's been made clear by Josh. This is/was not a time-value-of-money (TVM) article.

A few things:

1st: Paying extra towards the mortgage doesn't change the amortization (read: interest) schedule for a FIXED-rate loan. You still pay heavier interest payments due up front. Period. Paying extra towards principle just "shortens" your loan on the back end 30 years from now. (In Josh's example it would shorten from August 2050 to whatever you're paying down. But NOT payments due tomorrow. That's still the "heavy" interest payment.) So the interest you're "saving" is actually on a lower principle amount, at the END of the loan. (This is what I think all the mortgage experts had a hard time conveying in earlier posts.) The amortization schedule would, however, change if you were to refinance. Except one thing...

2nd: Refinancing isn't free (usually, unless your broker factors it into the rate they're giving you and then it's definitely not "free"). The cost of multiple refinances would eat into your strategy. Not to mention that fixed rates are going up from what they were a year ago. And it's only going to get "worse". (4% ain't a bad mortgage man, it's not 2.5% but not bad at all).

3rd: Paying off your primary residence eliminates any tax savings, however little, you would get from being a "home-owner". (this used to be a good perk, not so much since 2018. This has recently been causing a lot of people to go towards renting (no equity/wealth building, but more advantageous financially in the short run according to recent articles.) I also understand that HELOC interest is NOT tax deductible as it once was. (At least not until 2025 or whenever they change the rules.) So you're paying for the full interest amount on a higher rate without the tax savings. (Can a CPA fact check me on that, please?) I don't believe any of the posts above addressed this.

However:

Most states, including the District of Columbia, allow you to re-cast your mortgage for free or a small, negligible amount (usually $250). You can only recast a loan once a year and requires at least 10k of additional principle payment, since inception or the last recast. This strategy would actually capture the "savings" you are trying to achieve. The way it's being described above seems less advantageous (higher HELOC interest rate, cost of refinance, and loss of (miniscule) tax savings). This will lower your UP-FRONT interest amounts as it re-amortizes the the loan in it's ENTIRETY.

Conclusion:

If you pay more towards principle - then RE-CAST your mortgage periodically. Otherwise, you probably aren't saving what you're think you're saving. However, you are paying your home off faster, and for those that don't like debt and want peace of mind/SWAN, that's worth all the money in the world to them. Just know, if you're every liable for anything, whomever is coming after you doesn't have to deal with the 1st lien-holder anymore and having a fully paid off home, is just ripe for the taking. /shrug

Also, with inflation the way it's going, it may be silly to not keep debt on the books. Given how much money the Fed just printed, we're going to laughing at our mortgage payments in 5-10 years given how low they are. I'm not smart enough to explain that part, but just know it matters.

Disclaimer: I am not a financial professional and this is not financial advice. This is purely my opinion. Do your own research.

@Joshua S. Hey, what are the heloc terms? I have been thinking of doing this to have the available funds if I wanted to buy more property. But Iam not thinking I can use my heloc as a checking account because for every withdraw they charge me a min of $100, or 1.5% whichever is greater. Maybe I have the wrong kind? We are super cash poor but have 3properties, this may help my situation. What do you think? They also do allow me to lock in a balance at 5% APR. Do I just have a weird Heloc?

Originally posted by @Rahul So:One-word: Re-cast.

Just want to add my two cents since I took the time to read through this entire post. I am 100% writing this post assuming that the intent of the article was to pay off your home quicker and "save" interest on primary residence. I think that's been made clear by Josh. This is/was not a time-value-of-money (TVM) article.

A few things:

1st: Paying extra towards the mortgage doesn't change the amortization (read: interest) schedule for a FIXED-rate loan. You still pay heavier interest payments due up front. Period. Paying extra towards principle just "shortens" your loan on the back end 30 years from now. (In Josh's example it would shorten from August 2050 to whatever you're paying down. But NOT payments due tomorrow. That's still the "heavy" interest payment.) So the interest you're "saving" is actually on a lower principle amount, at the END of the loan. (This is what I think all the mortgage experts had a hard time conveying in earlier posts.) The amortization schedule would, however, change if you were to refinance. Except one thing...

2nd: Refinancing isn't free (usually, unless your broker factors it into the rate they're giving you and then it's definitely not "free"). The cost of multiple refinances would eat into your strategy. Not to mention that fixed rates are going up from what they were a year ago. And it's only going to get "worse". (4% ain't a bad mortgage man, it's not 2.5% but not bad at all).

3rd: Paying off your primary residence eliminates any tax savings, however little, you would get from being a "home-owner". (this used to be a good perk, not so much since 2018. This has recently been causing a lot of people to go towards renting (no equity/wealth building, but more advantageous financially in the short run according to recent articles.) I also understand that HELOC interest is NOT tax deductible as it once was. (At least not until 2025 or whenever they change the rules.) So you're paying for the full interest amount on a higher rate without the tax savings. (Can a CPA fact check me on that, please?) I don't believe any of the posts above addressed this.

However:

Most states, including the District of Columbia, allow you to re-cast your mortgage for free or a small, negligible amount (usually $250). You can only recast a loan once a year and requires at least 10k of additional principle payment, since inception or the last recast. This strategy would actually capture the "savings" you are trying to achieve. The way it's being described above seems less advantageous (higher HELOC interest rate, cost of refinance, and loss of (miniscule) tax savings). This will lower your UP-FRONT interest amounts as it re-amortizes the the loan in it's ENTIRETY.

Conclusion:

If you pay more towards principle - then RE-CAST your mortgage periodically. Otherwise, you probably aren't saving what you're think you're saving. However, you are paying your home off faster, and for those that don't like debt and want peace of mind/SWAN, that's worth all the money in the world to them. Just know, if you're every liable for anything, whomever is coming after you doesn't have to deal with the 1st lien-holder anymore and having a fully paid off home, is just ripe for the taking. /shrugAlso, with inflation the way it's going, it may be silly to not keep debt on the books. Given how much money the Fed just printed, we're going to laughing at our mortgage payments in 5-10 years given how low they are. I'm not smart enough to explain that part, but just know it matters.

Disclaimer: I am not a financial professional and this is not financial advice. This is purely my opinion. Do your own research.

Thanks for the reply, but unfortunately you're incorrect about a couple things.

First of all, a recast will save you money monthly if you are just paying the minimum payment, but it simply stretches your principal over a longer period of time and doesn't affect your interest at all. If you recast (lower your monthly principal amount) and then just put in more principal next month like I'm doing then it's pointless for the purpose of paying off faster. I have recasted to lower my monthly burden in case of a job loss or something, but it doesn't allow you to pay off quicker, which is my goal.

Second, you're incorrect about where the savings come from when paying extra principal and there's a real easy way to show you.

Pull up bankrate's amortization calculator for me. Click on show amortization table. Take note of the total amount of interest at the top - $136K and the interest portions of the last 24 payments. It's a range of $3 to $72, which is an average of $37.50.

In your theory, if you shave off two years of the mortgage by paying extra principal you'll have a savings of $900 ($37.50 x 24 months) at the back end of the mortgage in 28 years, so let's put that to the test.

Click on where it says add additional payments and put $5500 into the one time payment box and click calculate. You'll notice that it takes two years off of the mortgage, but the total interest goes from $136K to $121K for a savings of about $15,000. That's a lot more than $900.

That's because when you pay additional principal you are skipping over the next $5500 worth of principal payments and the corresponding interest you would have paid over that time.

So, let's test that claim. Add up the next 24 payments after that lump $5500 payment. It's an average of $586.50, so multiplied by 24 it comes out to $14,076. I think it comes shy of the $15K savings because you're also essentially re-amortizing the loan and the payments are a little less, but obviously $14K is way closer to $15K than $900 is.

See what I mean? The explanation CAN'T BE that you're simply shaving interest off the back end of the loan, because the savings would be pathetic. Obviously, you should test this on other amortization calculators, but the last couple years worth of interest payments will never match up with the savings on the calculator, because that's not where the savings are coming from. Hope this helps.

Quote from @Evelyn Tilman:

@Joshua S. Hey, what are the heloc terms? I have been thinking of doing this to have the available funds if I wanted to buy more property. But Iam not thinking I can use my heloc as a checking account because for every withdraw they charge me a min of $100, or 1.5% whichever is greater. Maybe I have the wrong kind? We are super cash poor but have 3properties, this may help my situation. What do you think? They also do allow me to lock in a balance at 5% APR. Do I just have a weird Heloc?

Yes, I think you have a weird HELOC. I am just charged x amount of interest on my HELOC depending on what I have out at the time. I have a couple of them with rates between 4-8%, but the thing is that in this strategy the rate doesn't matter. What matters is that you're using otherwise dead money that's sitting in your checking or savings account to keep downward pressure on your mortgage. Using a HELOC to buy other properties is fine, but it doesn't really have anything to do with this strategy. Thanks.

This thread got really long due to some factors:

Different goals. Most investors at the time of their writing had low interest rates so their goal was to continue to acquire more mortgaged properties. OP (original poster) also does that but additionally wants to have properties paid off.

Lack of clarity. OP's strategy of velocity banking actually works, but he did not make it clear enough. Velocity banking works because the HELOC or PLOC (Personal Line of Credit) takes time to accrue interest following his withdrawal to pay mortgage early. Before it accrues OP pays back the HELOC with next income. So he's paying his mortgage faster while not paying interest on the HELOC. For this reason it does not matter if the HELOC has a higher rate than the mortgage. Rinse and repeat. OP is winning on both ends.

@joshua I see how the strategy can work, but nobody reading this thread likes you because of your horrible attitude. Also when I saw you got a 2.99% from Rocket Mortgage I knew you were a sucker. Rates that end in 9 are always scammy in how they rob you of hundreds of dollars compared to if you got a 3% flat. But you are exactly the type of person a loan officer would of sold a 2.99% to. With how fast you are paying off your mortgage because of your amazing strategy it doesn't even matter. And guess what you don't even need to be sad about that $500 you wasted on a 2.99 because you are saving so much money! Is your attitude always like this? Everyone on this thread you argue with. Regardless if you are right or wrong it was hard for me to read. So much negativity. I did not help with this and rant over. I wish you more happiness in your life sir.

- Lender

- The Woodlands, TX

Quote from @Carl B.:Not correct. Whether interest accrues or is paid immediately, it is the same amount of expense and no effect on PROFITABILITY. Velocity banking doesn’t work anywhere near like its proponents believe; they’re merely accounting for the amount of additional investment they add from their other income to pay down their credit line incorrectly. The bottom line is that there is a very small positive financial gain resulting from utilizing this method. But, if it results in a”forced savings” of money that would otherwise be spent, I guess that can be considered a success.

This thread got really long due to some factors:

Different goals. Most investors at the time of their writing had low interest rates so their goal was to continue to acquire more mortgaged properties. OP (original poster) also does that but additionally wants to have properties paid off.

Lack of clarity. OP's strategy of velocity banking actually works, but he did not make it clear enough. Velocity banking works because the HELOC or PLOC (Personal Line of Credit) takes time to accrue interest following his withdrawal to pay mortgage early. Before it accrues OP pays back the HELOC with next income. So he's paying his mortgage faster while not paying interest on the HELOC. For this reason it does not matter if the HELOC has a higher rate than the mortgage. Rinse and repeat. OP is winning on both ends.

Quote from @Jacob Trogan:

Also when I saw you got a 2.99% from Rocket Mortgage I knew you were a sucker. Rates that end in 9 are always scammy in how they rob you of hundreds of dollars compared to if you got a 3% flat. But you are exactly the type of person a loan officer would of sold a 2.99% to. With how fast you are paying off your mortgage because of your amazing strategy it doesn't even matter. And guess what you don't even need to be sad about that $500 you wasted on a 2.99 because you are saving so much money!

This confused me. But I am not a lender, so hopefully you can help me understand because I do borrow from time to time.

Are you saying that there is something intrinsically scammy about rates that end in 9 and that a 2.99 rate is inherently worse than a flat 3.0 rate? Why? Is there something about the closing cost of the loan that you are referencing here? Maybe points charged? I dont get it.

And are you saying that there are loan officers that look for people who seek innovative strategies that may differ from the tried and true, and when they find them, are more likely to offer this scammy rate? Why? I truly dont understand.

Quote from @Roger Flot:

Quote from @Jacob Trogan:

Also when I saw you got a 2.99% from Rocket Mortgage I knew you were a sucker. Rates that end in 9 are always scammy in how they rob you of hundreds of dollars compared to if you got a 3% flat. But you are exactly the type of person a loan officer would of sold a 2.99% to. With how fast you are paying off your mortgage because of your amazing strategy it doesn't even matter. And guess what you don't even need to be sad about that $500 you wasted on a 2.99 because you are saving so much money!

This confused me. But I am not a lender, so hopefully you can help me understand because I do borrow from time to time.

Are you saying that there is something intrinsically scammy about rates that end in 9 and that a 2.99 rate is inherently worse than a flat 3.0 rate? Why? Is there something about the closing cost of the loan that you are referencing here? Maybe points charged? I dont get it.

And are you saying that there are loan officers that look for people who seek innovative strategies that may differ from the tried and true, and when they find them, are more likely to offer this scammy rate? Why? I truly dont understand.

I am overly sarcastic over text a lot of the times. I was implying about the type of person the original poster is. Yes never get a 2.99% instead of a 3% flat or nowadays a 6.99% instead of a 7% flat.

If you look at the savings in interest over 30 years for .01% it is very small. It may be like $200 but what happens is the mortgage company will charge some higher origination charge of $500-600 for that rate.

so you are paying $500+ to save $250 over 30 years. So not a good deal. This is a very nuanced thing. I would be happy to defend this math to any loan officer who has sold a client a rate ending in .99. It is a promotional gimmick.

So to reiterate someone who wanted the bragging rights of having a 2.99% instead of 3% is the same type of person who would argue with every comment in this thread to prove they are right. It is a comment about the nature of the person nothing more. Velocity banking can work in some ways but it’s not as great as many who preach it say it is.

Most things in finance are very nuanced.

Quote from @Jacob Trogan:

Quote from @Roger Flot:

Quote from @Jacob Trogan:

Also when I saw you got a 2.99% from Rocket Mortgage I knew you were a sucker. Rates that end in 9 are always scammy in how they rob you of hundreds of dollars compared to if you got a 3% flat. But you are exactly the type of person a loan officer would of sold a 2.99% to. With how fast you are paying off your mortgage because of your amazing strategy it doesn't even matter. And guess what you don't even need to be sad about that $500 you wasted on a 2.99 because you are saving so much money!

This confused me. But I am not a lender, so hopefully you can help me understand because I do borrow from time to time.

Are you saying that there is something intrinsically scammy about rates that end in 9 and that a 2.99 rate is inherently worse than a flat 3.0 rate? Why? Is there something about the closing cost of the loan that you are referencing here? Maybe points charged? I dont get it.

And are you saying that there are loan officers that look for people who seek innovative strategies that may differ from the tried and true, and when they find them, are more likely to offer this scammy rate? Why? I truly dont understand.

I am overly sarcastic over text a lot of the times. I was implying about the type of person the original poster is. Yes never get a 2.99% instead of a 3% flat or nowadays a 6.99% instead of a 7% flat.

If you look at the savings in interest over 30 years for .01% it is very small. It may be like $200 but what happens is the mortgage company will charge some higher origination charge of $500-600 for that rate.

so you are paying $500+ to save $250 over 30 years. So not a good deal. This is a very nuanced thing. I would be happy to defend this math to any loan officer who has sold a client a rate ending in .99. It is a promotional gimmick.So to reiterate someone who wanted the bragging rights of having a 2.99% instead of 3% is the same type of person who would argue with every comment in this thread to prove they are right. It is a comment about the nature of the person nothing more. Velocity banking can work in some ways but it’s not as great as many who preach it say it is.

Most things in finance are very nuanced.

Thanks for replying. I "get" the sarcasm angle.

I just wanted to verify if there was something inherent to the 9 in the rate. Figured there was a closing costs backdoor angle.

Quote from @Joshua S.:

Hi, everyone. I wish everyone knew how great this strategy is, so I'm trying to spread the word. I'm not selling anything, just trying to let people know how it works.

When you're paying your mortgage month in and month out, you are paying MOSTLY interest for many years. That's because you are paying interest on the whole loan - $200K @ 4%, let's say. In the first year you'll only bring the balance down about $4K, but you'll pay about $8.5K in interest - twice as much, obviously. To pay the balance down $10K it will take you 2.5 years and over $20K in interest. To me, that's a sickening waste. Check out from Sept to Sept on this pic. Only $4K in principal yet $8.5K in interest. Work it out on bankrate yourself (link at bottom) and you can see how long and how much interest is wasted to pay off $10K from your mortgage. And this should go without saying, but if you're further along in your mortgage then your savings will be less, because you are paying less in interest at that point. This strategy is more suited to someone who is in their first decade of a mortgage.

Now, follow me here. You can take all of your extra money and put it toward your mortgage which will shorten your mortgage and save you on interest. Most people know this. But most people also realize that money is usually tight and many people don't have $400 for an emergency let alone a bunch of extra money to put against their mortgage. Anyway, do that if you want, but there's also another better way to accomplish the same thing.

Here's how it works. You get a HELOC or a PLOC with a reasonable rate. It doesn't have to be 4%, but it also shouldn't be 18% like a credit card. You take a portion of your mortgage ($5-10K, for example) and put it on the HELOC. Then you put all of your income toward the HELOC and try to depress the balance as much as possible all month. When bills come you use HELOC funds to pay them, because you're not putting your income into a checking account anymore. You continue like this, putting all bills and income toward the HELOC balance. Since you make more than you spend, the balance will gradually come down. Then you put another portion of your mortgage on the HELOC and repeat the process.

Here's how and why it works (and works better than just paying extra principal when you have the money):

1. You are putting all of your available "checking" funds toward your mortgage at all times, yet you still have money to pay bills due to the revolving credit line.

2. Money that you DON'T end up using toward bills stays on the mortgage balance permanently, limiting the amount of interest you will pay.

3. Money that you DO end up using toward bills temporarily "leans" on the mortgage balance keeping it down and limiting the amount of interest you will pay.

4. Here's the silver bullet, though, that most people can't fully grasp. On the above mentioned $200K / 4% loan you will pay $144K in interest over 30 years paying by the amortization schedule. For that amount, you might as well have purchased an extra smaller house. But here's the thing - the interest is SCHEDULED, but hasn't been CHARGED TO YOU YET. If you struggle with this idea, imagine that you won the lottery tomorrow and wanted to pay the house off. You'd pay off the balance of your mortgage, but not the balance and all the scheduled interest charges. In other words, the interest can be AVOIDED COMPLETELY by paying the principal back early, but time is of the essence. The more you pay and the faster you do it the better. So, remember above when I explained that it takes a person about $20K in interest to pay down $10K in principal? Well, when you put that $10K on the HELOC, you COMPLETELY AVOID the $20K in corresponding interest payments on the mortgage (like the lottery example, just a smaller amount) and it will cost you about $1000 in interest to pay off on the HELOC. This allows you to save TENS OR HUNDREDS OF THOUSANDS OF DOLLARS simply by adjusting the way you pay it. It's not a scam or a method of gaming the interest rates or anything like that, it's simply a way of paying more efficiently without having thousands of dollars lying around to throw at your mortgage.

5. When you pay these large chunks, your subsequent REGULAR PAYMENTS are also more effective, because your principal / interest ratio is improved by quite a lot. Normally, every month you will pay $1-$2 less toward interest than the previous month, but the month after you take $10K off of the mortgage your regular payment will charge about $30 less toward interest than the previous month - and every month thereafter. So, you are saving all the interest from #4 as explained, but every month you're also paying significantly less toward interest (and more toward principal) than you were before. Each time you take another "chunk" off of the mortgage your regular payments also become that much more efficient.

Hopefully, that covers the explanation, but I told you there was proof, so here you go. Here's my closing package where it says that this month I should be at a balance of about $290K.

And here's my actual loan balance of $236.5K. So, as you can see I've been able to put $53.5K extra toward my mortgage over the last two years (started the strategy May 2018) and I haven't been skipping lattes or doing any other financial voodoo. All I have done is started using the HELOC to pay off chunks of the mortgage like I explained and because of all the various mechanisms I described I've been able to put a ton of extra money toward the mortgage. When I look at the balances of $290K and $236K on my closing doc, I find that it is about 85 regular payments (7 years) shaved off the mortgage at an average of $825 interest per month (first payment in range $907 / last payment in range $743). 85 payments at an average of $825/month is $70K worth of interest savings in only two years. Obviously, I have a higher dollar mortgage, so your results may vary, but this isn't milk money, it's life changing money simply from rearranging the way you pay your number one expense. Let me know if you have any thoughts or questions. Thanks!

I've been confused on how this works. I read this whole post and you convinced me to try this. You broke it down (several times) so that I can understand it. I'm paying off 2 large loans within a year or so and as soon as I do pay them off (for peace of mind), I'm going to try this. I hope I can find a HELOC like yours that you just pay interest and now extra yearly fees or withdrawal fees. Thanks for breaking it down and sharing your story!

@Joshua S., I love this strategy as well! I teach the strategy and helped to build the First Lien HELOC at the bank I'm with. It works in coordination with a checking account with a bi-directional sweep so there's no manual transfer of funds necessary. Let me know if you'd like to connect!!